Avid Photographer. Travel the world to capture moments and beautiful photos. Sony Alpha User

Thesis

There is a clear difference between a good business model, a good service or product, and a good price to purchase a stock. They can be complimentary, but not interchangeable, when determining if a stock is a good buy. I think most would agree Spotify provides a good service. They offer a fair subscription that unlocks access to a wide-breadth media selection. This is accompanied by a sleek and user-friendly interface, and most importantly, a personalized experience. However, since its inception, Spotify has been scrutinized regarding their business model, and whether it will be profitable or not. And because of this, their stock has dropped immensely, to a point where the current price is compelling.

As it stands, the negative sentiment towards Spotify is largely oversaturated because of misses on profit margin expectations from recent earnings. The stock is now priced at a level where it could operate at razor thin margins, lower than management’s expectations, for the next ten years and still yield a great return, so long revenue growth holds true. Any slight increases to profit margins, through the many solutions they have, could spell even bigger returns for investors, providing massive upside.

Minimal Leverage

The root cause of Spotify’s profitability issues could be summed up in two words: Minimal Leverage.

While better than it used to be, Spotify still struggles to have leverage over anyone, primarily because of three reasons:

- The Big Three Record Labels, Warner, Universal, and Sony, still own the majority of content, thus having monopoly-like pricing power over Spotify.

- Apple has monopoly-like pricing power over Spotify, since they collect thirty percent of services and products the app produces.

- Competition with Tidal, Google, Amazon, YouTube Music, Pandora and other media outlets drives subscription prices down.

Spotify realized this issue and plans to attack it by three different solutions:

- Invest heavily in personal content, or ways to maximize more profitable content, to help leverage over the Big Three.

- Invest in a personalized experience, to help leverage over competition, ultimately leading to inelastic pricing changes, thus profit.

- Negotiations between The Big Three and Apple, along with other general cost cutting tactics that most business would use.

Maximizing Profitable Content

As mentioned, Spotify needs to gain leverage over the Big Three, to increase profits. One way they can do this is by producing or owning their own content. This is similar to when Netflix included Netflix Original Series. Two modes of new content include the wave of podcast acquisitions Spotify made the last couple years, along with audiobooks. The premise is that owning these modes of content are far more profitable and incorporating them in their operations would help boost profitability. The following remarks from Ek on the 2022 Investor Day help explain this:

- “And while the podcast vertical is still largely in investment mode and not yet profitable, we believe it has a 40-50% gross margin potential.”

- “While it’s still early, we expect audiobooks to also have healthy margins, above 40% and be highly accretive to the business.”

Maximizing Personalized Experience

The second way Spotify can increase profits is by maximizing a personal experience, so users are loyal to their service. One of the first ways Spotify tackled this is by offering a free, add revenue, service for customers. Although, only making up around 10% of their revenue, and ultimately losing money internally in the beginning, this service was paramount in attracting first time customers. Eventually, customers fell in love with the product and converted to the paid subscription version, which was much more profitable.

Furthermore, Spotify invested heavily in machine learning to create personalized playlists based on hours of data points, logged by the customer. Some examples include Discover Weekly, Daily Mixes, and Radar. At first it can be a little difficult to conceptualize how this can be profitable, but let’s set the stage:

- You are a huge Taylor Swift fan and Spotify realizes this by the ten hours you logged last week listening to her music. Spotify’s software will then create a personalized playlist, consisting of many Taylor swift songs, but also a variety of lesser-known names and artists, similar in genre and sound. It can be inferred that lesser-known artists are more profitable, since their license is cheaper. If you get hooked on the playlist, the following week, you listen to ten hours of a more profitable playlist. As you discover lesser-known names, you keep the ball of profitably rolling for Spotify. And if you are like me, someone who loves to discover new music, this system plays you like a puppet.

What is so powerful about this machine learning is it provides an opportunity for Spotify to promote unknown, profitable, artist. Conversely, they also have the power to suppress certain artists, due to profitability, or other moral and ethical reasons.

This now leads for more opportunities for unknown musicians to make it big, and they are paying Spotify for it. Ek views Spotify as a two-sided marketplace, where they gain revenue from listeners and from artists looking to make it big. In fact, labels are now paying Spotify for inclusions in playlists and more money for higher ranking in the playlists. In this instance, Spotify’s personalized experience leads to leverage over the record labels.

