designer491/iStock via Getty Images

The iShares 0-5 Years Investment Grade Corporate Bond ETF (NASDAQ:SLQD) is an instrument that investors might consider for getting some bond exposures. The problem is that it doesn’t contain the right type of bonds. Durations are somewhat long, and current declines don’t seem to reflect this ETF’s sensitivity to the rate hikes that have happened, and certainly not those that are very likely to come. While at current prices the credit risk seems to be priced in relative to reference rates, it’s likely not pricing in the incoming rate hikes despite its 2.3-year duration.

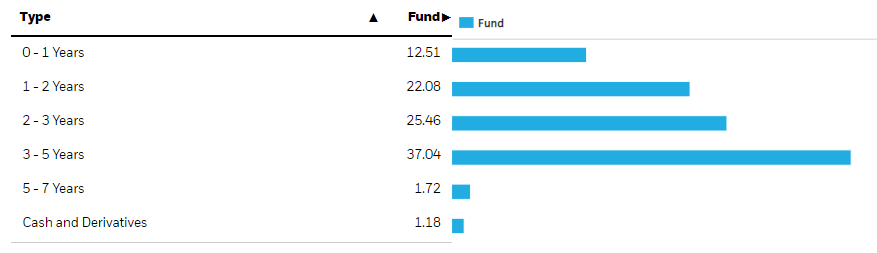

SLQD Breakdown

Bond investors cannot autopilot anymore. It’s not just a question of being a place to put cash, the duration concern should be fundamental at this point, because rate hikes are still trending higher as the Fed is determined to fight inflation rates. They know misery will come, and that’s the point – it’s the only way to stop inflation, it seems as we’ve returned to the Phillips Curve era.

If rates increase, it makes fixed coupons issued in markets where rates were assumed lower less attractive and economical. Thus, it causes capital depreciation of bonds. Duration measures how much of the cash flows from bonds come in a distant future, where the previous rate environment and not the current one has been implied. The higher the duration, the worse those future cash flows affect the bond price when rates rise.

Maturity Profile (iShares.com)

SLQD has quite long maturities, and this correlates with higher durations which reflect the effective maturity of cash flows considering also their timing in the life of the bond. Looking at the detailed holdings, the weighted average duration is about 2.3 years. What that means is that a 1% rate hike will approximately cause a 1% x 2.3 decline in the bond price, or -2.3% declines per unit rate hike. We’ve had a cumulative rate hike of about 3.5%, which implies a 7% decline should be expected in a bond portfolio with a 2.3-year duration. 6% has been the current decline, which is close but a little bit of an undershoot.

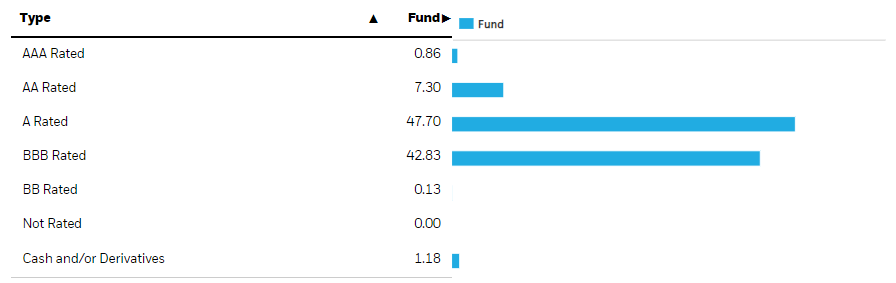

Credit Profile (iShares.com)

Looking at maturity, a lot of it is BBB rating, which can justify about a 2% premium for credit risk. With reference rates being about 3.7% right now, the YTM should be about 5.7%, but it’s actually 5.2%, which is not that far off but suggests a slight possible mismatch with the credit profile.

Remarks

The problem though is that it’s already maybe slightly overvalued based on current rates, which are consistent with the implemented rate hikes. Rates are continuing to rise, however, and that just means more declines should be coming, and the price should be anticipating that which it’s not. Therefore, the SLQD price looks rich to us still, and it may be because retail allocators are not yet properly cognizant of the declines we should be expecting from rate hikes and are attached to yield or determined to see these bonds to maturity. With the notion that the Fed might pause on rate hikes being an unlikely reality, ETFs priced as such are likely still expensive. This is not a buy.

While we don’t often do macroeconomic opinions, we do occasionally on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment