HJBC/iStock Editorial via Getty Images

This morning, Société Générale (OTCPK:SCGLY) presented its half-year results to the investor community. Three months after the bloody sale of the subsidiary Rosbank, the French bank closed the Q2 with a loss of almost €1.5 billion compared to a €1.44 billion profit reported at the end of June last year.

This number is shocking but we should not be worried about that. We previously covered its Russian exposure in a detailed publication providing to our readers some support and a buy valuation case. And today, numbers in hand, the impact on the Russian front is less heavy than analysts’ expectations, who expected a total loss of more than €2 billion in the last line of the income statement. To be precise, Russia’s exit resulted in a “loss of 3.3 billion, gross of taxes” in the P&L, the institute explained in the just release note.

Our buy case recap was based on the following:

- SocGen restructuring plan in progress with important cost-saving;

- Compelling valuation after the stock price sell-off;

- Sum-of-the-Part ALD valuation;

Looking at the presentation, we can clearly say that SocGen is delivering:

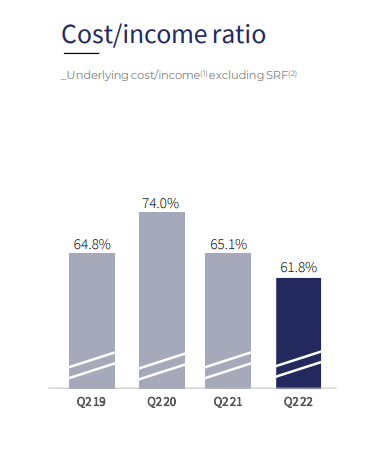

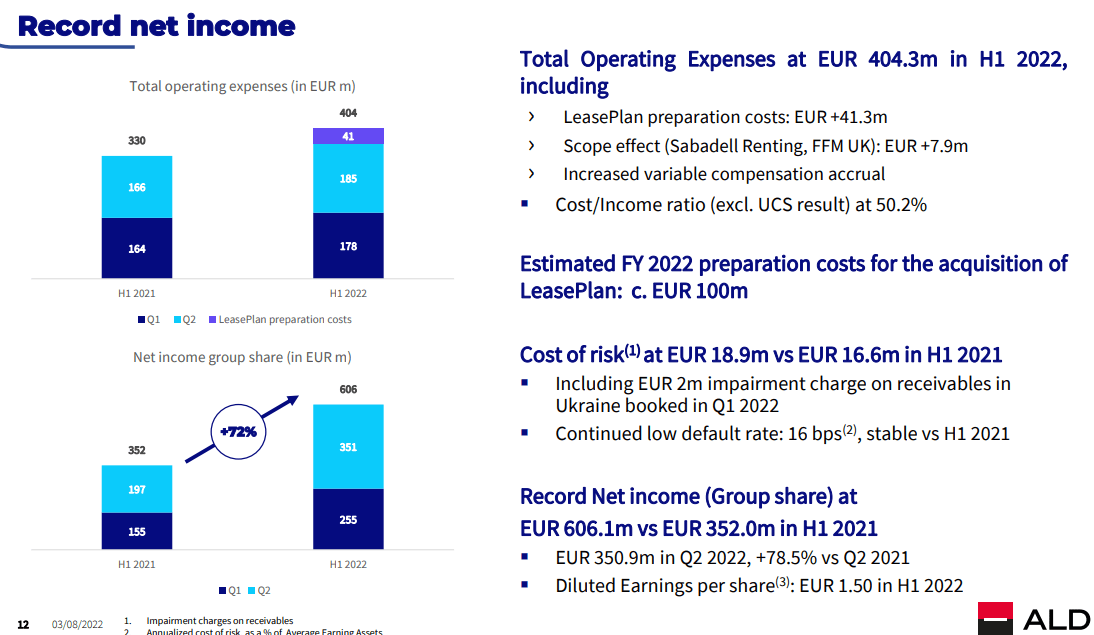

The cost/income ratio is constantly declining and ALD which is a separate listing company (in which SocGen is the major shareholder) just delivered its record net income. This result was driven by multiple positive factors: a positive one-off recorded in Turkey for the hyperinflation (as happened to BNP) and a favorable price environment in used cars. We should also note that EV penetration stands now at 27& of its entire market fleets.

ALD cost/income ratio

Source: Société Générale Q2 Results

ALD record results

Source: ALD Q2 Results

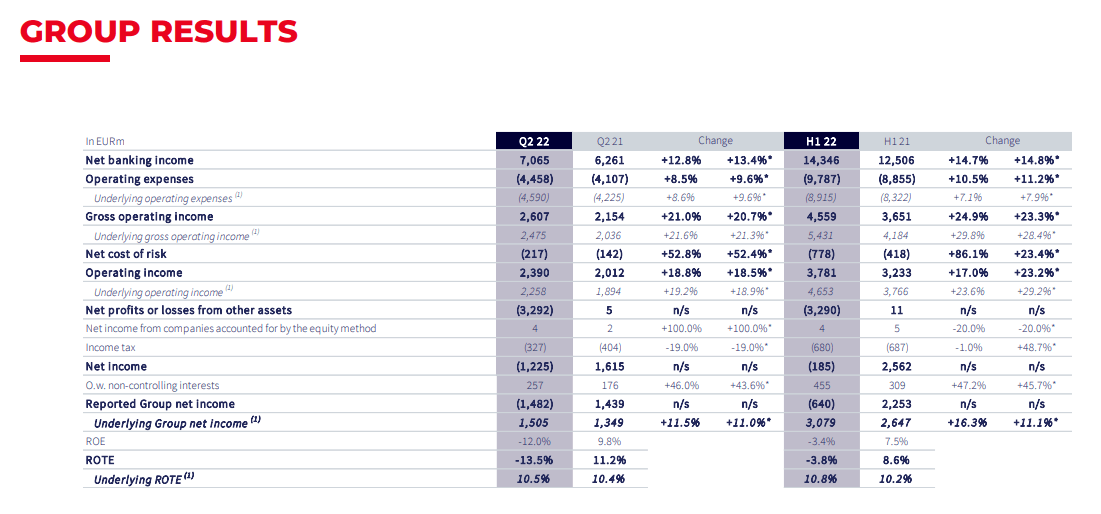

Q2 Results

Looking at the profitability and excluding the Russian impact, the Parisian institute showed to be healthy and managed to report solid indicators beating Wall Street analyst’s expectations. Operating profit rose from €2.01 to €2.39 billion with a double-digit trend, while the ROTE strengthened to 13.5% compared to 11.2% in the second quarter of 2021. On the balance sheet side, the CET1 ratio remains stable at 12.9% but on a quarterly basis is down by 70 basis points. However, it is no coincidence that the market has shown to appreciate the numbers – the stock price was up 4% at the opening this morning.

Société Générale financial results

Source: Société Générale Q2 Results

Conclusion and Valuation

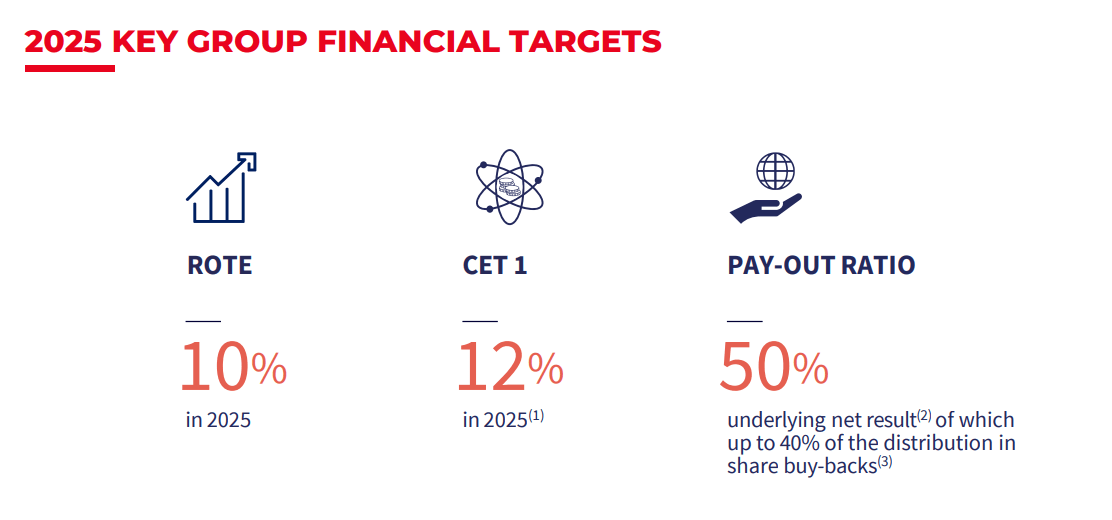

As for the remainder of the year, SocGen continues to expect a cost of risk ranging from 30 to 35 basis points. In 2025, the company aims for a ROTE of 10% and a minimum Common Equity Tier 1 of 12%, while it indicates at least a 3% average annual growth rate at the revenue line for the three-year period 2023-2025 with a cost/income ratio compressed to at least 62% and a payout ratio at 50% of its underline profits. New targets are ahead of consensus.

In the conference call to comment on the mid-year results, CEO Frederik Oudea described the accounts for the period as “excellent“. As is known, the banker will leave the institution next year after having led it for almost 15 years. The name of his successor is expected in the fall.

To sum up, SocGen paid less than expected for the Russian consequences, achieved an excellent performance in the quarter, increased its 2025 targets forecasting cautious assumptions and is still trading at 0.3x of its book value. We say no more, €30 share price reiterated.

SocGen 2025 target

Source: Société Générale Q2 Results

Be the first to comment