cmannphoto

Investment Thesis

SoFi (NASDAQ:SOFI) is a bank that describes itself as a fast-growing fintech company. And while I recognize that the semantics here are highly contentious with many investors, I urge readers to look beyond this battleground.

Therefore, rather than putting the argument on whether or not SoFi should be valued on a multiple commensurate with a fast-growing bank.

Instead, let’s put the thesis squarely on its earnings potential over the next twelve months. And here, I struggle to find much upside to paying a $5 billion market cap for this business. And I believe you’ll also agree.

My thesis is that the market hasn’t sufficiently priced in the new macro environment we now find ourselves. The new inflation report yesterday is the catalyst that will drive SoFi’s next leg lower.

What’s Happening Right Now?

The inflation report yesterday showed that inflation is still going to remain high. That household disposable income is going to get increasingly stretched in the coming months. And that the Fed will continue on its path by raising rates a little further.

Not much further, thankfully, the vast majority of the lifting has been done. But there’s still some work to be done. The key characteristic is this, the Fed is not going to pivot. That’s the reality.

And for a really long time, either implicitly or explicitly, investors’ bull thesis had been contingent on a Fed pivot. But with the Fed not having to reduce rates any time soon, SoFi is going to struggle to be a compelling investment.

Let me put it another way, the most realistic scenario is that interest rates are going to hover around 4%.

And even though the market is forward-looking and a lot of stocks have already derisked, I maintain that not all pockets of the market have sufficiently derisked.

SoFi’s Community Perspective

I’ve followed SoFi long enough to know that its shareholders have one of the strongest communities of investors. Indeed, simply looking through SA, the bulls dramatically outnumber the bears plus those investors on the fence.

And I fundamentally get many of the bull arguments. For example, I’ll highlight three such considerations.

- The time for selling out was this time last year, not now.

- There’s already too much negativity priced in.

- I’m already down 30%, at this point, I might as well wait to return to breakeven.

However, I contend that these considerations are backward-looking. They don’t sufficiently consider what the next twelve months are going to look like.

SoFi’s Near-Term Prospects

SoFi describes itself as the AWS of fintech. Anyone that describes themselves as the next Amazon (AMZN) should minimally put investors on guard. Amazon is a very rare company.

This is the premise, SoFi is on the path to creating an end-to-end technology platform to liberate customers from having to seek different products, whether it is to borrow, save, or invest.

SoFi believes that its high-earnings members are technologically proficient and want better control over their finances.

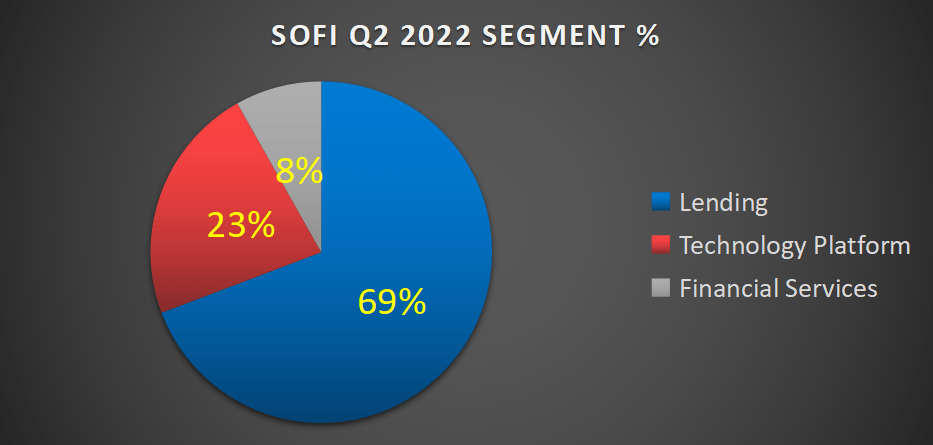

Author’s work

As you can see above, the vast majority of what SoFi does is lending. And when interest rates were low, the appetite to refinance was very strong.

But with rapidly raising rates, I believe that consumers’ appetites to refinance will substantially decrease. Why would you want to refinance onto a higher loan? You wouldn’t want to.

Furthermore, within lending, SoFi believes that its biggest opportunity will come from home loans.

I believe that this avenue will not work. Why? By definition, higher earners with higher education and technological proficiency will bargain hunt for the cheapest mortgages!

