NYCstock

Snap (NYSE:SNAP) just reported a solid quarter and guided to very conservative Q4 numbers, causing the market to run in fear. The social media company is oddly preparing for a hurricane by announcing another $500 million share buyback. My investment thesis is finally Bullish on the stock following a Bearish view since nearly $60 due to Snap trading based on pending doom I think is unlikely to arrive.

Is A Hurricane On The Way?

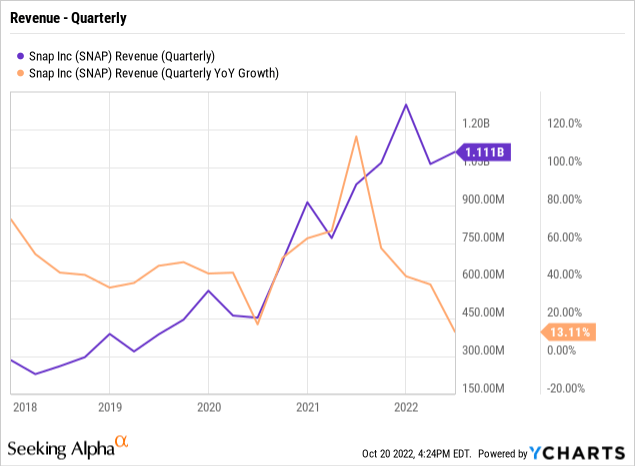

Everyone knows the advertising market is tough with the Federal Reserve aggressively hiking interest rates and the global economy headed into a recession. Snap reported Q3’22 revenues of $1.1 billion, up 6% from last year. The company slightly missed revenue targets, but any revenue growth is solid at this point in the cycle.

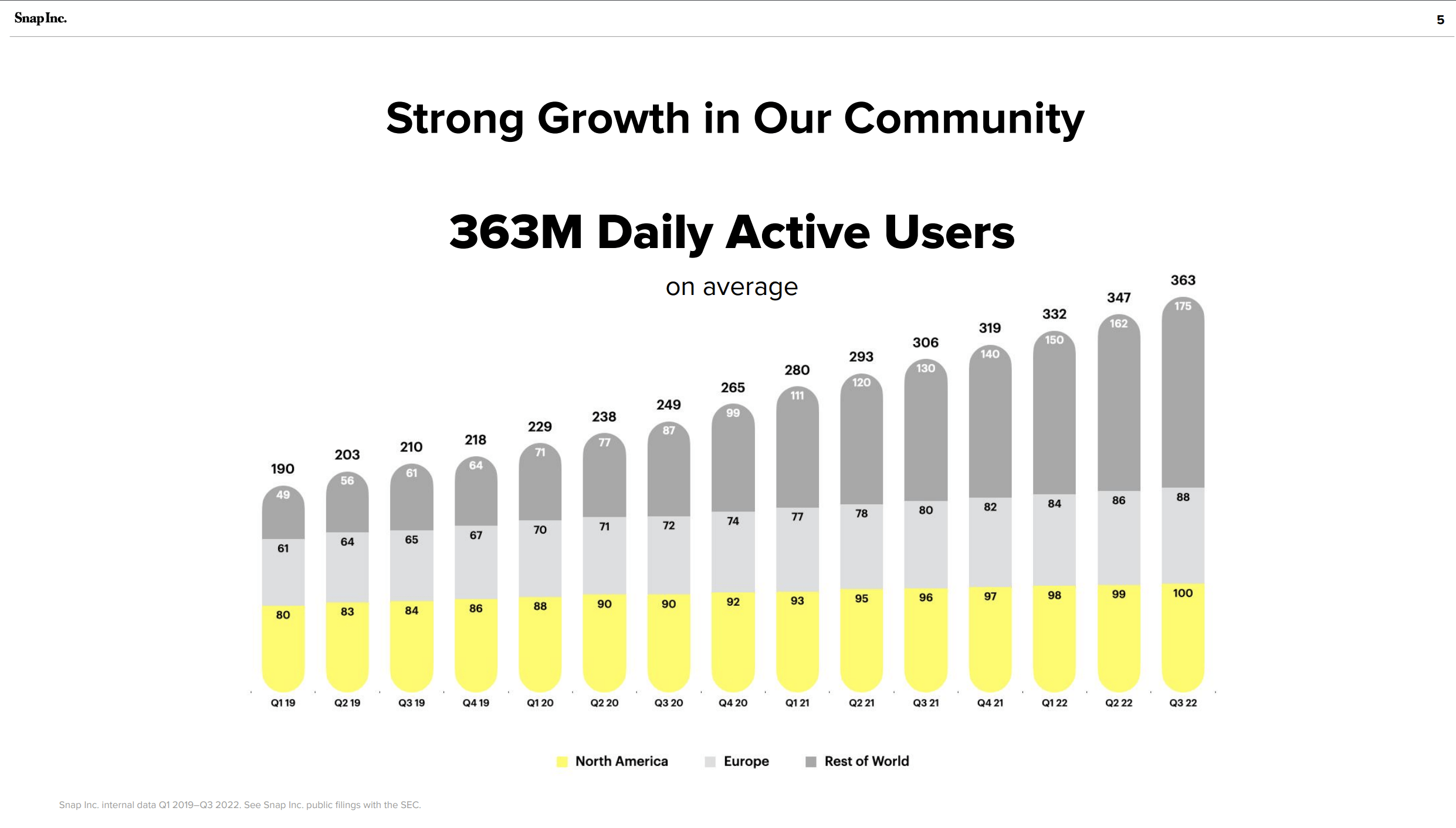

As usual though, social media companies should be valued more on user growth and Snapchat is back into full growth mode. The company reported quarterly daily active users (DAUs) up a very impressive 19% to 363 million. The social messaging service is seeing strong growth in ROW with key North America and Europe markets showing slight growth.

Source: Snap Q3’22 presentation

Any social media company growing users at this rate should be worth more money now. With the Covid normalization over, investors can now value a company like Snap based on a better picture of the going forward view of the business.

This statement by the company in the Q3’22 Investor Letter is being utilized by algos and traders to sell off the stock in my opinion:

As we look toward Q4, we are pleased with the growth we have observed in our community, and we estimate that DAU will be approximately 375 million in Q4. Thus far in Q4, we have observed revenue growth of approximately 9% year-over-year. Forward looking revenue visibility remains incredibly challenging, and this is compounded by the fact that revenue in Q4 is typically disproportionately generated in the back half of the quarter, which further reduces our visibility. Given these factors, we do not intend to provide formal financial guidance for Q4. That said, we believe it is highly likely that year-over-year revenue growth will decelerate as we move through Q4, due in large part to the fact that Q4 has historically been relatively more dependent on brand-oriented advertising revenue, which declined slightly on a year-over-year basis in the most recent quarter. As a result, we have set our internal forecasts based on the assumption that year-over-year revenue growth will be approximately flat in Q4, and we estimate that Adjusted EBITDA would be approximately $200 million under that revenue assumption for Q4.

Snap just pulled a classic under promise and over deliver performance. The company has seen revenue growth of ~9% 20 days into the quarter, but somehow revenues are going to decelerate to the point where revenues for the quarter will end flat YoY with the $1.3 billion reported last Q4. Snap made a very key statement with the “assumption” part of the phrase.

As the below chart highlights, Snap has already seen revenues more than double from the Q4’19 levels of $561 million. The company saw growth rates accelerate above 100% after the initial slowdown in 2020.

Stock Buyback

Snap announced a $500 million share buyback, which plays as odd considering the guidance for brutal revenue in November and December. The company already bought another $500 million worth of shares during Q3 and has $4.4 billion in cash on the balance sheet, but management has no reason to buy shares into collapsing revenue, if the assumption made by the company is accurate.

The after-hours stock action is interesting considering the numbers were all generally bullish outside of the ad-hock commentary on the remaining part of Q4. Snap doesn’t appear to have any data actually supporting the conservative forecasts.

In such a dire situation, management shouldn’t be so aggressive on share buybacks. The stock is down 25% in after-hours trading providing a prime opportunity to purchase another $500 million worth of shares, only if the company predicts the business snap.

Source: Seeking Alpha

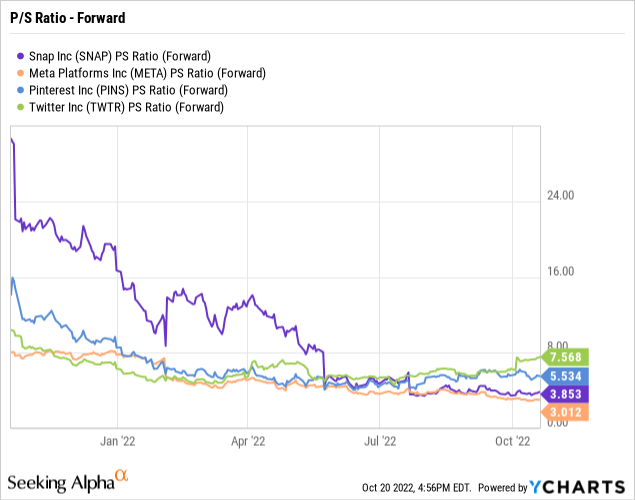

The market cap is down to only $13.6 billion and will likely fall further with a share buyback. Snap hasn’t been this cheap in history with the stock last trading this low pre-covid when revenues were far lower.

Snap is now approaching the lowest forward P/S ratio in the social media space depending on how the stocks shake out tomorrow. The stock is trading at close to 3x ’23 sales targets with a P/S multiple similar to Meta Platforms (META) and far below where Twitter (TWTR) is being taken out by Elon Musk and Pinterest (PINS) trades.

Takeaway

The key investor takeaway is that now is when investors should use the weakness to consider a position in Snap. With fears the revenue trends will only turn negative next year, investors don’t have to rush into the stock here. Ultimately though, Snap is as cheap as ever with the stock at $8 and investors should use maximum fear here to start buying shares.

Be the first to comment