Wachiwit

When I published a bullish investment thesis for Snap, Inc. (NYSE:SNAP) last October, SNAP stock was struggling around $9.50. In a little over three months, SNAP has surged 26% higher against the S&P 500’s 7% gain but unfortunately, these gains have nothing to do with a notable improvement in the company’s financial performance. In fact, Q4 earnings yet again disappointed investors, triggering a selloff last week while Wall Street analysts threw caution to the wind. Yesterday, in a surprise move, Snap shares rose nearly 10% aided by Texas Governor Greg Abbott’s announcement of a statewide TikTok ban. Social media stocks also received a boost last week on the back of Meta Platforms, Inc’s (META) recovery. This analysis focuses on identifying the reasons behind Snap’s stellar stock market performance yesterday and the factors behind disappointing ARPUs.

Snap Gets a Boost From Texas Model Security Plan

Yesterday, Texas Governor Gregg Abbott announced a statewide model security plan for state agencies banning the use of TikTok and a few other software products on personal and state-issued devices. Security risks associated with software developed by Chinese companies were highlighted as the reason for this ban. State agencies have until February 15 to comply with this directive. The below excerpt from a news release by the Office of the Texas Governor highlights the directive issued by the Governor on the use of TikTok.

Ban and prevent the download or use of TikTok and prohibited technologies on any state-issued device identified in the statewide plan. This includes all state-issued cell phones, laptops, tablets, desktop computers, and other devices capable of internet connectivity. Each agency’s IT department must strictly enforce this ban.

This new development in Texas boosted hopes among investors that the U.S. will eventually force Apple, Inc. (AAPL) and Google to remove TikTok from App Store and Play Store, respectively. Last June, FCC Commissioner Brendan Carr wrote a letter to Tim Cook and Sundar Pichai requesting to remove TikTok from their respective app stores citing national security threats. Investor expectations regarding a nationwide ban on TikTok, therefore, are not unfounded.

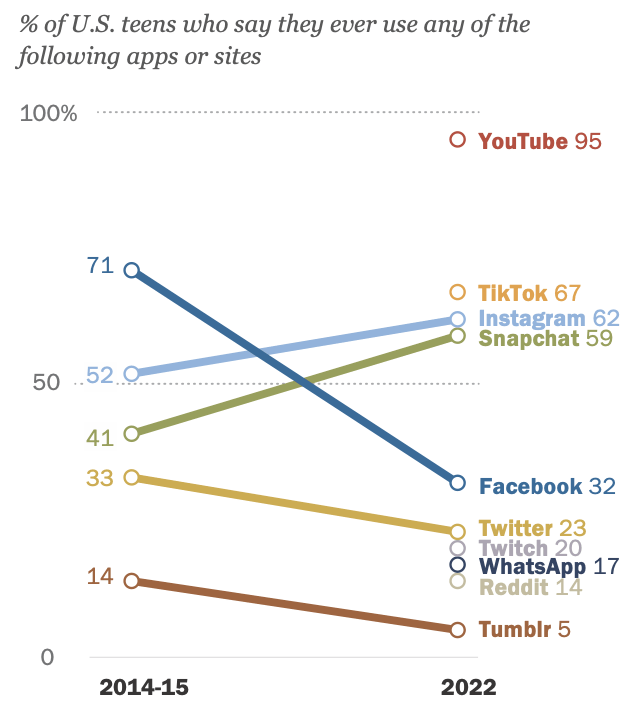

In the U.S., Snapchat is one of the prime contenders of TikTok as Snapchat offers a somewhat similar short-form video-sharing platform for users. In addition, both Snap and TikTok fight for market share in the same demography; Generation Z. Considering these factors, it makes sense to believe that a nationwide ban on TikTok will be a net positive for Snapchat. Last year, a Pew Research survey of U.S. teens found that Facebook usage among teens has declined sharply from 2014-15 while TikTok, Snapchat, and Instagram have become the most popular social media apps among teens.

