stockcam

Snap’s (NYSE:SNAP) stock has been under tremendous pressure since peaking in late 2021, falling approximately 90% over this period. Much of this decline has been due to a valuation correction amongst growth stocks, but Snap’s poor business performance is also responsible. Despite weak revenue growth and large losses, Snap continues to grow its user base and offer advertisers a differentiated platform. Current headwinds are more of a reflection of Apple’s (AAPL) privacy efforts and a post-pandemic hangover than fatal flaws in Snap’s business. Snap will likely need to rein in spending and demonstrate a viable path to sustainable profitability before the stock recovers though.

Snap is currently prioritizing:

- Growing their user base and deepening engagement

- Reaccelerating and diversifying revenue growth

- Investing in augmented reality

This could be viewed as a positive, as it indicates management remains focused on the long-term success of the business, but could also leave investors seeking short-term profitability disappointed.

In response to soft demand, Snap is focusing on their direct response advertising business and trying to increase the return on ad spend that they can deliver. Snap believes that direct response ad budgets are less discretionary in a challenging economic environment, but this business has also been the most impacted by Apple’s privacy initiatives.

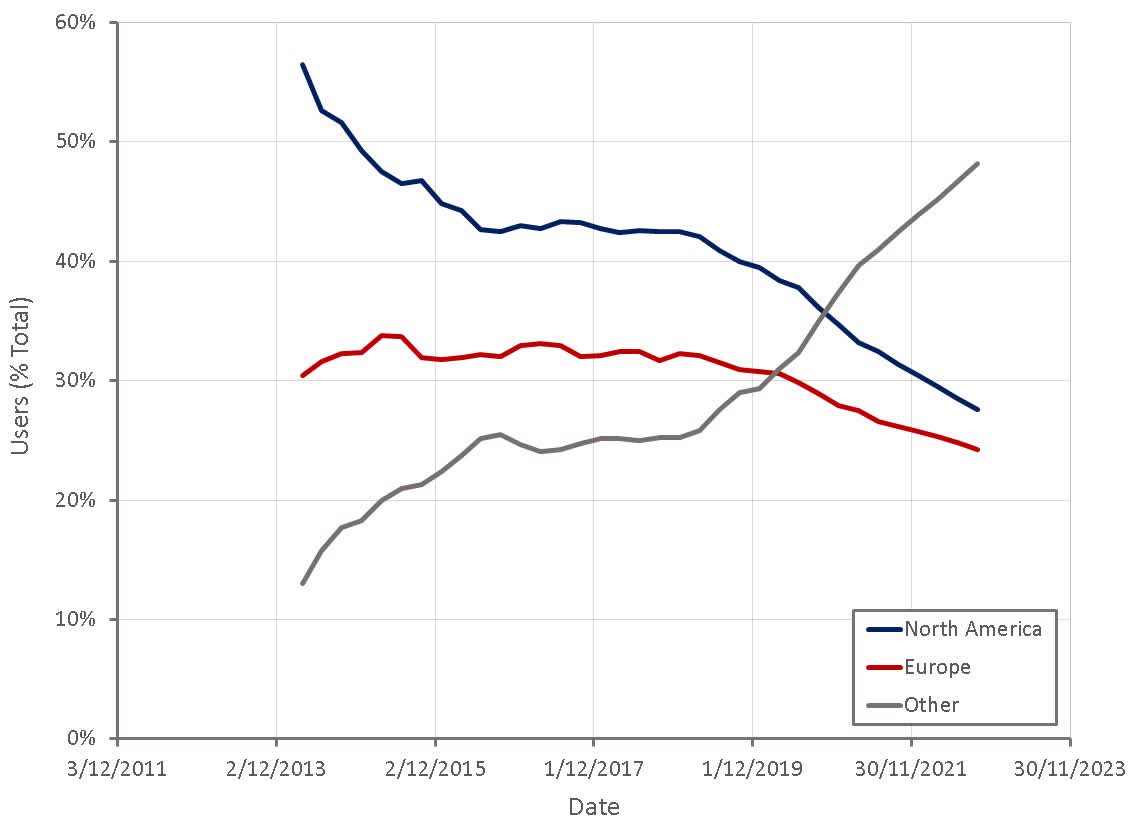

Snap’s user base continues to grow rapidly, which suggests competitive concerns may be overblown, but this growth is being driven by relatively low value international users. Investors are likely to look past user growth if it continues to be driven by low-value users, unless Snap can demonstrate these users can be profitably monetized.

Figure 1: Snapchat Users by Geography (source: Created by author using data from Snap)

There is also the question of user engagement, which is possibly being negatively impacted by the normalization of user behavior after the pandemic. Impressions were up approximately 8% YoY in the third quarter, as a result of Snap’s growing user base. Users were up 19% over the same period though, and revenue was up only 6%. This could indicate a lack of engagement from users and weak demand from advertisers.

Snap’s younger user base, and focus on image-based messaging, is potentially a vulnerability for the company as it is not clear how sticky the platform will be for most users in the long run. Snap appears to be losing engagement to TikTok, and other camera-based apps like BeReal also present a threat.

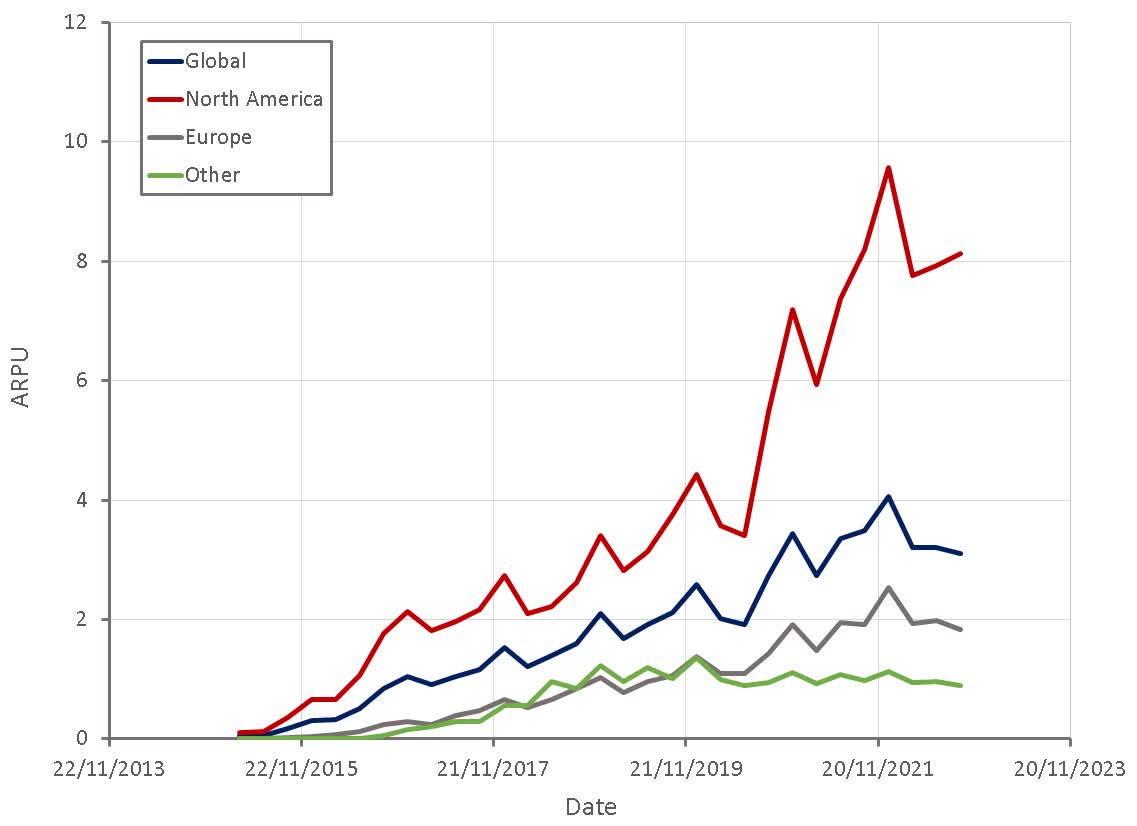

Snap has a proven ability to improve ARPU over time, but the pandemic appears to have pulled forward growth, which may be a near-term headwind. The rapid increase in the number of low-value users is also hiding progress in user monetization. Lower user growth and easier comparable periods in the future should lead to continued improvement in ARPU.

ARPU is also being impacted by Apple’s privacy initiatives and Snap pulling user attention towards lightly monetized surfaces, like Spotlight. If Snap can find ways to improve targeting and attribution, despite ATT, ARPU growth will follow, particularly as surfaces like Spotlight are further monetized. These are not problems specific to Snap though, with similar dynamics playing out across Instagram and Pinterest (PINS).

Figure 2: Snap ARPU by Geography (source: Created by author using data from Snap)

Despite growing competition, Stories remain the largest driver of revenue for Snap, although management have suggested that engagement drops off significantly outside of users’ close friends. Spotlight or Discover therefore becomes an important means of driving engagement beyond this.

Spotlight aims to showcase entertaining snaps created by the community (user created or content publisher), and appears to an attempt to create more viral content, a la TikTok. Response to Spotlight has reportedly been overwhelmingly positive so far, but there is a risk that Snapchat loses some of its differentiation by focusing on viral video content.

Spotlight ads is expected to be launched in the fourth quarter of 2022, which will potentially help to support growth going forward. Management has stated they are currently demand challenged though, and as a result adding Spotlight inventory may pressure CPMs.

While Snap’s advertising business still has significant potential, it appears to also be a business with issues. This is highlighted by management’s inability to accurately project revenue, even in the short-term, and recent executive turnover. Netflix (NFLX) poached Snap’s chief business officer and vice president of sales to support the launch of their own ad business. This type of turnover is bound to happen, but it is also more likely when a business has poor prospects.

Snap’s senior management remains constructive on the business though, if a leaked internal memo is anything to go by. The memo mentioned 6 billion USD revenue and 450 million users as targets for 2023, both of which are aggressive targets which appear extremely unlikely to be achieved given the current macro environment. Spiegel has since clarified that these are aspirational goals. Snap hopes that 350 million USD of revenue will come from paid subscriptions, which are already on track to hit 4 million subscribers by the end of this year. At 3.99 USD per month this represents approximately 192 million USD of annual revenue. Snap also wants AR-based advertising to contribute 10% of its ad revenue next year and is setting up an AR enterprise division to sell its technology to other companies.

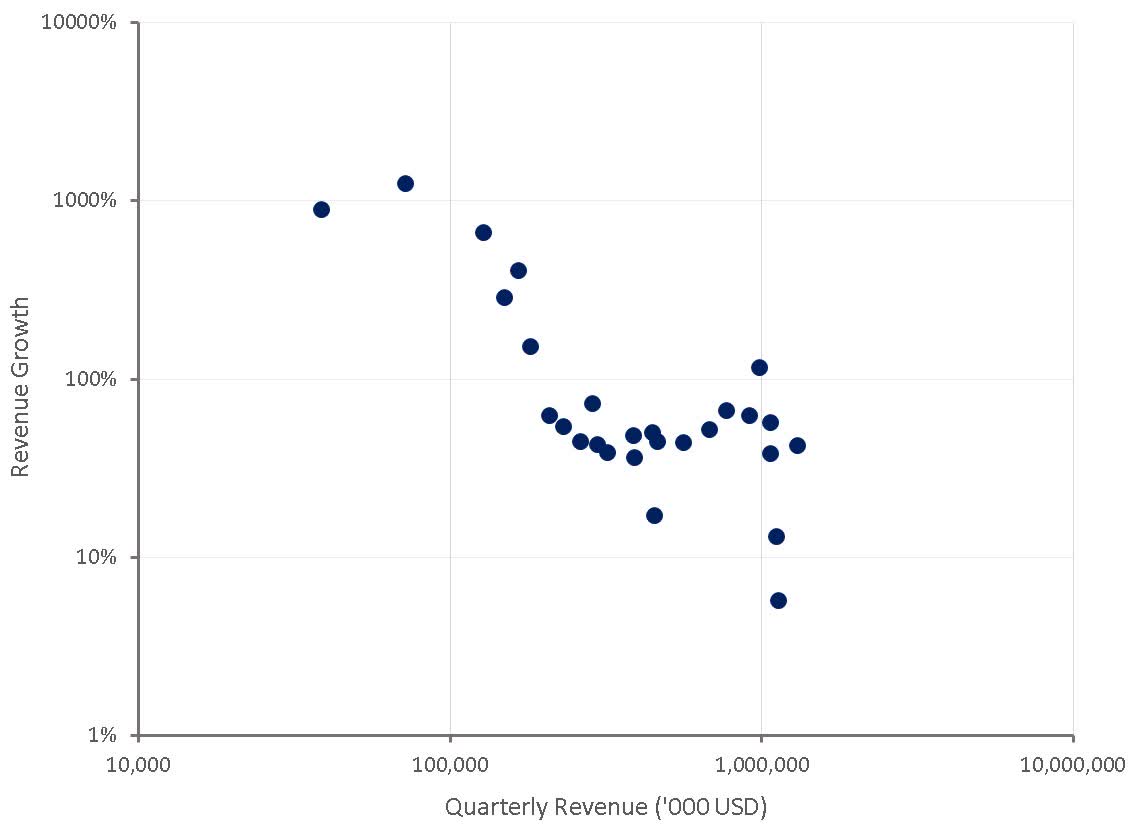

Figure 3: Snap Revenue Growth (source: Created by author using data from Snap)

