GeorgePeters/E+ via Getty Images

Small and mid caps are now testing critical breakout levels, and despite the strength in equities in the past month, investors have arguably not trusted this rally.

After all, what is there to be optimistic about when we are supposedly entering a recession next year?

Nevertheless, I urge traders and investors to focus on the price action alone, and pay special attention to a market that manages to break out of a big base.

That is exactly what the Russell 2000 (IWM) and SPDR Midcap ETF (MDY) are poised to do – they are right at key breakout levels that could take them out of 1.5 year bases.

If they succeed in doing so, there is high potential for explosive upside.

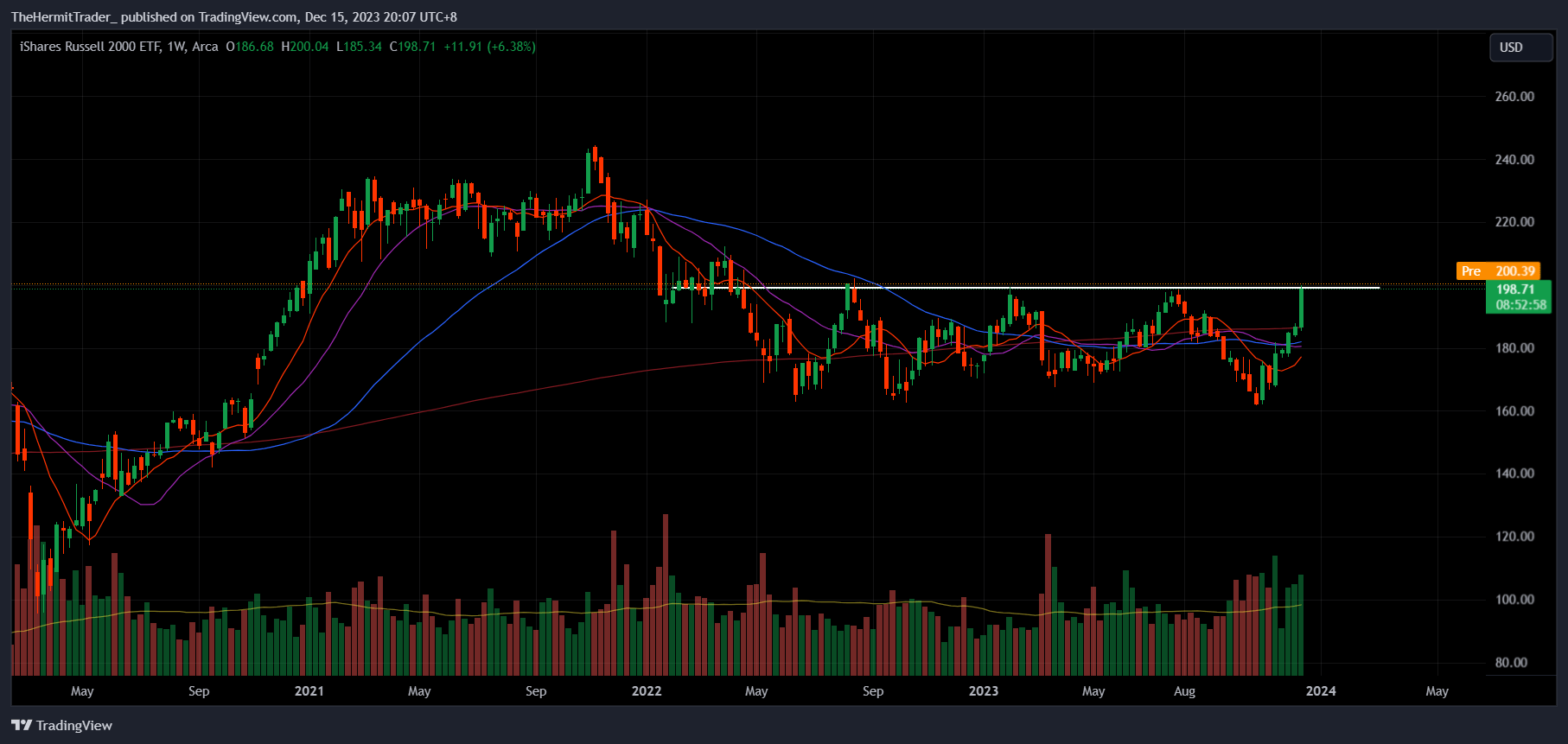

First, let us look at the charts. The Russell 2000 (IWM) is testing the key 200 level for the 4th time in the past 1.5 years.

Looking at the manner in which the S&P 500 (SPY) and Nasdaq 100 (QQQ) are at or close to all-time highs, I think odds are that the IWM breaks out of this base.

Weekly Chart: IWM

Tradingview

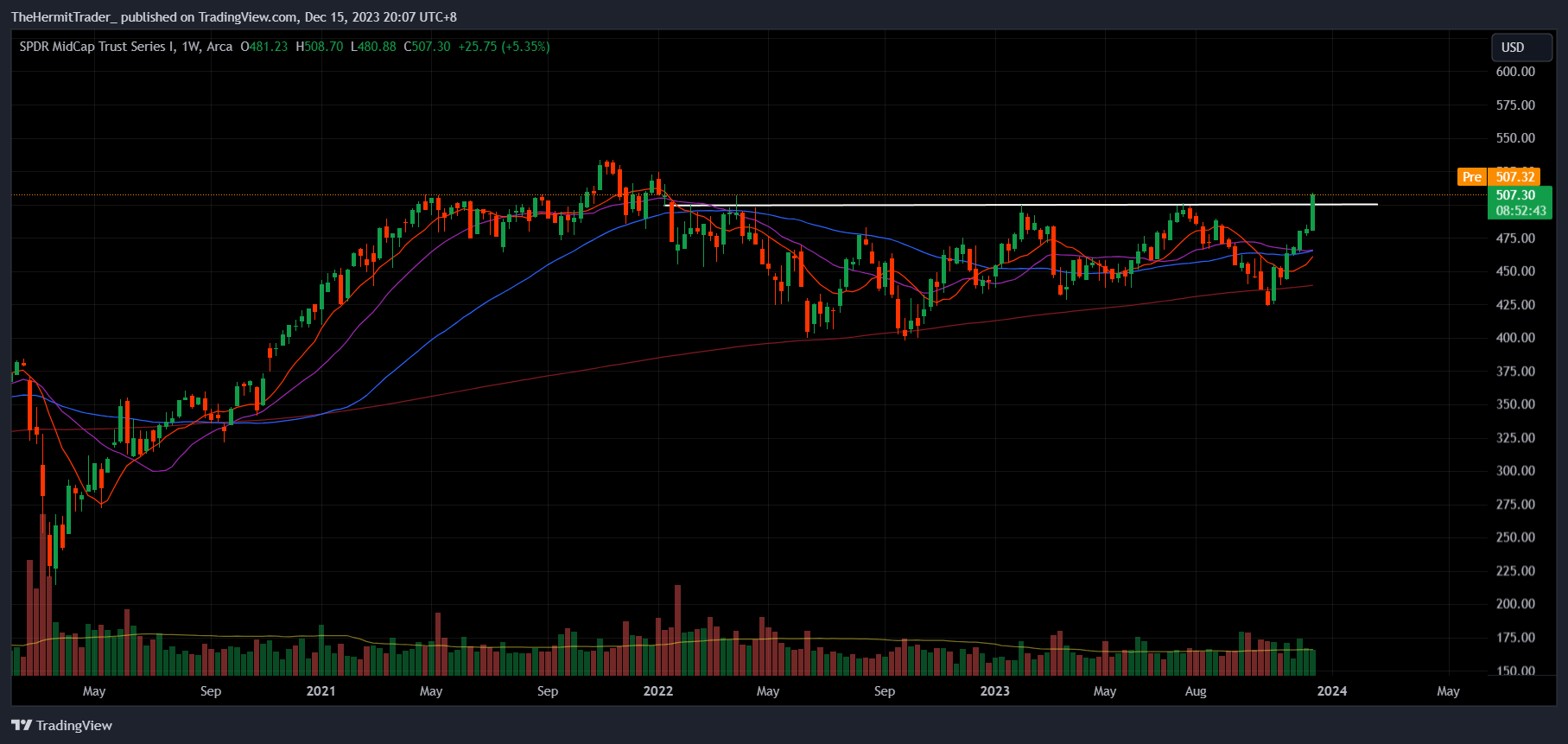

Midcaps also look poised to breakout from their base. The chart of the SPDR Midcap ETF (MDY) looks very similar to that of the IWM.

MDY is faring better than IWM, as they are closer to their highs than the latter.

Weekly Chart: MDY

Tradingview

There could be huge upside potential if small and midcaps successfully breakout.

For one, small and midcaps have lagged large and mega caps. IWM is still at levels seen in 2020 while MDY is at levels seen in 2021.

The SPY and QQQ are up +23% and +51% YTD, while IWM is up +13% and MDY is up +15%.

I first wrote here on 28 November that small and mid caps were going to breakout higher. Since then, IWM has risen +11%, and I do not think the rally is going to stop here.

As IWM is made up of a more diverse number of sectors, unlike SPY and QQQ which are dominated by technology, we are likely to see a higher frequency of sector rotations. Rotations are the lifeblood of a bull market, and would be constructive for the rally.

Yahoo Finance

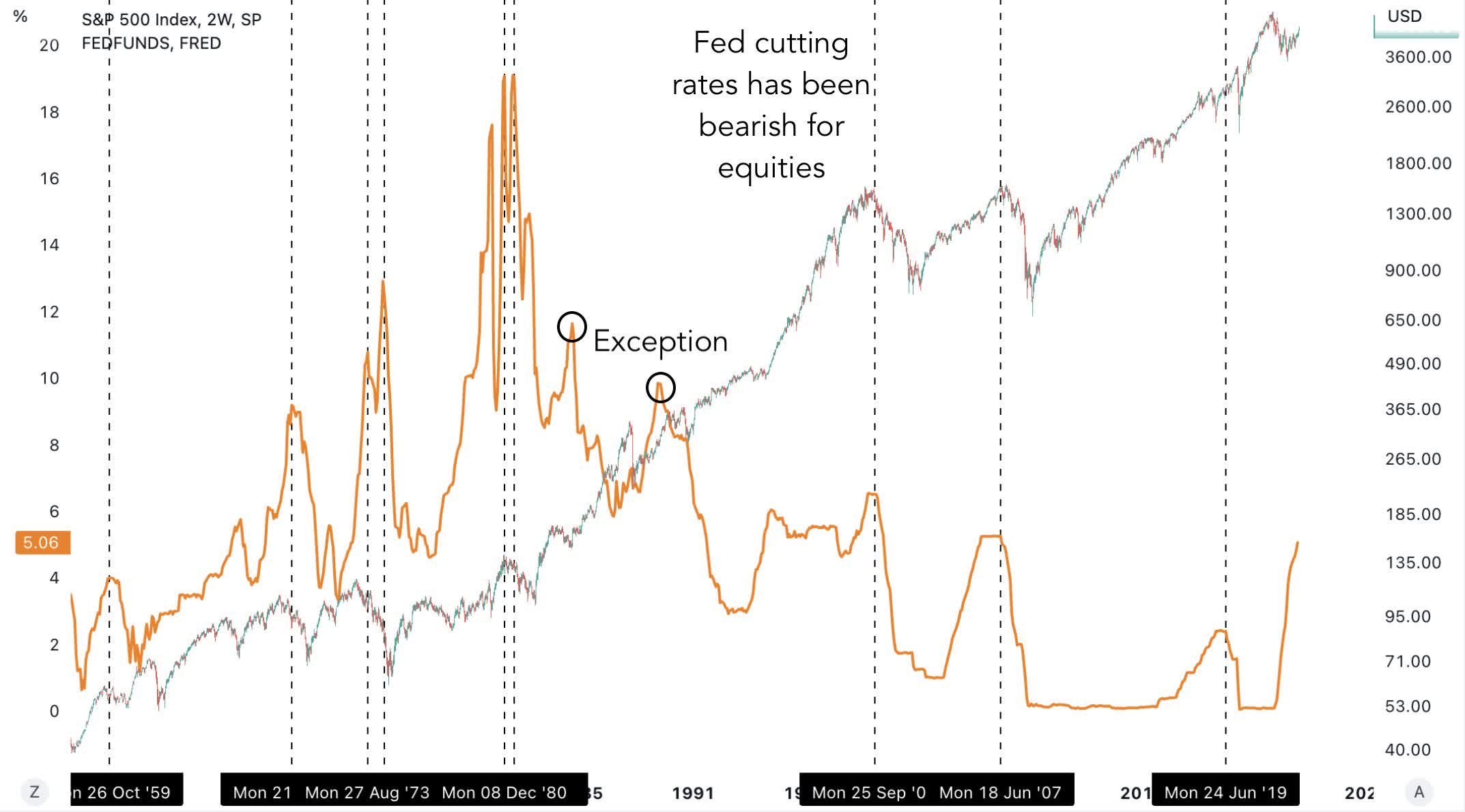

A fundamental macro catalyst that could fuel the rally in small and mid caps is a dovish Fed.

In this week’s FOMC, Powell’s comments were dovish, with the central bank now expecting 2023 to end with a core inflation rate of 3.2% versus 3.7% expected three months earlier.

While Powell mentioned inflation is still above the central bank’s target of 2%, and there is no need to entertain the thought of cutting rates for now, I believe this is the best situation for stocks to be in.

That is because actual rate cuts have historically been bearish for equities. The current situation is constructive – bond yields and the USD are softening, but we are not seeing the Fed actually taking action to cut rates.

Tradingview

I remain long IWM, and am targeting new all-time highs in this. I am however, watchful of a “false breakout” – that is, if prices breakout of the base, and then swiftly selling off and losing the breakout. That would be a tell that my thesis is likely wrong.

Be the first to comment