David Ramos

Thesis

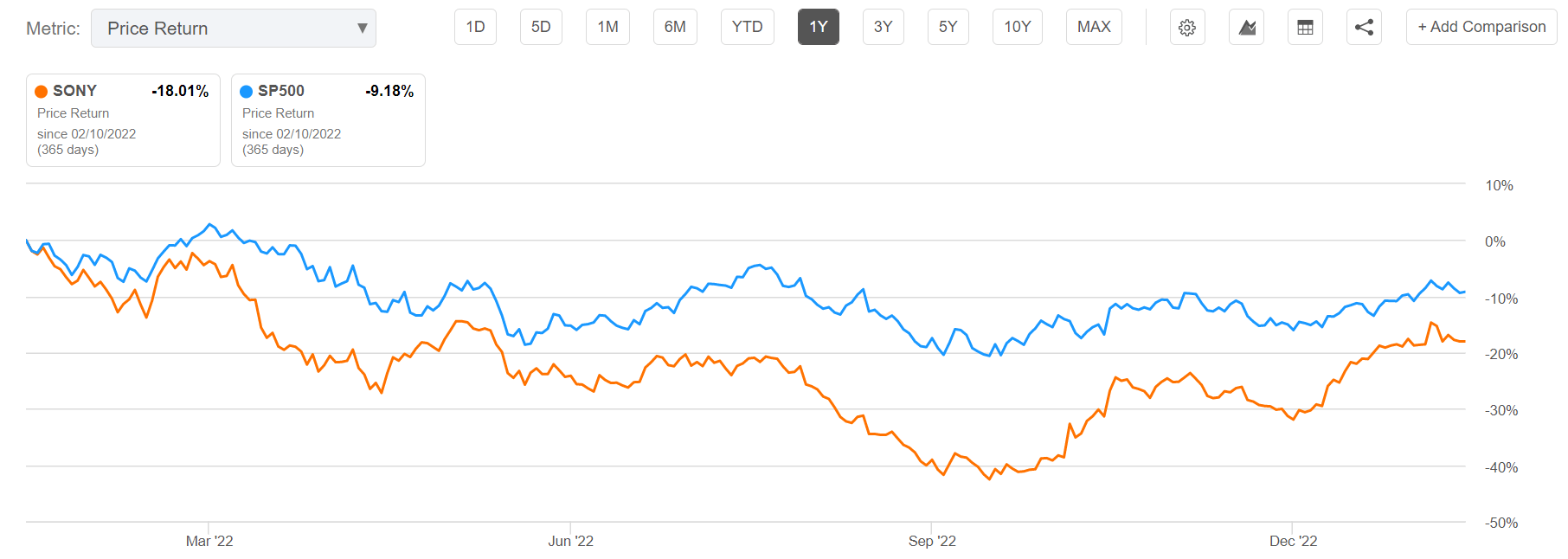

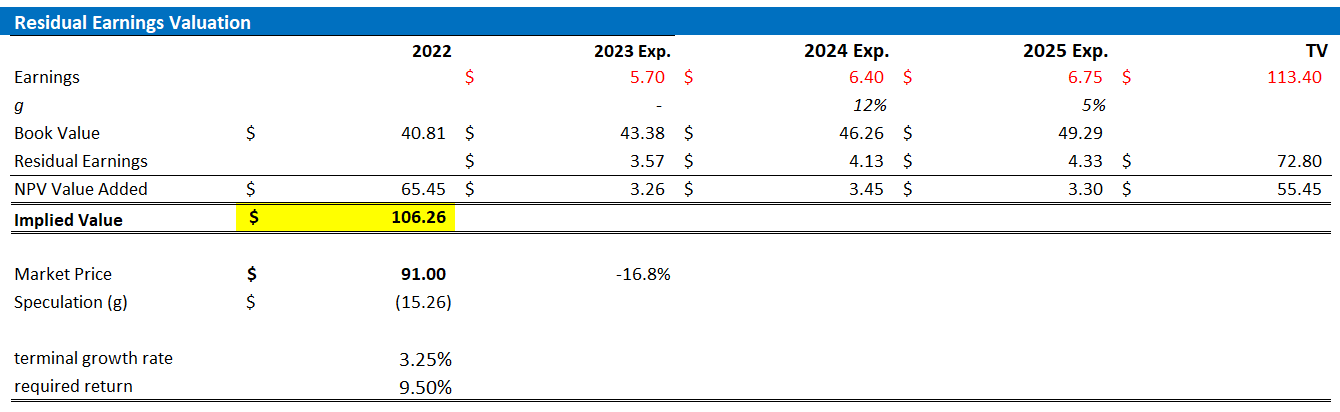

Sony (NYSE:SONY) is up about 25% since I have upgraded the Japanese electronics and entertainment conglomerate to ‘Buy’. And reflecting on a solid Q3 FY 2022 performance, with stronger than expected PlayStation 5 momentum, I continue to believe that Sony stock could appreciate in value. In fact, anchored on EPS upgrades through 2025, I update my residual earnings valuation model and now calculate a fair implied share price equal to $106.26/share. Reiterate ‘Buy’ rating.

