metamorworks

Investment action

Based on my current outlook and analysis of SolarWinds Corporation (NYSE:SWI), I recommend a hold rating. I expect the business to continue facing challenges in the near term that will keep growth at the current weak levels, making the comparative performance vs. peers much weaker. I believe investors that are investing in this space are more interested in profitable growth than FCF yield; hence, SWI should screen much weaker.

Basic Info

SWI designs and develops information technology management software. The company offers solutions such as network performance monitoring, configuration, virtualization, database management, hosted logs, security, and configuration. SolarWinds serves customers globally and hence taps into the global growth of this industry. Based on third-party research, the industry is expected to grow at a mid-single digit CAGR to a size of $33.9 billion in 2030 from $22.9 billion in 2022. While there are many estimates out there, using this estimate would imply that SWI has only around 3% of the global market share.

Review

Although I believe SWI to be a market leader in the context of network performance monitoring (based on Gartner’s research), I believe that the company faces a number of internal and external challenges that it must overcome before I will consider buying its stock. Among these difficulties is a slowing of customer growth, as evidenced by the sequential decline in customers spending over $100,000 to 933 (from 945). The net loss of large customers was 12, compared to gains of 56 in the first quarter of this year and 27 in the second quarter of last year. The macro environment remains also weak for SWI, and the company is seeing prolonged deal cycles among enterprise customers.

And the only variability that I will refer to is what I have previously alluded to, which is because of the macro situation in EMEA, some of the deal conversion cycles have been a bit more protracted. 2Q23 call

Since the macro environment did not significantly improve in the most recent quarter (2Q23), deal cycles continued to extend into the next quarter as customers became more cautious with their spending and demanded more approvals. Despite management’s confidence that these deals will continue to close in the coming quarters, I anticipate this situation will persist for some time, as businesses will likely remain cautious while monitoring the economic situation. Good news for the medium-term future is that deals are still in the pipeline, which means they are just waiting to be turned into revenue. Following the cyber security incident that affected its Orion Software Platform, SWI is also dealing with lower maintenance renewal rates in the near future. Putting everything together, I don’t think the business will be able to return to its historical low-teens growth rate from its current run rate growth in the low- to mid-single digits anytime soon.

Comparatively to peers like Datadog (DDOG), Splunk (SPLK), and Dynatrace (DT), the case to go long SWI becomes weaker as well. All of these comps are expected to grow at 10 to 20+%, which is way better than the low to mid-single digit growth expectation for SWI. While SWI has a better FCF yield profile, I believe investors that are investing in this space are not looking for yield; rather, they are looking for profitable growth given that the industry is still facing secular tailwinds.

On the other hand, if one looks at the stock for the medium term, there could be a case to buy SWI. Putting aside the short-term difficulties, SWI proved that margin growth is possible even in turbulent times. SWI increased its EBITDA by 18%, leading to margins of 42.8%, a significant increase of 470bps from the previous year. Subscription ARR increased to 33% from 30% in the previous quarter, which I interpret as a positive sign that the shift to subscriptions is gaining traction. Due to the positive trend, management increased their forecast for FY23 from $725 to $740 million to $740 to $748 million (note that this still points to low-single digit growth, but it does speak well of management’s view of growth trend). In addition, the FY23 outlook has shifted to call for an EBITDA of $308-$313 million, or 41.5% margin at the midpoint, up from the previous forecast of $295-$305 million, or 40.9% margin at the midpoint.

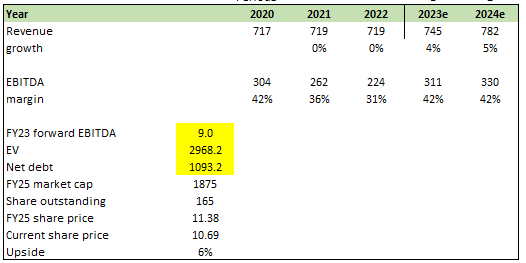

Valuation

Author’s work

I believe SWI will continue to see its growth stay within the current range, as I believe the near-term challenges will persist for a while. My assumption for 5% follows the same magnitude that management is guiding for FY23. I also remain conservative with regards to margin and assume EBITDA margin to stay flat in FY24. I also assumed valuation to continue to stay depressed when compared to peers for the reason stated above (SWI is the worst performing among peers, hence, should see lesser capital inflow).

Final thoughts

My recommendation for SWI is to hold. The company is currently facing near-term challenges that are likely to limit its growth potential, resulting in weaker performance compared to peers. These challenges include a slowdown in customer growth, extended deal cycles, and lower maintenance renewal rates due to a recent cybersecurity incident. Consequently, SWI’s growth is expected to remain in the low- to mid-single digits, significantly lagging behind peers like Datadog, Splunk, and Dynatrace, which are projected to grow at 10 to 20+%.

Be the first to comment