Alistair Berg/DigitalVision via Getty Images

Chalk up the year-end selloff to interest rates, macro uncertainty, and tax-loss selling: but in my view, investors should be positioned for a rebound next year, and for me that means buying into battered growth stocks again. And even within the growth space we need to be selective, and focus particularly on companies that have shown the ability to scale toward profitability and are also trading at attractive valuations.

Smartsheet (NYSE:SMAR) is an excellent example of this “growth at a reasonable price” play. A collaboration and workflow software vendor, Smartsheet’s technology continues to be propelled forward by secular tailwinds toward remote work and hybrid teams, even in the post-pandemic era. Growth rates remain strong even as Smartsheet achieves a much larger scale.

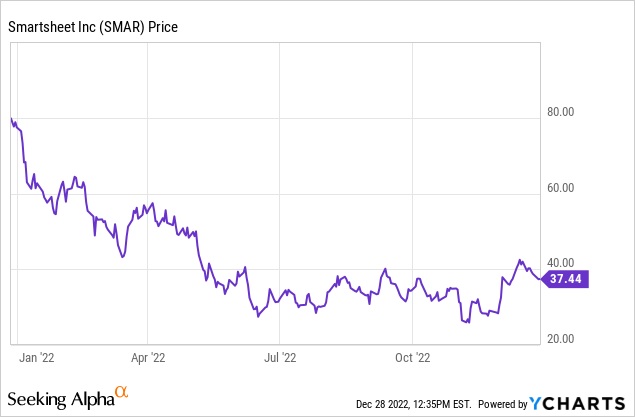

Year to date, shares of Smartsheet have lost ~50% of their value, though the company has been on an uptrend since late summer on the back of strong quarterly results.

I remain very bullish on Smartsheet heading into 2023, and it remains a core holding in my portfolio. The stock decline this year was based almost purely on weakened sentiment toward growth: but amid a massive loss of market value, Smartsheet has remained focused on hitting its growth targets while scaling toward profitability.

Here is my full bull case on Smartsheet:

- Remote work is going to continue being the “new normal” – Now realizing that productivity doesn’t suffer as much as originally thought when teams go remote, some companies are relaxing their expectations for employees to be fully back in the office even after the pandemic subsides. Some companies have even let their employees know it’s okay to work remotely indefinitely. But remote teams need a workspace to collaborate in, and tools like Smartsheet are perfect complements for that. This is especially true for distributed teams, where people are in different locations and some are in-person while others are remote: tools like Smartsheet help to rein in the geographic distance.

- Smartsheet is moving to bigger and bigger deals, and expansion rates remain high – As Smartsheet has proven its utility and flexed its muscles as a more prominent public company, the company has been able to sign larger deals. In its most recent quarter, its count of >$100k ACV customers grew 55% y/y to more than 1k such customers. The average customer is also upgrading their relationship with Smartsheet: net revenue retention rates are clocking in around 130%, which exceeds most other SaaS stocks.

- Horizontal software and broad use cases – Smartsheet is broadly applicable to virtually any industry and virtually any team or function within a company, making its addressable market wide.

- High gross margins – Smartsheet’s 80%+ pro forma gross margins are among the highest in the software industry, and enable the company to achieve significant operating leverage as it scales.

- Nearing profitability – Despite still-robust growth rates, Smartsheet is able to hover around breakeven profitability (on a pro forma operating margin basis), demonstrating the leverage inherent in the software business model made possible by high gross margins.

The valuation also remains quite modest. At current share prices near $37, Smartsheet trades at a market cap of $4.91 billion. After we net off the $434.7 million of cash (against no debt) on the company’s most recent balance sheet, Smartsheet’s resulting enterprise value is $4.48 billion.

Meanwhile, for FY24 (the fiscal year for Smartsheet ending in January 2024), Wall Street analysts have a consensus revenue target of $964.2 million for the company, representing 27% y/y growth (data from Yahoo Finance). This puts the stock’s valuation at just 4.6x EV/FY24 revenue – a bargain for a company growing at this rate and achieving near-profitability.

The bottom line here: the market continues to undervalue Smartsheet despite its fundamental strengths in the face of tough macro headwinds. A combination of continued quarterly beats plus an undemanding valuation will be key catalysts to sparking a rebound in 2023.

Q3 download

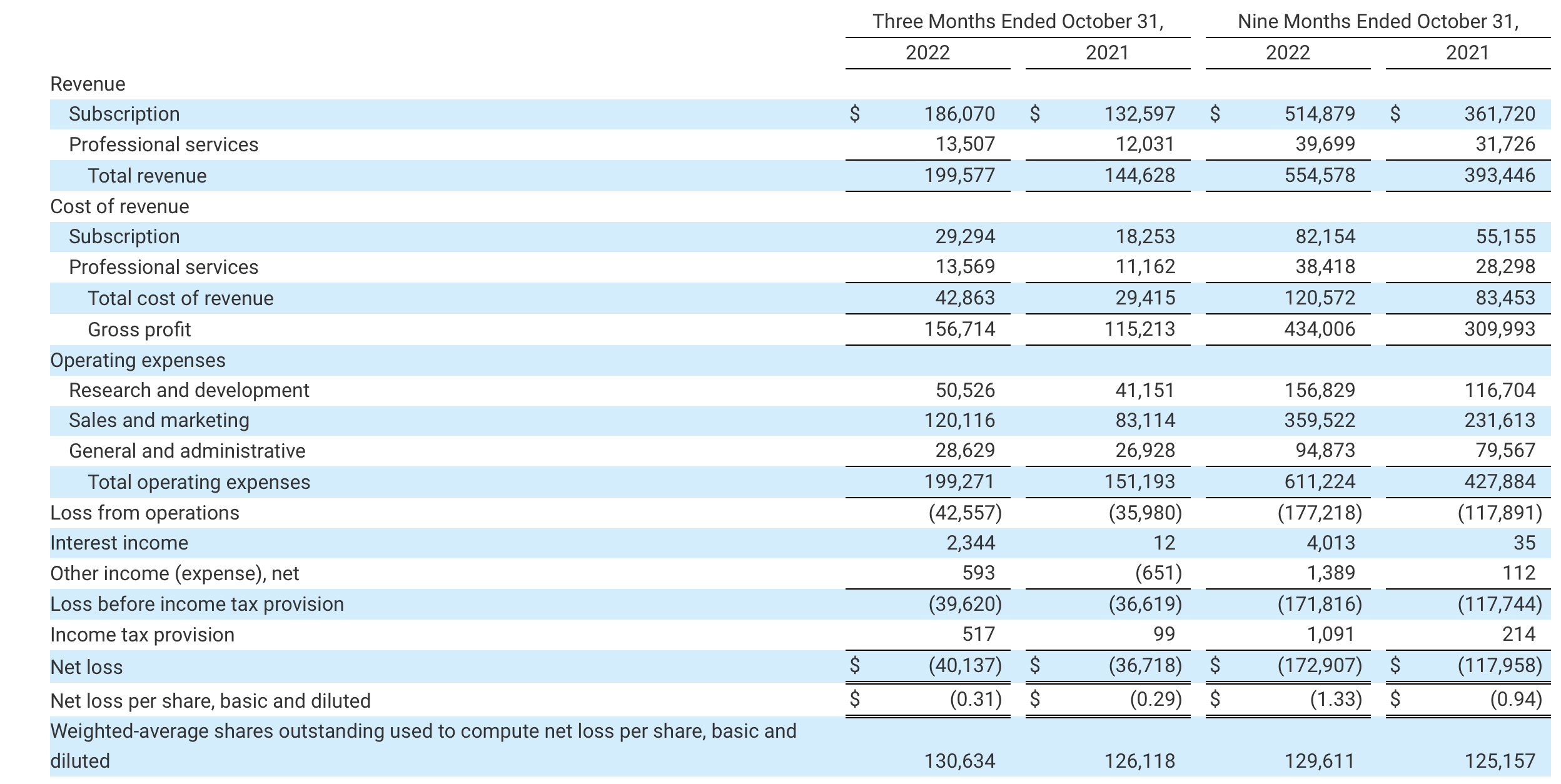

Earnings beats have been relatively scarcer in the software sector in the back half of 2022, but Smartsheet has not disappointed. Take a look at the company’s most recent Q3 results below, released in early December:

Smartsheet Q3 results (Smartsheet Q3 earnings release)

Smartsheet’s revenue grew 38% y/y to $199.6 million, beating Wall Street’s expectations of $194.7 million (+35% y/y) by a robust three-point margin. Revenue growth did decelerate from 43% y/y growth in Q2, but A) this was common across the software sector this quarter due both to macro and FX headwinds sharpening, and B) this was already portended by the company’s billings growth slowing to 36% y/y in Q2.

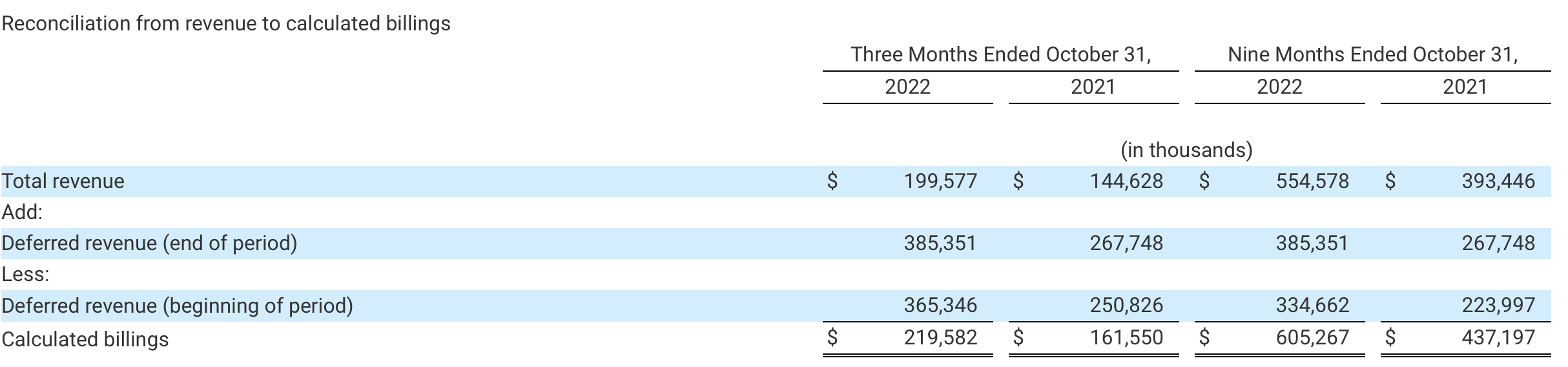

Thankfully, billings growth continued to keep pace with Q2. Billings of $219.6 million grew 36% y/y in the quarter, and hopefully signal that growth will remain in the mid-high 30s for several quarters to come (which would mean opportunity on top of Wall Street’s 27% y/y growth consensus for FY24).

Smartsheet bilings (Smartsheet Q3 earnings release)

Management noted strong performance from its sales teams, calling out that new sales reps have improved their wins as well as pipeline generation. Smartsheet also believes it has entered Q4 with a record pipeline. Per CEO Mark Mader’s prepared remarks on the Q3 earnings call:

Our strong expanded climb motion within our customer base continued with 235 customers expanding by $50,000 or more and 79 customers expanding by $100,000 or more. We also now have 40 customers with ARR over $1 million. And we ended the quarter with more than 11.7 million Smartsheet users. Last quarter, we discussed how our new sales reps were ramping more slowly than sales reps from previous years. This quarter, we saw improvements in quota attainment and pipeline generation from our newest reps. We exited the quarter with a record pipeline, improved after macro-related softening in Q2. We also made significant improvements to our profitability in Q3.”

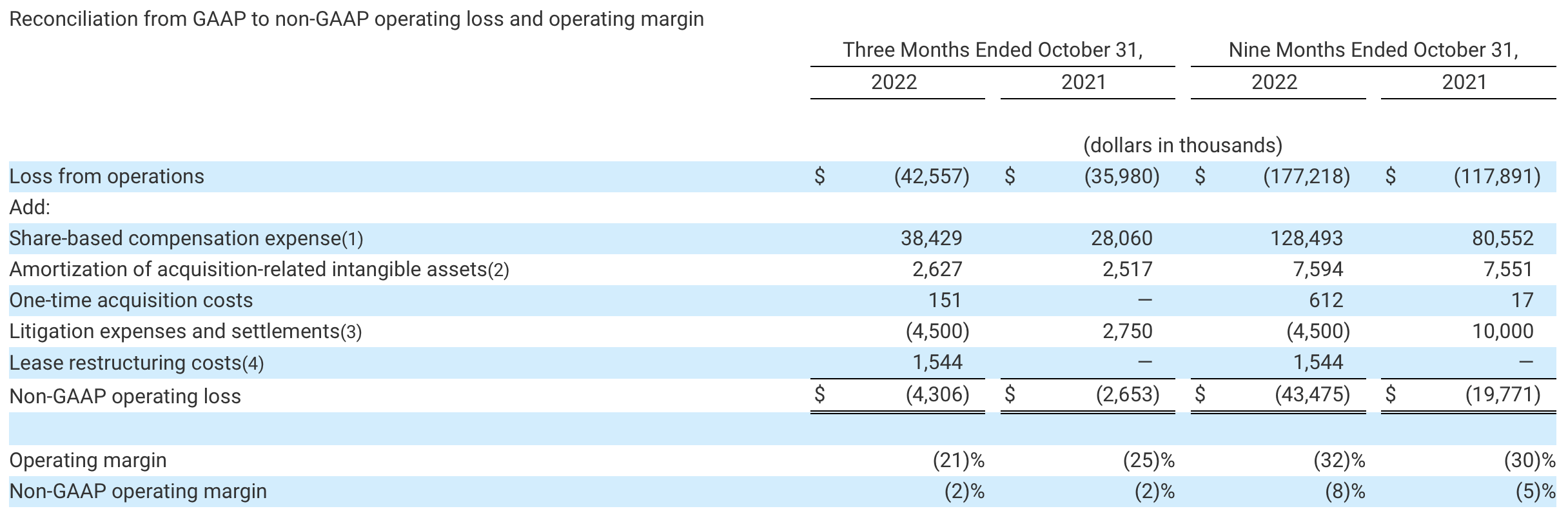

Smartsheet also delivered on the bottom line as well. Pro forma operating margins clocked in at -2%, representing seven points of sequential improvement versus -9% in Q2 and flat y/y – which is impressive as most companies have cited opex inflation as the driver behind steep operating margin declines.

Smartsheet margins (Smartsheet Q3 earnings release)

Smartsheet, on the other hand, drove early cost rationalization efforts alongside a targeted hiring slowdown. The company also raised its free cash flow outlook for the year (to positive $5 million), and pro forma EPS of -$0.01 in the quarter dramatically outpaced Wall Street’s -$0.15 expectation.

Key takeaways

There’s a lot to like about Smartsheet heading into 2023: robust growth rates, a path toward breakeven profitability and positive cash flows, and a sticky software product with ~130% retention rates – all trading at a very reasonable price. Though a relatively unknown and out-of-the-spotlight name, stick with this stock for a 2023 rebound.

Be the first to comment