onurdongel/E+ via Getty Images

SM Energy (NYSE:SM) may now be able to generate over $1.2 billion in positive cash flow in 2022 at current strip prices. This would allow it to reduce its leverage to 0.3x by the end of 2022, as well as potentially redeem more of its notes.

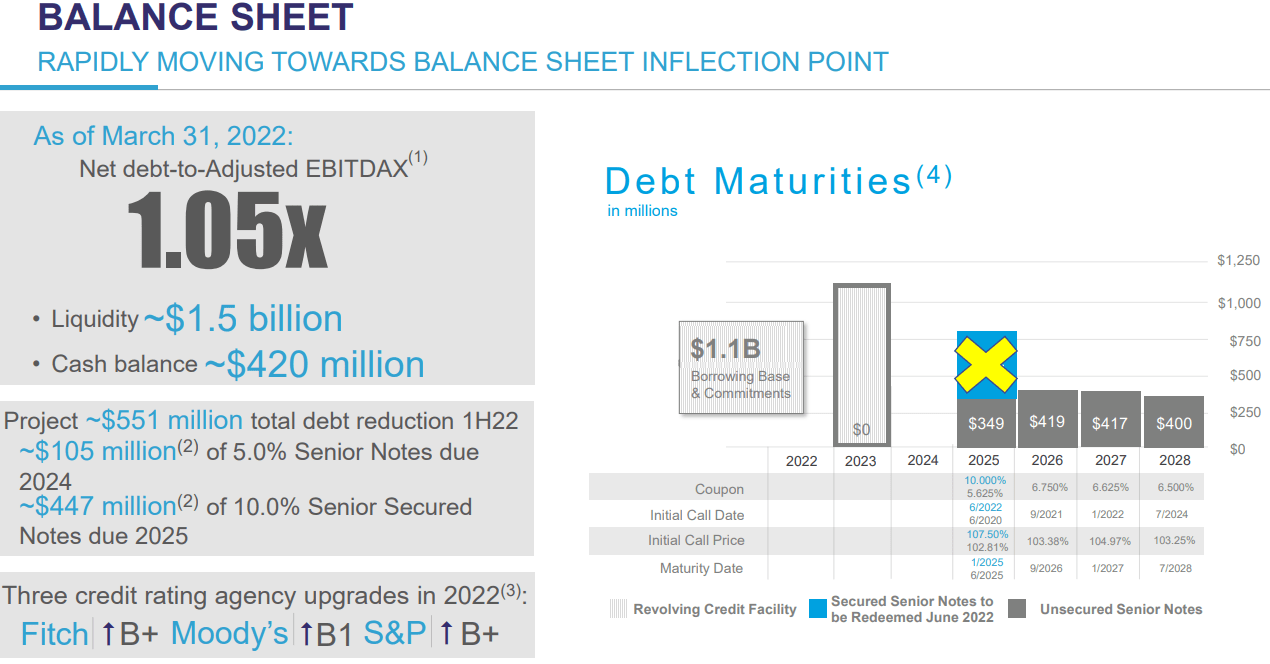

It has already redeemed its 5.0% unsecured notes due 2024 and is in the process of redeeming its 10.0% second-lien notes due 2025. It could also redeem its 5.625% unsecured notes due 2025 and its 6.75% unsecured notes due 2026 this year, leaving its next note maturity in 2027. This would also reduce its annual interest costs to approximately $54 million per year, down from around $152 million at the start of the year.

2022 Outlook At Current Strip

Based on current strip prices for 2022 (including roughly $108 to $109 WTI oil), SM Energy is projected to generate $3.766 billion in revenues before hedges. SM’s 2022 hedges have an estimated negative $922 million in value at current strip since it has a significant amount of hedges at prices way below strip.

| Type | Barrels/Mcf | $ Per Barrel/Mcf | $ Million |

| Oil | 24,412,500 | $107.00 | $2,612 |

| NGLs | 6,600,563 | $42.00 | $277 |

| Gas | 128,921,625 | $6.80 | $877 |

| Hedge Value | -$922 | ||

| Total | $2,844 |

Despite that large hedging loss, SM is still expected to generate $1.261 billion in positive cash flow at current strip in 2022 before dividends (which are only $2 million per year currently).

| $ Million | |

| Lease Operating | $243 |

| Transportation | $158 |

| Production and Ad Valorem Taxes | $214 |

| Cash G&A | $95 |

| Cash Interest | $123 |

| Capex | $750 |

| Dividends | $2 |

| Total | $1,585 |

SM is also calling its $447 million in 10% second-lien notes due 2025 at a price of 107.5% of par. Thus after dividends and the redemption premium, SM may be able to reduce its net debt by $1.225 billion in 2022.

Balance Sheet

This could allow SM to end 2022 with around $579 million in net debt. It may also choose to call its remaining 2025 and 2026 notes, which would cost it $13 million in redemption premiums. This would leave it with $817 million in 2027 and 2028 notes remaining along with $225 million in cash on hand. SM’s projected leverage at the end of 2022 is only 0.3x.

SM’s Debt (sm-energy.com)

SM’s interest costs would be reduced to around $54 million per year if it chooses to redeem its 2025 and 2026 notes.

Estimated Valuation

SM’s estimated value is now approximately $47 per share in a long-term (after 2022) $70 WTI oil and $3.50 NYMEX gas scenario. This is up around $2 from my previous estimates due to the improved outlook for 2022 cash flow.

In a scenario where 2023 prices follow current strip (approximately $97 WTI oil and $6 NYMEX gas) before reverting back to $70 WTI oil and $3.50 NYMEX gas after 2023, SM’s estimated value would be around $53 to $54 per share instead.

Conclusion

SM appears capable of generating over $1.2 billion in positive cash flow in 2022. This could allow it to redeem its remaining 2025 and 2026 notes, reducing its annual interest costs to around $54 million per year. SM’s leverage is also projected to be reduced to 0.3x by the end of 2022, so its balance sheet situation should be pretty good.

I estimate that SM could be worth $53 to $54 per share in a scenario where oil and gas prices follow current strip until the end of 2023 before reverting back to $70 WTI oil and $3.50 NYMEX gas after that.

I’d also expect SM to increase its dividend and institute other shareholder return plans once it redeems its nearer-term notes. Based on current strip, it could end up with close to $1 billion in net cash by the end of 2023 without any changes to shareholder returns.

Be the first to comment