sturti/E+ via Getty Images

Investment Thesis

SLB (NYSE:SLB) is an oilfield services vendor. For investors, that means one thing. SLB is well positioned at the center of a strong and stably rising oil market.

And yet, despite clamoring that SLB is undervalued now for several months, the stock has gone nowhere fast.

So why should this time be different? The obvious headline is China’s reopening. But I proclaim that there’s more nuance beyond this headline.

I go through the bearish and bullish points facing SLB and lay out why I’m bullish on this stock.

What’s Happening Right Now?

China is reopening. Thus, one question looms large in investors’ minds. Will China’s reopening after nearly 3 years of being closed lead to enough oil demand to offset a diminished appetite for oil from a potential US and European recession?

That being said, I believe that this is an oversimplification of the events at hand. Not only is the demand picture hugely more complex than just a simple China vs the rest of the world, but there are other countries, such as India, Russia, Brazil, and the South East Asian bloc, that are huge oil consumers too.

Secondly, I don’t fundamentally buy the argument that the US and Europe will materially bring down their oil consumption, irrespective of a potential recession. Why?

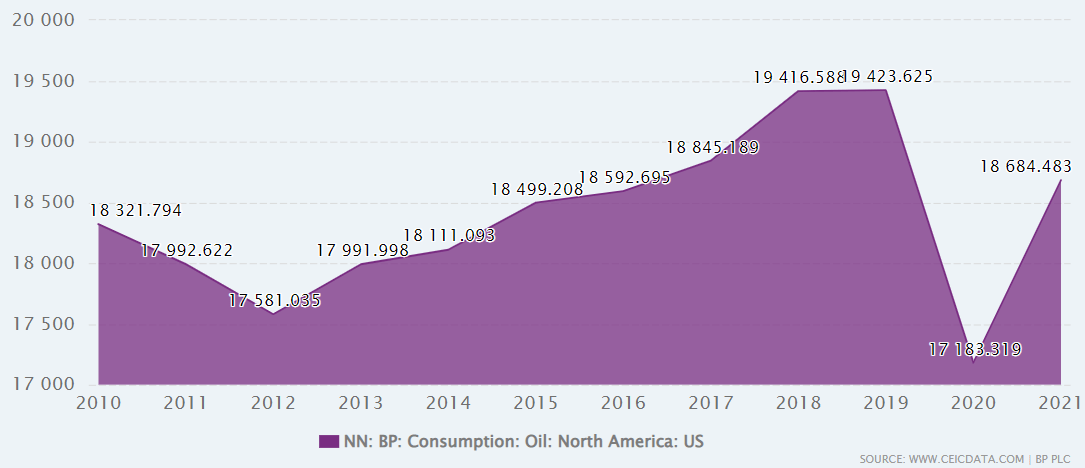

ceicdata.com

What we see here is that in 2020 in the US, when the US economy shut down, oil demand dropped by approximately 11%. Remember, the country shut down. And that saw an 11% drop. That was it.

Hence, this is my contention. I believe that we are firmly dependent on oil. With oil prices in a range of $60 to $90, we’ll continue to consume oil, and even if there’s a recession. We’ll see a global recession dent oil demand by less than 10%.

Put simply, I believe that oil prices will remain in the range of at least $60 to $90 in 2023.

And this now leads me to discuss SLB’s balance sheet.

Balance Sheet is at the Core of the Bull Case

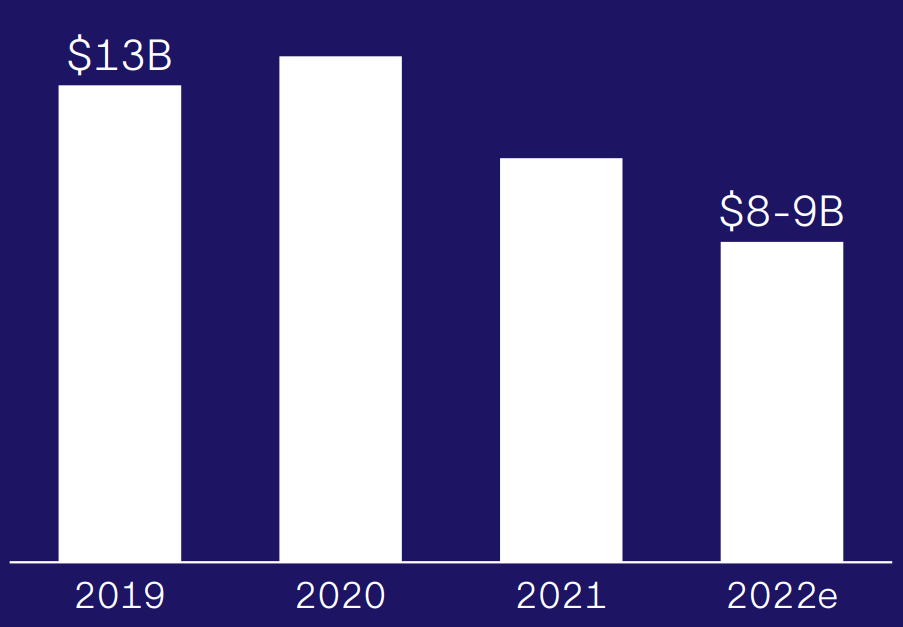

SLB is already up more than 50% in the past year. So, why get involved now? Because SLB’s balance sheet is substantially improved. After two years of strong cash flows, SLB’s balance sheet is meaningfully de-risked.

SLB Investor Day

So, this is what’s at play now. SLB won’t have to work as aggressively to shore up its balance sheet with cash to get its balance sheet into shape. This is different from previous commodity cycles.

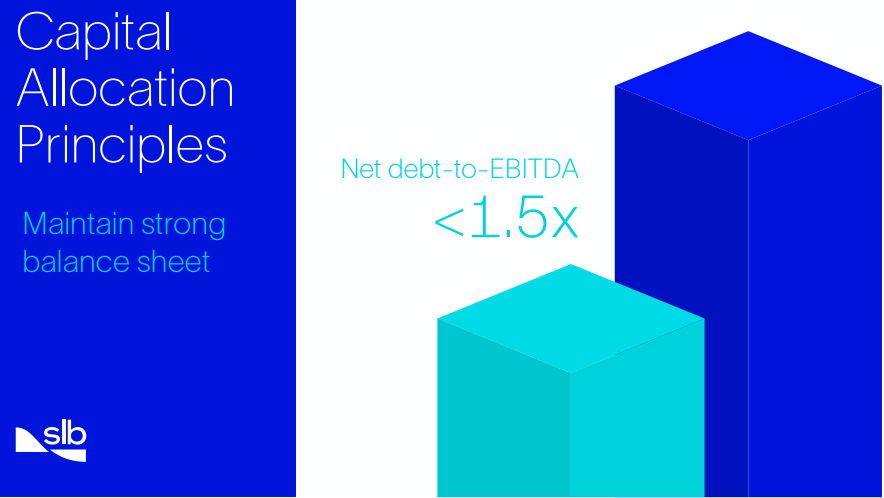

SLB’s balance sheet is already strong. And if my reasoning that oil prices should remain strong in 2023 proves to be accurate, there’s going to be a lot more demand for SLB’s services.

SLB investor day

This will mean that SLB will be well-positioned to return capital to equity holders rather than creditors. And that’s precisely what SLB’s recent commentary alludes to.

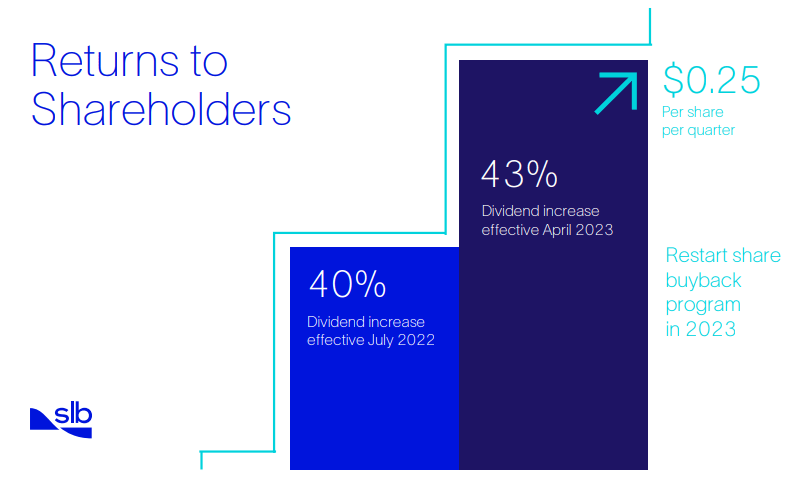

Indeed, SLB itself has stated that it will restart its share repurchase program.

Or better still, SLB believes that it can resume its share repurchase program while keeping its A credit rating from both S&P and Moody’s.

