designer491

Intro

We wrote about SPDR Portfolio Long Term Treasury ETF (NYSEARCA:SPTL) in April of last year when we issued a sell signal on the exchange-traded fund. Shares of the ETF (Currently trading around the $31 mark) are down roughly 10% since we issued a sell rating. In fact, the percentage return of the SPTL short position was well into double-digit percentage territory by October of last year but sustained hikes in interest rates by the Fed along with declining reported rates of inflation have resulted in roughly a 15% hike in the SPTL fund over the past three months or so.

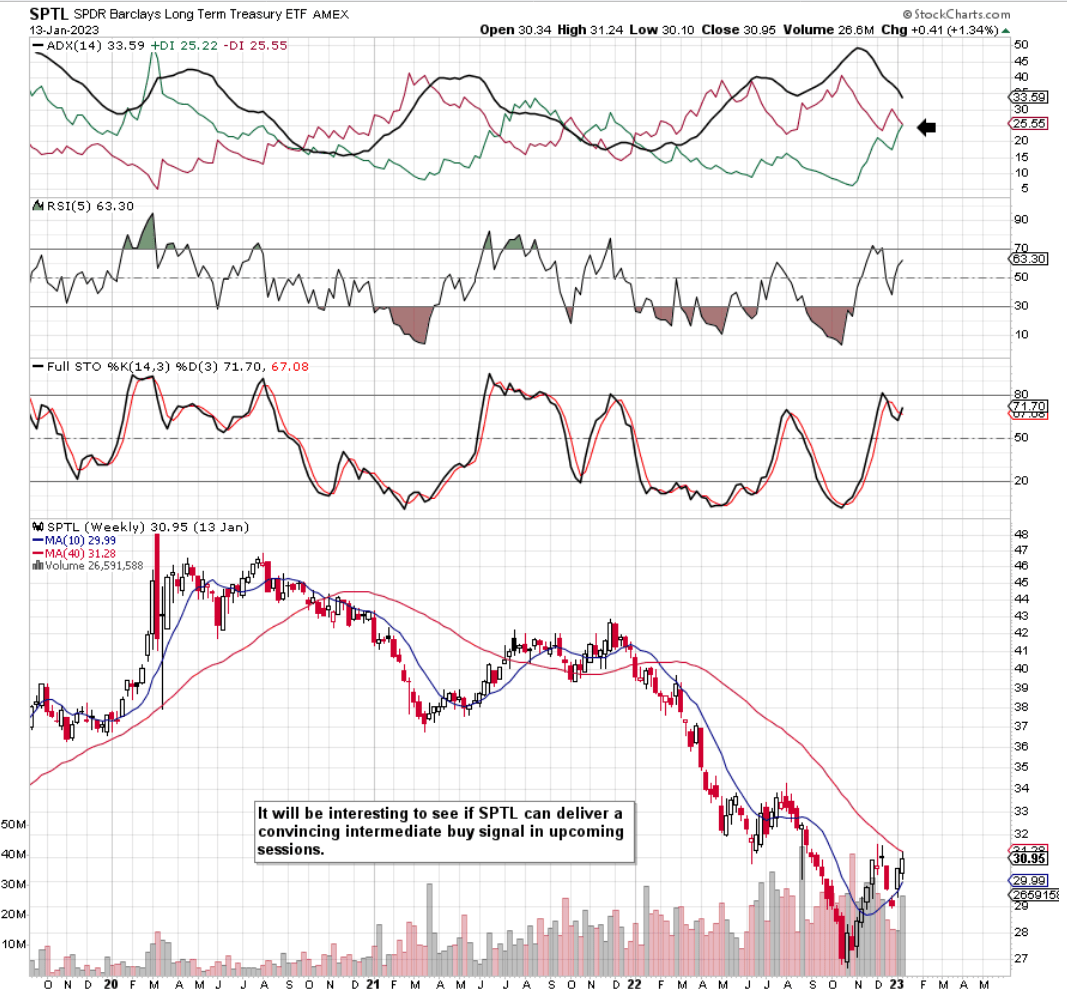

If we look at the fund’s intermediate chart, we see a potential pending buy signal through the ADX trend-following indicator. This technical indicator offers a complete trading system as it combines the directional movement indicators of the red & blue lines (DI & -DI) with the main ADX indicator which solely focuses on the strength of the trend. Suffice it to say, although the recent uptrend (Which commenced in October of last year) in SPTL is nowhere near as powerful as the downtrend which preceded it, present conditions could still facilitate a trending move to the upside in US treasuries. This pretense would be enhanced if the fund’s recent December highs (Which correspond roughly with the 200-day moving average of approximately $31.51) can be taken out with conviction. SPTL has not delivered an intermediate directional ADX buy/sell signal for well over a year so it would be significant if it indeed takes place.

SPTL Intermediate Chart (Stockcharts.com)

Therefore, SPTL bears need to be ready for a snap-back rally here but we maintain that all that will unfold here will be a bear-market rally. Ultimately, we expect the fund to eventually roll over & make lower lows once more for the following reasons.

Interest Rates Too Low

Although inflation has subsided in recent months, the reported rate of between 6% to 8% remains well above short-term interest rates in the US. The government through the Federal reserve has to come at this problem with a two-pronged approach which we can not see happening any time soon. Short-term interest rates need to remain above the prevailing inflation rate for a considerable amount of time and government spending needs to be reigned in significantly.

SPTL bulls believe that the falling inflation we are seeing in the market today will continue to drive the ETF higher as bonds will look appealing once more. This may very well be true over the near term, but the political will simply is not there to run budget surpluses over a sustained period of time.

Significantly higher interest rates dampen demand for goods significantly as savers actually begin to earn something on their money whereas debtors need to pay higher payments back to their creditors. As a result, prices of goods and services can come down because the supply of these very same goods and services can increase. Suffice it to say, higher interest rates reduce the velocity of money in the real economy which means you have fewer dollars chasing goods and services. Inflation, as a result, comes down which would be bullish for a long bond fund such as SPTL as bond investors would target getting paid in future dollars which would be actually worth something.

Spending Remains Too High

The US government however continues to run budget deficits where in fact, it needs to be cutting spending significantly while also raising taxes significantly. The recent inflation reduction act only focuses on the symptoms of the problem (lower prices) instead of tackling the source (Too much spending). The man on the street believes he is actually being helped when in fact his money is losing value by the month. This is why we believe there is every opportunity (like in 2008) that interest rates in the US would actually be cut if and when a hard recession arrives which ultimately would be ultra-bearish for SPTL long term.

Conclusion

Therefore, to sum up, we have seen from history that inflation curves are not linear and can very easily return and take out pre-existing highs after a downward trend. Although the Fed has kept up its hawkish stance on interest rate hikes in recent months, we have seen no movement by the government in cutting spending, which would in turn reduce budget deficits significantly (Reduce Demand). It remains in spending mode and would most likely increase spending even more if a significant economic contraction was to occur. Remaining bearish in SPTL but will wait for this upward run to run its course. We look forward to continued coverage.

Be the first to comment