John Kevin

Impressive rally in both the US stock, bond, and international equity markets this week. That will be discussed in another post since this update will focus on S&P 500 earnings. However (quickly), the S&P 500 as of 11/11/22 was down -15.13% YTD, while the Barclays Agg was down -13.85%, leaving the 60%/40% balanced portfolio down -14.62%, a full 5.5% improvement from the -20.11% return as of 9/30/22.

S&P 500 data:

- The forward 4-quarter estimate (FFQE) fell to $225.20 from last week’s $226.72 or a sequential decline of -0.67%, the smallest sequential decline of the last 3 weeks

- The forward P/E is now 17.7x after the near 5% rally in the S&P 500

- The S&P 500 earnings yield fell to 5.64% from last week’s 6.01%

- The Q3 ’22 bottom-up estimate fell to $55.90 vs. last week’s $55.97, still above $55

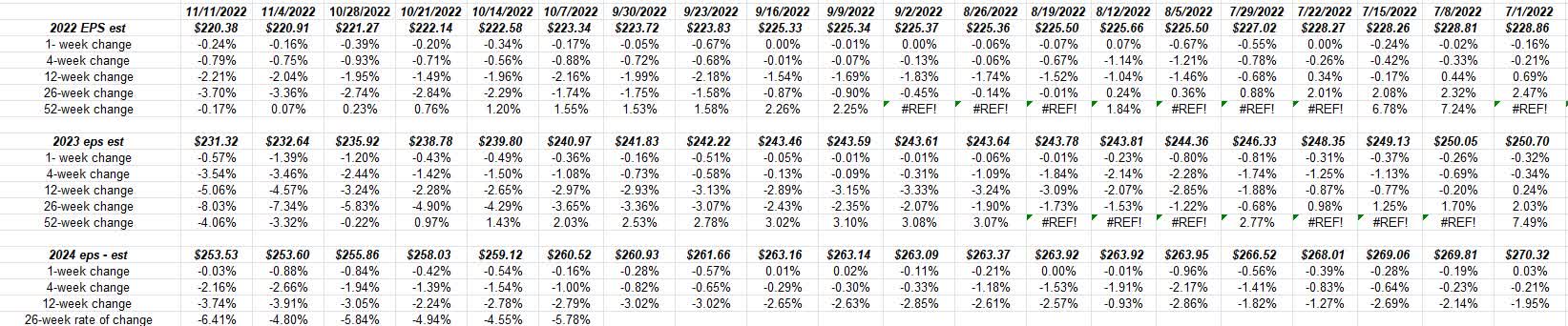

Rates-of-change:

Author

Expand this spreadsheet and then examine the three years from 2022-2024: the 2023 EPS estimate is degrading faster than 2022, although the 2022 “52-week rate of change” went negative this week for the first time. (This was discussed last week, too.)

