ArtistGNDphotography

SolarEdge Technologies (NASDAQ:SEDG) is responsible for designing, developing and selling direct current optimized inverter systems internationally. A large portion of their customers being solar companies who develop solar modules and the likes. Operating in different segments, they also offer residential areas with smart energy management solutions.

But valuations are important to me. At the current share price it seems too expensive and investors might be better of selling shares in the company. I think it will take time before the company manages to generate revenues that would support the current price. Until then, investors money could be spent better in other places. This makes me keep a sell rating for SolarEdge.

Expansion And Growing Their Market Share

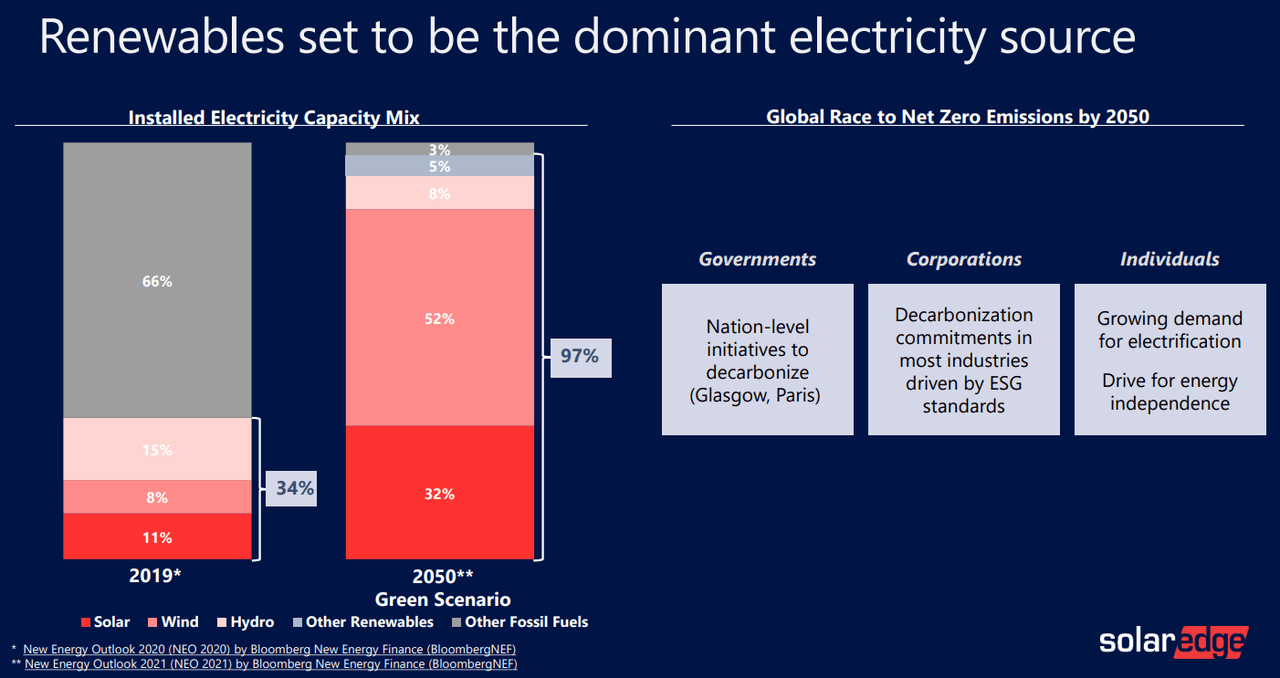

In their recent earnings report, SolarEdge Technologies provides some pretty optimistic outlooks for the entire solar industry in my opinion. The entire solar sector is expected to provide more than 30% of all energy in 2050, that would be almost 3x more than the current portion it provides.

For me, this signals there are tailwinds for the company’s path to become a large and more dominant player in the space. I believe a lot of the tailwinds will not only be because of companies choosing green energy sources, but also people living in residential areas wanting a “cleaner life”.

Potential Growth Tailwinds (SolarEdge Q3 Earnings Report)

SolarEdge Technologies offers an almost all-in-one product where they will provide you with their solar panels and also the entire ecosystem that comes along with their product. I think a product such as this will create customers coming back for more in years to come. Being that a large portion of their current sales are in residential areas, I believe word travels fast about the quality of their product. I’m confident in them executing their expansion plans and taking more market share. Since they are already present in 133 different countries I think a large part of that initial work has been done, now it’s up to them to establish themselves as “the solar panel company”.

Last Earnings Report Run-Through

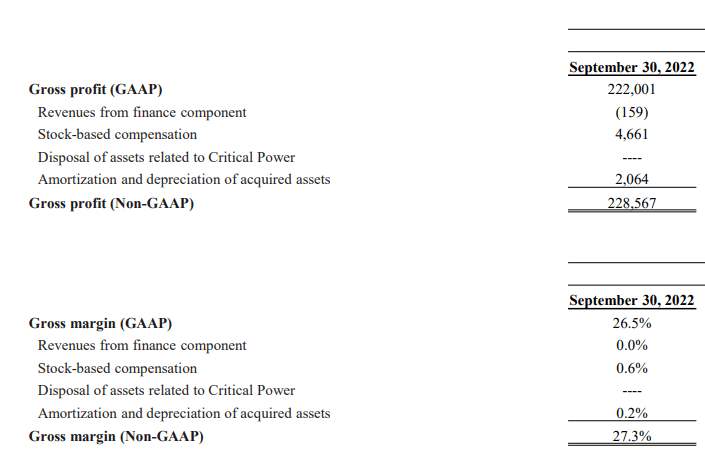

On November 7, 2022 SolarEdge Technologies provided investors with their Q3 earnings report. One of the highlights for me reading through the report was the company’s ability to reduce their operating expenses by quite a large portion compared to a year ago. With operating expenses making up 16% of total revenues, SEDG managed to reduce it by almost 4%, quite impressive in my opinion given the tougher economic climate that was 2022.

Another thing I noted was the still rapid increase in revenues. An increase of 56% YoY gives me confidence SolarEdge might someday catch up to its current valuation. A large portion of this increase in revenues comes from the back of more pressure to adapt to solar and renewable energy sources.

Revenue Sheet For SolarEdge (SolarEdge Q3 Earnings Report)

Even though the revenues were up by a good amount, the decrease of net income and in turn the EPS became something that pushed down the otherwise impressive goal the company managed to achieve. Keeping profitability, and more importantly a steady increase of it over time is vital for me as an investor. With a good increase in units shipped all across the board, time will tell if SEDG can capitalize on this an increase their bottom line.

SolarEdge’s Technologies Financial State

To me, it’s incredibly important to know how a company is doing right now financially. That goes before looking into any future projections by the company themselves. If they are unable to pay back debt forcing them to issue shares for example, those are issues I want to know about beforehand.

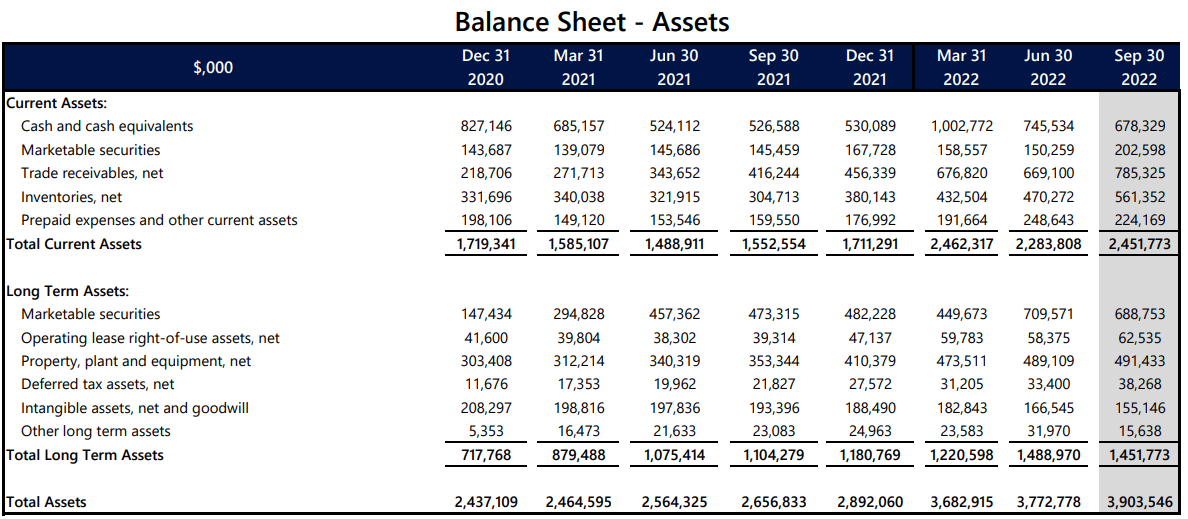

Having that said, I think SolarEdge Technologies are sitting in a really good spot financially. They have more cash at hand than total debt. That gives me great optimism that paying back debt would be a problem. In terms of assets to liabilities, they hold almost 2x more assets right now. A large part of their assets are from both “inventory” and “long-term investments”, but one that I am particularly interested in is the “accounts receivables”. To me, this signals a large demand for their product and it’s now up to the company to deliver it and get the money that is due.

Balance Sheet Of SolarEdge (SolarEdge Q3 Earnings Report)

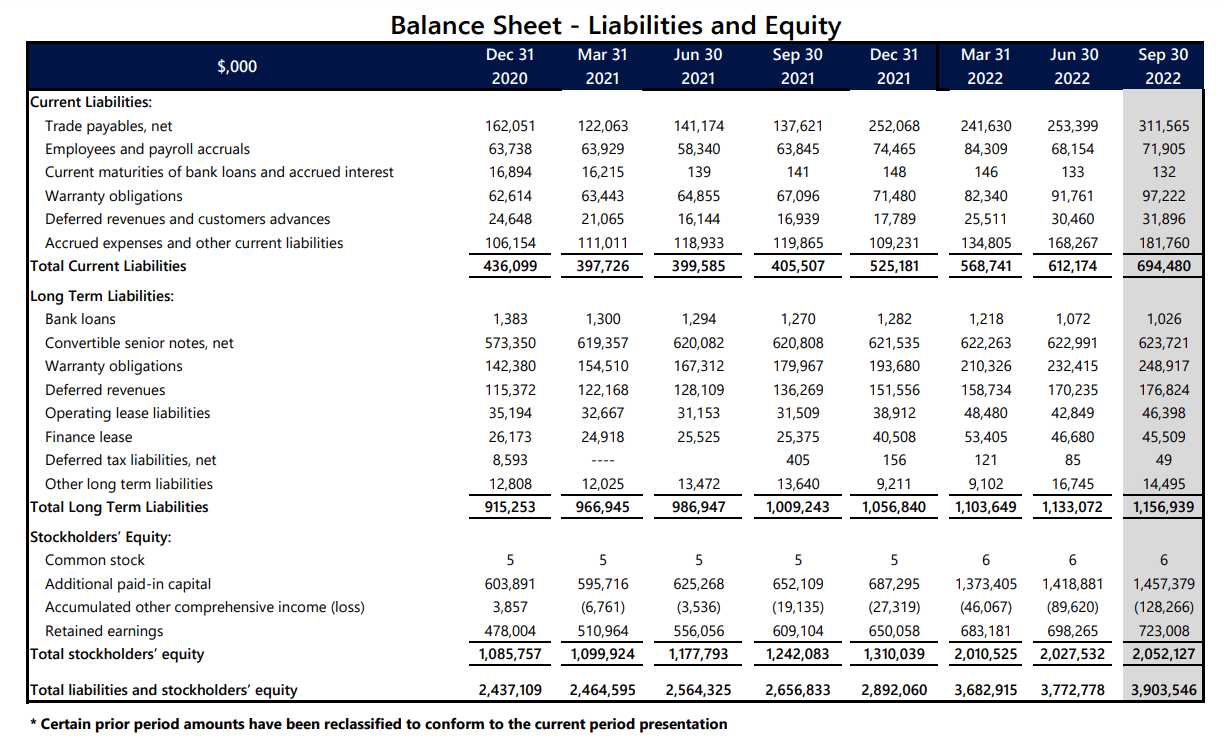

If I look at the liabilities that SolarEdge has then there is nothing really worrying popping out immediately. The company doesn’t hold a large amount of debt to the amount of cash they have, and could even pay it back now if they wanted to. In the future it might be by looking at the lease’s costs. It’s a small portion, but if SolarEdge is not able to invest and vertically integrate their production in the coming years, they might be forced to lease certain machines and equipment, further raising the operating expenses.

