imaginima

Investment Thesis

Sprott Inc. (NYSE:SII) is a Canadian investment company, focused on the precious metals and uranium industries. I have covered the stock many times in the past few years, those articles can be found here. The company has a listing in both the U.S. and Canada.

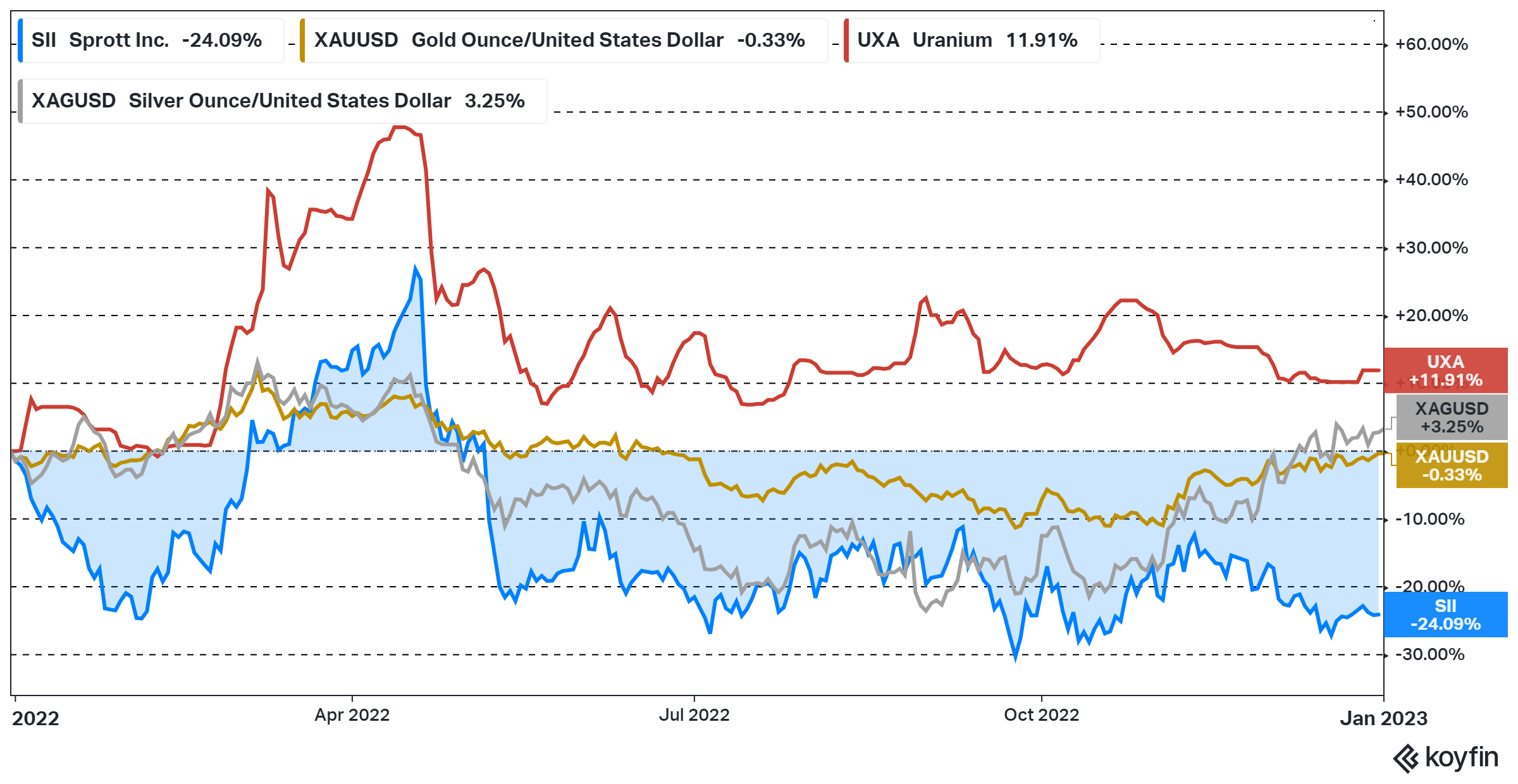

Assets Under Management is by my calculations almost at a peak level in Q4-22, up around 14% from Q4-22, but the stock price has declined by as much as 24% during 2022. Even if the sentiment has been relatively poor for miners during the year, most producers have still fared better than this without the impressive AUM growth we have seen for Sprott. So, it has led to an excellent opportunity for investors, and I have continued to add to the stock over the last couple of months.

Figure 1 – Koyfin

Exchange Listed Products Segment

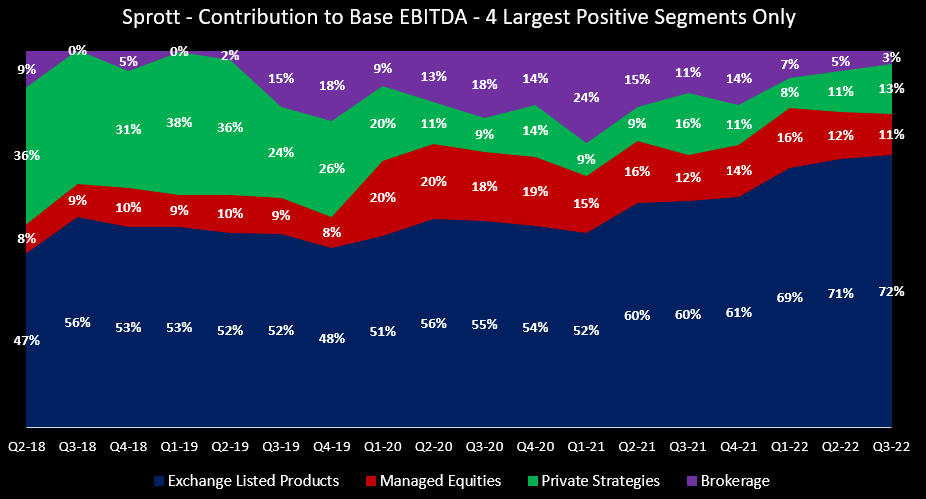

The exchange listed product segment has become increasingly important to Sprott over time, due to new mandates being added, and very healthy inflows to the exchange listed products.

Figure 2 – Quarterly Reports

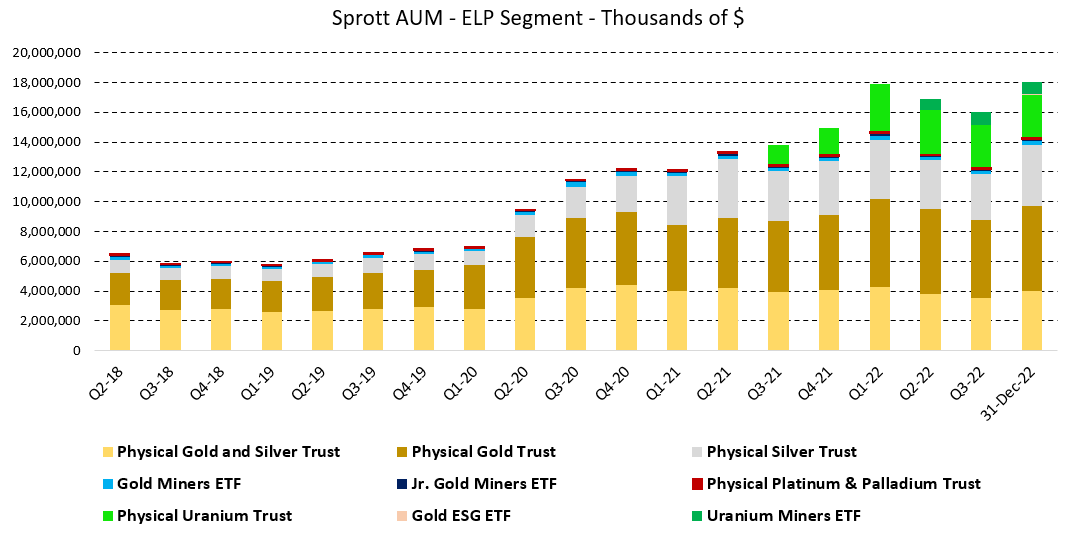

The segment is comprised of 9 different trusts and ETFs, where the physical trusts account for most of the AUM and effectively all the AUM growth in the segment during 2022.

Figure 3 – Data from Quarterly Reports & Sprott.com

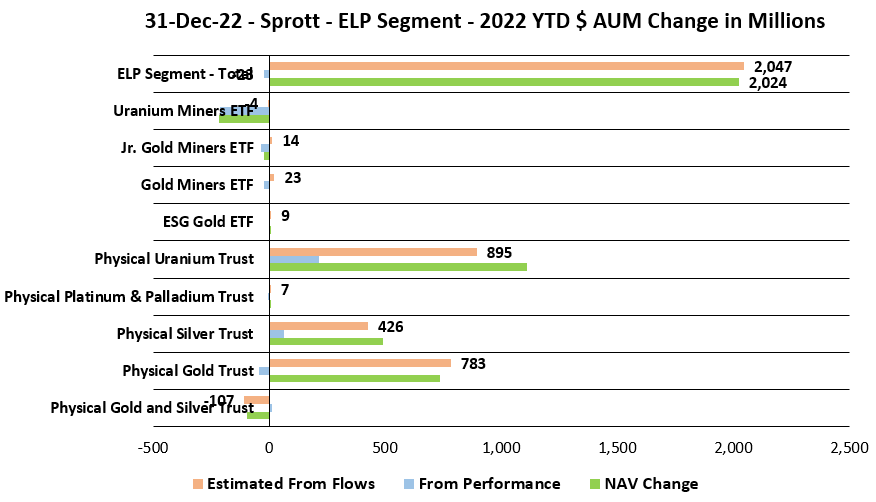

The Uranium Trust has been a very important source of growth over the last 18 months and that trust saw about $900M of inflows during 2022, which is impressive when we consider that 2022 was not a very bullish year for uranium equities in general.

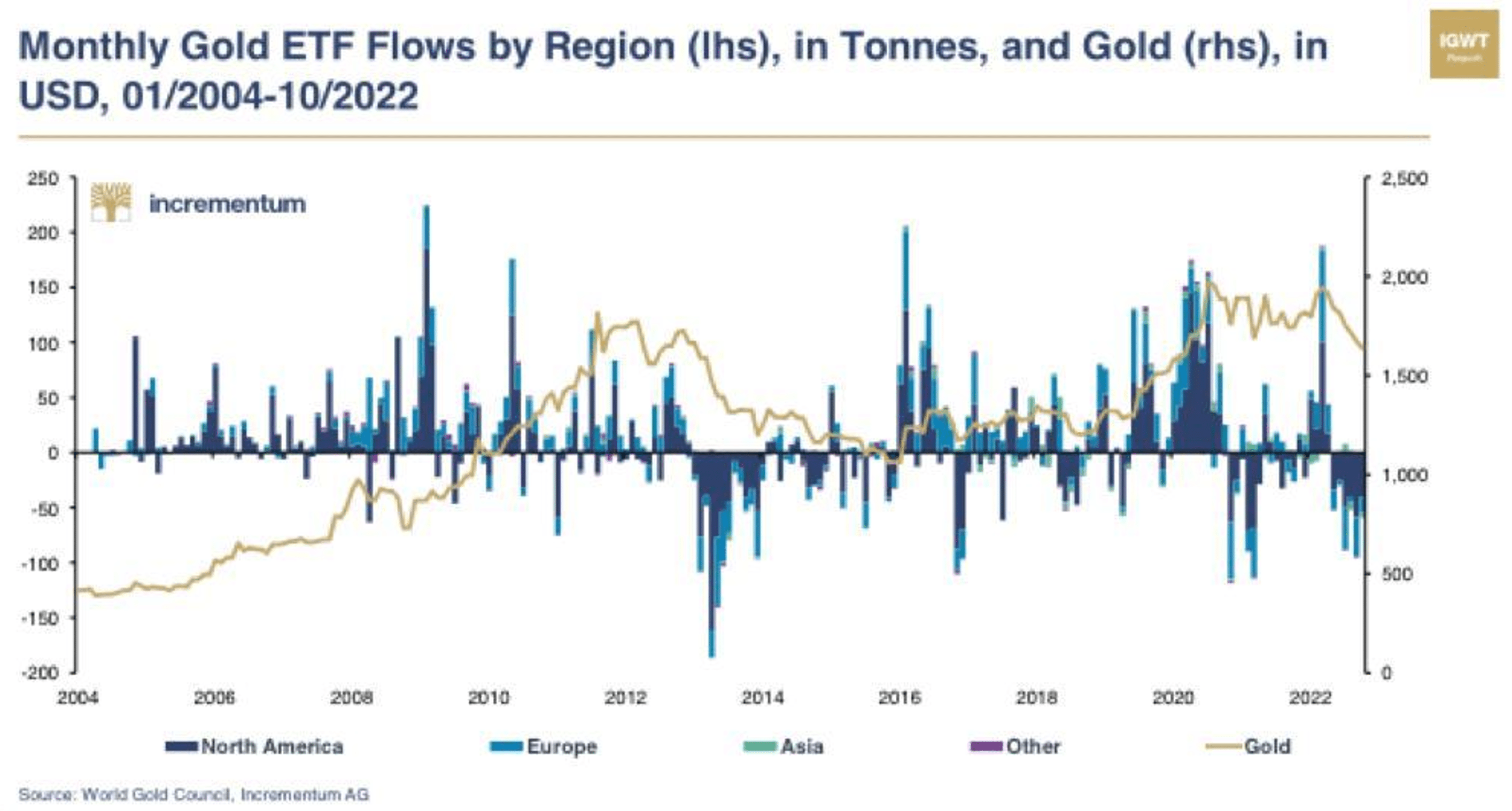

We also continue to see very sizable inflows to the Gold Trust and the Silver Trust. The combined inflows in those two trusts were slightly more than $1.3B, which is also a very impressive figure when we consider that many other precious metals backed trusts or ETFs saw outflows during 2022.

Figure 4 – Data from Sprott.com

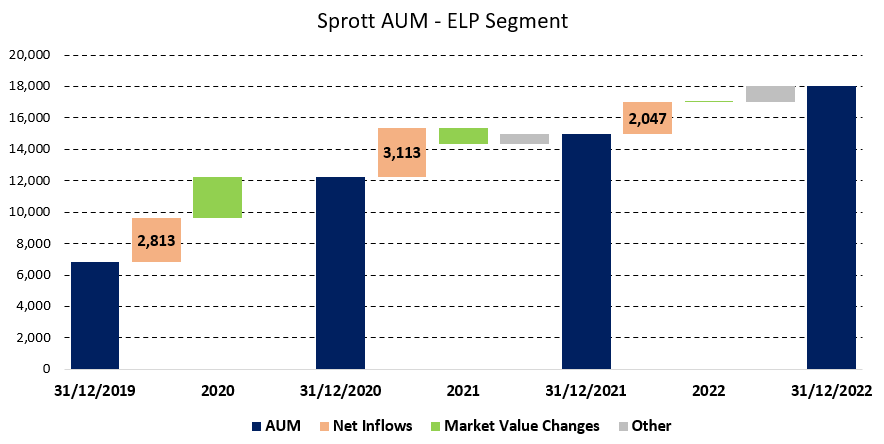

The below chart illustrates how impressive and instrumental these inflows have been over the last few years in growing AUM in this segment and for Sprott as a whole. Having had strong inflows in 2021 and 2022 when the performance has been lackluster is a great competitive advantage. Sprott has spent a long time building brand recognition and trust, which is now to the company’s benefit.

Figure 5 – Data from Quarterly Reports & Sprott.com Figure 6 – In Gold We Trust Report

Total AUM & Other Segments

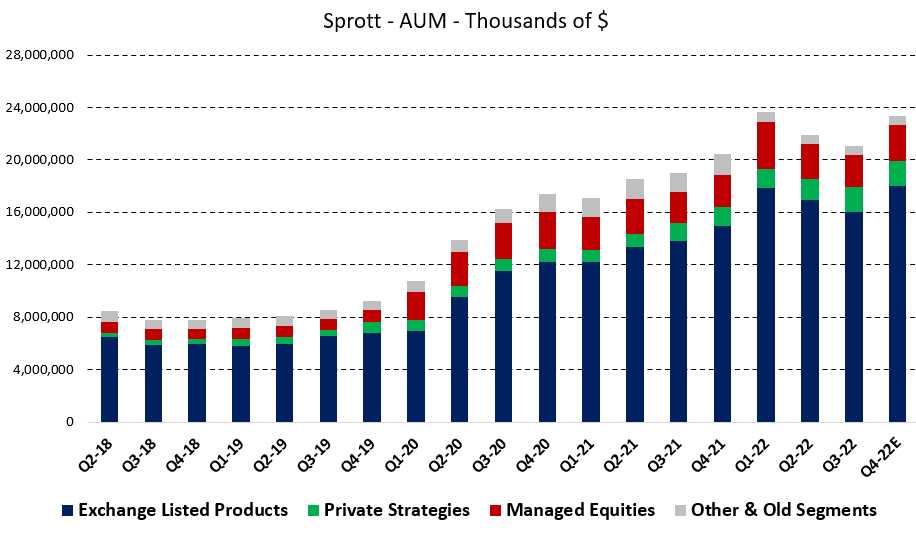

The below chart illustrates the company’s AUM growth over the last few years and my estimates for Q4-22. There should be little ambiguity about the exchange listed product segment in Q4-22, as those figures are available on Sprott’s homepage.

I have conservatively assumed no growth in the private strategy and other segments from Q3-22. The managed equity segment is assumed to have seen 15% growth during Q4-22, based on what the largest fund in that segment has done, and precious metals equities in general. That means total AUM will in Q4-22 be somewhere around $23.4B, almost at the $23.7B peak we saw in Q1-22.

Figure 7 – Quarterly Reports & My Estimates

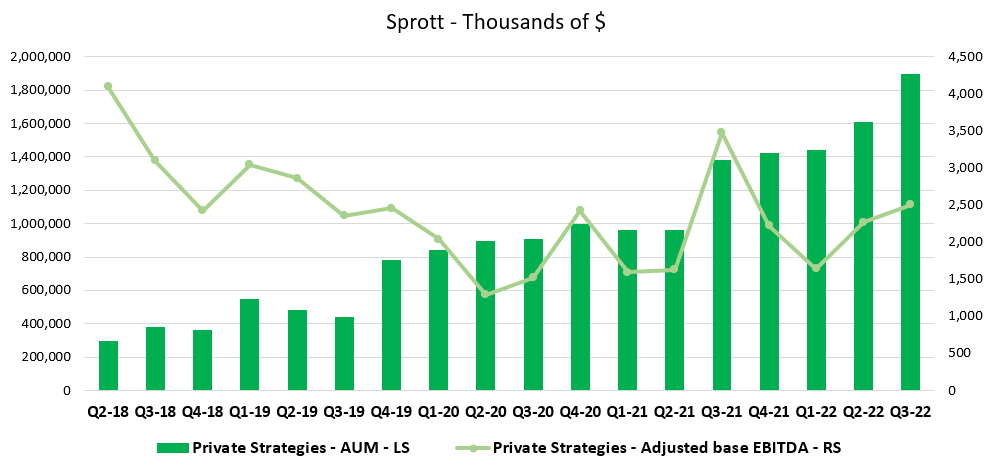

We have lately started to see both AUM and earnings growth in the private strategies segment, which is primarily lending & streaming mandates. The expectation would be for that segment to continue to grow slowly.

Figure 8 – Quarterly Reports

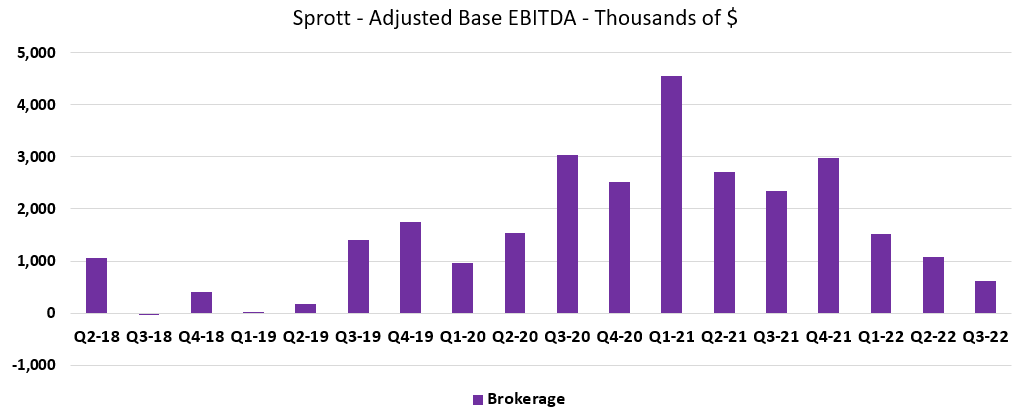

Given the recovery we have seen in metal prices and to some extent miners, I do think we will start to see the brokerage segment make more of a contribution again. The segment has as of late seen little activity due to the very poor sentiment.

Figure 9 – Quarterly Reports

Valuation & Conclusion

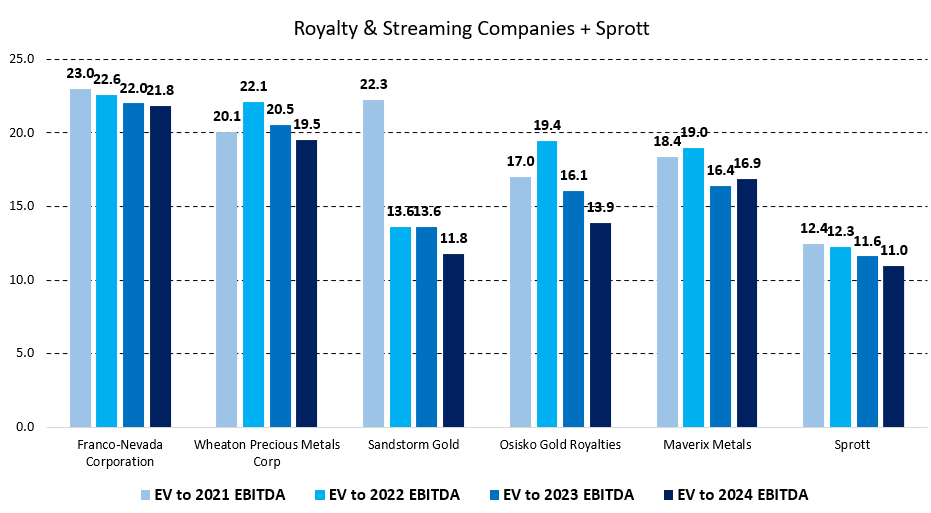

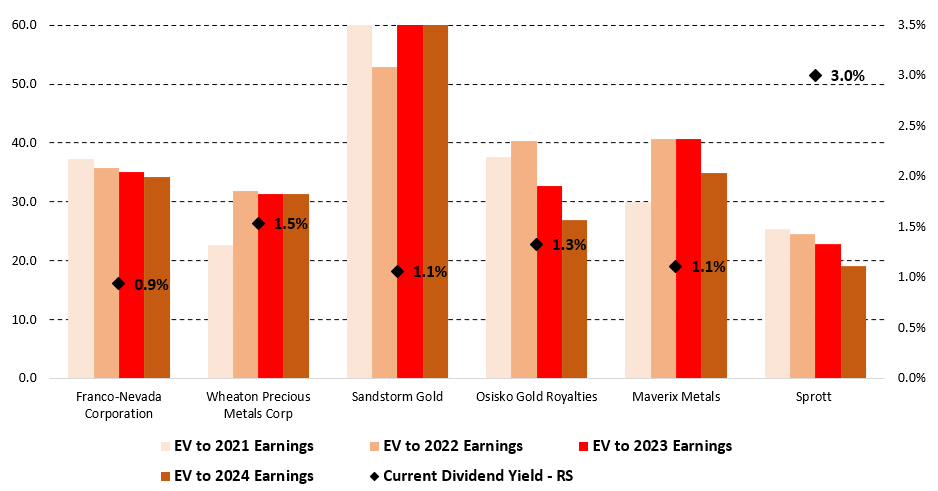

Sprott is currently trading with a forward EV to EBITDA around 11-12 and a forward EV to Earnings in the 19-23 range, which is well below most royalty & streaming companies that I view to have similar risk profiles.

Figure 10 – Estimates from Koyfin Figure 11 – Estimates from Koyfin

I have mentioned it in the past and continue to think the 2023 estimates are somewhat conservative, which I view to be even more true based on how much AUM has recovered lately. The stock also pays a dividend yield of 3.0% with a quarterly distribution.

The exchange listed products and private strategies segments have good long-term growth prospects. The brokerage segment and some balance sheet co-investments Sprott has are likely to pick up once the sentiment improves. The recovery in Q4-22 is hopefully an indication of a brighter future even as Sprott has managed to grow during the last couple of turbulent years as well.

Be the first to comment