Seeking Alpha

Sony’s December Quarter

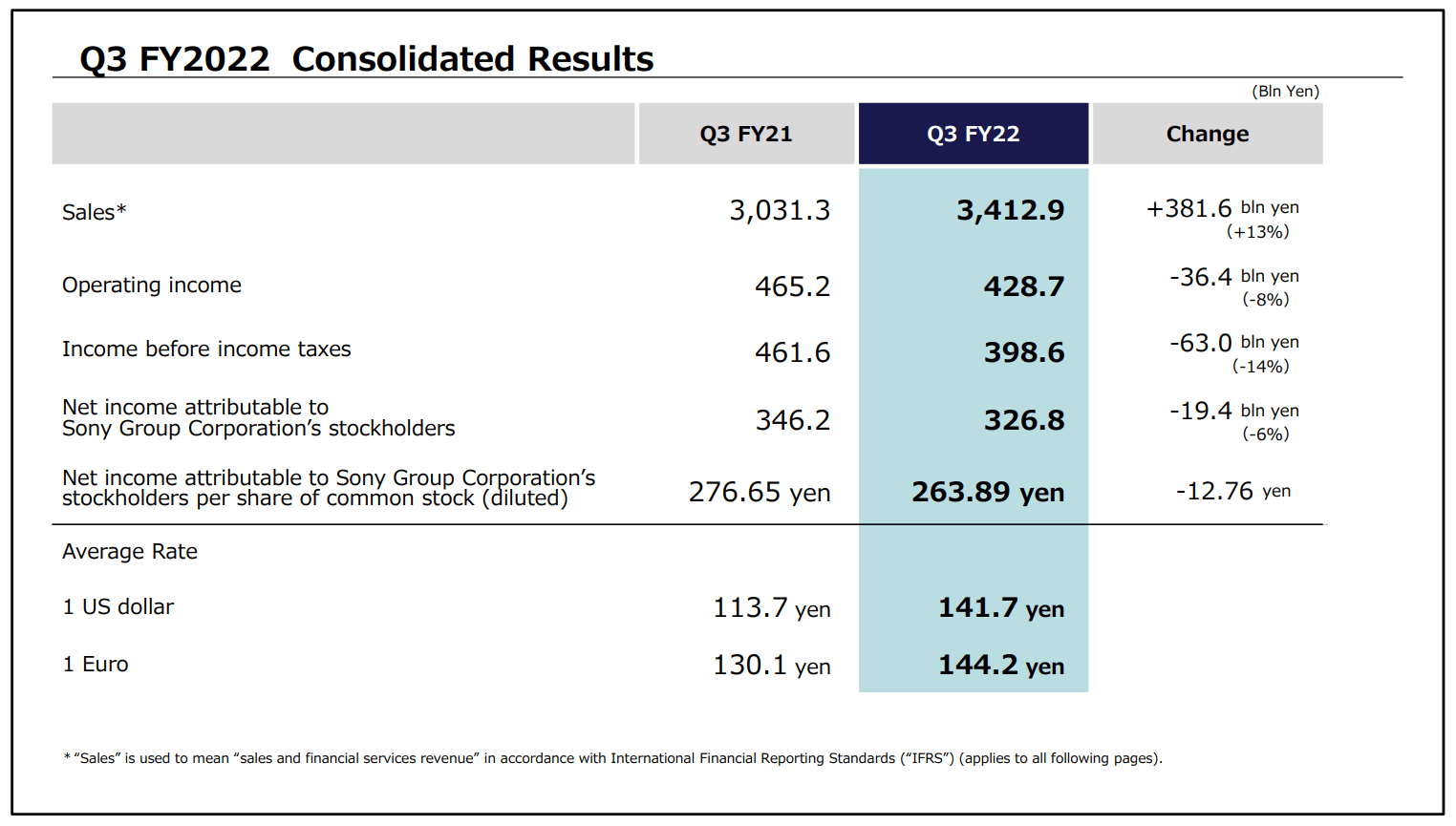

Despite a challenging macroeconomic environment that pressured results of many leading electronics and entertainment companies, including Apple (AAPL), Samsung (OTCPK:SSNLF) and Microsoft (MSFT), Sony delivered a solid holiday quarter. During the period from September to end of December, the PlayStation maker generated total group sales of approximately 3.4 trillion yen, an increase of about 13% as compared to the same period one year earlier. Although consolidated operating income declined by nearly 36.4 billion yen, to 428.7 billion yen, (8% year over year contraction), Sony’s earnings came in above expectations–and remained relatively close to the previous fiscal year’s profitability record.

Similarly, Sony’s income before income taxes decreased by about 14% year over year, to 398.6 billion yen, and the net income attributed to Sony shareholders fell by approximately 6%, to 326.8 billion yen.

