greenbutterfly

Investment Thesis

Snowflake (NYSE:SNOW) experienced a sharp decline of 50% in 2022 mainly due to broader multiples compression. The company is engaged in a data warehousing and analytics segment which presents immense TAM expansion opportunities as sooner or later all SMEs in developed countries will demand such services to some degree to maintain their competitiveness. Its shareholders composition is quite favorable, predominantly consisting of institutional investors. According to my DCF valuation model the stock is currently trading inside its intrinsic range of $134 to $152, so for value investors who prefer to buy undervalued stocks it is still not a very compelling buy, but for one who prefers to buy high-quality business with strong growth prospects this stock looks attractive.

Business At A Glance

Snowflake Inc. is a tech company that operates in a DaaS segment and provides a cloud-based data storage and analytics service in the US and globally.

It was founded in 2012 and had several raising rounds until going public in September 2020. Its IPO was one of the largest software IPOs at that time, raising $3.4 billion and its price doubling on the day of listing. Since its IPO, the company has been growing like on steroids with revenues increasing fivefold over the last three years. At a current share price of $140 its value is approximately $45 billion which is five times larger than its market cap three years ago.

Its data cloud platform was launched in 2014 with the data warehousing as its main product. The offering has expanded since then and now it offers data lakes, Unistore, data engineering, data exchange and cloud-based applications. Their solutions enable customers to store and structure data to drive meaningful business insights, build data-driven applications, and share data. Its platform is used by various organizations of sizes in a range of industries.

Its share price has suffered dramatic fall since mid of 2021 together with an array of other tech companies and wiped 50% of its value which still is less than some of its peers, such as, Palantir, (PLTR) which lost nearly 80% of its value over the same period. Its relative outperformance can partly be explained by its shareholders composition. SNOW is by 64% owned by large institutions with public owning of only 24%, conversely, Palantir is by 52% owned by public. Institutional money is stickier, hence, the prices of companies with high institutional ownership are less volatile.

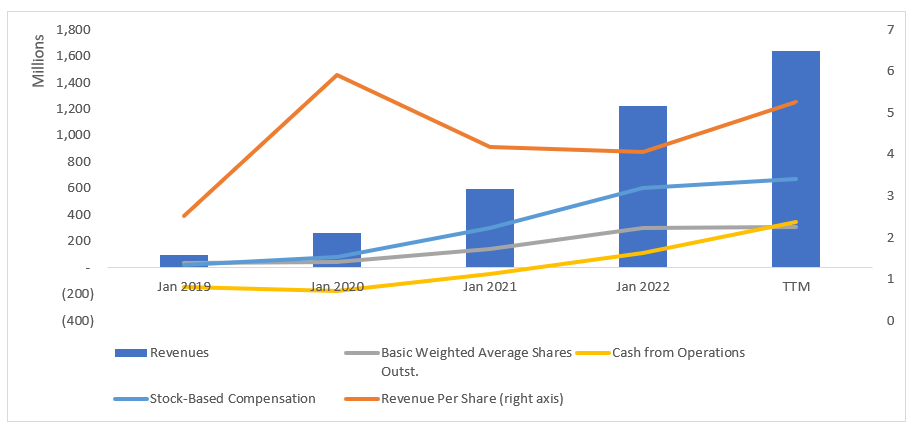

Stock-Based Compensation Practices

Although its top line has been increasing quite impressively over the last years, its revenue per share has been falling (excluding the trailing numbers) as is seen on the chart below as a result of its stock-based compensation scheme that has a diluting effect.

Author’s presentation based on SNOW financials

With regards to the SBC practices in general, it is not uncommon for high growth software companies to attract staff with equity incentive schemes. Highly experienced and skilled staff is the most important asset of such companies and paying them with company’s stock creates twofold positive impact. First, it incentivises staff to maintain high standard of their work and be willing to contribute as their compensation directly depends on the company profits. Second, it frees up some cash for its owners to be able to invest in the growing business. Lastly, SBC is not a cash item and is added back when estimating company’s free cash flow and it is a source of financing if/when options are exercised. As an example, out of $605 million in the SBC expense the $179 million (or 30%) were recorded back as an issued stock as a result of the options exercise within the equity incentive plan.

SBC is a good tool in financial engineering, particularly when the company is growing at a double (or even in our case at a triple) digit. From a shareholder standpoint, it is normally ok to accept this practice but it should not be overdone due to its diluting impact.

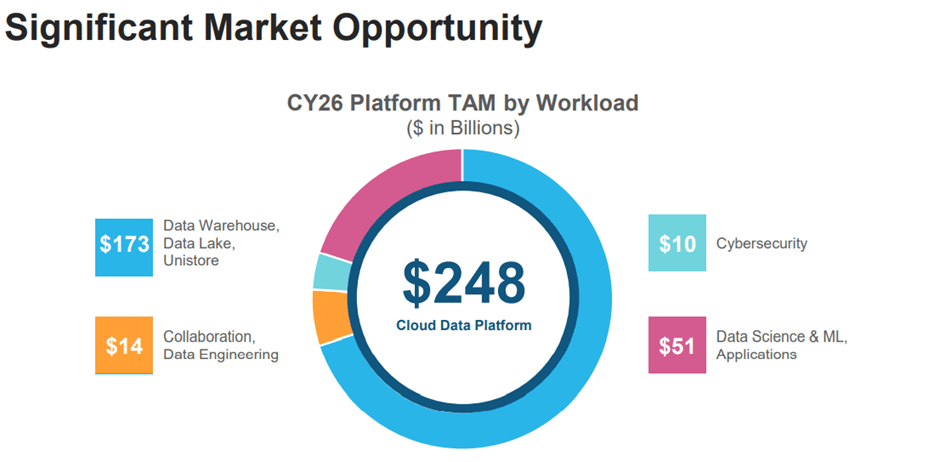

Significant Market Opportunity

The data warehouse segment where SNOW is engaged in is probably the most demanded solutions in the tech space right now. All large corporates and financial institutions have tons of data they are in desperate need to put in a proper use and that is when data warehouses come into play because they help to structure, analyse, and provide context to the data that otherwise would be wasted.

To remain competitive, companies in all industries have no other choice as to continue invest heavily in data-driven solutions. It is estimated that SMEs should set aside around 2-6% of their total budget for data analytics. To have a perspective, a company with revenue of $1 million (the average revenue of SMEs in the US) would need to spent on average $60k on data analytics solutions annually and there are over 7 million of SMEs. Simple math exercise gives us $281 billion in market opportunity. Of course not all SMEs spend that amount on data analytics, but this may shed some light on this segment future prospects.

Not surprisingly, all tech giants, such as, Amazon (AMZN), Google (GOOGL) and Microsoft (MSFT) currently offer data warehouse solutions. What is striking, however, SNOW is the leader (so far at least) in that space due to its ability to operate across all giant cloud providers as one can seamlessly integrate and use Snowflake with AWS, Azure, Google Cloud Platform. Snowflake and Amazon Redshift account to nearly 40% of the data warehousing share (18% and 19% respectively).

According to Snowflake’s projections its TAM is going to reach $248 billion by 2026 and yet it is not even penetrating 1% of that at a current annual revenue of approx. $2 billion.

