SeanShot

S&P Global (NYSE:SPGI) has solid fundamentals and a business that is well exposed to structural growth trends in the financial industry, while its current valuation is undemanding considering its stronger growth profile than in the recent past.

Company Overview

S&P Global is a financial services company, providing market information and insights across several asset classes. The company has a market value of about $109 billion and trades on the New York Stock Exchange.

The company has a well-diversified business profile, especially after the merger completed during 2022 with IHS Markit, increasing its exposure to market intelligence. Following this acquisition, S&P Global has five operating segments, namely Global Market Intelligence, Global Ratings, Global Mobility, Global Commodity Insights, and Dow Jones Indices.

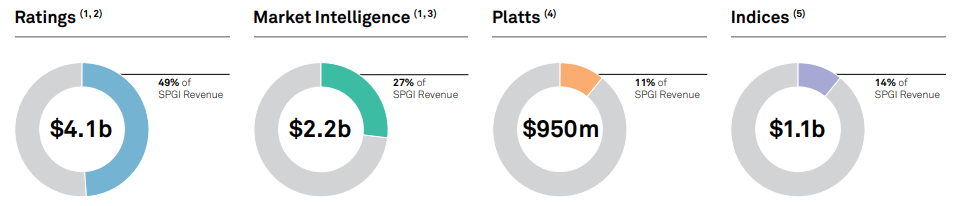

While historically S&P Global had a large exposure to ratings, which represented more than half of its revenue and earnings, it now has a less concentrated business profile. Indeed, in the last quarter, market intelligence was its largest segment measured by revenue, with a weight of around 35% on total revenue, followed by ratings with a 23% weight, while other operating segments had a more balanced weight on revenue.

Business Strategy & Growth

S&P Global’s business has changed considerably in recent years, as the company’s strategy was concentrated on reducing its exposure to its largest, and mature, segment of ratings, and increasing its exposure to segments with better growth prospects.

It has performed several acquisitions and divestments to change its business mix toward areas that are in demand in the financial industry, namely market information, indices, and data intelligence. More recently, the acquisition of IHS Markit was a strong bet on market intelligence, given that it valued the acquired company at $44 billion in an all-stock deal. This increased significantly S&P Global’s overall size, and its exposure to this operating segment, which seems to be a sensible move for the company positioning it well to benefit from structural growth trends in the financial industry.

There are several trends that benefit S&P Global’s growth prospects over the next few years, including demand for risk solutions, the sustainability and energy transition, the shift to passive and investment automation, beyond others. S&P Global is well positioned to benefit from these structural trends, through its several operating segments. For instance, its index segment benefits from the rise of passive investing and ETFs, while market intelligence is supported by the rise of automated trading and quantitative investing, which require access to market data and analytical tools.

Taking into account this backdrop, S&P Global made a strong bet on market intelligence, with its recent merger with IHS Markit. While this merger was announced at the end of 2020, it was only completed in February 2022, and valued Markit at more than 28x EBITDA, which was not a cheap deal. However, this deal significantly increased S&P Global’s exposure to a growing segment, enhancing its growth profile, leading to margin expansion, and a higher cash flow generation capacity.

Moreover, it increased S&P Global’s recurring revenue to about 76% of total revenue (vs. 69% previously), providing more visibility regarding its long-term financial figures, and is expected to lead to significant cost and revenue synergies. Indeed, S&P Global expects to deliver cost synergies of around $480 million and revenue synergies of some $350 million, with a positive impact on EBITDA of around $680 million. After synergies, the transaction multiple decreases to less than 20x EBITDA, which is a valuation that is more acceptable, but still not particularly a bargain in my view.

Nevertheless, as S&P Global has a very good track record on integrations and has historically delivered good value from its business strategy, which has led to a much higher operating margin over the past decade (operating margin improved from 33.7% in 2013 to 45.3% in Q3 2022), this means that potentially the company can deliver higher synergies than expected as the two business are highly complementary.

Regarding its medium-term financial targets, to be achieved by 2025-26, S&P Global expects to grow organic revenue by 7-9% per year, achieve an adjusted operating margin between 48-50%, and deliver low to mid-teens annual EPS growth. More recently, as part of the company’s growth strategy and capital allocation discipline, it announced its intention to sell its engineering solutions business, which in the last quarter reported revenue of $95 million. While this is expected to be a small divestment, it is a segment that has a below-average operating margin, and therefore seems to make sense in the company’s overall business strategy.

Financial Overview

Regarding its financial performance, S&P Global has a very good financial history, considering that it has been able to report strong revenue and earnings growth in recent years.

In 2021, it reported record revenue of close to $8.3 billion, an increase of 11.5% YoY, with close to half of its revenue coming from ratings, followed by market intelligence (27% of revenue), while other segments had smaller weights.

Revenue (S&P Global)

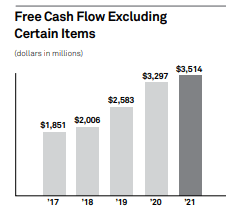

Its operating profit was nearly $4.6 billion, an increase of 15% YoY, as the company was able to cut costs and improve efficiency, leading to an adjusted operating profit margin of 55% (+190 basis points compared to 2020). Its free cash flow was above $3.5 billion, a new record high, and almost double from its 2017 levels.

Free cash flow (S&P Global)

While historically S&P Global has returned a large part of its free cash flow to shareholders, it suspended its share repurchase program in 2021 due to the IHS Markit merger, while dividend payments were maintained. This led to only 21% of free cash flow being returned to shareholders during 2021, a much lower value than in previous years.

During the first nine months of 2022, S&P Global has maintained a positive operating momentum, despite the challenging macroeconomic environment and weaker capital markets, which had some negative impact on the ratings segment.

In Q3 2022, its revenue amounted to $2.86 billion, an increase of 38% YoY due to the integration of IHS Markit, while adjusted revenue decreased 8% YoY. Its ratings segment reported lower revenue due to lower debt issuance in 2022, reporting a revenue decline of 33% YoY in the last quarter. On the other hand, its market intelligence revenue increased by 83% due to the integration of Markit, while adjusted revenue increased by 4% YoY.

S&P Global’s adjusted net income declined 11% YoY to $968 million, due to weakness in its ratings segment, which was the only segment to report lower operating profits in recent months. During the first nine months of 2022, S&P Global returned more than $11 billion to shareholders, through its accelerated share repurchase agreement of $12 billion to be completed during the year, plus $749 million in dividends. For the full year, S&P Global expects revenue to increase by 30% YoY, while guidance for 2023 is only expected to be announced next month when it publishes its annual results related to 2022.

Over the medium term, according to analyst’s estimates, S&P Global is expected to maintain a solid growth path, given that revenue is expected to increase to close to $14 billion by 2025 (vs. $11.6 billion in 2022), and its net income should be near $5 billion (vs. $3.7 billion in 2022). This growth and improvement in profitability are supported by the integration of Markit and the company’s exposure to growth markets, with potential upside to current estimates coming from higher synergies than expected, as the company’s track record on acquisitions is quite good.

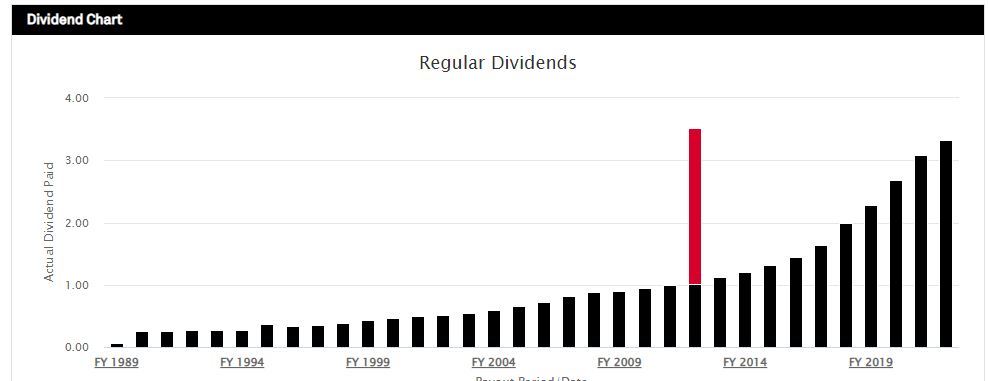

Regarding its shareholder remuneration, S&P Global has a very strong track record given that it has delivered a growing dividend and performed several share repurchases over the past few years, a strategy that is not expected to change much in the foreseeable future.

Dividends (S&P Global)

Its last quarterly dividend was $0.85 per share, or $3.40 annualized, which at its current share price leads to a dividend yield of about 1%. Thus, its income appeal is not particularly attractive, even though its dividend growth history is quite good.

Conclusion

S&P Global has changed its business profile considerably in recent years, of which the recent merger with Markit is a step forward to increase its exposure to market intelligence and reduce its presence in the mature ratings business. Despite that, S&P Global is currently trading at 26x forward earnings, in-line with its historical average over the past five years, which seems to be somewhat undemanding and makes it a good long-term growth play within the financial industry.

Be the first to comment