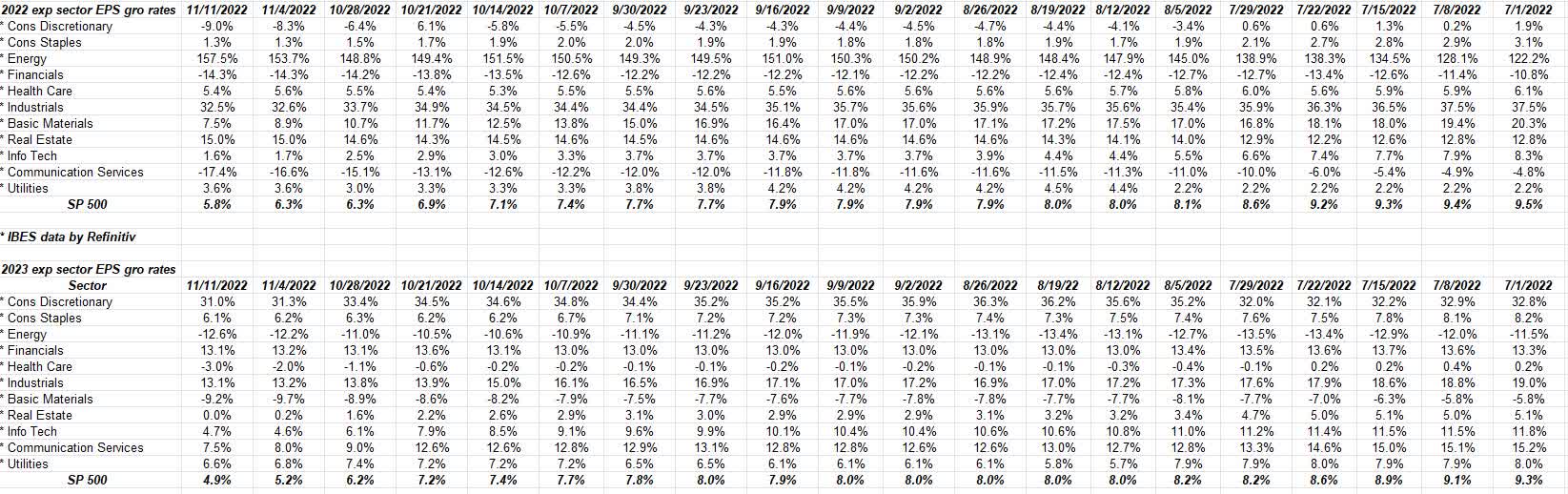

Sector updates: 2022 and 2023:

Author

Four sectors are expected to show faster EPS growth rates in 2023 (vs. 2022) as the forecasts stand today: Consumer Discretionary, Consumer Staples, Financials, and Utilities.

Take that with a dose of skepticism.

Summary/conclusion: The 3rd quarter, 2022, S&P 500 earnings season ends unofficially this week with Walmart’s report on Tuesday morning. Q4 ’22 S&P 500 EPS estimates have been coming down but that’s not a surprise if you’ve been reading this blog, since 2023 has been weakening too.

The relationship between changes in the S&P 500 forward EPS estimates and the 10-year Treasury yield makes for an interesting discussion. There is no question, a less restrictive Fed policy will help take the edge off the bond market, but it will also help the S&P 500 as well. Four separate 75 bp increases in the Fed funds rate in 2022, and yet the S&P 500’s worst YTD decline in terms of end-of-week calculations was on 9/30/22 when the S&P 500 was down -23.93 YTD.

If you had asked me in January ’22 what would be the YTD return in the S&P 500 after four 75 bp increases in the Fed funds rate, I would have speculated or guessed that it would have been a lot worse than down 23% – 24% YTD.

Throw in the incredible dollar strength this year and the S&P 500 and the stock market in general has absorbed quite a beating in 2022 and yet has held up pretty well (in my opinion).

This blog post from last week was prescient, but truly that’s not a boast, and last week’s blog post wasn’t a prediction either. CNBC is loaded every day with various predictions about many different stocks, and asset classes and it’s almost a comedy of errors. Evaluate “risk vs. reward” and be patient. International and non-US asset classes given the 10- and 15-year annualized returns look particularly compelling. Clients are still long the Oakmark International Fund (OAKIX) and the EMXC or emerging markets ex-China ETF. Using the American Funds Growth Fund of America as a growth stock proxy, the fund was up 5% this past week.

On a personal note, my 40th reunion from undergrad was held this past weekend, and it was in 1980 – during a Money & Banking class that was taught by an official from the Cincinnati Federal Reserve – that the Fed funds rate hit 20% under Paul Volcker and the 30-year Treasury traded to 15%. Watching the 10-year Treasury yield hit 53 basis points in late July 2020, just a few weeks before the Jackson Hole economic conference started, was really like watching your life come full circle.

The general opinion is that the S&P 500 could be in for another leg lower as the S&P 500 earnings continue to deteriorate. No question the forward estimates are under pressure. I’m not going to argue with that notion or assumption, but only say that an enormous amount of damage has been done YTD from P/E compression, so the switch can flip if the bond market pressure eases in terms of consistently higher yields, and there could be seen a longer period of P/E expansion, like the early 1990s.

It’s going to be tight (as they say) whether lower forward EPS estimates can be offset by steadier long-term yields.

Anyway, take everything here with a grain of salt and substantial skepticism. It’s one opinion. Past performance is no guarantee of future results, and nothing here today may be updated or brought current. Capital markets can change quickly, for better and worse.

Thanks for reading.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment