Elitsa Deykova/E+ via Getty Images

Investment Thesis

Spotify Technology S.A. (NYSE:SPOT) is about to report its Q4 earnings next Tuesday, January 31, premarket.

In the past year, I’ve been either uninterest or bearish on this name. I didn’t see a positive risk-reward on its share price.

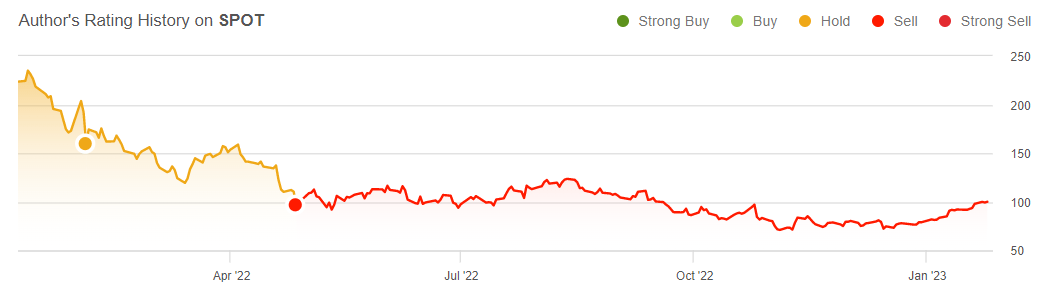

SPOT author’s work

Today, given that investors are also now uninterested in this stock, I make an about-turn on my point of view. I hereby take the contrarian angle and I believe that in the next 6 months, Spotify Technology S.A. stock could provide an attractive return.

Spotify 2023 Prospects Discussed

Asides from its balance sheet positioning, which we’ll discuss imminently, I believe that Spotify could now be better than many investors have come to perceive.

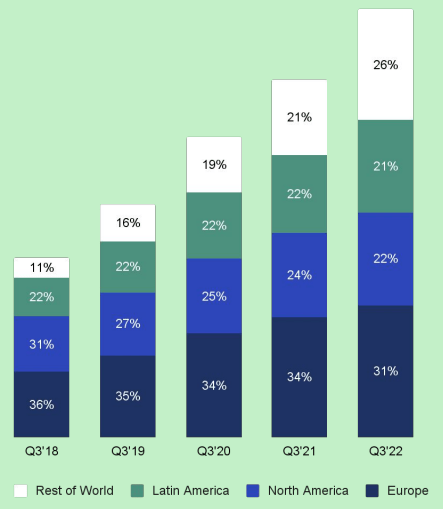

Yes, there are ample issues with Spotify. For instance, the fact that the majority of its monthly active user (“MAU”) user growth is coming from outside North America and Europe.

SPOT investor presentation

That means that users in other geographies are likely to be less profitable to Spotify.

Simply put, there are really many hairs on this investment thesis. But I’m inclined to believe that this insight may already be priced in.

Revenue Growth Rates Are Stabilizing

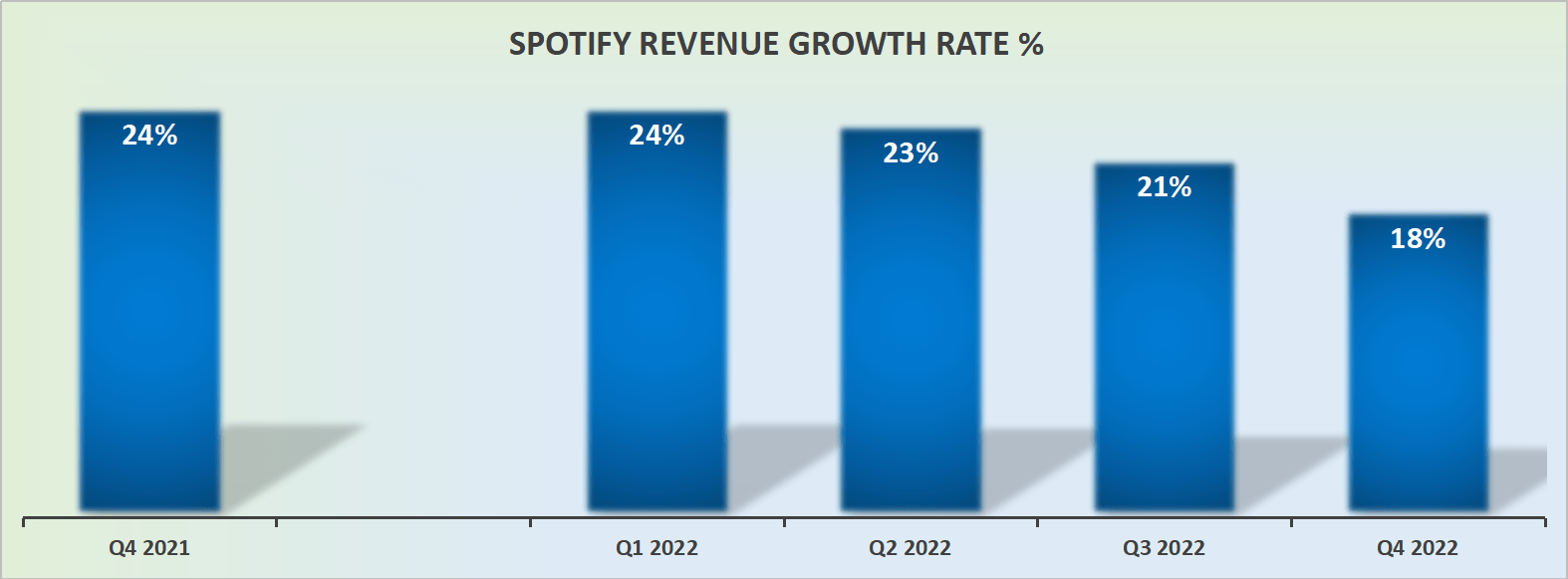

SPOT revenue growth rates; as reported revenues

Spotify’s revenues are now hovering around the high teens. Particularly once we factor in its 800 basis point FX tailwind.

Now, the problem that immediately materializes is that the bulk of these revenues, nearly half of Spotify’s Q4’s revenues, are expected to come from positive tailwinds in the USD to EUR exchange rate.

What happens in 2023 if the USD was to weaken relative to the EUR?

If the USD were to become a headwind, this would crystalize my contention that Spotify’s revenue growth rates are coming in around the mid-teens range.

But that may not be such a bad thing. Firstly, if revenues stabilize in the mid-teens, that means that the business is predictable and stable. That means it becomes easier to budget, forecast, and ultimately value.

When investing, the less uncertainty there is in the outlook, the more investors are willing to pay for that conviction.

Also, if the business is stable and growing at mid-teens CAGR, then Spotify Technology management will have less incentive to be aggressively investing for growth, and it can reduce its workforce while also cutting back on unnecessary investments in an effort to improve its free cash flow potential.

Profitability and Expectations for 2023

Typically, two types of investments work well.

Either a business is growing super-fast and that attracts a certain shareholder base because the business is delivering something remarkable. Or, something is growing at a slower pace, but it’s expected to be more profitable and that, too, gets a distinctive shareholders base.

The problem for Spotify is that it went from being perceived as being a high-growth stock and is now in the process of churning out of its prior shareholder base, to a newer shareholder base.

This takes a considerable amount of time. However, I believe that throughout 2022 that has already been broadly underway. That means that if we look out 6 months from now, Spotify Technology’s newer investor base will have quite different expectations from the investors today. And that’s really the key to seeing this contrarian investment opportunity for what it is.

SPOT Stock Valuation — 1x Sales Is Compelling

Spotify Technology S.A. ended Q3 with EUR3.8 billion of cash and equivalents, or approximately EUR2.6 billion of net cash (once its notes are factored in). That means that approximately 14% of its market cap is made up of cash.

Hence, even though the Spotify business isn’t highly free cash flow-yielding, the fact that it holds a significant amount of cash and is not burning through much cash means that Spotify can continue to plow ahead undeterred. Or put more accurately, it can cut back on excess fat and still invest in high ROI opportunities, without external funding.

That said, I declare that the key to Spotify will be to convince investors that it can exit 2023 as a meaningfully more free cash flow-producing business than it will report next week.

The Bottom Line

SPOT investor presentation

Next week, when Spotify Technology S.A. reports its Q4 earnings and provides guidance, one hopes to hear more about why Spotify’s platform has seen two outages in two weeks.

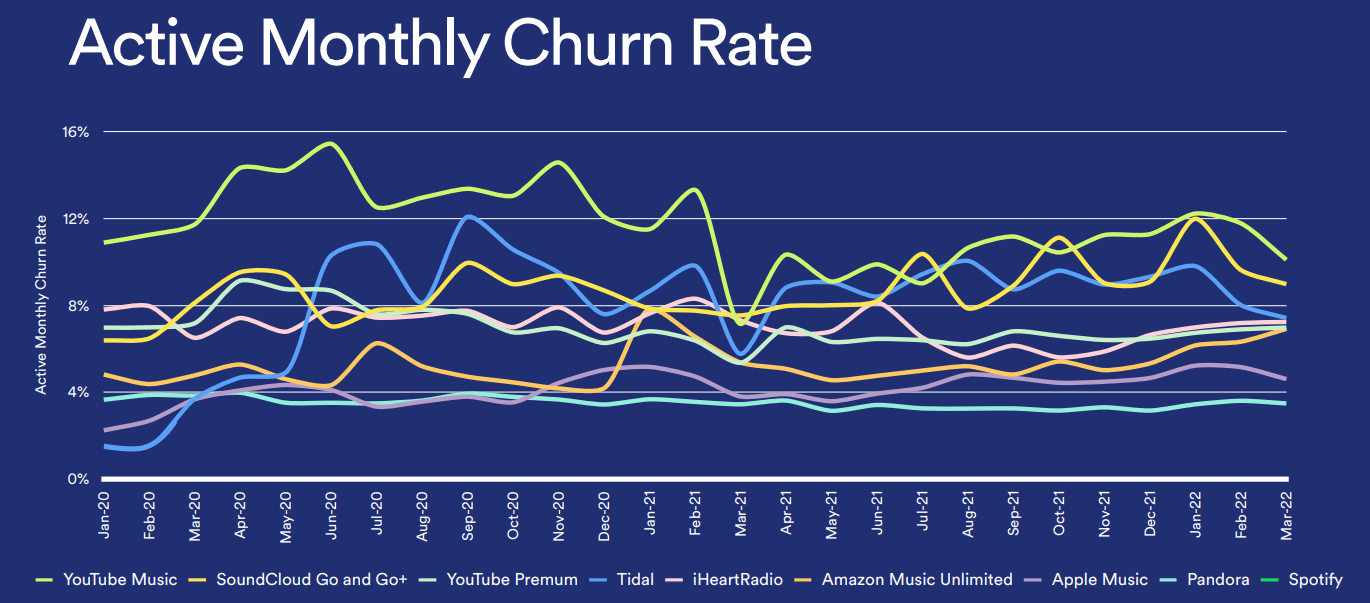

Since Spotify appears to have one of the lowest monthly churn rates among its competitors as of right now, I’m inclined to think that its consumers won’t be overly irritated by this situation.

In sum, I believe that this investment, Spotify Technology S.A., could have a positive risk reward. There are clearly still significant issues with its operations and execution, not to mention there’s significant uncertainty about exactly when Spotify can become more profitable. But I’m eager to believe that’s already priced into Spotify Technology S.A.’s market cap valuation.

This investment in Spotify Technology S.A. will not be for the faint-hearted. So price this position in your portfolio accordingly.

Be the first to comment