Snowflake’s Q3-FY2023 Investor Presentation

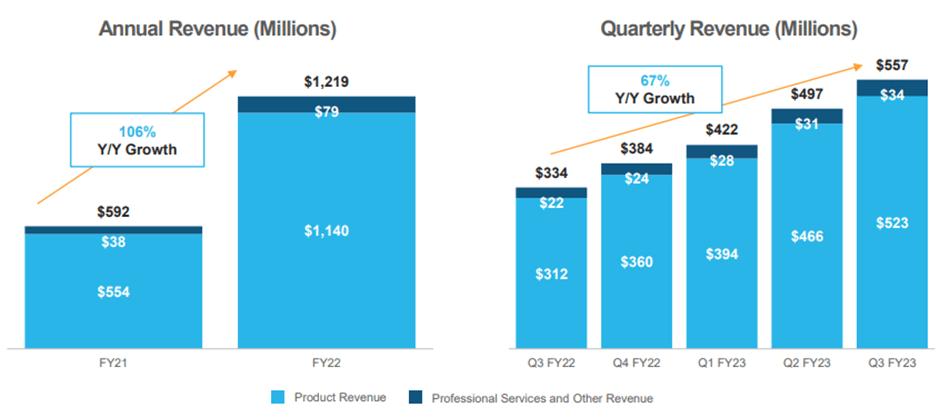

Financials

SNOW’s latest financial results Q3-FY2023 were well ahead of the consensus. Quarterly revenues rose to $557 million, representing YoY growth of 67%, bringing its annual trailing revenue to $1.86 billion.

Snowflake’s Q2-FY2023 Investor Presentation

Another important component of growth is the remaining performance obligations, which is a contracted revenue not yet recognized. At the end of the quarter this stand at $3 billion with 55% of that to be recognized as revenue in the next twelve month. These are substantially higher than its RPOs at the end of Q3 last year when it was approx. $1.8 billion.

Snowflake’s customer momentum remains strong with total customers annual growth of 34%. The growth of clients, who bring over $1 million in sales, has been even more rapid with total count of 287 at the end of the Q3, which is more than twice higher than a year earlier. Another widely used success indicator in DaaS companies is a net revenue retention rate, i.e., what is the fraction of its clients continuing to use its services in the following year and this rate has been around 165-170% for the last several quarters which is by all means quite impressive. To give a perspective, Palantir’s NRR is around 150% while Cloudflare’s (NET) 125%.

SNOW’s gross margin is 75% which is higher than the industry average of 71%. It has been improved by six percentage points over the year because of increased marketing efforts and increased efficiency due to a better storage compression. In my model I assume unchanged margins for the forecasting period.

The company is generating a positive Non-GAAP free cash flow for the second fiscal year in a row. For the first three quarters of this fiscal year it generated $305 million which represents a cash flow margin of 21%. The company’s guidance suggest improvement in the FCF margin to 25% over the next five years.

It has nearly $4 billion in cash and short term investments, and no debt, so from the liquidity perspective it does not have any current issues and has plenty room for manoeuvre. If we add back

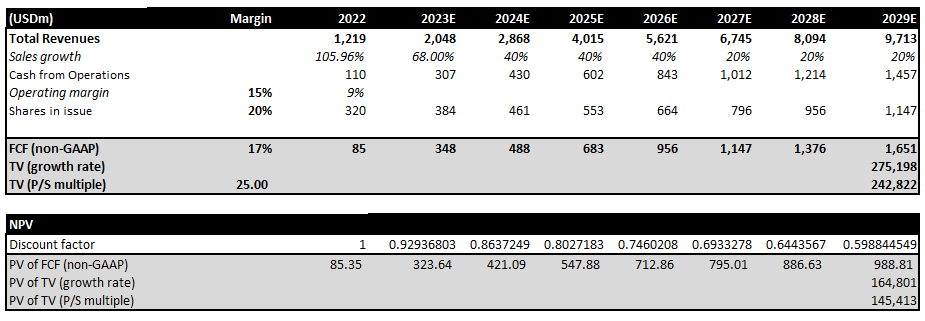

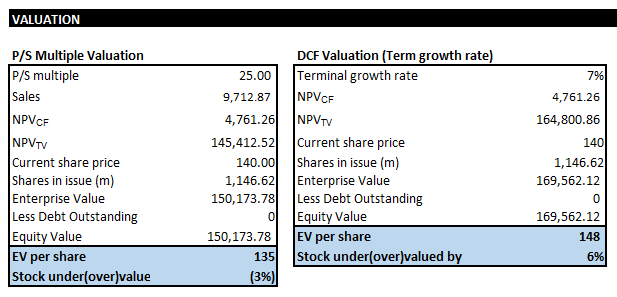

Valuation

To value the company, I’ve used discounted cash flow model. Although top line growth has been more than impressive over the last several years I am expecting it to subside somewhat as no company can double its revenue annually for a prolonged period of time and I generally prefer to be on a conservative end. I used sales growth of 68% for FY2023 (in line with the company projections) with the growth declining to 40% in the next several years and lowering to 20% in the last three years in my pro forma statement.

Author’s pro-forma valuation

I assumed FCF margin of 17% throughout (slightly less than the company projection of 21%) and I also accounted for share dilution of 20% per year as there is no indication that the company is not going to continue with its SBC practice in the future. To estimate discounting rate I applied CAPM model with the risk-free rate of 4% and equity risk premium of 7%. Due to a relatively low beta of 1.2 the final discounting rate has come to 8%.

To estimate terminal value, I’ve used two approaches. In the first approach I am using a future growth rate of 7% while in the second I am estimating TV based on the company’s historic P/S of 25.

Author’s calculation

Using these assumptions, the intrinsic target price is somewhere in the range of $135 to $148 which is where the stock is trading at the moment.

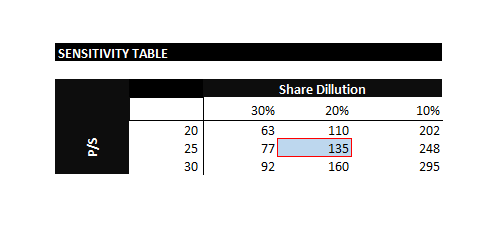

As always in DCF models the target price is highly dependent on the assumptions we make down the line. My projections normally are somewhere at the conservative end. For more bullish or bearish investors I normally present a sensitivity table. The most impactful parameters in the model are share dilution rate and the P/S multiple.

Author’s Calculation

As you can see if we assume share dilution of 10% per year the target price will move to nearly $250 handle.

Risks

The main risks impacting the target price range are further multiples compression and increasing competition.

As I’ve already noted previously some well-known tech names are the main Snowflake’s competitors and considering their superior potential in the R&D spending, they can match Snowflake’s products with ease in a short period of time.

However, Snowflake does have one strong competitive first-mover advantage. In 2019 SNOW launched its public data exchange, which means once data is somewhere in SNOW’s universe it becomes readily available to anyone using SNOW’s infrastructure. It provides huge benefits to members of a common supply chain providing they are using SNOW services. This is when first-comer advantage can play a big role as members of the platform quite unlikely will decide to change the provider once all members of the supply chain are jointly using it.

Another risk is related to further multiples compression. Right now the stock is trading at its lowest historic multiples since its IPO. It is still more expensive than its peers, but for the company in a leading position it is not uncommon. It doesn’t however mean multiples cannot go any lower. Further multiples development is mainly dependent on macro environment. Multiples are inversely correlated with real yields and looking at the recent real yields development this year’s multiples compression looks obvious. I am discussing multiples compression in more details in this article.

Conclusion

Snowflake is a great business by all means. The data analytics segment it is engaged in offers immense opportunity for TAM expansion. It is a leader in cloud-based data warehousing and data analytics and since its inception it has been ahead of its competitors utilising its first-mover advantage. Its shareholder structure mainly consists of institutional investors, which makes it less volatile than some of its peers. The stock is down 50% in 2022 which is mainly due to multiples compression. Although it trades at its intrinsic value range of $135 – $148, the potential for growth is quite high, so I maintain a buy view on this stock and consider it a good addition to a portfolio.

Be the first to comment