Getting a loan is a big decision. It’s not like getting merchandise from Amazon, where convenience and speed are the main considerations. With home loans, the ultimate price is probably the only consideration.

I believe that you’ll agree with me. Even though SoFi describes its biggest strength as its ability to cross-sell into its member base, we should not give credence to that narrative.

SOFI Stock Valuation – Too Difficult to Find Upside

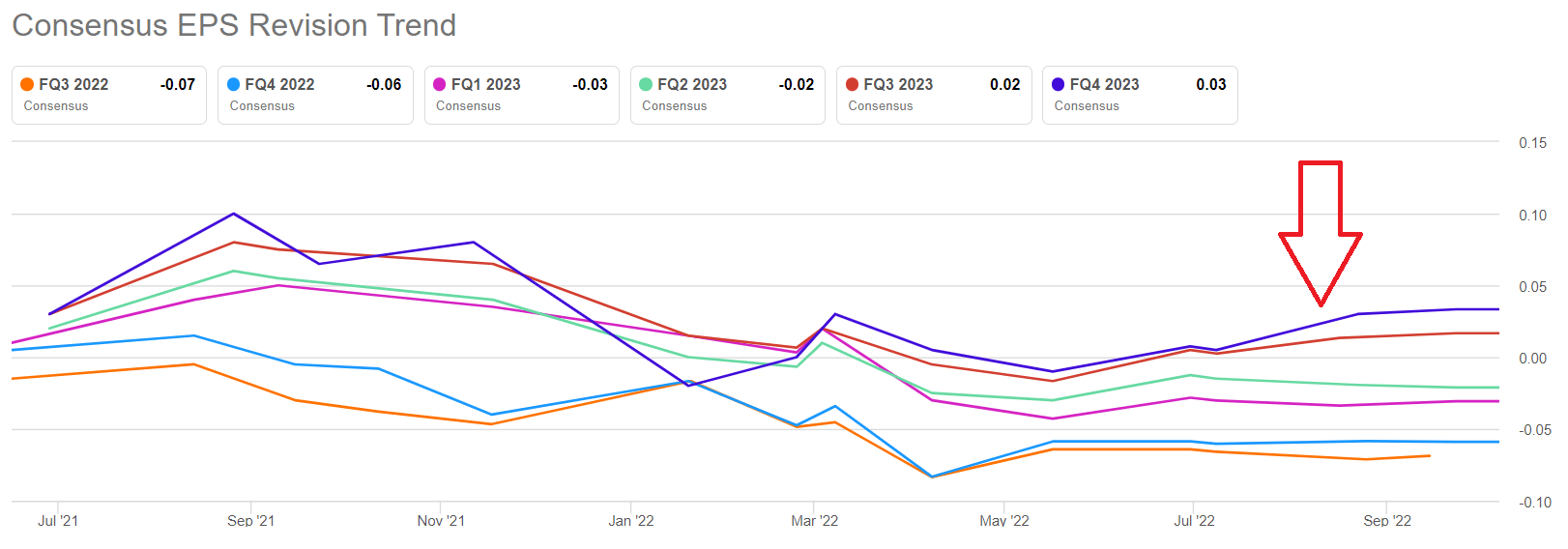

Consider the following EPS consensus chart.

SOFI EPS consensus

What you see above is that after all the evidence has become reflected that the economy is waning, through rampant inflation, high cost of energy, and higher interest rates, analysts are still raising SoFi’s EPS estimates. How is this possible?

I’m trying to be fair. I admit that I make mistakes. We are all human. We are all on the same page, trying to increase our savings.

But there’s a clear inadequacy where analysts are still upward revising SoFi’s EPS estimates. How can anyone put any faith in these figures?

I’m not being harsh. I’m being fair. This is a legitimate question.

The Bottom Line

At the best of times, investing is super challenging. We all make regular investment mistakes. But I believe that there’s no need to overcomplicate investing. Stocks follow earnings.

Investors need to try to look forward over the next 12 months and think about where SoFi’s earnings could be. I passionately believe that SoFi’s earnings estimates need to be downwards revised to factor in the new status quo we find ourselves in, of higher rates and higher inflation.

And that when SoFi’s earnings get downwards revised, this will see SoFi’s share price follow suit.

Be the first to comment