Jerod Harris/Getty Images Entertainment

Sound tremendously influences how many of us live our lives. From the toe-curling scrape sound of nails on a chalkboard, to the monotonous droning of the news on TV, to the pleasant sound of music emanating from our headphones, sound has a profound impact on those who can experience it. One company dedicated to innovating sound technology is none other than Sonos (NASDAQ:SONO). Over the past several years, the business has done incredibly well to grow its top line. Profitability has always been a bit mixed, but that trend has also been positive. Most recently, we have seen revenue continue to climb even as profitability takes a slight step back. But on the whole, shares of the company don’t look unreasonably priced. Add on top of the pricing of the firm the fact that it has cash in excess of debt in the amount of $606.7 million, and to me it looks like a fairly attractive ‘buy’ prospect at this point in time.

Sound pays

According to the management team at Sonos, the company operates as one of the leading sound experience brands. Today, the firm’s portfolio of products is vast and it would be useful for investors to understand that. At present, the company’s products are broken up into different categories. For instance, under the Sonos Speakers category, the company offers a number of products such as the ultra-portable smart speaker known as Roam. It also sells a premium smart sound bar for TV, movies, music, gaming, and other activities under the Arc product name. Five is another product that operates as a high-fidelity speaker that has been redesigned over the years. The list goes on.

There are, of course, other product categories that the company has. Under the Sonos System Products line, for instance, it offers the Port, which is a versatile streaming component that is used for stereos or receivers. The Amp is an amplifier powering its customers’ entertainment. And the Boost product offering is a simple WiFi extension that can be used for uninterrupted listening for its customers. The company also has what it refers to as the Partner Products and Other category. This comprises a variety of other products the company has, some in partnership with other firms like IKEA and Audi. Examples of specific products would include the accessories that it sells such as mounts, stands, shelves, cables, chargers, etc. It also has a free, ad-supported streaming radio offering that reaches over 60,000 stations that is known as Sonos Radio, as well as a premium version known as Sonos Radio HD. Just as important to the company as its physical products is also the software it produces. One example would be the Sonos S2, which the company has described as being a new app and operating system that will enable the company’s new product lines and other offerings that also happens to include new features, usability updates, and user personalization.

Author – SEC EDGAR Data

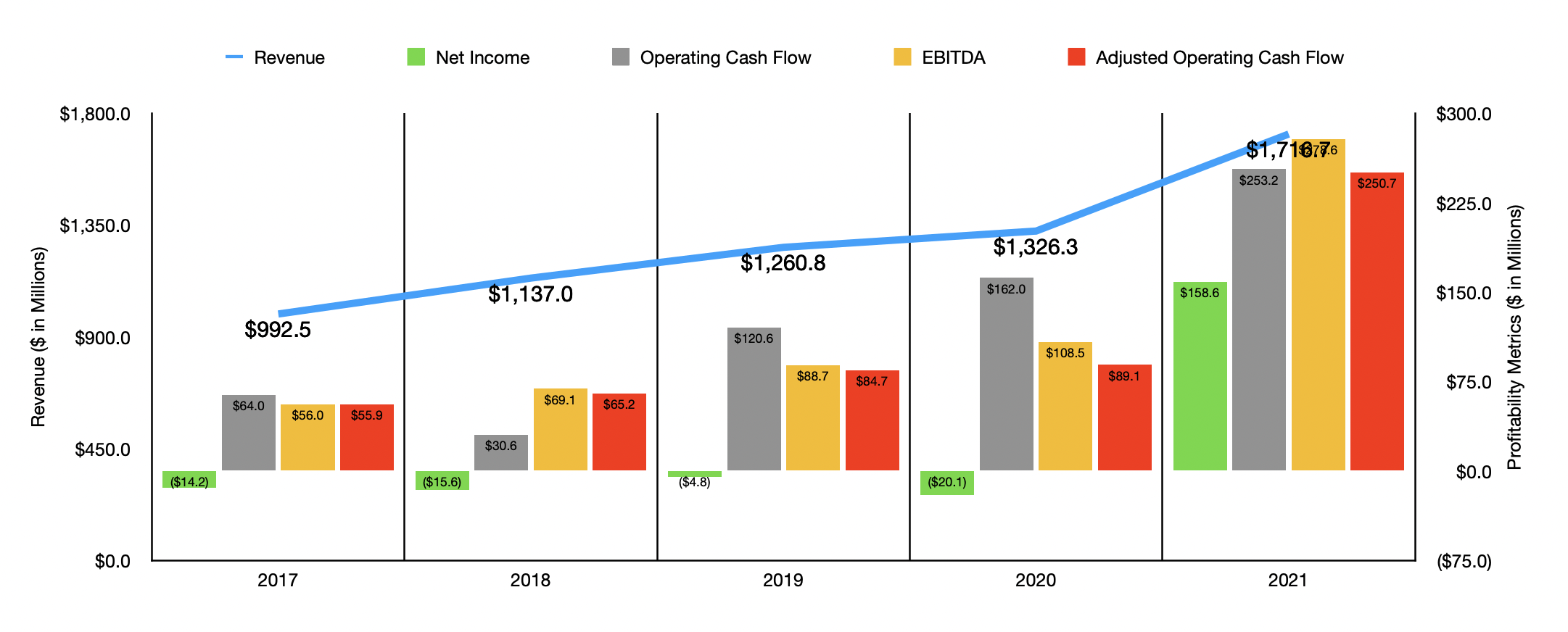

Over the past few years, the management team at Sonos has done a really good job growing the company stop line. Revenue jumped from $992.5 million in 2017 to $1.72 billion in 2021. The biggest leap for the company came from 2020 to 2021, when sales skyrocketed by 29.4%. This number would have been even higher at 31.9% had an op in for a 53rd week in the 2020 fiscal year. This increase in sales was driven in part by a 12% increase in the number of products sold, a number that grew from 5.806 million to 6.503 million. The greatest amount of growth came from the company’s line of speakers, with sales climbing by 33.2% year over year. The rest of the increase was attributed to higher pricing and favorable changes in product mix.

Profitability for the company has been a bit of a mess. In the four years ending in 2020, the company generated consistent net losses. However, in 2021, it generated a net profit of $158.6 million. Operating cash flow has largely increased over the years, rising from $64 million in 2017 to $253.2 million last year. If we adjust for changes in working capital, it would have risen from $55.9 million to $250.7 million. Meanwhile, EBITDA for the company increased from $56 million to $278.6 million over the same window of time.

Author – SEC EDGAR Data

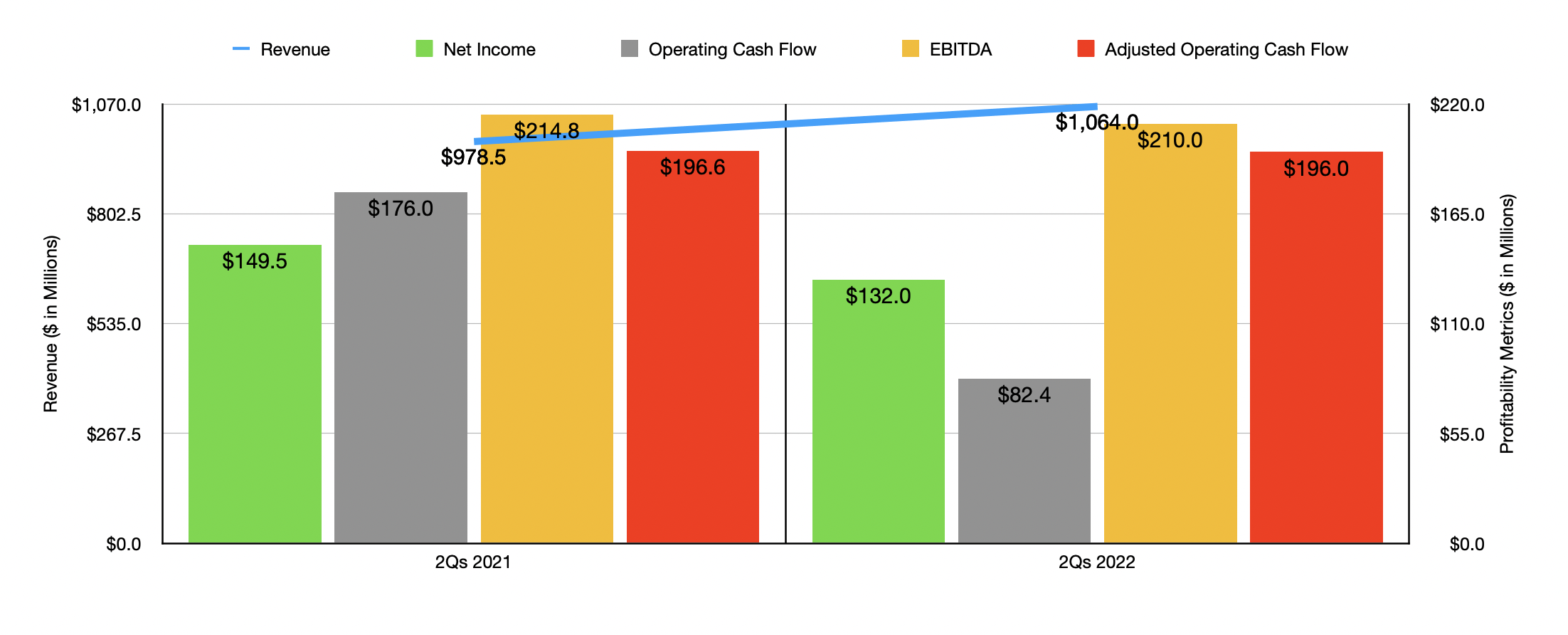

Results so far for the 2022 fiscal year have been somewhat mixed. Revenue in the first half of the year came in at $1.06 billion. That compares favorably to the $978.5 million generated in the same time of the 2021 fiscal year. At the same time, however, profitability did suffer. Net income declined from $149.5 million to $132 million. Operating cash flow plunged from $176 million to $82.4 million. If we adjust for changes in working capital, it still would have fallen from $196.6 million to $196 million. During that same time, EBITDA also fell modestly, dropping from $214.8 million to $210 million.

When it comes to the 2022 fiscal year as a whole, management does expect sales to come in fairly strong at between $1.95 billion and $2 billion. That would be somewhere between 14% and 16% above what the company generated in 2021. This increase in sales may be driven in part by acquisition-based activities, such as the company’s announced purchase, in April of this year, of Mayht in exchange for $100 million in cash. The only profitability metric that management gave guidance on was EBITDA. This is forecasted to come in at between $290 million and $310 million. If we assume that other profitability metrics will increase at the same rate that this one should, we should anticipate adjusted operating cash flow of around $270 million and net income of roughly $170.8 million.

Author – SEC EDGAR Data

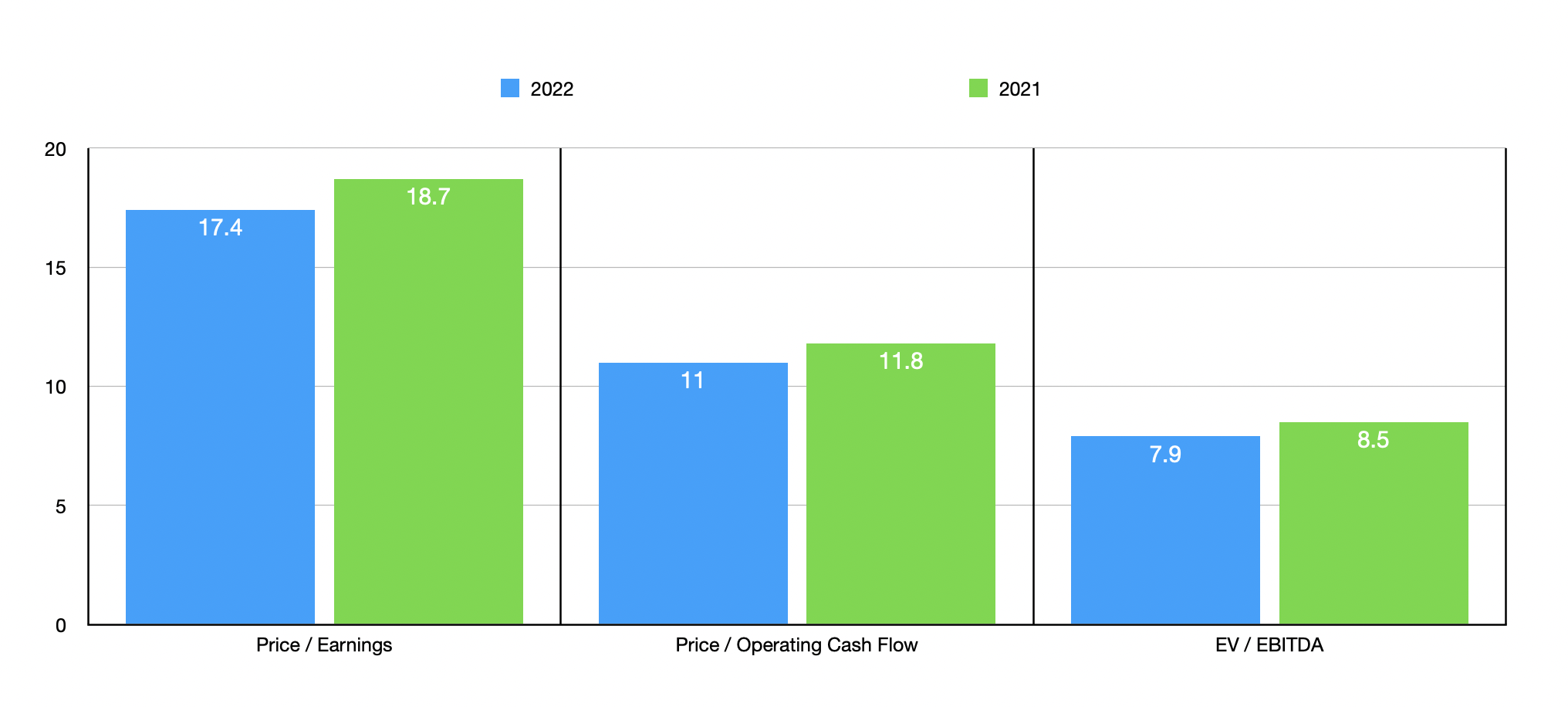

Using this data, we can see that shares of the company are not all that pricey. On a price-to-earnings basis, the company does look slightly lofty with a multiple of 17.4 on a forward basis. Though this does compare favorably to the 18.7 reading we get if we rely on 2021 results. The price to adjusted operating cash flow multiple should drop from 11.8 using last year’s results to 11 this year. And the EV to EBITDA multiple should drop from 8.5 to 7.9. Truth be told, there aren’t very many good companies to compare this one to. I did find three that I felt were fairly appropriate. On a price-to-earnings basis, these companies range from a low of 2.8 to a high of 79.6. And using the EV to EBITDA approach, the range was from 5 to 19.2. In both cases, two of the three companies were cheaper than Sonos. Meanwhile, using the price to operating cash flow approach, only one of the three firms had a positive reading and that was of 6. In this case, Sonos would be more expensive.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Sonos | 17.4 | 11.0 | 7.9 |

| Nikon Corporation (OTCPK:NINOY) | 12.1 | N/A | 5.0 |

| GoPro (GPRO) | 2.8 | 6.0 | 7.3 |

| Snap One Holdings (SNPO) | 79.6 | N/A | 19.2 |

Takeaway

Although I am a fan of comparing firms to other similar businesses, in this case, I wouldn’t put too much weight in that approach. Instead, I would rely on the company’s historic track record and on its pricing on an absolute basis. The fact of the matter is that recent performance has been quite strong. Although profitability has shown signs of weakening in the first half of this year, management seems to think that picture will improve in the second half of the year. No, I don’t think that this particular prospect is a strong opportunity for investors. But it could offer some upside potential from here. So because of that as well as the excess cash on the company’s books, I have decided to rate the business a soft ‘buy’ for now.

Be the first to comment