John Kevin

2022 has been quite challenging for the stock market as the S&P 500 (SP500) has lost nearly 20%, following rapid rate hikes by the Fed in order to tame the raging inflation. Despite recent data indicating that the growth of the price level is slowing down, the Fed maintains a hawkish stance with no signs of a pivot. In the meantime, the effects of high rates are already beginning to show in some sectors of the economy like housing. The so called zombie companies are also very vulnerable to the high interest rates environment as the chance for bankruptcy increases. I think that when the effects of the high interest rates began to show in full scale, the Fed will be forced to pivot. The three latest cases of a U-turn in monetary policy indicated, that rates were dropped much faster than they were raised, so by the end of 2023 I won’t be surprised if rates are much closer to 0 than to the current level of 4.5%. This should naturally lead to multiples’ expansion on the stock market, so assuming estimated 2024 earnings of 215.9 and forward P/E multiple of 21, the SP500 could finish 2023 at 4,534.

The Fed’s latest stance

The latest FOMC meeting on 14 December hiked its policy interest rate by 50 bps to 4.5%, following four consecutive 75bps increases. While such rapid hiking is unprecedented for the 21st century, on the press conference, following the FOMC decision, the Chairman – Jerome Powell maintained a hawkish tone:

With today’s action, we have raised interest rates by 4-1/4 percentage points this year. We continue to anticipate that ongoing increases in the target range for the federal funds rate will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.

Although the tone of Powell was hawkish, I’m pretty skeptical as to whether the same policy line will be maintained. After all, it won’t be the first time that the Fed ends up pivoting. Recall, that just a little more than a year ago, Powell was claiming inflation is transitory and there were was nothing in his speeches that was signaling the rapid rate hiking we saw in 2022. For example, in a press conference on 28 July 2021, Powell has said:

Inflation has increased notably and will likely remain elevated in coming months before moderating. As the economy continues to reopen and spending rebounds, we are seeing upward pressure on prices, particularly because supply bottlenecks in some sectors have limited how quickly production can respond in the near term. These bottleneck effects have been larger than anticipated, but as these transitory supply effects abate, inflation is expected to drop back toward our longer-run goal.

The aftermath of this speech was that not only inflation didn’t moderate, but it shot up quite rapidly. And that was before the Russian invasion in Ukraine started, so blaming Putin for the failure of the transitory thesis won’t do it. Meanwhile, the latest rate hike bonanza is starting to show within some sectors of the economy, sparking recession fears.

Recession could be beneficial

The writings of the Austrian School of Economics teach us, amongst other things, of the role of credit cycles in the economy and the negative implications of market interventionism. Artificial expansion of credit availability, just like the one caused by the Fed with the quantitative easing, leads to reduction in the discount rate that investors use to make an economic assessment of a project. In this way, a project that wouldn’t have been economically viable under normal market conditions becomes all of a sudden attractive.

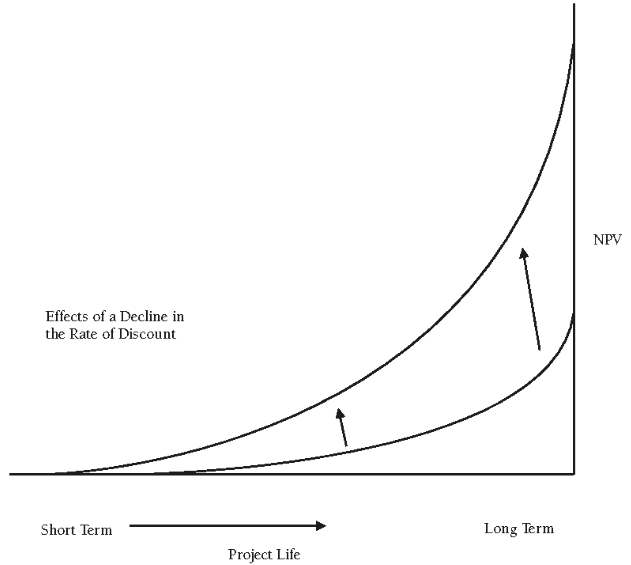

The discount rate effect (Mises Institute)

The inevitable happens when the artificial credit support is pulled away, just like it’s happening now with the rate hikes and quantitative tightening, as such malinvestments are no longer economically viable and have to be liquidated. If this process is left to unfold, the economy will recover in a more sustainable way, as the capital from the liquidated projects is put elsewhere, where it could operate under normal market conditions.

Bankruptcy filings in the US (S&P Global)

This theory could be seen in practice by the multi-year low number of bankruptcy filings of US companies, covered by S&P Market Intelligence. Trillions of dollars, labeled by politicians as “aid”, “stimulus” and “relief”, poured into the economy definitely have something to do with the low figure. Now that the generous handouts have been stopped and interest rates are rising, I expect sharp increase in bankruptcies into 2023. The “pool” of potential bankruptcy candidates has been pretty constant during the last few years, despite the unprecedented monetary and fiscal “stimulus”.

Share of zombie companies in the US (Goldman Sachs)

The primary suspects for bankruptcy – the so called zombie companies have remained near multi-year highs, despite interest rates being kept artificially low, shows data from Goldman Sachs (GS). Now that rates are rapidly rising, I expect a number of them to find themselves into the bankruptcy filing statistics.

The pain element

While recession is sweeping through the economy and cleaning out malinvestments, other more resilient and profitable firms are also tightening their belts, cutting costs deemed unnecessary and emerging more efficient in the aftermath. However, this process is quite painful as it impacts the quality of life of the general population. And that pain comes in various forms.

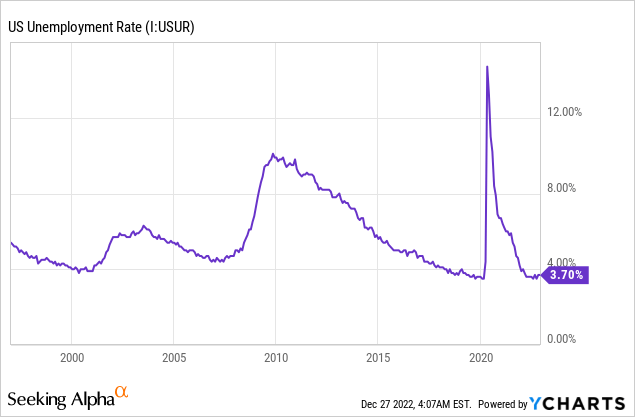

(Un)employment

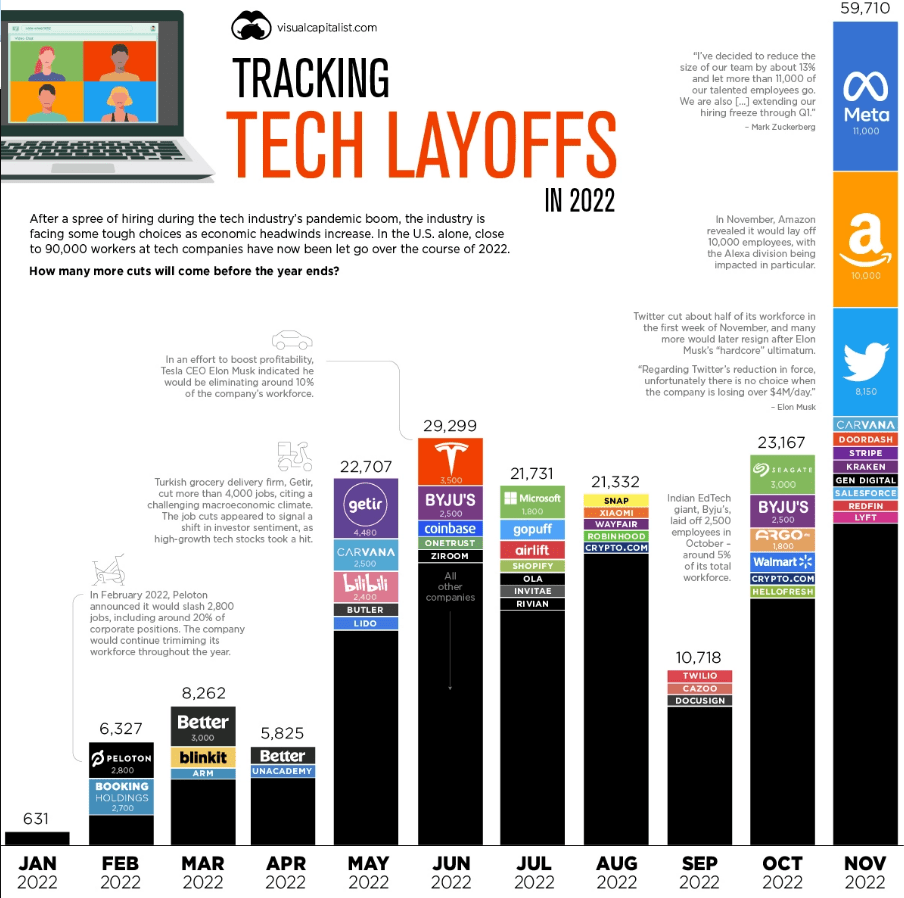

Following the sharp jump in 2020 amidst the introduction of the lockdowns, unemployment has fell to historically low levels in the 3-4% range. That being said, some companies have begun optimization processes ahead of the expected recession. And this includes layoffs too. For example, in November 2022 there was a massive jump in the tech layoffs.

Big Tech layoffs (Visual Capitalist)

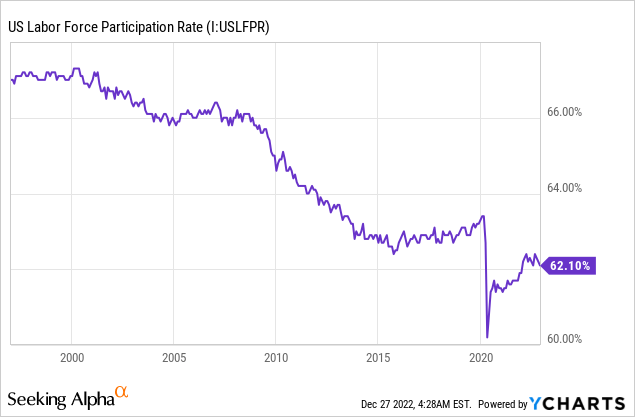

I expect this trend to continue, as companies are pressed by higher financing expenses, while revenue is facing potentially weaker demand. And the low unemployment figure itself is quite misleading. It’s not that record % of the population is working, it’s just that some people have for some reason exited the labor force as evident from the declining labor force participation rate.

If for some reason the sources from which these people cover their expenses begin to dry up, as it would be logical under a recession, they may start rejoining the labor market, sending the unemployment rate soaring.

Housing

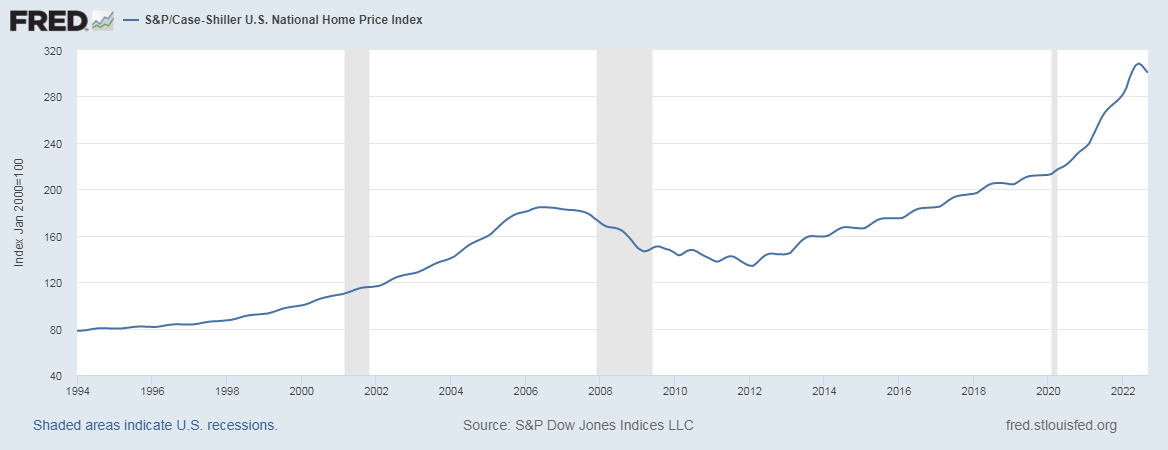

Housing is at the cornerstone at the US economy. It’s substantial part of the nation’s wealth and problems in the housing market could have devastating effects on the overall economy as evident in 2007-8.

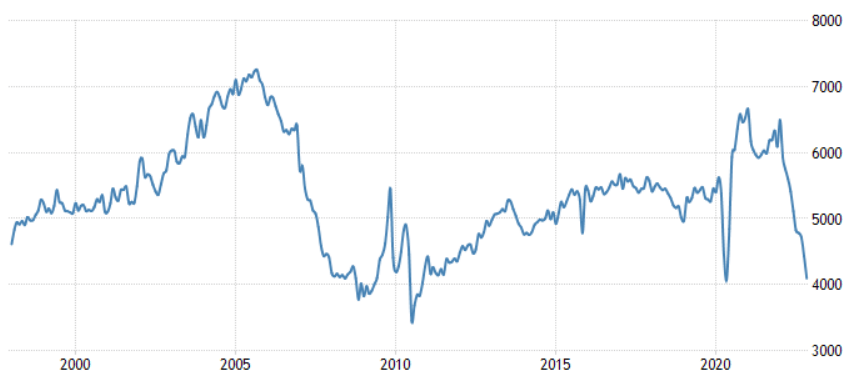

S&P/Case-Shiller US National Home Price Index (FRED)

The period of artificially low interest rates and unprecedented forms of stimulus have impacted the housing market by sending home prices soaring. The rapid increase in housing pieces in 2020, 2021 and the beginning of 2022 has been a lot sharper than that preceding the 2007-8 period. However, now that interest rates are climbing with a record speed for the 21st century and 30-year mortgage rates have surpassed 6%, the housing market seem to be in a standstill. This is evident from a sharp decline in the number of existing home sales.

Existing home sales in the US (Trading Economics)

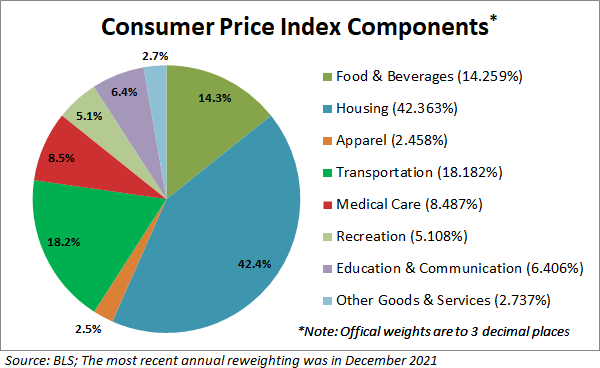

Such steep decrease of activity on the housing market in conjunction with increasing interest rates is a recipe for a decline in housing prices, which has already begun as evident by the S&P/Case-Shiller US National Home Price Index being down in the last few months. And since shelter has by far the biggest weighting in the CPI basket, a continuous decline in housing prices within 2023 could offer the Fed the reason to claim victory over inflation.

CPI basket weights as of 2021 year-end (BLS)

Of course, prolonged deterioration of housing prices could pose major challenges to the financial system as it happened in 2007-8, so I doubt that the Fed will be pleased with such a development and could be forced to step in with its interventionist policy again.

Mountains of debt

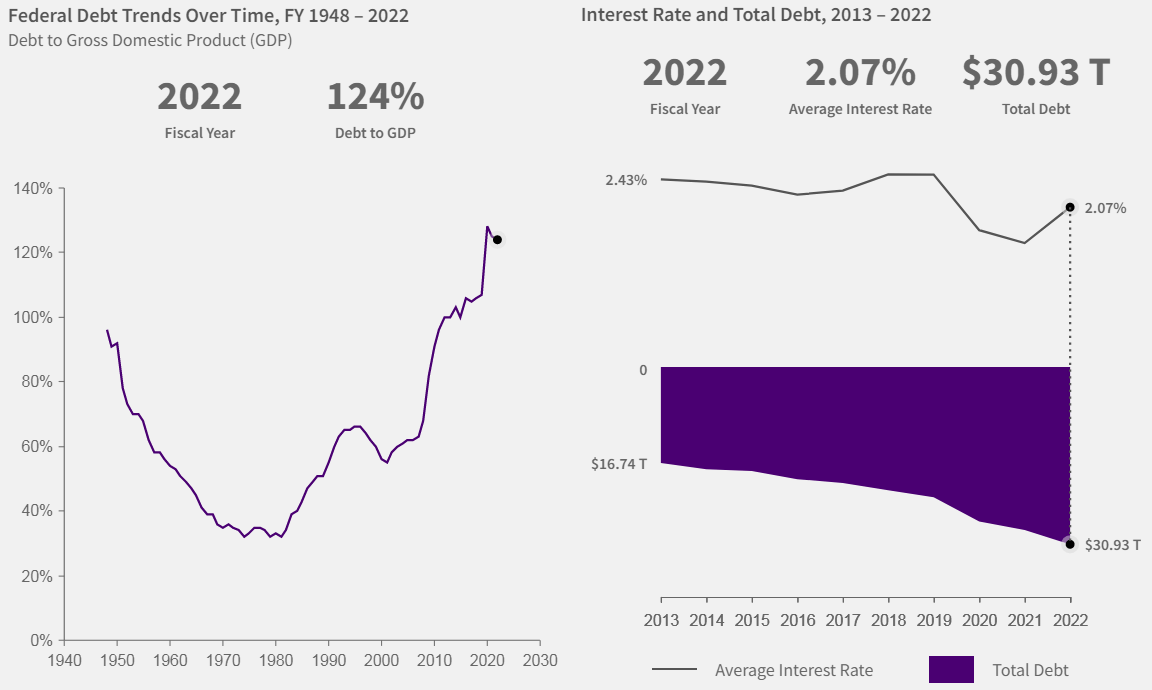

One of the biggest beneficiaries of the artificially low rates was none other than the US government itself, allowing it to maintain low borrowing costs on its growing mountain of debt. The latest weighted average interest rate on the US debt is 2.07%, implying around US$640B of interest payments each year on the US$31T of debt.

US national debt highlights (US Treasury)

The problem is that the debt is going to rise in nominal terms as the 2023 budget has embedded yet another US$1T+ deficit. The bigger problem is the rising interest rate. While the effect won’t be felt immediately in full force, due to the duration of the US debt, if for illustration purposes, the average interest rate reaches the current Fed’s policy rate of 4.5%, this would imply interest expenses of US$1.4T for interest alone, which in turn would be around 24% of 2023’s budget. This hardly seems sustainable.

The politics of pain

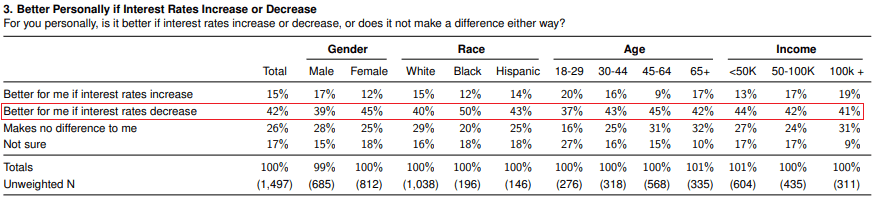

In a democracy, elections are carried every few years, regardless of the economic situation. It’s natural for the overwhelming majority of voters to punish the currently ruling elite for any hardship, regardless if the source of that hardship is the current administration alone or the problems were building up for years. A poll from October 2022 is indicating that the US population largely prefers lower interest rates and that’s before the economic pain has been widely felt amongst the population.

Public perception in the US about interest rates (The Economist/YouGov)

That’s why recession is the greatest fear of the government facing elections soon. And in the US 2024 is an election year. So I’m quite certain that the US administration will find a way to exert the necessary pressure on the presumably independent Fed to reverse course of action if needed. A new wave of trillions in “aid”, “stimulus” and “relief” shouldn’t be put out of question as well. After all, the 21st century has proven that political motives trump economic laws at least for now.

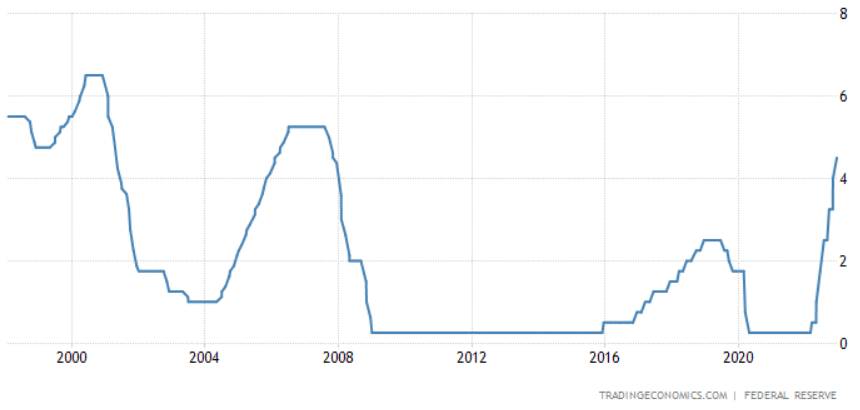

The magnitude of a potential pivot

Looking back at history, the last three U-turns in monetary policy share a common trait – rates came down a lot faster than they were raised in all three occasions. So it’s not unreasonable to expect that the next Fed pivot, which I expect somewhere in H2’23, after economic pain has become unbearable throughout H1’23 and inflation has likely fallen on collapsing house prices and decrease in consumer spending, will be again quite sharp, possibly sharper than the rate of monetary tightening in 2022.

Fed’s Funds Rate dynamics (Trading Economics)

Implications for the stock market

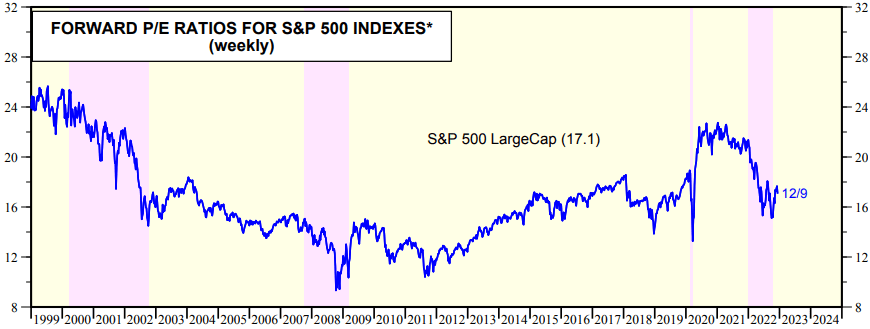

The implications of a monetary policy pivot on the stock market would be quite serious. The discount rate will fall, allowing for multiples’ expansion. Looking at back at 2020, this is exactly what happened, following the rate cuts and trillions of liquidity poured into credit markets. The Forward P/E ratio of the SP500 shoot up into the 20s. I expect a similar thing to happen and the index to finish 2023 with a Forward P/E multiple of 21.

S&P 500 Forward P/E (Yardeni Research)

Regarding the earning’s expectations for the SP500 in 2024, the current analysts’ consensus is for US$254, implying 9.9% growth on top of the US$231, projected for 2023 and 15.5% on the estimate for 2022 of US$220. I find these expectations quite optimistic, considering my view of worsening economic conditions in H1’23. For that reason, I’ll take a 15% discount to the analysts’ consensus estimate for 2024, which will put my forecasted 2024 earnings at US$215.9. Using a 21 Forward P/E multiple should put the SP500 at 4534 at the end of 2023.

Risks

My thesis is based around a Fed pivot, despite them claiming that tightening will continue through 2023. I simply believe that the economic pain from high rates will be unbearable and especially given the 2024 approaching election, rates will be brought down. However, there’s the tiny chance that the Fed stays on course and allows the recession to clear out malinvestments throughout the economy no matter the political pressure. This will be a win for the US economy in the long term as it will emerge more sustainable from the downturn. So I don’t mind being wrong, in fact I’ll be glad if I end up being wrong. Unfortunately, the economic and monetary developments in the 21st century indicate that politics trump over common economic sense.

Editor’s Note: This article was submitted as part of Seeking Alpha’s 2023 Market Prediction contest. Do you have a conviction view for the S&P 500 next year? If so, click here to find out more and submit your article today!”

Be the first to comment