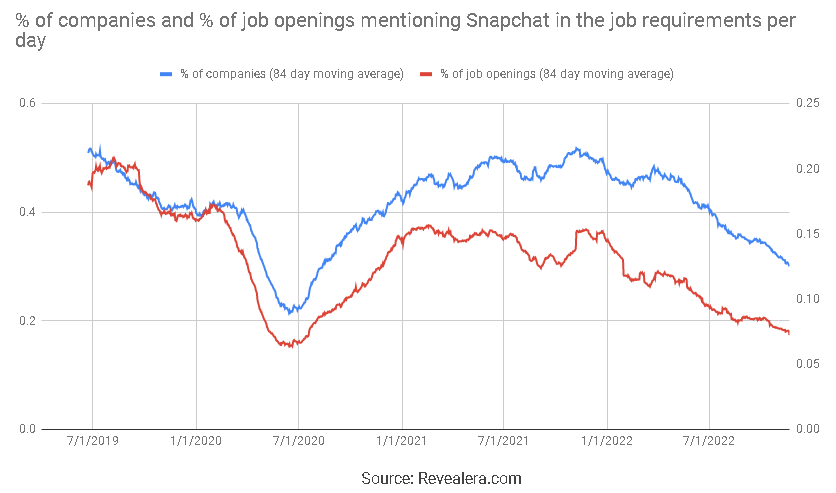

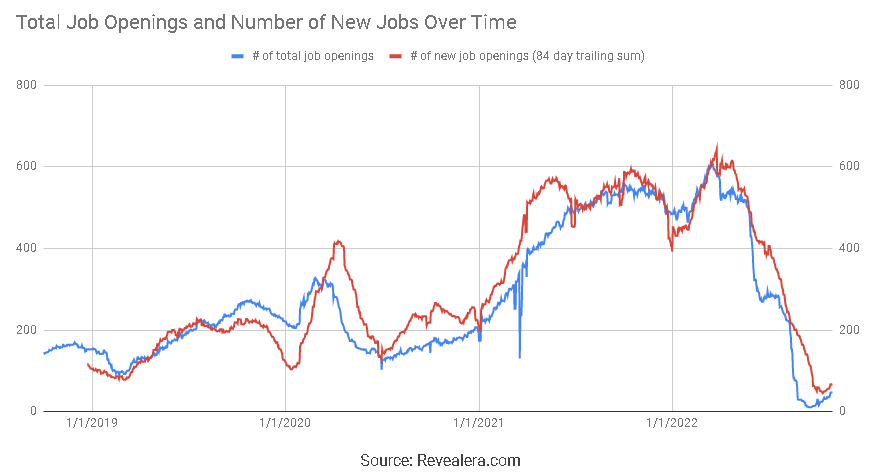

Job openings mentioning Snapchat in the job requirements have been in decline for almost 2 years and are now approaching levels not seen since the pandemic lows. If this is taken as a leading indicator of demand for Snap’s services it could point towards continued weak growth going forward.

Figure 4: Job Openings Mentioning Snapchat in the Requirements (source: Revealera.com)

Markets are currently far more focused on profitability than growth, and as a result demonstrating a credible path towards consistent GAAP profitability is likely to be more beneficial for Snap’s stock price than robust growth. Snap has demonstrated some commitment to this by laying off approximately 20% of its workforce, but they continue to invest aggressively in R&D for speculative projects with uncertain payoffs. Given Snap’s ownership structure, shareholders have little recourse and it is still unclear whether the market will force discipline onto management in a similar manner to Meta (META). Snap has also largely halted hiring, which should provide the business with operating leverage, provided that revenue continues to increase.

Figure 5: Snap Job Openings (source: Revealera.com)

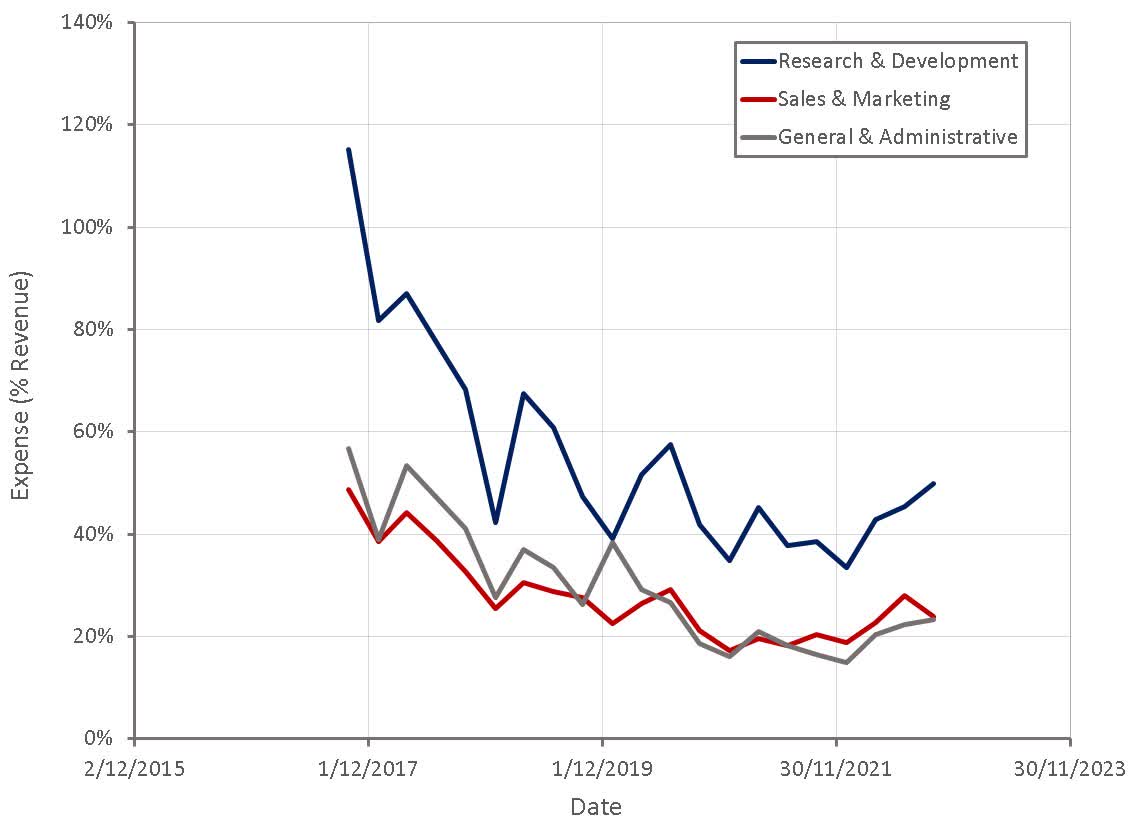

Snap’s general and administrative expenses appear fairly egregious for a company of its size, and should be brought down significantly if Snap is serious about cost control.

Figure 6: Snap Operating Expenses (source: Created by author using data from Snap)

Despite current weak growth and a lack of cost discipline, at some point the market will have to recognize that Snap has a relatively strong balance sheet and could be profitable whenever it chooses to be. Management may have to demonstrate greater commitment to reining in costs before this occurs though. The launch of Spotlight Ads and further growth in the subscription business should be supportive of revenue. The current chaos at Twitter (TWTR) also provides competitors with an opportunity to capture ad budgets which are moving away from Twitter. There also appears to be growing recognition of the problematic nature of TikTok, which could lead to restrictions on its use at some point in the future.

The macro environment is likely to be more important than any Snap specific issues in the short run though. Consumers are currently spending beyond their means and many retailers are carrying excess inventory. As a result, the macro environment could weaken further and hit ad spend far harder than it has been so far. Declining inflation and strong wage growth could lead to a soft landing with continued robust consumer spending though. For investors with a longer time horizon, Snap’s valuation provides a large cushion for negative developments and it seems likely the stock will move significantly higher at some point in the next few years.

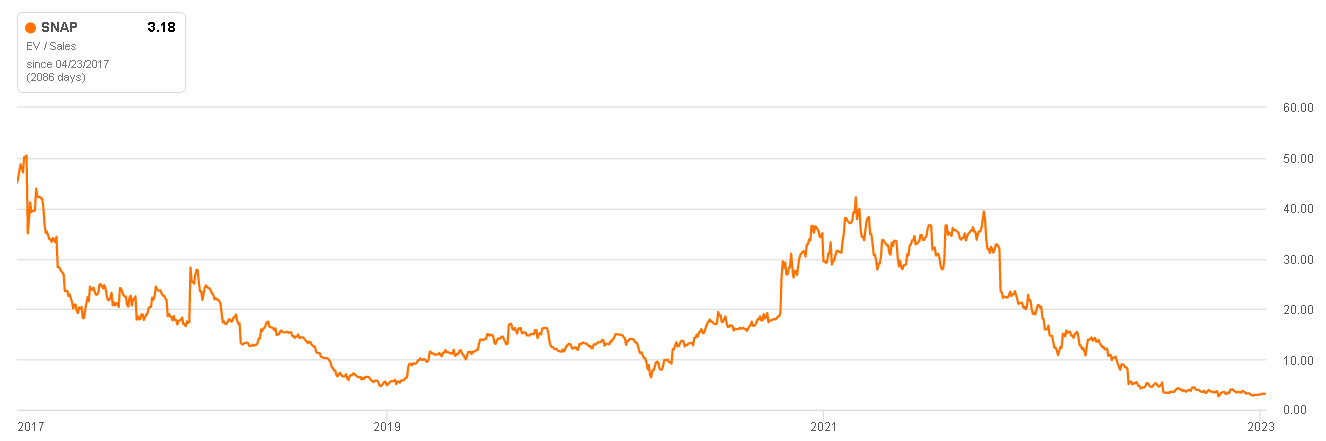

Figure 7: Snap EV/S Multiple (source: Seeking Alpha)

Be the first to comment