Pgiam/iStock via Getty Images

If you’ve been following us for a while, you will have realized by now that we analyze indices with hard-line quantitative data. I personally dislike subjective thought theory as it’s filled with confirmation bias. Therefore, today’s analysis of the SPDR S&P 500 Trust ETF (NYSEARCA:SPY) again follows a quantitative approach with an emphasis on the S&P 500’s risk premium.

A qualitative overlay is phased into the analysis. However, it should be taken with a pinch of salt as it’s only a summation of the index’s key influencing variables.

We maintain our previous Sell rating on SPY.

Establishing Proximities

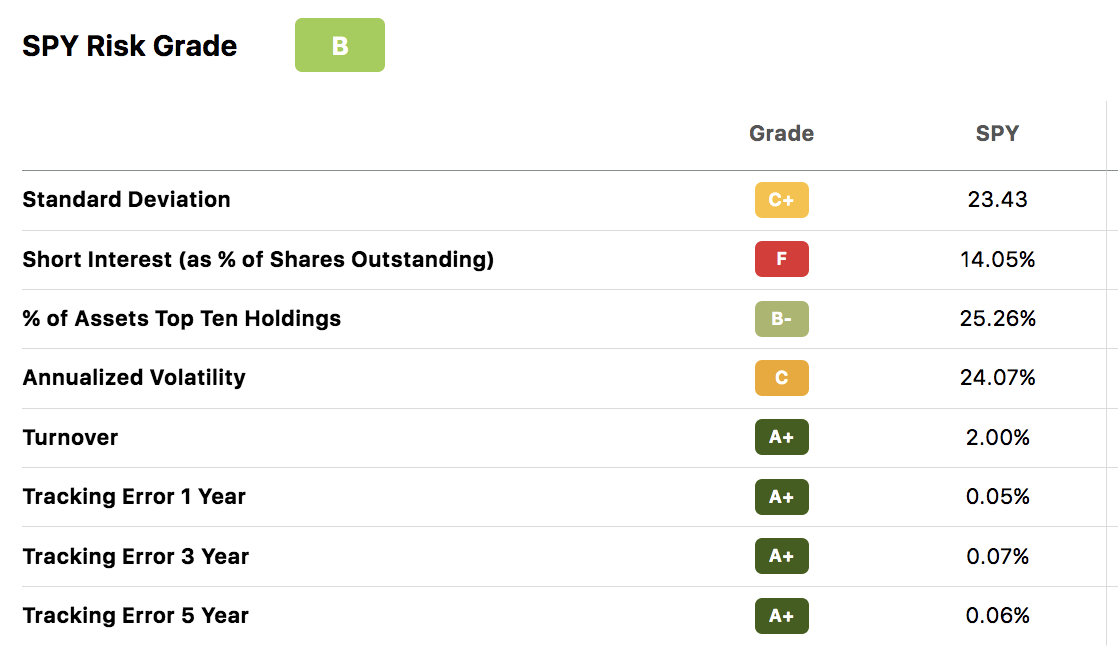

For those unaware, the SPY is an exchange-traded fund that tracks the performance of the S&P 500 while presenting a more investable price. The tracking error of the ETF is very low, thus, allowing us to analyze the SPY and S&P 500 in tandem. Therefore, today’s analysis applies to readers that are interested in the ETF or/and the index’s prospects.

Seeking Alpha

Equity Risk Premium

The equity risk premium is the extra percentage of incremental risk that investors demand to divest from corporate bonds and invest in the stock market. Fundamentally speaking, the market risk premium provides holistic risk demanded from investors; however, analyzing the ERP provides a more in-depth vantage point.

- The ERP is calculated as Market Risk Premium – Risk-free Rate

The market risk premium is influenced by factors such as geopolitical risk, foreign exchange market stability, general financial market stability, and any top-down macroeconomic variable. Furthermore, the risk-free rate is the default-free cost of debt. The Rf is difficult to obtain; thus, we utilize the 10-year treasury yield as the Rf. However, some analysts use shorter-term rates if the long-term rate is non-stationary (its long-term influencing variables are significantly different than today’s market variables).

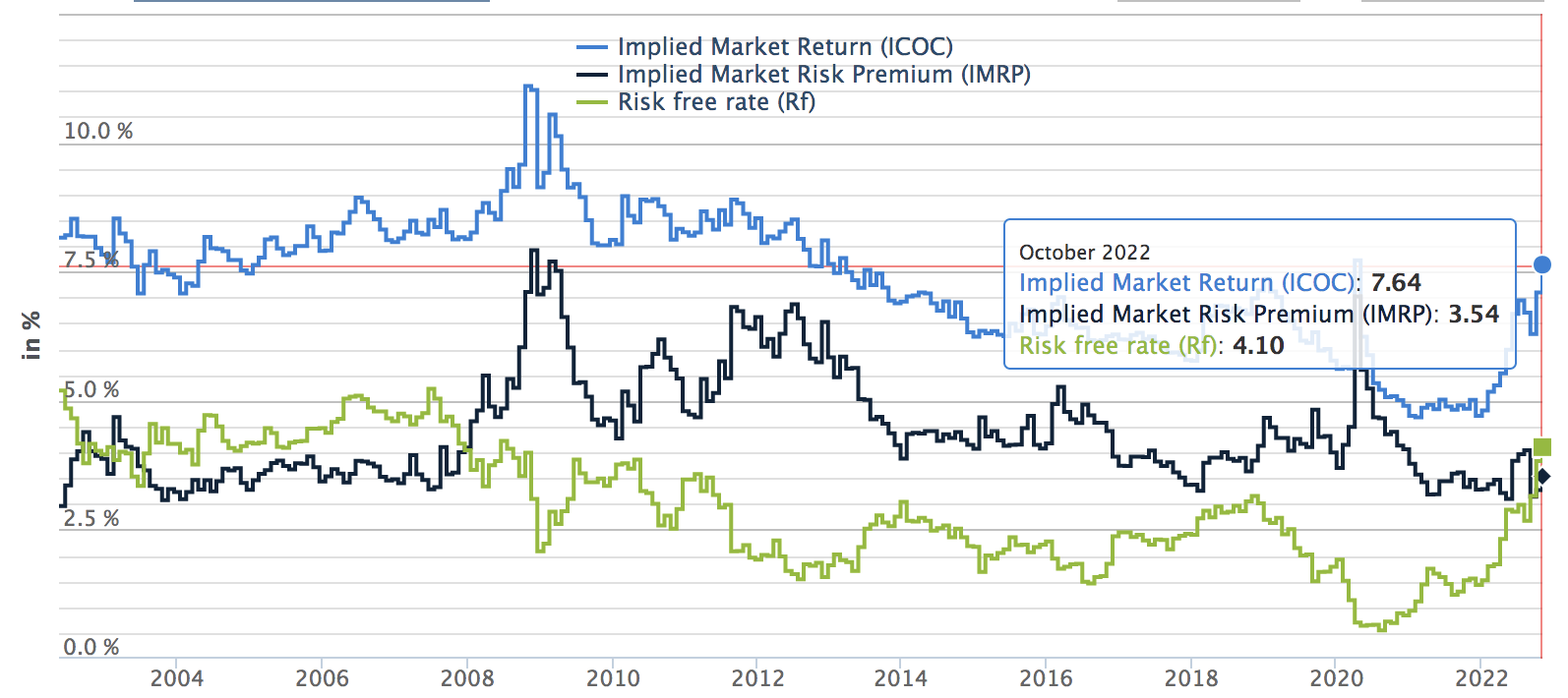

The diagram below illustrates how the market risk premium has proliferated during the past year. This could be due to geopolitical tensions in China, the war in Ukraine, unstable monetary policies, and 2022’s bear market.