Another feature Spotify added that has helped boom the personalized experience is the Spotify Wrapped Tour or Yearly Recap. In this recap, Spotify collects all the data it gathered from the user and displays it in the form of charts, lists, top artists and then tells a story about the year. This was originally a fun little addition for users to recap the year, but it has now turned into a very sought-after feature, with the ability to share on social media platforms. I can say from experience, it is very fun to post on your Instagram Story, share with friends, and have a discussion about your results. It is such a powerful feature, that Apple has included it in their Apple Music platform, but it doesn’t really hold the same social value as Spotify, since Apple lagged behind and Spotify’s wrapped tour is more popular. In fact, I personally remember seeing comments from users saying they are switching to Spotify, just so they have the ability to join in on the Spotify Wrapped Tour fun. What turned out to be a very silly feature, is pressuring users to fit the norm.

Other Profitably Options

The third way Spotify can help profits are perhaps more “boring” solutions, yet they will be important for the future.

As Spotify creates the optimal personal experience, and retain sticky customers, they have the ability to raise subscription charges, inelastically. They have done a great job becoming a customer-centric platform, so switching costs seem high for the customer. Many users don’t want to lose their custom playlists, Spotify wrapped, daily mixes, and other playlists specifically generated for the user. Furthermore, they have already learned to navigate the sleek user interface. As long as they don’t go overboard on pricing, I would not think minor price changes would push the customer over the edge.

Another option is continued backlash towards Apple for App store costs. Apple has continued to make Spotify’s access to customers extremely difficult as, previously mentioned, they collect thirty percent of services and products the app produces. Recently, Spotify feuded with Apple over the inclusion of audiobooks in the in-app store. It’s no surprise Apple would push back on this effort, since Apple music is one of Spotify’s competitors. But as the tech giants start to push back on Apple, it will be interesting to see if Apple is put in a position to lower app costs.

Furthermore, I have included some other subset profitability options:

- Laying off employees and transitioning to a work from home policy, reducing building space and total overhead.

- Stronger price negotiation with record labels.

- General economies of scale.

Valuation

We mentioned before that there is a distinct difference between a good product or service, a good business model, and a good price. In the valuation segment, our aim is to determine if Spotify is at a good price based on two different approaches. First, a Discounted Cash Flow (“DCF” analysis”) with several scenarios. Second, a multiples approach.