SolarEdge Liabilities (SolarEdge Q3 Earnings Report)

Looking At The Competitors

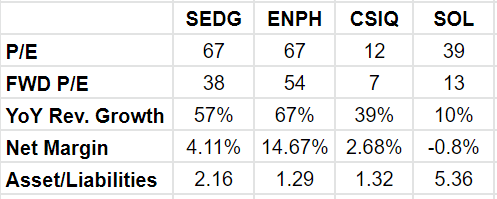

Before I buy a company I want to know what the competitors are doing both financially right now and what their growth prospects are like. In the solar sector right now there are quite a lot of companies competing for their own market share. It’s a capital intensive sector to gain a foot in. Let’s take a quick peek at how some of the similar companies to SolarEdge Technologies are valued.

Competition Valuation (Author’s Own Calculations)

Above are some of the quick valuation metrics that I look at to get an idea about how the company might be doing. What strikes me first is that SolarEdge seems to have quite a similar valuation to some of the other companies like Enphase Energy (ENPH), Canadian Solar (CSIQ) and ReneSola Ltd. (SOL). There was a large run up and increase in multiples for a lot of the solar companies, both this and last year.

For me they were unrealistic and made it impossible to buy any of the companies valued at p/e of 60+ without having a large downside risk. Some would argue that with time the companies would make up for the premium valuations they have today. But as I am a value investor, I seek to buy companies when they are undervalued and will with time outperform the market’s annual growth.

Some of the things I am looking out for in the solar sector as a whole when valuing companies are the net margins they have, cash flow and also cash/debt ratios. Those things go a little bit more in depth than the ones in the chart above. Companies taking on new debt happens all the time, the question becomes how they will manage to pay it off. Do they already have a good cash position if need be?

Valuing SolarEdge Technologies

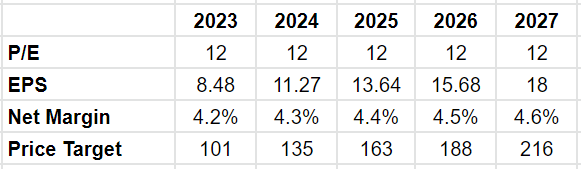

After all we have gone through, let’s now set some price targets and realistic future valuations to SEDG. I think that having price targets and numbers that you believe a company could reach is a large part of investing. I am buying a company, and if they are unable to successfully reach some of those targets, then I will reevaluate the true value of it. It gives me security and comfort when deploying capital into something.

Future Outlook For SolarEdge (Author’s Own Calculations)

The first thing that stood out to me with this chart and future price targets for SEDG is that right now, it would still be overvalued even 5 years out. I have put a p/e of 12 all across the board since I like being a bit more conservative with those numbers. If SolarEdge is able to successfully grow their revenues at a rapid pace, then a higher multiple might be deserved.

But I believe it could taper off as the market becomes saturated with more companies and margins won’t increase as quickly anymore. If I would invest money right now I can expect to lose about 43 % of my money by the time 2027 comes around if these price targets come true. Continued share dilution is also something that could weigh on the EPS growth, and in turn the share price too. But like I have made it clear, the business is most likely going to be around in 2027, it’s just that the appreciation of an investment right now might not be enough to justify a buy.

I think no company is worth paying 60x the earnings for, unless they are continuously dubbing their top and bottom line year after year. I have mentioned previously here that perhaps the entire solar sector could use a pullback to reach more realistic valuations. If that happens then you might want to take a look at SEDG again. But for me, I won’t touch this company until they reach more realistic numbers. From today’s price of $310 per share, it would need to drop over 66% before reaching interesting levels.

Conclusion

SolarEdge Technologies is a growing company with great margins compared to the rest of the sector, outperforming it by quite a bit. In their last earnings report they delivered a slightly shaky performance. The revenue grew at a rapid 56% YoY but the bottom line fell over 30% YoY.

Until the company is able to grow their bottom line at a steady pace, I will stay away from them. But what gives optimism is their ability to keep a very healthy balance sheet all throughout the year. With enough cash to pay off all debt they are well set-up for an upcoming slowdown in the economy.

With so many tailwinds for the solar sector, like increased demand for green energy adaption and government incentivising renewable solutions, SolarEdge should see increased demand for their product in my opinion.

I also think that valuations matter, especially if you are putting your money away for the long term. We want a favorable entry point and right now I don’t have that with SolarEdge. It might sound harsh, but I wouldn’t put money into the company unless they drop 66% from current prices down to around $100 per share. Right now I will hold off from buying any stock in the company, and would go as far as saying investors would be better off selling shares and placing that money elsewhere.

Be the first to comment