Sony Q3 FY 2022 reporting

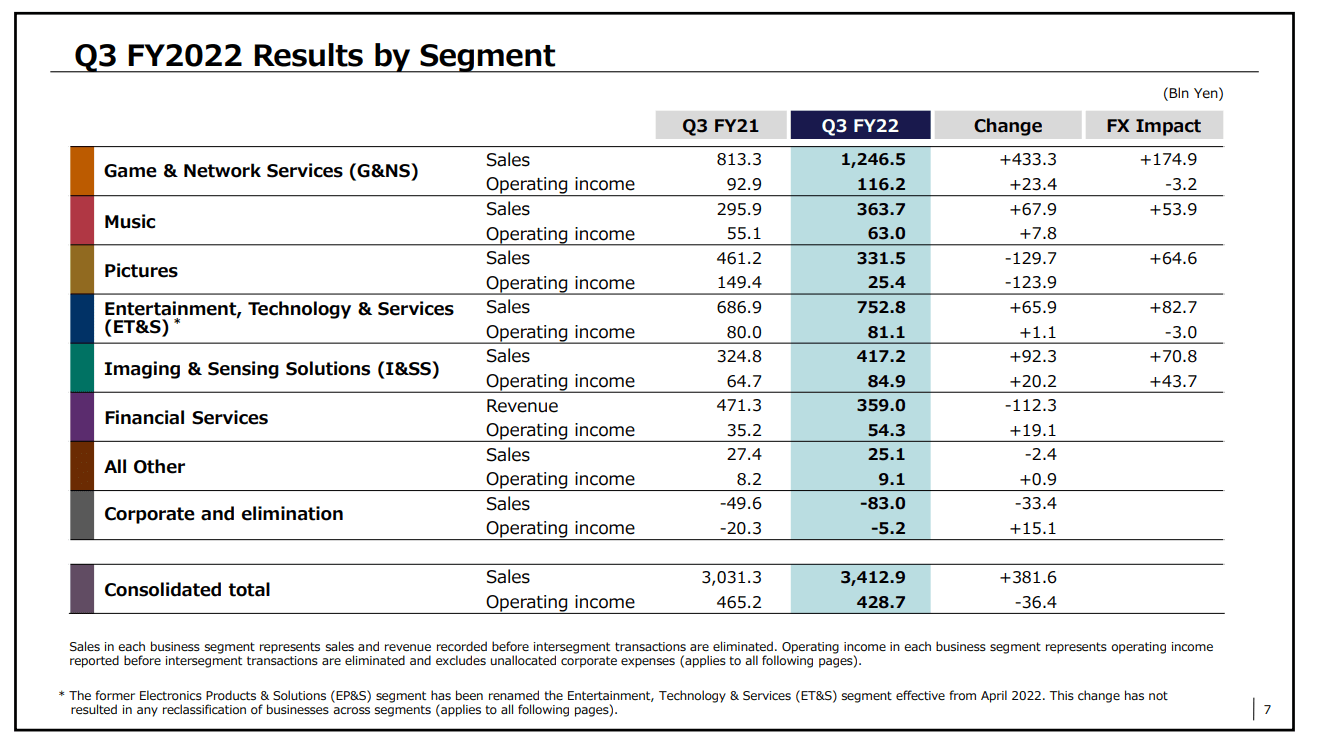

Sony’s solid Q3 2022 performance was supported by a material sales increase in the company’s G&NS, I&SS and Music segments, partially offset by a contraction in the group’s Pictures and Financial Services segments.

Moreover, given the weakening Japanese yen, Son has disclosed that the currency tailwind during the 2022 holiday quarter accounted for about 15 percentage points. And on a constant currency basis, group sales would have decreased by approximately 2%.

Sony Q3 FY 2022 reporting

The PlayStation Ecosystem Continues To Expand

Sony’s Q3 2022 results were supported by a strong G&NS segment. And the G&NS segment was supported by an expanding PlayStation ecosystem. During the quarter, Sony sold 7.1 million PS5 hardware units, bringing the total cumulative PS5 sales to over 32 million. Notably, during the investor and analyst conference following the earnings announcement Sony management commented that PS5 sales could have been even higher absent supply chain restrictions:

We by no means see sales of 7.1 million units as a poor showing, but we are still not getting enough units to our customers because of persistent production and logistical constraints. Units are not making it to all the stores in the various sales channels, so we want to work out any kinks we may have in our operations so that we can deliver more hardware to customers as quickly as possible. We are not very worried about the momentum of demand at present. Our focus has shifted to ensuring that our operations are robust so that we can deliver more units quickly …

Adding that:

… we are not seeing any pronounced differences based on geography at present. The PS5’s share of the European market remains high relative to our competitors, and after having shrunk somewhat during the summer, its share of the US market has also grown recently, widening the gap between ourselves and our peers. We are not seeing much in the way of impact from the macroeconomy at present, but that is subject to change, so we intend to keep a close eye on the situation in the fourth quarter and beyond.