Discounted Cash Flow

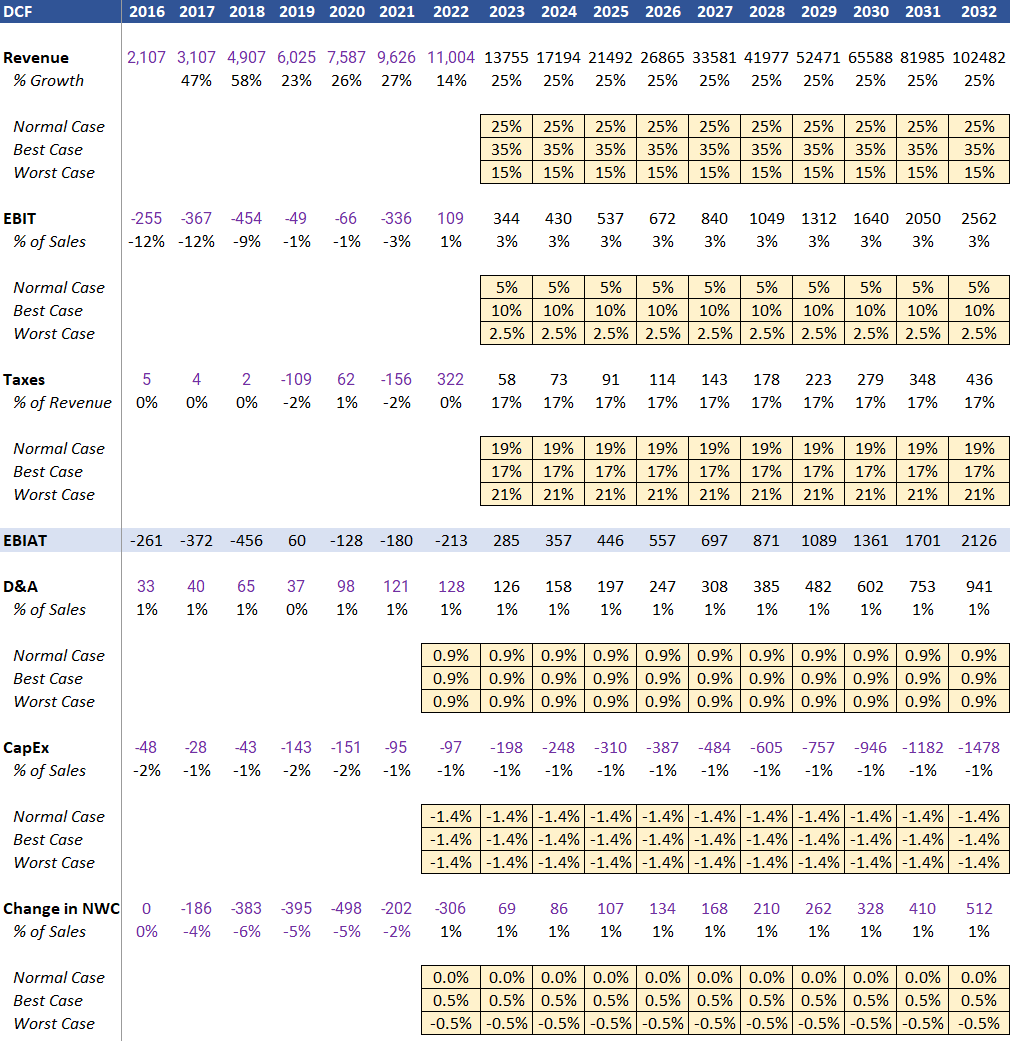

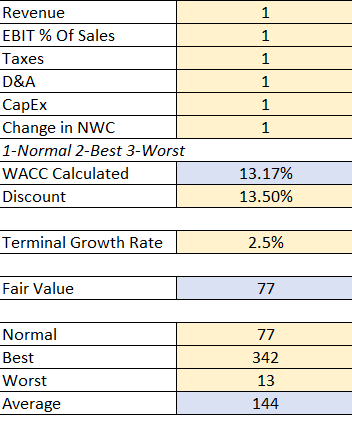

For the DCF analysis, we will model Revenue and EBIT in five different scenarios:

- Best Case Scenario: “Pie-In-The-Sky” scenario, using the upper revenue and gross margin expectations, outlaid by Ek’s investor day remarks. This includes a top line revenue growth of 35% and a gross margin of 35%. The model does not include gross margin assumptions, but rather EBIT. We can model this by using their current gross margin of 25%, and 0-1% EBIT and adding 10% to reach the 35% target, thus having a +10% EBIT margin projection.

- Normal Case Scenario: Using the lower bound revenue and gross margin expectations of 25% and 30% (+5% EBIT), outlaid by the same investor day remarks.

- Worst Case Scenario: Using a very bearish sentiment through analyst projections and failure to meet acceptable profit margins. This includes 15% revenue growth, derived from analysist estimates data, through Seeking Alpha and 2.5% EBIT margins.

- Bonus Case Scenario 1: Models a situation where revenue expectations are the best, but Spotify fails to deliver on profit expectations. Many believe Spotify will only be a successful company if they deliver on much larger profit margins. But what happens if they fail to do so, but continue to grow revenue at a rapid rate? Thus, a volume approach.

- Bonus Case Scenario 2: Follows the same scenario as Bonus Case Scenario 1, but revenues are dropped to reasonable levels, while still maintaining a low profit margin.

We also make assumptions through Taxes, D&A, CapEx, and Change in NWC.