Exhibit 1: Social media usage trends of U.S. teens

Pew Research

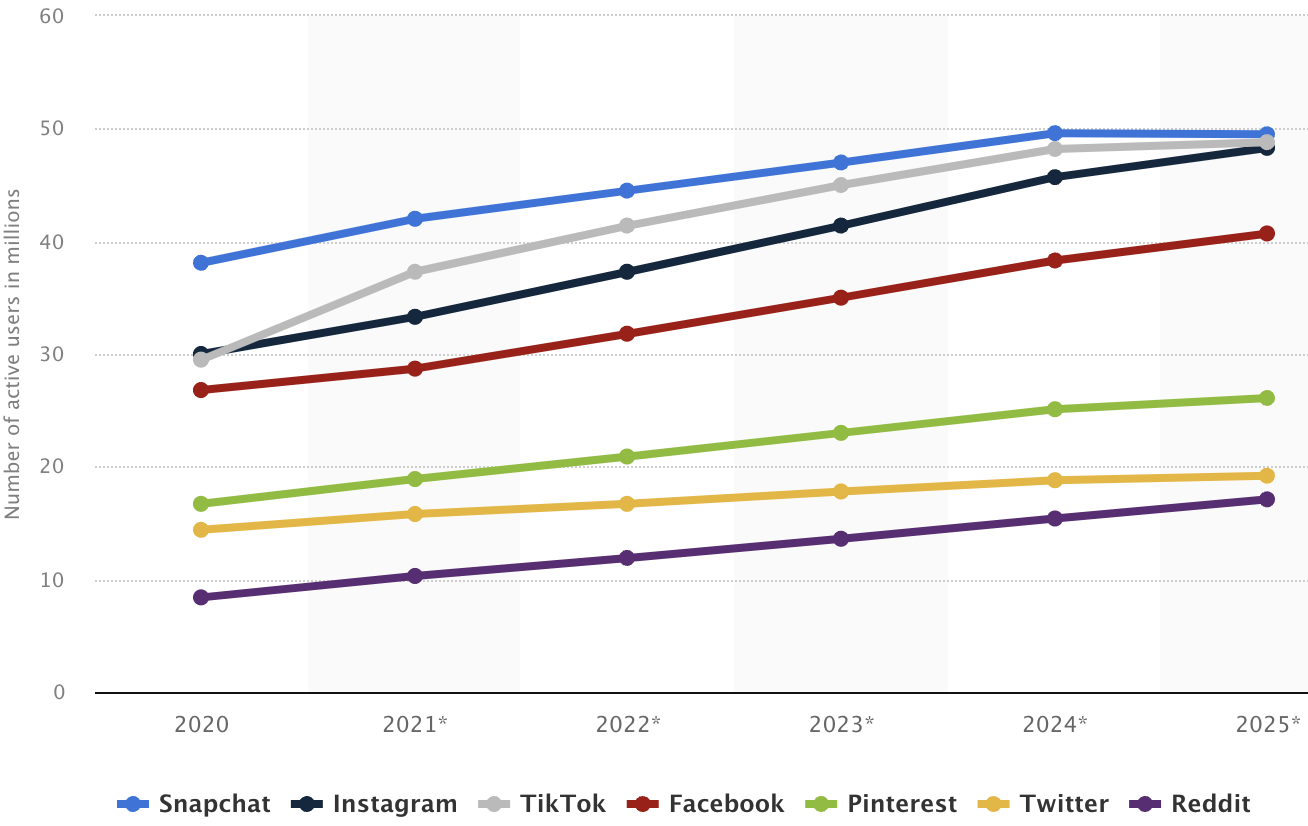

According to data from Statista, Snapchat was the most popular social media platform among Gen Z users in the U.S. back in 2021 but both TikTok and Instagram are expected the close the gap by 2025.

Exhibit 2: Number of Generation Z users in the United States on selected social media platforms

Statista

Considering the magnitude of the challenge posed by TikTok, it seems reasonable to expect a positive market response to Snap stock whenever American regulators focus on penalizing TikTok.

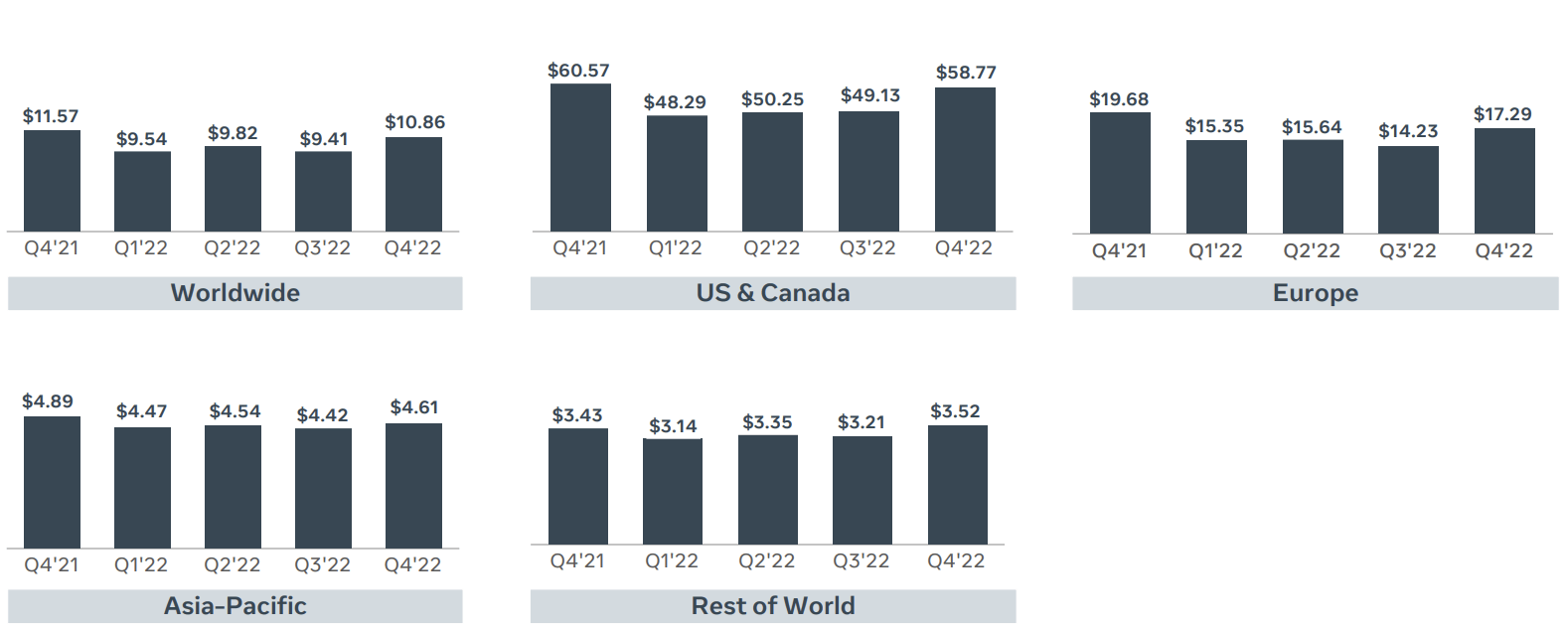

The ARPU Problem

Snap’s advertising revenue depends on daily active users and the average revenue per user. As I discussed in my previous article, Snapchat continues to attract new active users but the company is failing to monetize these users because of two primary reasons.

- Snapchat, until recently, was primarily used to direct-message with friends and family, and therefore, plugging in advertisements seamlessly proved to be a big challenge for the company. This is a fundamental issue faced by Snap.

- Snap’s rivals such as Facebook, owned by Meta Platforms, offer advertisers advanced tools to measure the performance of their ads and target the correct audience. These advanced measurement tools enable advertisers to earn more bang for the buck.

In my investment thesis for the company, I highlighted how Snap is addressing both these concerns with a renewed focus on increasing user engagement and investing in offering a data-rich experience to advertisers. None of these measures, however, could turn things around for the company in the fourth quarter of 2022.

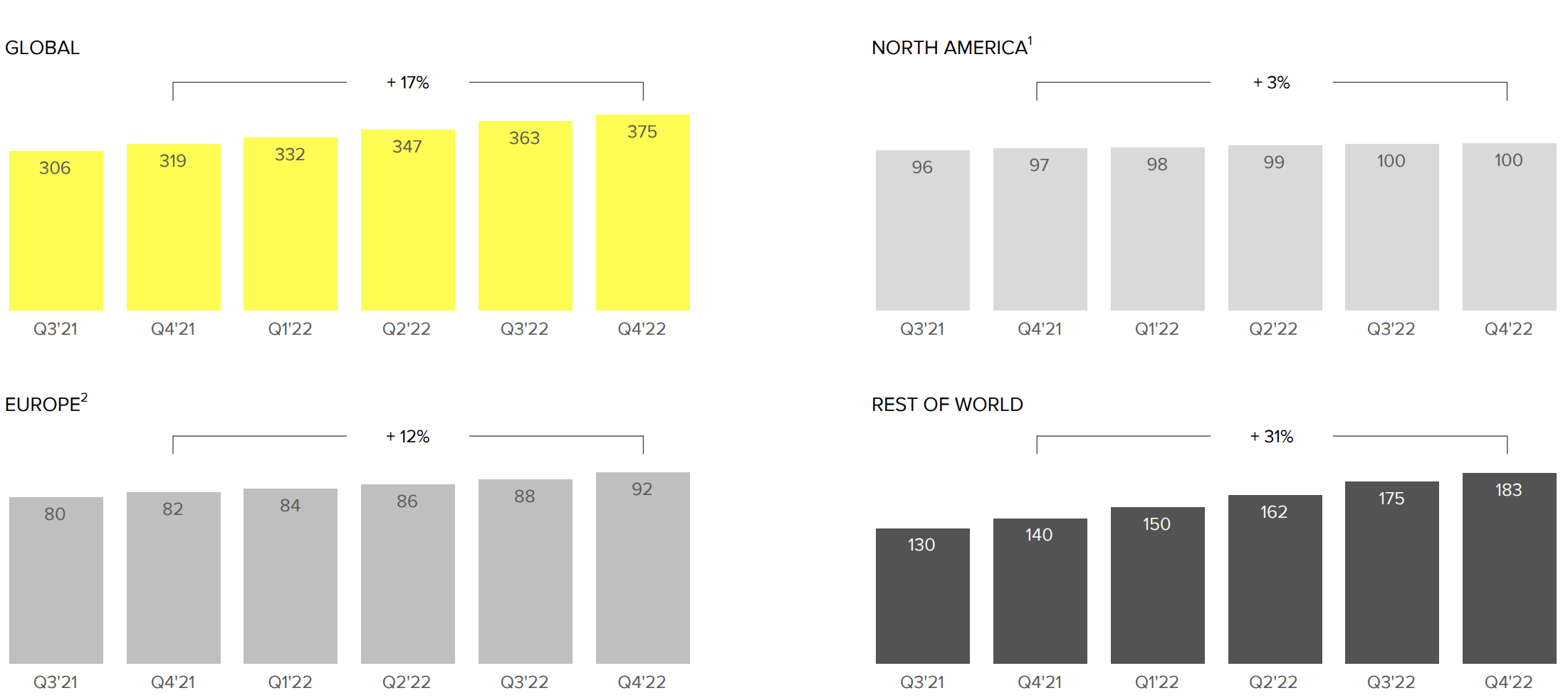

In Q4, DAUs increased 17% YoY to 375 million but revenue remained flat because of a 15% decline in ARPUs to $3.47 from $4.06 a year ago. Some of the negative impacts from revenue were masked by cost savings but there is no denying the fact that ARPUs are trending in the wrong direction. There are two major reasons behind the notable decline in ARPUs, and each of these reasons needs scrutiny.

- Macroeconomic challenges limiting the growth of the advertising industry.

- The composition of daily active users.

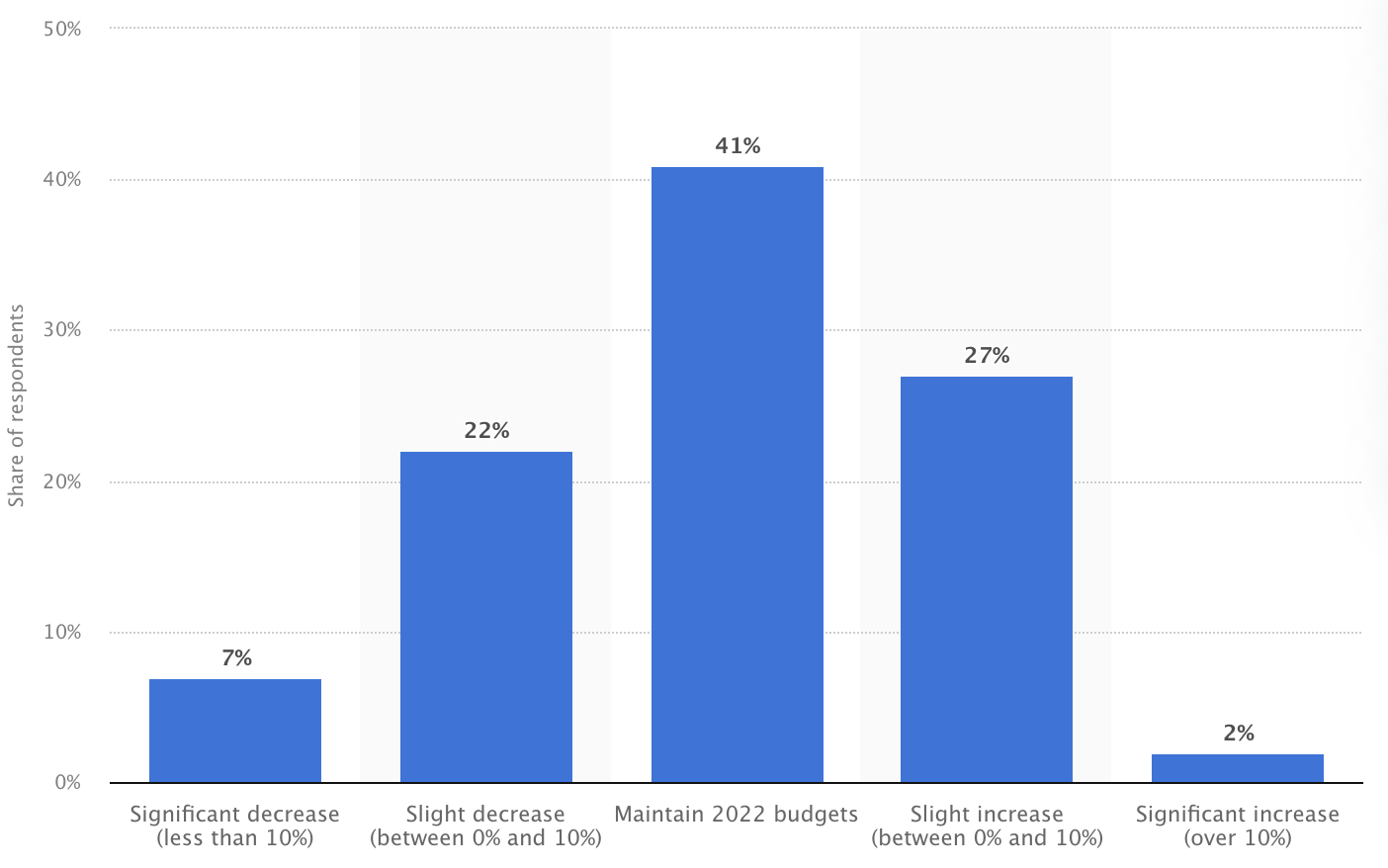

First, let’s look at how macroeconomic challenges are impacting Snap’s ARPUs. When a recession looms, corporate spending on advertising declines sharply as companies focus on maintaining appropriate liquidity levels going into the crisis. A Statista survey of 43 global brands found that 70% of companies will either maintain their marketing budget or slash it this year with only 30% of companies planning to increase their marketing budget in 2023.

Exhibit 3: Expected change to media budgets in 2023

Statista

This observation is in line with what we have seen during previous economic downturns, and I would be pleasantly surprised if 41% of respondents who are willing to maintain their marketing budgets this year actually end up doing so if the U.S. enters a recession.

With every social media company fighting for a declining pool of ad dollars, a notable decline in ARPUs seems unavoidable for Snap. However, to validate this, we need to evaluate the performance of its closest rivals as well.

| Company | YoY ARPU change in Q4 2022 |

| Snap | (15%) |

| Meta Platforms | (8%) |

| 1% |

Source: Company filings

From the data in the above table, it is evident that Snap’s struggles extend far beyond macroeconomic challenges as both Meta and Pinterest, Inc. (PINS) have performed better in comparison to Snap in the most recent quarter. This observation suggests Snap still has many things to sort out internally at a time when the industry outlook is not promising.

Snap revealed in the recent earnings call that ad impressions grew 8% YoY while ad CPM declined by 9%, completely offsetting the positive impact of ad impression growth. There is no doubt that macroeconomic challenges are limiting Snap’s potential but at the same time, the company still needs to invest and improve its ad delivery and measurement platform to attract and retain advertisers.

Second, we need to look at the composition of daily active users as this could be a major reason behind Snap’s declining ARPUs. If we look at more granular data related to DAUs, it becomes clear that the bulk of DAU growth is coming internationally, as expected. Although there is still room for growth, Snap is mature in North America compared to many of its international markets. Asia is one of the fastest-growing markets for Snapchat and many other social media platforms, and so is Latin America.

Exhibit 4: Snap DAU breakdown

Earnings presentation

The higher proportionate growth in DAUs in the Rest of World demography will have a negative impact on Snap’s ARPUs as revenue generated in this region per user will remain substantially lower than in North America for quite some time.

| Region | DAUs (millions) | Revenue (millions) |

| North America | 100 | $880 |

| Europe | 92 | $219 |

| Rest of World | 183 | $201 |

Source: Company filings

While Snap generated revenue of $8.80 per active user in North America in Q4, ARPU declined to just over $1 in the Rest of World region. Considering the bulk of user growth is coming from the Rest of World region, it is not a surprise that the company is facing a massive obstacle in increasing ARPUs. However, this is not a problem unique to Snap. Facebook faces a similar problem despite investing substantial amounts of money to improve the ad delivery experience in Asia and emerging markets in other regions.

Exhibit 5: Facebook average revenue per user in Q4 2022

Earnings presentation

It would take many years and billions of dollars in IT infrastructure investments for the social media industry to make the most of its active users outside of North America. Snap is doing the right thing by aggressively expanding outside of North America to win active users in the hopes of monetizing them in the future.

Takeaway

Snap is moving in the right direction but this will not be reflected in the company’s financial performance in the foreseeable future. Competition in the industry will continue to increase in coming years as social media giant Meta is already investing aggressively to win back Gen Z users who are moving away from its crown jewel, Facebook. Although l remain bullish on the long-term prospects for Snap, I believe it makes sense to cautiously invest in the company rather than jumping on board based on recent optimism that may not last long.

Be the first to comment