Moreover, Sony also disclosed that the PS5 is accreditive to user base expansion and engagement: Firstly, Sony said that the engagement metrics of PS5 users who transitioned from PS4, such as their PS Plus subscription rate, gameplay time, and average spending, are higher than those when they used PS4. Secondly, Sony estimates that nearly 30% of PS5’s monthly active users are new to the PlayStation platform, indicating progress in expanding the ecosystem’s user base. Overall, although total gameplay time for all PlayStation users during the quarter decreased by about 3% year over year, the same metric increased 6% compared to the previous quarter and 14% in December compared to the previous month.

Sony Raised FY 2022 Profit Outlook

On the backdrop of a strong PS5 demand, and after beating earnings estimates in Q3, Sony raised its profit outlook for the fiscal year 2022. The company now expects PS5 sales to top 19 million units, as compared to 18 million previously.

In addition, software sales are also encouraging. The newly launched game “God of War Ragnarök” has reportedly achieved sales of over 11 million copies in its first 10 weeks since its release on November 9th, making it the fastest-selling first-party title in the company’s history. Looking ahead to the next fiscal year, Sony has a strong lineup of both first-party and third-party titles planned for release, including “Marvel’s Spider-Man 2” and “Destiny 2: Lightfall”.

According to company estimates, the stronger than expected performance from G&NS could add about 20 billion yen to the conglomerate’s FY 2022 profitability, bringing operating profit forecast to 1.18 trillion yen (as compared to 1.16 trillion yen estimated previously).

Valuation: Update Target Price

Reflecting on strong Q3 FY 2022 reporting, I now estimate that SONY’s EPS in 2023 will likely expand to somewhere between $5.6 and $5.8. Moreover, I also slightly raise my EPS expectations for 2024 and 2025, to $6.4 and 6.75, respectively.

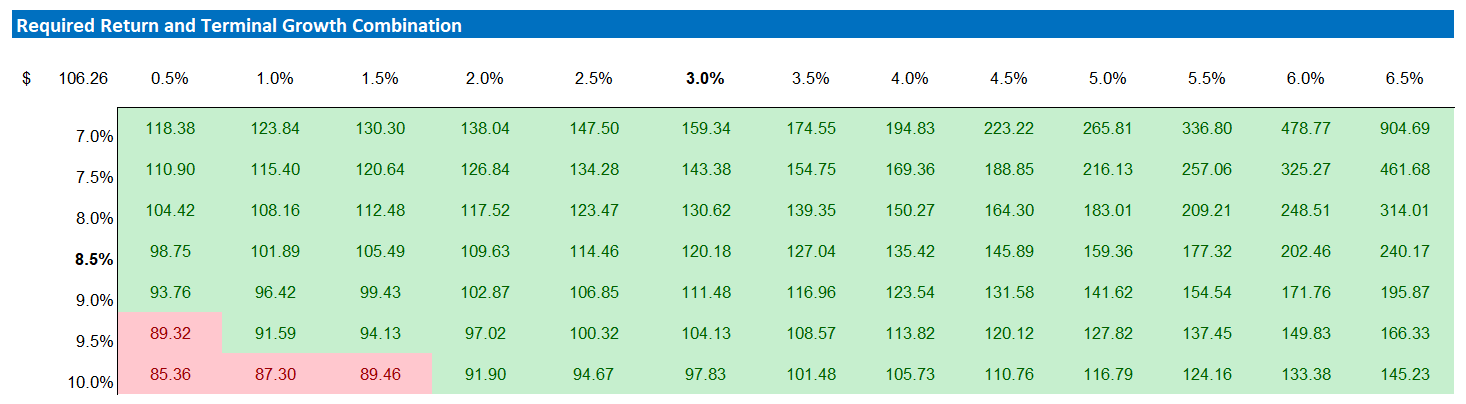

I continue to anchor on a 3.5% terminal growth rate (one percentage point higher than estimated nominal global GDP growth), and a 9.5% cost of equity capital requirement.

Given the EPS updates as highlighted below, I now calculate a fair implied share price of $106.26.

Author’s EPS Estimates & Calculation

Below is also the updated sensitivity table.

Author’s EPS Estimates & Calculation

Risks

As I see it, there has been no major risk-updated since I have last covered Sony stock. Thus, I would like to highlight what I have written before:

I think Sony is relatively low-risk at current valuation levels. However, investors should monitor the following headwinds that could cause Sony stock to materially differ from my target price: 1) slowing consumer confidence due to inflation outpacing wage growth and rising interest rates could cause a temporary slowdown in Sony’s sales number of discretionary consumer products; 2) loss of competitive advantage in various business segments such as PC and smartphones given accelerating industry competition; 3) higher than expected R&D investments in order to realize new product initiatives and/or to defend competitive positioning; 4) macroeconomic uncertainty relating to the monetary policy actions; 5) That said, much of Sony’s share price volatility is currently driven by investor sentiment towards risk and growth assets. Thus, investors should expect price volatility even though Sony’s business outlook remains unchanged.

Conclusion

Sony delivered a solid holiday quarter, despite a challenging macroeconomic environment that pressured results of many leading electronics and entertainment companies. The PlayStation maker, supported by strong G&NS performance, generated total group sales of approximately 3.4 trillion yen, an increase of about 13% as compared to the same period one year earlier. On the backdrop of a strong PS5 demand, and after beating earnings estimates in Q3, Sony raised its profit outlook for the fiscal year 2022.

Anchored on EPS upgrades through 2025, I update my residual earnings valuation model and now calculate a fair implied share price equal to $106.26/share.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment