Soluna Burdened By Preferred Shares Commitment

EduLeite/E+ via Getty Images

Introduction

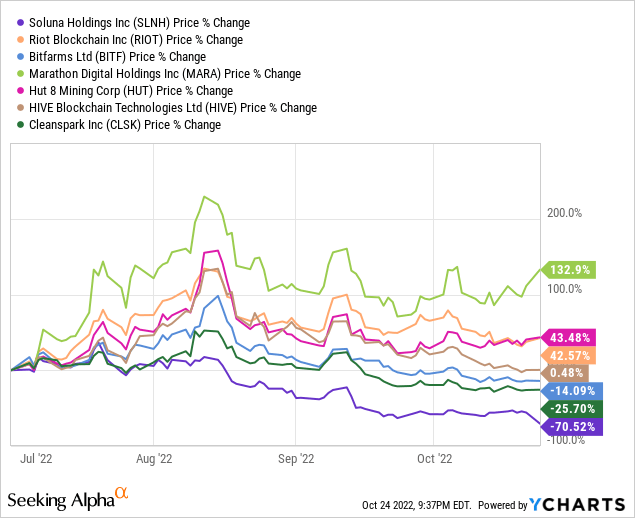

In our previous coverage, we argued that Soluna Holdings’ (NASDAQ:SLNH) curtailed energy business model isn’t sustainable due to efforts in reducing curtailed energy (SLNH’s main source of income). In addition, SLNH’s foreseeable capacity (Q3: 1.02 EH/s) severely lags behind the industry (Table 1). At the very least, these imply limited upside potential. At that time of writing, Soluna was trading (market cap = ~$63.5mil) above its adjusted book value ($37.15mil = $2.8mil cash + $68.245mil PP&E + $14.90 prepaid – $48.8 Total Liability), implying excessive downside risk. The combination of limited upside potential and excessive downside risk suggests that Soluna could not offer sufficient margin of safety. So far, Soluna’s share price has reflected this pessimistic outlook where the company has severely underperformed the industry (Fig 1).

Our thesis was further validated by SLNH itself when it announced that it has priced its previously announced public offering at $1.44 per share, about 20% lower than the market price before the announcement. To make things worse, SLNH’s share price has suffered another leg down and is trading at $1.20.

In light of SLNH’s Q2 performance, this article aims expand our initial analysis to uncover an additional downside risk and examine whether SLNH offers a sufficient margin of safety after the 70% decline since our previous coverage.

Table 1. Near-term Expected Capacity Comps

| Miners | Near-Future Expected Capacity (EH/s) |

| Soluna Holdings | 2.62 (End of 2022) |

| Marathon Digital (MARA) | 23 (mid-2023) |

| Bitfarms (BITF) | 6 (End of 2022) |

| Hut 8 Mining (HUT) | 3.5 (End of 2022) |

| Riot Blockchain (RIOT) | 12.8 (2023Q1) |

| CleanSpark (CLSK) | 5 EH/s (end of 2022) 22.4 EH/s (end of 2023) |

Source: Author

Fig 1. Soluna Severely Underperformed The Industry (YCharts)

Another Potential Victim From Overcentralizing in Texas

We explained that Texas offers low-cost energy, crypto-mining-friendly regulations, and opportunities in the curtailed energy market due to local transmission constraints. As a result, many major Bitcoin mining companies have decided to locate the majority of their Bitcoin mining operations in Texas. This decision may also prove problematic for these Bitcoin mining companies because Texas’s power grid has suffered from overheating and potential blackouts in summers and winters.

- During the 2022 summer, Bitcoin miners in Texas had to halt mining operations to prevent blackouts from the summer heat.

- During the 2021 winter, Bitcoin miners also had to halt mining operations to prevent blackouts due to winter storms. The winter storm was particularly devastating which saw 10 million Texans without electricity and hundreds of casualties.

Due to these events, scrutiny on crypto mining activities in Texas is gathering momentum while the Electric Reliability Council of Texas (ERCOT) has recently announced a slowing of application approvals. These events could significantly impact SLNH’s expansion plans in the state because SLNH has yet to obtain approval from ERCOT to energize Project Dorothy, as of September 2022.

Currently, SLNH’s operations are located mainly in Kentucky (50MW: Project Sophie, Project Marie). In the short run, Project Dorothy (50MW) is expected to provide 50MW capacity by 2024Q4. This represents ~60% (=1.4 EH/s / 2.4 EH/s) of SLNH’s total mining capacity.

Over the long run, Project Dorothy is expected to provide 150MW of capacity, representing over 75% of SLNH’s total Bitcoin mining operation. If we were to consider SLNH’s 2 other projects in Texas (Project Kati: 150MW; Project Cynthia: 130MW) over a longer time horizon (no timeline yet), over 90% of Soluna’s operation will be located in Texas.

Therefore, there is evidence of over-centralization risk which further adds to the downside. We showed that these events could undo MARA’s 23 EH/s capacity expansion efforts and now the same can be applied to SLNH.

SLNH’s Mining Efficiency is Average at Best

Another claim by Soluna is that the company has one of the lowest Bitcoin mining cost in the industry:

Soluna remains one of the lowest-cost Bitcoin miners, and we believe the terms of this new agreement strongly insulate it from recent fluctuations in fuel charges.

We’re not aware of the basis of the claim, but we found contradictions compared to our findings. When we compare to other Bitcoin miners (both big and small; Table 2), we can see that SLNH’s Bitcoin mining cost efficiency is average at best. When other business costs are included, SLNH is severely underperforming the industry (Table 3).

That being said, we should give SLNH credit for matching HUT’s and RIOT’s mining costs despite being 69% smaller than HUT (= 0.87 EH/s SLNH / 2.78 EH/s HUT; Q2 basis), and 80% smaller than RIOT (= 0.87 EH/s SLNH / 4.44 EH/s RIOT; Q2 basis).

Another positive take is that Project Dorothy is expected to increase Bitcoin production more than the increase in non-operating costs, which will ultimately reduce all-in business costs per BTC. Project Dorothy is expected to more than double Bitcoin production (from 3.6 BTC per day to 8 BTC per day) by 2022Q4.

However, this positive observation is quickly offset by the risks from ERCOT approval and a bearish Bitcoin outlook. Moreover, we need 2 to 3 more quarters to confirm the positive observation.

Table 2. Cost of Revenue (Excl. Depreciation) Comps

| Miners | Cost of Revenue (CoR, Excl. Depreciation) |

| SLNH | 2022Q2: $13,500 = $3.6mil CoR / 267 BTC mined2022Q1: $14,000 = $2.671mil CoR / 226 BTC mined |

| MARA | 2022Q2: Invalid due to Montana One-Off Disruption2022Q1: $6,240 = $7.86mil CoR / 1,259 BTC mined2021Q4: $6,500 = $7.1mil CoR / 1,098 BTC mined |

| BITF | $12,000 |

| HUT | Q2: $20,200 = $19.1mil CoR / 946 BTC minedQ1: $13,800 = $13mil CoR / 942 BTC mined |

| RIOT | Q2: $12,900 = $18mil CoR / 1,395 BTC minedQ1: $13,500 = $19mil CoR / 1,405 BTC mined |

| CLSK | Q2: $9,600 = $10.3mil CoR / 964 BTC mined |

Table 3. All-in Business Cost per BTC Comps

| Miners | All-in Business Costs per BTC |

| SLNH | 2022Q2: $74,000 = $19.74 all-in cost / 267 BTC mined |

| MARA | 2022Q2: Not valid2022Q1: $31,700 = $40mil all-in costs / 1,259 BTC mined2021Q4: $32,240 = $28.57mil all-in costs / 1,098 BTC mined |

| BITF | 2022Q2: $36,700 = $34.3mil (excl. Financial Gains) / 1,2572022Q1: $34,340 = $33mil / 961 BTC mined |

| HUT | 2022Q2: $49,500 = $46.8mil all-in costs / 946 BTC mined2022Q1: $40,750 = $38.4mil all-in costs / 942 BTC mined2021Q4: $40,200 = $31.7mil all-in costs / 789 BTC mined |

| RIOT | 2022Q2: $35,300 = $49.3mil all-in costs / 1,395 BTC mined2022Q1: $30,800 = $43.25mil all-in costs / 1,405 BTC mined |

| CLSK | 2022Q2: $37,800 = $36.4mil all-in costs / 964 BTC mined |

Valuation

In our previous studies, we explained how different Bitcoin mining companies raise money for expansion and operation. MARA is more leveraged compared to peers where total liability ($0.76bn) is 53% of total adjusted assets ($1.445bn), which is detrimental to its equity-based valuation. In comparison, SLNH’s total liability ($41.4mil) is 40% of adjusted total asset ($102.33mil = $4.63mil cash + $87mil PP&E + $10.7mil prepaids).

Unlike MARA (which has no preferred stock outstanding), SLNH carries the burden of preferred stock. As of Q2, SLNH has 3mil preferred stock 3mil outstanding 9.0% $25 liquidation preference Series A cumulative perpetual preferred stock. In other words, SLNH received less than $75mil “perpetual loan” funding (because preferred shares are issued at lower prices) but has to pay interest on a $75mil loan. If SLNH were to buy back all 3mil outstanding preferred shares today, it’ll theoretically cost SLNH about $12mil (=$4 x 3mil). Depending on how investors want to look at it, SLNH’s total liability + preferred stocks ($53.4mil) would at least be 52% of its adjusted total assets, similar to MARA.

Therefore, SLNH’s adjusted book value would be at most $49mil (=$102.33-$53.4mil). On this basis, SLNH (market cap = $29mil) is now trading below its book value. But what stops SLNH from becoming an attractive investment is the lack of Bitcoin holdings.

The main attraction of a Bitcoin mining company trading below book value is the upside potential derived from the rebound in Bitcoin price. For instance, HUT’s current Bitcoin reserve alone would already be worth $587mil (= 8,388 BTC * $70,000) when Bitcoin reclaims its all-time high, more than its current $438mil market cap. SLNH does not possess such upside potential due to the lack of Bitcoin reserve nor does it possess the mining capacity (only ~1 EH/s) to derive such value.

Verdict

We’ve expanded our initial analysis on SLNH to uncover an additional risk from over-centralization and showed that SLNH is not positioned well to benefit from a Bitcoin recovery due to a lack of Bitcoin reserves and mining capacity. Furthermore, SLNH carries a heavy financial burden from the preferred shares outstanding during this period of distress.

Unfortunately, we have to maintain our verdict that SLNH still does not offer sufficient investment value proposition even after the 70% decline since our previous coverage. In addition, investors should also be concerned that Soluna has yet to fulfill its monthly preferred shares dividend commitment in October.

Be the first to comment