We anticipate the market risk premium to remain elevated going into 2023 because of the speculative environment surrounding interest rate policies. Moreover, the political situation in China remains unknown; thus, the secondary effects on the U.S. economy could be priced by equity investors.

market-risk-premia.com

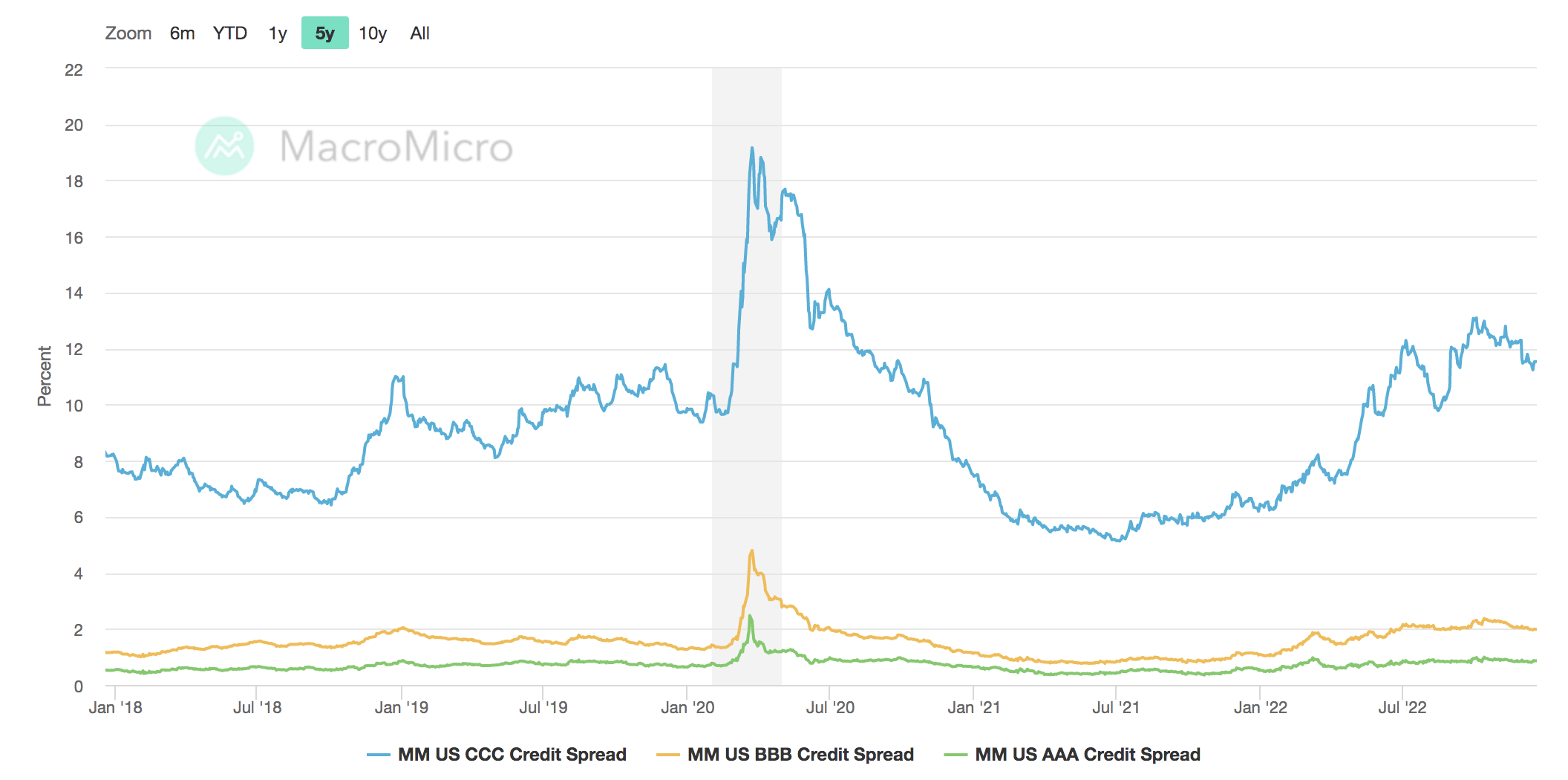

The rise of the risk-free rate has somewhat phased out the upward trajectory of the market risk premium. However, the increase in the risk-free rate needs to be assessed. In our opinion, widening credit spreads have been a key influence on the risk-free rate. Although wider credit spreads have an adverse effect on the bond market, they also deter the equity market’s outlook, as many stock market participants probably won’t be interested in investing during the heightened possibility of a credit event.

We expect credit risk to remain elevated, given 2023’s recession risk narrative. A higher risk-free rate needs to be supported by bullish steepening of the yield curve for it to truly phase out equity risk.

MacroMicro

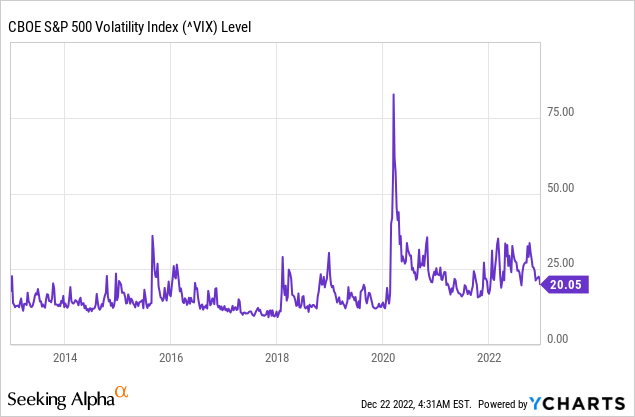

Furthermore, the VIX remains a concern as it’s above its decade average. Measuring the ERP’s risk-return utility is best done by comparing the ERP to market volatility. If volatility overshadows the ERP, investors are less likely to invest, especially when recession risk is elevated, as consumers’ marginal propensity to consume increases.

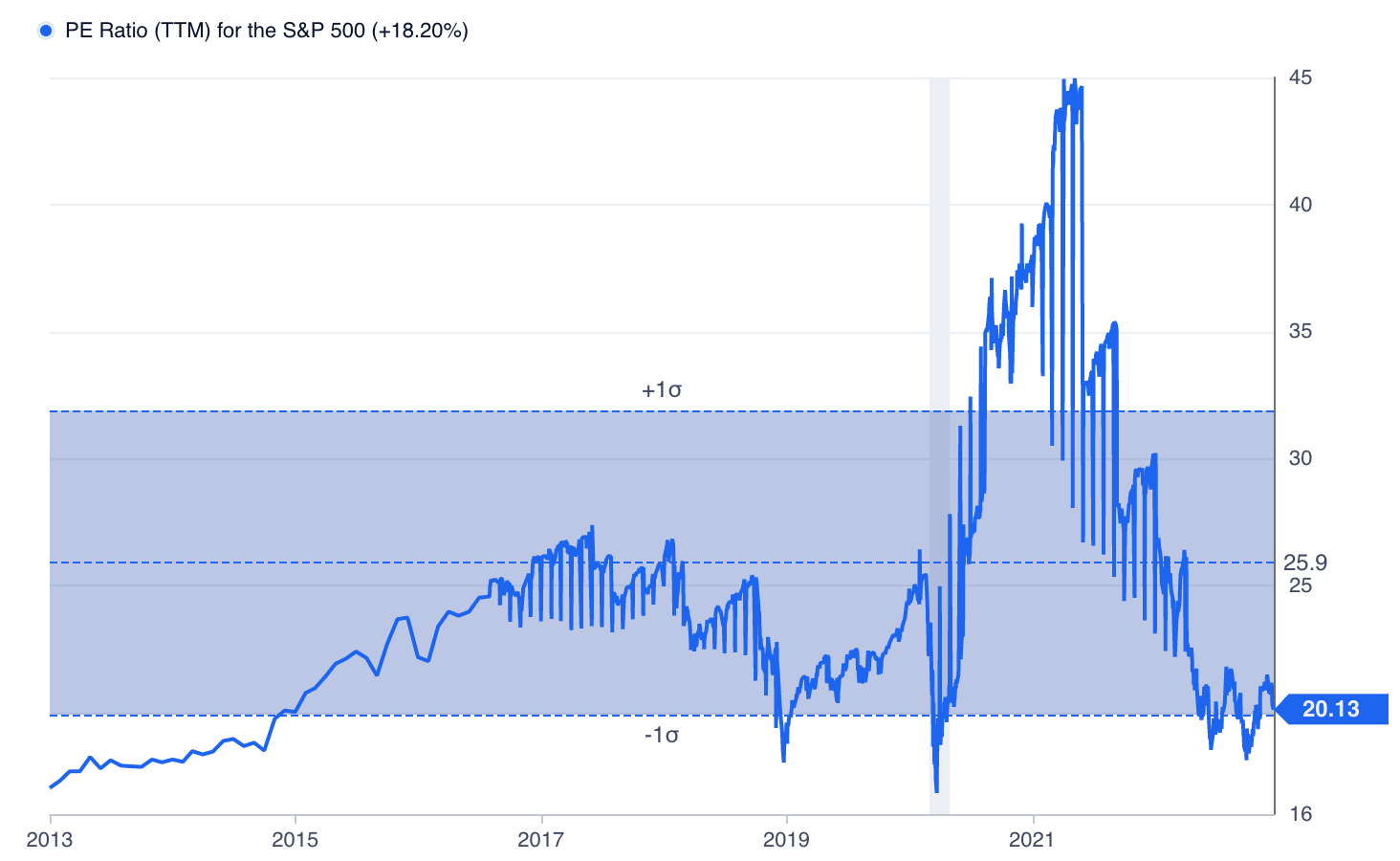

Valuation as a counterargument

Valuation metrics can be used as a counterargument to the risk premium. Even though earnings could drop off in 2023, the S&P 500’s PE ratio has reverted to a more realistic level. Thus, many value-driven investors could opt to invest for portfolio cost basis reasons.

GuruFocus

As displayed below, many high-quality companies experienced significant drawdowns in 2022, which could urge investors to “buy the dip”. As a portfolio research scientist, I know that the correlation between a good company and a good stock is less apparent than most believe. Nonetheless, many investors could decide to speculate on price mean reversion.

| Stock | YTD Return |

| Apple (AAPL) | -25% +/- |

| Microsoft (MSFT) | -27% +/- |

| Amazon (AMZN) | -50% +/- |

| Alphabet (GOOG) | -38% +/- |

| Tesla (TSLA) | -65% +/- |

Source: Seeking Alpha

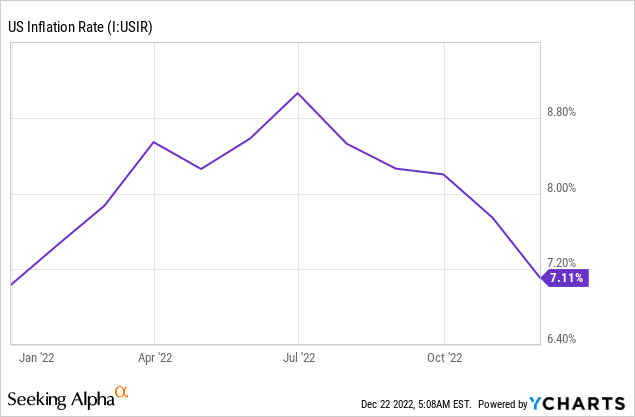

Lastly, the U.S. inflationary surge that we experienced in 2022 seems to have abated. Again, I don’t think fading inflation alone is a reason to be bullish on the stock market, as the nature of inflation needs to be assessed. However, many market participants invest with confirmation biases, which could cause inflation to be a primary influencing factor.

Concluding Thoughts

We reiterate our bearish outlook on the S&P 500 and the SPY ETF, as equity risk premiums and volatility are unfavorable. Many might seek confirmation bias in cooling inflation and a drawdown in the index’s PE ratio. However, we’re sticking with our asset pricing vantage point and assigning a sell rating with an indefinite horizon.

Be the first to comment