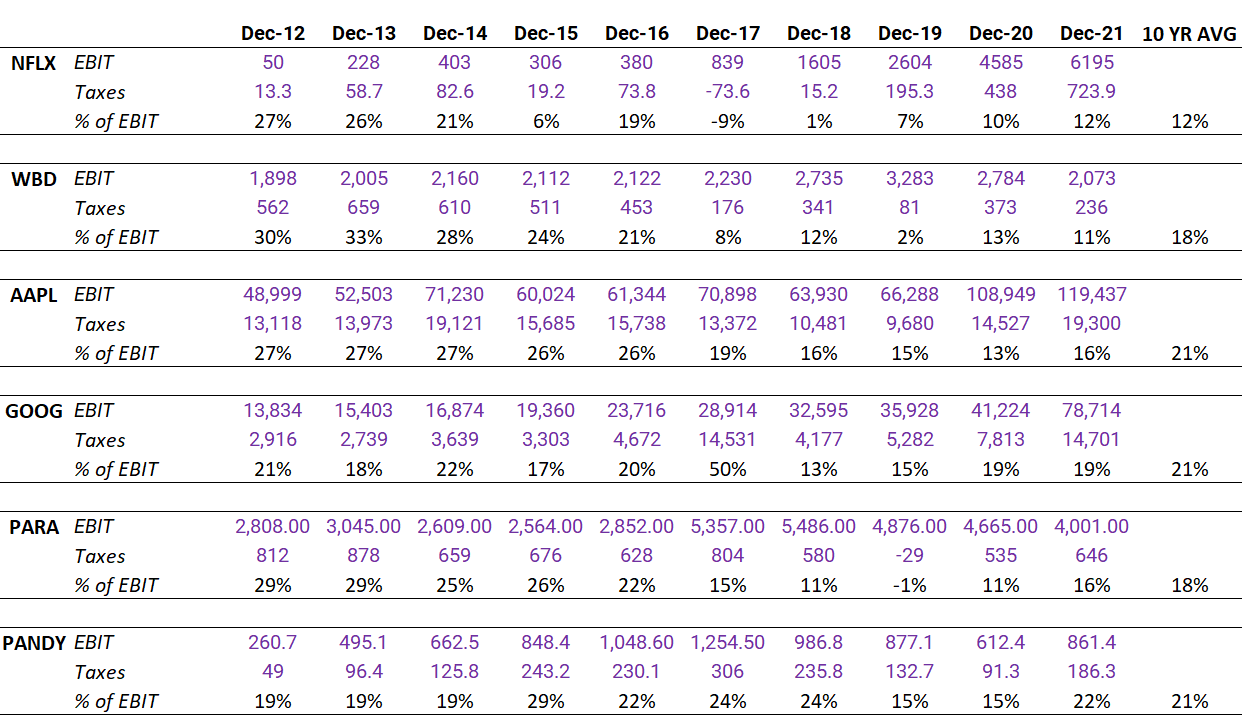

- Taxes: We assume 17%, 19%, and 21% of EBIT for Best Case, Normal Case, and Worst-Case scenarios. To predict taxes can be a little tough, since Spotify is still in the growing phase and making minimal profit. However, we wanted to avoid picking rates out of the blue, but rather use average tax rates from competitors and peers. This information was gathered from Seeking Alpha and displayed in the spreadsheet below.

Spotify Comparable Tax Rates (Seeking Alpha and Author)

