Justin Sullivan

The recent volatile market has whipsawed investors to the point of making irrational decisions on the accurate financial metric to utilize to value a stock. SoFi Technologies (NASDAQ:SOFI) is a prime example of a fast growing fintech where investors want to irrationally and suddenly value the stock like a slow growing bank. My investment thesis remains ultra-Bullish on the fintech already generating adjusted profits completely overlook by the market.

Already Profitable

Investors need to learn the difference between momentum trading and investing along with the appropriate metrics to value a company. One shouldn’t alter the true valuation of a stock based on the market sentiment.

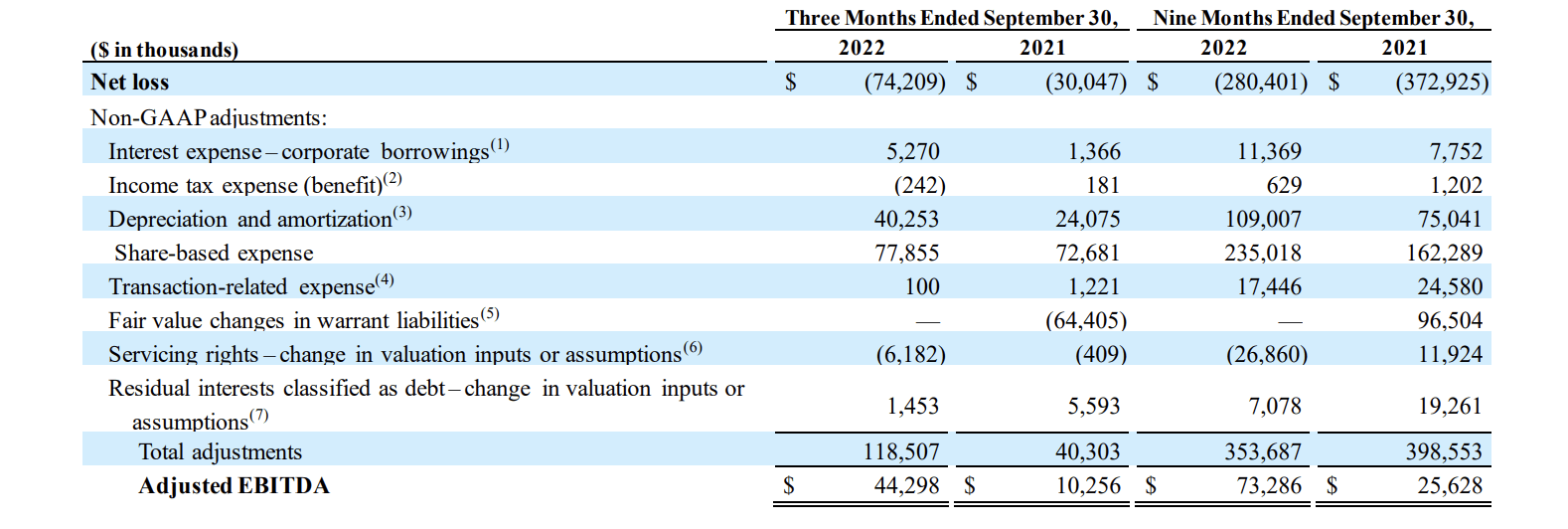

Fast growing companies should always be valued on future cash flows with adjusted EBTIDA being one of the best metrics for valuing a stock. In this case, SoFi is already highlight profitable with an impressive $44.3 million worth of adjusted EBITDA in the last quarter alone.

Source: SoFi Q3’22 earnings release

Of course, investors have to be careful with using EBITDA measures due to the exclusion of expenses such as interest, deprecation, and taxes. This isn’t the general case for SoFi with virtually all of the adjustments of $118.5 million tied into non-cash amortization costs and stock-based compensation.

Investors not happy with using non-GAAP numbers still shouldn’t value a company based on non-cash charges. In the case of SoFi, the adjusted profit pretty much equates to the adjusted EBITDA figure.

The main adjustment to the net loss of $74.2 million is the SBC expense of $77.9 million. Just excluding this amount immediately makes SoFi profitable by $3.7 million.

The other main charge is the Deprecation and Amortization category of $40.3 million. A large part of this charge is related to Amortization of Intangibles and Goodwill related to acquisitions. SoFi ended Q3 with $1,623 million in Goodwill and another $457 million in Intangible Assets on the balance sheet.

At the end of Q2’22, SoFi had $1,625 million in Goodwill and another $481 million in Intangible Assets. The asset reductions amount to ~$26 million in expenses during Q3.

The fintech doesn’t provide a lot of detail in the Q3’22 10-Q to isolate how much of the $40.3 million is true depreciation of actual assets. Even just using the $26 million figure for the amortization of intangibles, SoFi now generated a nearly $30 million adjusted quarterly profit.

The other charges are mixed and can be offset. Ultimately considering the vast majority of the adjustments from adjusted EBITDA are non-cash charges, investors are simply better off utilizing the adjusted EBITDA figure to value the stock. SoFi has generated $73.3 million in adjusted EBITDA YTD and the target is for over $115 million for 2022.

The original financial targets predicted a very large ramp in adjusted EBITDA with the digital bank and full student debt refinancing. SoFi won’t see this full benefit until the Biden Admin. is either forced by the Supreme Court to cancel any loan forgiveness plan or the administration can move forward with such a plan freeing up SoFi to refinance the remaining borrowers not qualifying for forgiveness.

Either way, the fintech forecast EBITDA margins of 30% in the future when business normalized with incremental margins of 45%. SoFi spent more to invest in the business last year hitting margins, but the fintech should be able to scale back some of the spending in 2023 with the general market dynamics shifting away from excessive spending.

Fast Growth Valuation

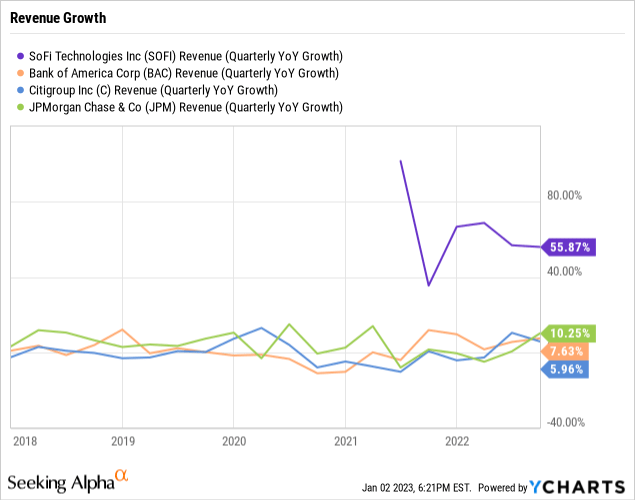

SoFi definitely should possibly be valued similar to a bank, but the company shouldn’t be valued the same as the large banks. SoFi is growing revenues in excess of 50% while Bank of America (BAC), Citigroup (C) and JPMorgan Chase (JPM) regularly have growth rates in the 5% to 10% range.

One wouldn’t value a fast growing tech. company at the same multiple as IBM (IBM) or Oracle (ORCL) with limited growth after scaling up to multi-billion companies. One might use a similar valuation metric to value a tech stock, but one will definitely apply a much higher multiple to the fast growing tech. stocks. It shouldn’t be any different with a fintech.

Of course, the big deal with SoFi is that the fintech generally doesn’t carry much in credit risk. The digital bank doesn’t hold loans for investments with a focus on selling loans to investors. Outside of the current crazy period, the company is far more a traditional fintech without credit risk unlike the above large banks with a principal business in lending.

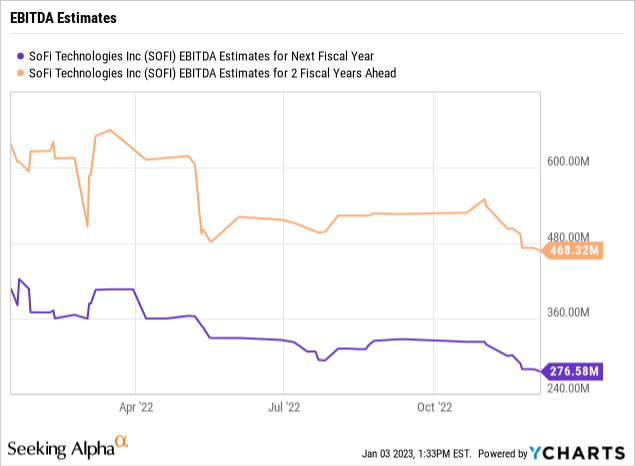

Considering adjusted EBITDA targets are similar to adjusted profits for SoFi, investors should have confidence valuing the stock based on this metric. The stock only trades at 15x 2023 EBITDA targets for a business set to double and triple EBITDA in a short period.

Takeaway

The key investor takeaway is that SoFi is an exceptionally cheap stock with the market not understanding the financial of the fintech. The stock should be worth far more based on actual adjusted profits and the expectations for strong growth ahead.

Be the first to comment