winyuu

Despite the downturn in stocks during 2022, the underlying U.S. economy remains strong and stable. While real GDP growth for 2023 might be flat, the nominal growth will match the realized inflation rate for the year. I expect the average inflation rate for 2023 to be about 5%, ending the year near or below 4%. The bulk of the economic slowdown is expected to be in large purchases, especially housing, automobiles, and to a lesser degree, appliances. For 2024, I expect real GDP growth to pick back up to a longer-term trend level of 2%.

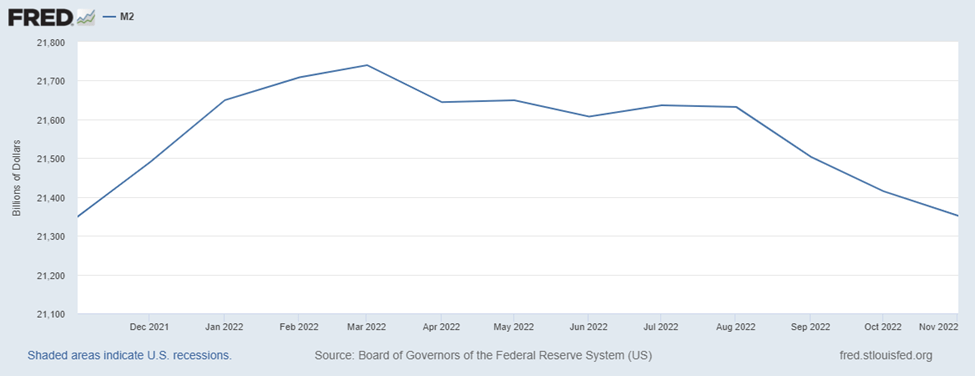

In addition to the slowdown in housing and auto sales, the money supply has also been contracting as measured by M2. While money supply shot higher as a result of massive monetary and fiscal stimulus to support the economy during the pandemic lockdowns, it has been steadily falling since March of 2022, and is likely to do so as the Fed continues its quantitative tightening.

1-Year M2 Money Supply (St. Louis Federal Reserve)

Unemployment has been steady and stable in the 3.6%-3.8% range since recovering off the 2020 Covid lows. While it might be reasonable to assume that unemployment will creep higher in the coming months, given corporate and consumer balance sheet strength, it does not appear to be in any imminent danger of rising too much. I suspect unemployment will rise throughout 2023 but is likely to peak in the 4.2%-4.5% range by year-end 2023 or early 2024. This estimate is based on information provided by The Conference Board.

Corporate Revenue Growth

Revenue growth is difficult to estimate for the S&P 500 for the coming year given the multiple variables at play. Revenue and profit figures will be driven by consumer spending, which is highly dependent on sentiment and unemployment, inflation and interest rates, and the relative strength of the dollar.

Taking each major factor individually, consumer spending should remain strong, but be neutral to current revenue growth on a year-over-year basis because of other considerations. Strong consumer spending is likely to be offset in part by weakness in housing purchases and related spending. In other words, the impact of continuing low unemployment but slower housing due to higher interest rates is unclear, but likely flat. As discussed above, my base case is for inflation to continue to fall steadily throughout 2023, finishing the year at or below 4%. If this scenario comes to fruition, then it is likely the Fed will move to a more neutral position, which would help mortgage rates stabilize and put a backstop on declining housing sales. Declining inflation, neutral Fed, and stable interest rates would be expected to result in a stable dollar, or even a falling dollar relative to other countries that may be behind the U.S. in fighting inflation. In that scenario, this would serve as a tailwind for revenue, profitability, and ultimately stock prices as exports would be expected to increase significantly throughout the year.

Margins

Given the level of wage growth, unemployment, and continually improving operational efficiencies at businesses in the aggregate, I think that it is reasonable to assume that net margins for the S&P 500 will continue to improve, or at least hold steady at about 12%, based on FactSet estimates.

S&P Profit Margins (FactSet)

That said, I think taking a more conservative approach makes sense, and that using a range of 11%-12% is reasonable.

2022 Performance

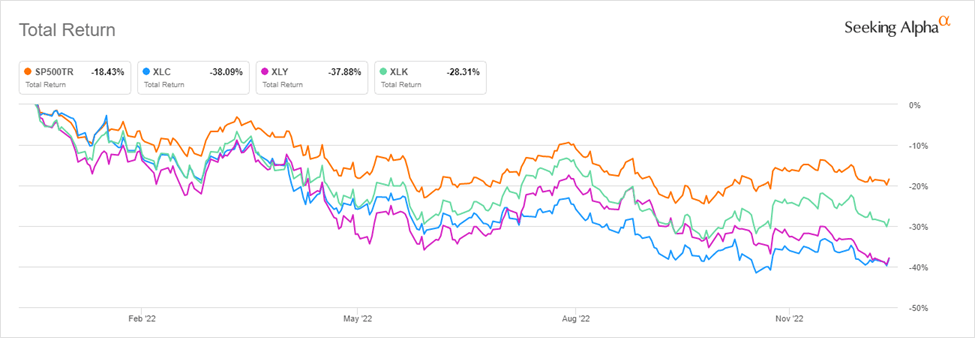

The S&P 500 is down about 12% for the year, but certain segments of the market have fallen much more, and the drawdown in some individual names, particularly pandemic era darlings, has been catastrophic for some. Communication services, consumer discretionary, and technology are the worst-performing S&P sectors for the year, falling more than 30%.

YTD Performance of the S&P versus the Communication Services, Consumer Discretionary, and Technology Sectors (Seeking Alpha)

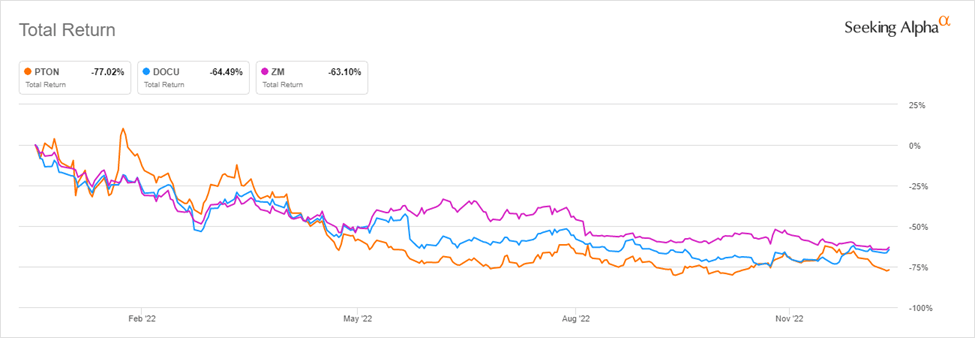

Pandemic era favorites including Peloton (PTON), DocuSign (DOCU), Zoom (ZM), and even many of the mega-cap Tech names have declined by more than 50% (90%+ in some cases), and are trading below pandemic lows experienced in March 2020.

YTD Performance of Peloton. Docusign, and Zoom (Seeking Alpha)

Putting It All Together: Estimated S&P 500 Earnings For 2023 & 2024

Earnings are reported in nominal terms, so even as inflation declines, the higher-than-average level will serve as a positive contributor to nominal earnings while possibly eroding them in real terms.

For 2022, there isn’t much estimation required, given that three of four quarters have been reported. For the year, I expect total earnings of nearly $200. However, earnings for next year 2023, should be about 5% +/- 2% higher on a nominal basis. This would indicate 2023 earnings of $206-$214. Using the top end of the range and rolling that forward based on a recovery in earnings plus inflation would give a 2024 forward earnings estimate of about $235.

As the year-end 2023 S&P 500 value will be based on estimated 2024 earnings, the forward multiple at that time should be applied. Valuations, based on earnings and multiples, are always forward looking. So to estimate a year-end 2023 value for the S&P 500, and therefore a 2023 return, it is critical to understand that the forward-looking earnings and multiple will be.

I expect some multiple expansion over the next year based on two conditions: continually falling inflation, and stable unemployment. Falling inflation will lead to lower interest rates, which decreases the discount rate applied to earnings, effectively increasing the earnings multiple. Stable unemployment implies that the economy remains robust, which will be manifested in continued revenue and earnings growth as well as constant or improving margins.

The current forward P/E on the S&P 500 is about 17x, below the 5-year average, but slightly above/in-line with the 10-year average.

Because I believe that the value of the S&P 500 will finish next year based on 2024 earnings estimates multiplied by the forward P/E at that time, my estimate based on pure current fundamentals for the S&P 500 is to close 2023 at about 4,250, or about 10.4% above the December 29, 2021 close (based on $235 in earnings and 18x multiple, plus a little rounding.) However, because I am optimistic that conditions will have improved by then with greater certainty with regard to earnings, earnings growth, inflation, interest rates, geopolitical issues, and the next U.S. presidential election, I believe the return for the S&P 500 will be significantly greater than that for 2023. I believe that 2023 earnings will exceed the above estimates, as will the multiple expansion. While I think my fundamental analysis resulting in a 10.4% return for next year is reasonable, with my rose-colored glasses, I expect 2024 earnings of about $250 and year-end 2023 forward P/E of 18.5x, resulting in a December 31, 2023 S&P 500 value of about 4,625, or about 20.1% above the December 29, 2021 close.

Risks

Given my optimistic views on the market in the near and long-term, there are numerous risks that could derail my estimates. For example, the Fed could remain too aggressive in the face of declining inflation and rising unemployment. Increasing energy costs driven by continued or escalating geopolitical factors could cause inflation to remain higher than expected while creating general uncertainty around the global economy and financial markets. These two factors could result in the economy slipping into a recession, possibly one that is deeper or longer than expected, causing a protracted slowdown in consumption and capex that would also cause earnings and equity values to stall. If inflation remains persistent, it is unlikely the Fed will ease or for interest rates to moderate, placing additional downward pressure on multiples. Finally, and this list is far from exhaustive, housing and auto markets could crash due to persistently high interest rates, making borrowing costs unaffordable to a greater percentage of would-be consumers.

Final Thoughts

Predicting the future is typically an exercise in futility. The case I have made for the performance of the S&P 500 over the next year in based on existing data and historical norms and should be viewed as one scenario within a broad range of possible outcomes. I am a long-term investor, and as a result, I am optimistic over the long-term. I believe in the steady march of capitalism, the development of new technologies, and economic growth here and abroad. Given the challenging market conditions during 2022, I believe that this is an excellent time to put money to work, regardless of what happens over the next twelve months. After all, historically, U.S. stocks have risen about 70% of the time on annual basis. Also, the broadly held assumption of a 2023 recession is one that I do not share, and therefore do not believe that corporate earnings will declines as other economic conditions improve. Thank you for reading, and I look forward to seeing your comments below.

Editor’s Note: This article was submitted as part of Seeking Alpha’s 2023 Market Prediction contest. Do you have a conviction view for the S&P 500 next year? If so, click here to find out more and submit your article today!

Be the first to comment