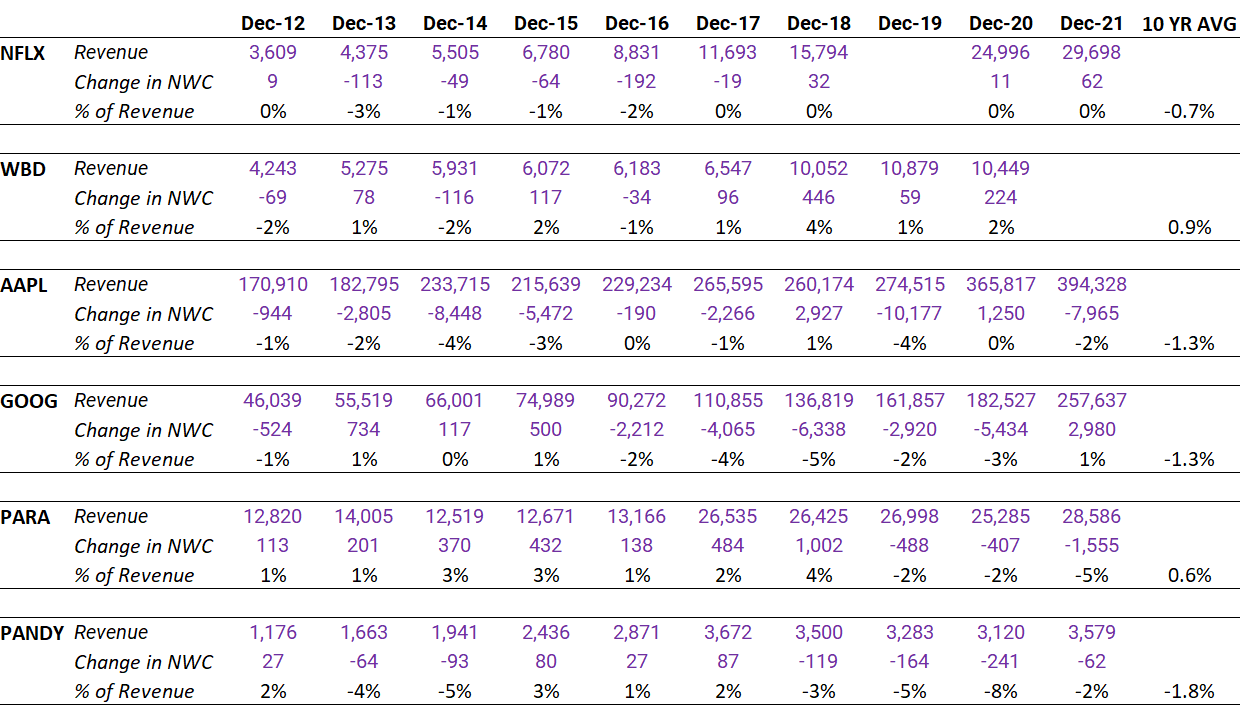

- Change in NWC: We assume 0.5%,0%, and -0.5% of Revenue for Best Case, Normal Case, and Worst-Case scenarios. Like Taxes, change in NWC is also tough to predict because historical Spotify data suggest we use extreme negative values such as -5%. This is simply not sustainable and would rather predict based on averages of peers and competitors. Again, raw data was pulled from Seeking Alpha and compiled in the sheet below.

Spotify Comparable Change in NWC (Seeking Alpha and Author)

- D&A: We take a simpler approach here and average the last 3 years for a 0.9% of Sales, since this value is consistent.

- CapEx: Again, a simpler approach here is made by averaging the last three years for 1.4% of sales.

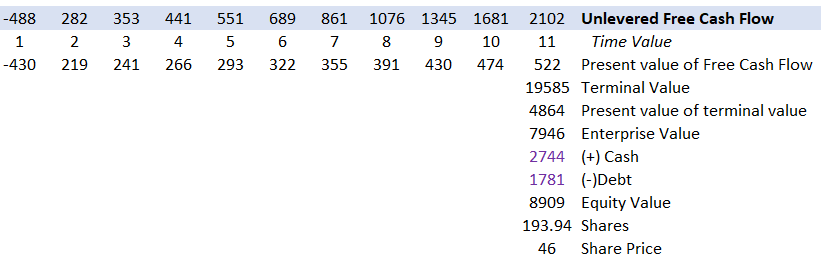

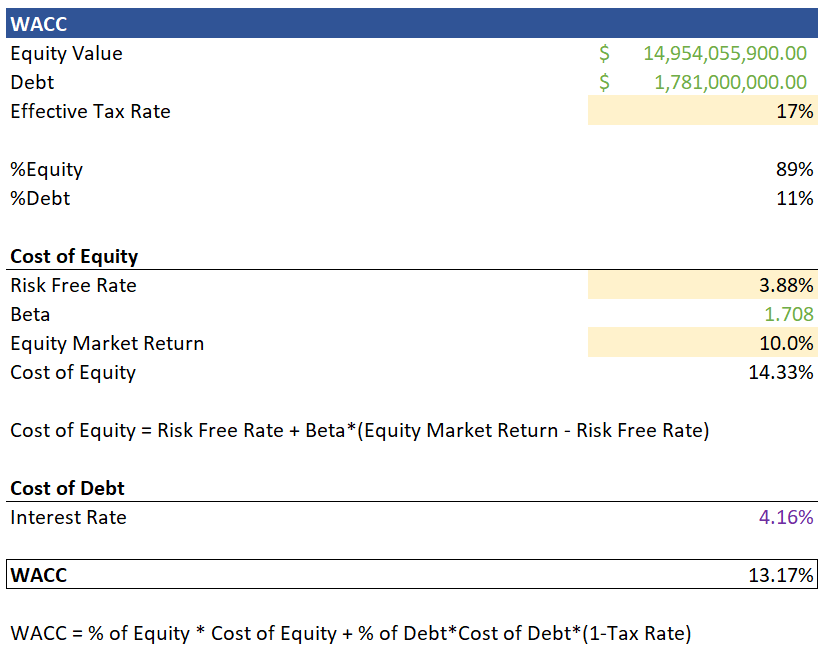

The final assumptions were plugged in the tan boxes below and project out Unlevered Free Cash Flow ten years. From there, we discount back by a calculated WACC of 13.5%. We then add cash and subtract debt, then divide by the number of shares, to arrive at a final share price, depending on the scenarios. All assumptions and calculations are shown below.

Spotify DCF Assumptions (Seeking Alpha and Author) Spotify DCF Final Calculations (Seeking Alpha and Author) Spotify WACC Calculation (Seeking Alpha and Author)

After playing with scenarios, we arrive at a couple different target prices:

- Best Case Scenario: All switches (2), meaning all scenarios for Revenue, EBIT, Taxes, D&A, CapEX, and Change in NWC follow the best outcome – $342 Per Share

- Normal Case Scenario: All Switches (1), meaning all scenarios for Revenue, EBIT, Taxes, D&A, CapEX, and Change in NWC follow the normal outcome – $77 Per Share

- Worst Case Scenario: All Switches (3), meaning all scenarios for Revenue, EBIT, Taxes, D&A, CapEx, and Change in NWC follow the worst outcome – $13 Per Share

- Bonus Case Scenario 1: All Switches (2), except EBIT margin is switch (3), indicating maximum revenue gain but failure to meet profit expectation. – $87 Per Share

- Bonus Case Scenario 2: All Switches (2), EBIT Margin switch (3) and Revenue switch (1) indicating minimum profit and normal revenue growth. $46 Per Share

Spotify DCF Switches (Author)

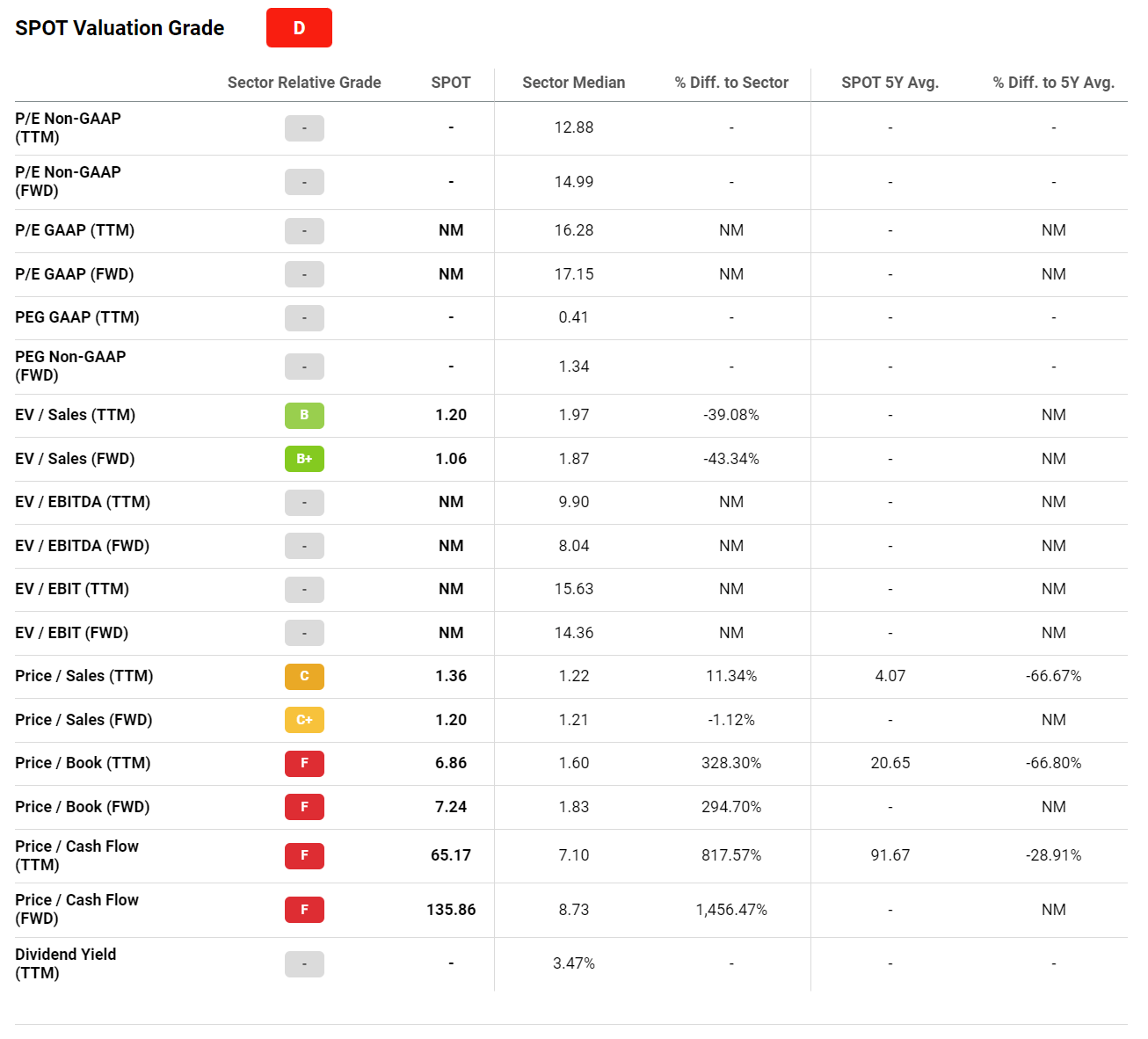

Multiples

The multiples section of evaluation will be straightforward compared to the DCF. Using Seeking Alpha’s Valuation Grade card, we will pick through some multiples and tell a story about each one:

Spotify Multiples (Seeking Alpha)

EV/Sales and EV/Sales FWD: Anything close to 1 here is a bit absurd, in a good way, for a growth stock such as Spotify.

Price/Sales and Price to Sales FWD: Again, values close to 1 are very hard to come by for high growth stocks

Price/Book and Price/Cash Flow: They receive an F here, which is reasonable. However, we should keep in mind that has revenue grows, and margins improve slightly, cash flow should increase relative to the current stock price. Perhaps a 1-year FWD Price/Cash Flow doesn’t look great. But what about a price/5Year cash flow down the line or a Price/10Year Cash flow? Simply using my DCF, I can get very rough estimates from 1.0 to 10.0, which seem very favorable.

All other Multiples: Simply aren’t possible because the company isn’t consistently profitable yet.

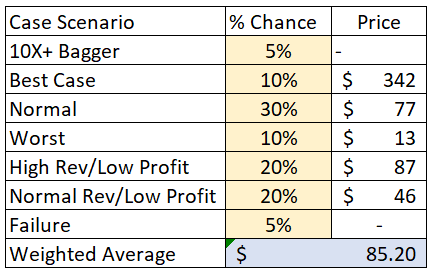

Valuation Final Target Price And Discussion

One of the outstanding things about Spotify is that they are a growth company with ten quarters of free cash flow. To be able to successfully run a DCF on such a company speaks volume in itself. Combine this with very compelling multiples, Spotify shows evidence of a value play with extreme upside. But alas, the results indicate a target price of $85, indicating Spotify is undervalued.

Spotify Target Price (Author)

Going down the left-hand side of the chart, you’ll notice I included the five scenarios discussed, along with a multibagger and failure scenario. The 10X bagger is truly a possibility. If Spotify grows and profits at rates expected, WACC should lower, and we can discount at a 10% rate, instead of an original 13.5%. Doing this in the DCF, while playing around with profitability can yield price targets in $600+. However, I did not want to include this in the weighted average to massively inflate the target price.

The main take away here, however, is the returns on the low profitability stories. High Rev/Low Profit Scenario, Normal, and Normal Rev/Low Profit yield stock prices that are very close to the current price. By adding these percentages, we essentially gave ourselves a 70% chance to make a good return, even if Spotify delivers average or below average profit expectations over the next ten years. It seems at its current levels; we can essentially profit on thin profit margins.

Risks, Catalysts, And Concluding Thoughts

The main risk centered around Spotify, is failure to become profitable. One could discuss many other risks, such as competition, leverage, general economic headwinds, global expansion, new technology, and the list goes on. But if Spotify captures profit, it means they have already taken care of a long list of risks. And if they don’t, they will find themselves in the graveyard of media middlemen with the likes of AM and FX stations. However, I have a two-part catalyst to combat this risk.

The first catalyst to this scenario is through a “Charlie Munger Inversion” of sorts:

The question is not “if” Spotify becomes profitable. Rather, the question is: Spotify “will” become profitable, but “how” will they execute this? Furthermore, “how much” profitability do they really need to justify a buy at the current price?

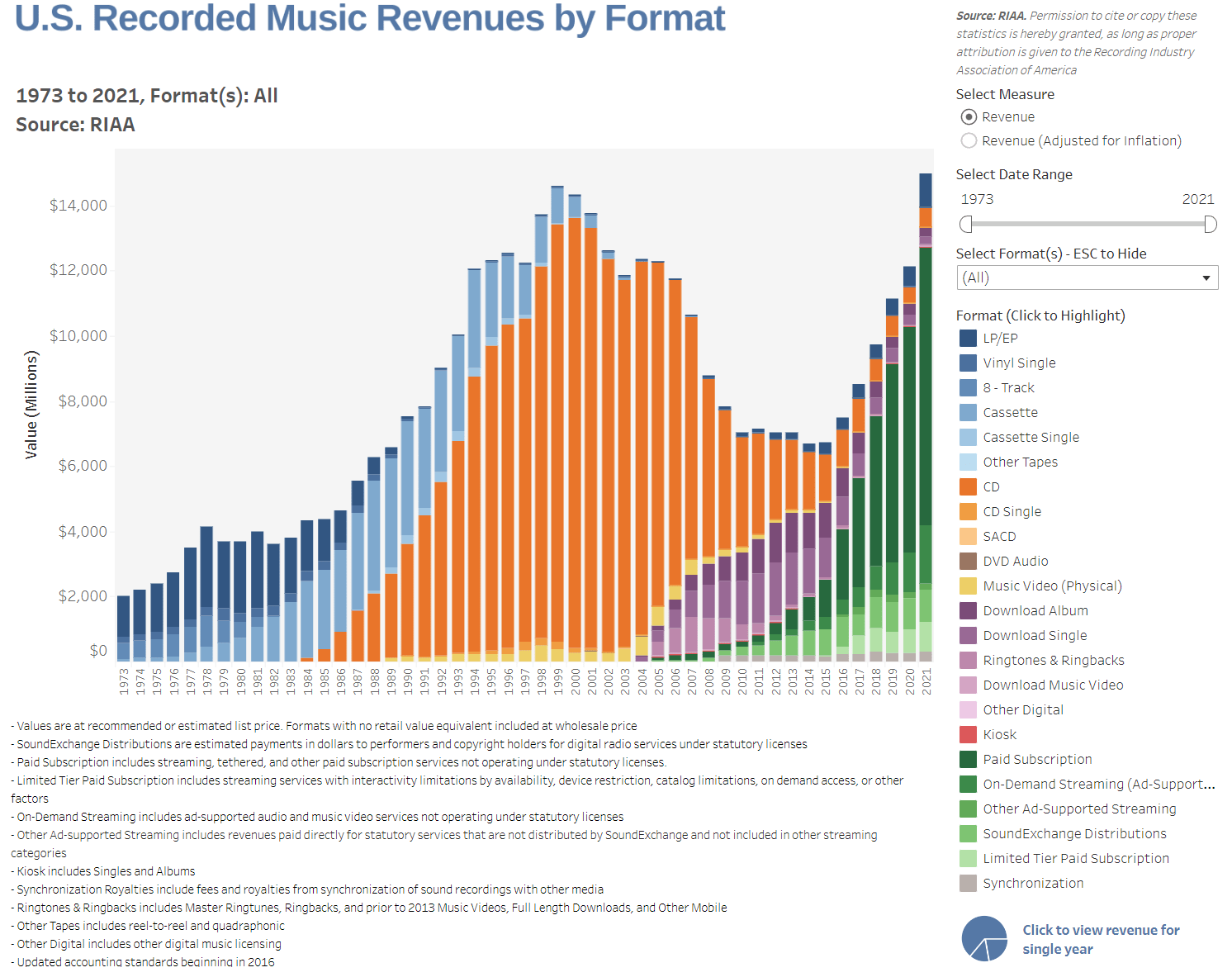

I form this basis on the simple fact that society does not want to revert back to non-online media. And in order for society to push forward and maintain what they want, online media platforms must become profitable at some point. If these platforms must become profitable at some point, my bet is Spotify will find a way. The U.S Recorded Music Revenue from the RIAA will help us walk through this logic.

U.S. Recorded Music Revenues By Format (RIAA)

The last ten years, music revenue dropped as downloads, streaming and paid subscription of the online world of music started to take over. With this happening, the notion was that online music providers would have to become profitable to compensate for the lack of revenue. However, as paid subscriptions have boomed, and the mass market becomes equipped with technology, we see revenue start to pile up to compete with late 90s level, when CDs were at its peak. With this in mind, it no longer seems Spotify has to become as profitable as people say, to become a great business. This leads me to my second point that not only will Spotify eventually have to become profitable, but it also won’t take nearly as much margins as the general consensus seems to believe, reflective of the stock price at least.

This is easily shown through our discounted cash flow results for low margin scenarios. We can see that even with measly 2.5% EBIT margins, Spotify stock will still be a great buy so long as the capitalize on revenue, thus playing the volume game. And if revenue continues to rise through these modes, then that allows Spotify to get away with even lower margins. Yet no one is bearish on Spotify’s revenue growth, they only focus on the profit margin. This provides informed investors more opportunity to pick up a great stock that provides a great service, at a great price.

Be the first to comment