SLB Stock Valuation – 19x 2023 Free Cash Flow

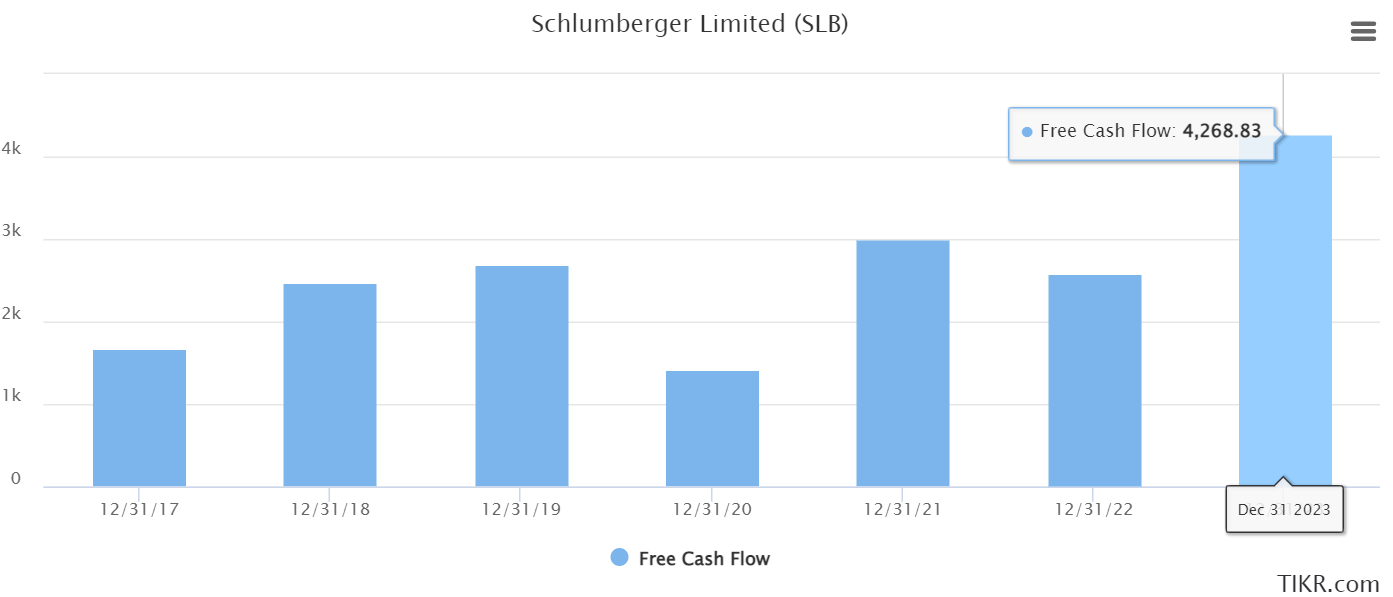

Moving on, analysts following SLB believe that it could make more than $4 billion of free cash flow in 2023.

TIKR.com

I’m not sure that SLB will quite reach this high free cash flow. But what’s more important to note here is the view that SLB’s free cash flows in 2023 will be significantly higher than in 2022.

Furthermore, consider the objectives from SLB’s recent Investor Day.

SLB Investor Day

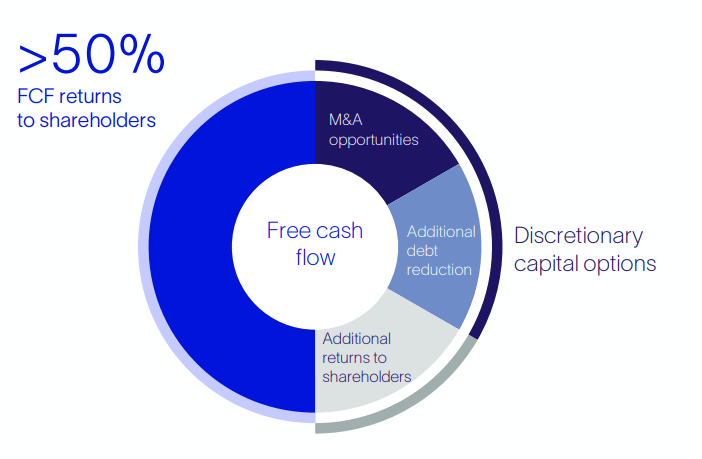

SLB believes that it can grow its top line by 15% CAGR into 2025, while its bottom line will grow even faster. And then, on top of that, SLB believes that of its strong free cash flows, more than 50% can be returned to shareholders via dividends and buybacks.

SLB Investor Day

After raising its dividend for 2023, SLB’s dividend yield stands at 1.8%. I’m not going to make the case that getting approximately 1.8% yield is all that interesting.

SLB Investor Day

What I can say is that getting close to $2 billion of free cash flow back, provides a 2.6% total yield, via buybacks and dividends, on top of benefitting from an increase in intrinsic value. It’s this multipronged return that is very compelling.

The Bottom Line

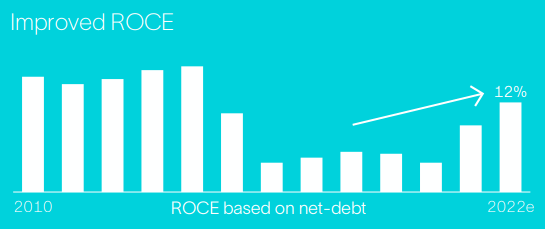

Investing in an oil services company is renowned for two characteristics: cyclicality, and asset-heavy ROE profiles.

On cyclicality, the stock is clearly not expensive at 19x free cash flow. What’s more, cyclicality in an upwards cycle is not negative. Particularly if the starting point is a valuation that most investors would agree is attractive.

And this brings me to my second characteristic, that of investing in an asset-heavy company.

SLB Investor Day

Asset-heavy companies typically have low-single-digit ROEs (or ROCEs). What the graphic above shows is quite the opposite. SLB is expected to exit 2022 with +10% ROCE and I suspect that 2023 will mostly bring more of the same, or even better for SLB.

In sum, I’ve been upfront with both the bearish and bull arguments facing SLB. I’ve made the case that SLB’s balance sheet is stronger, allowing for shareholder returns to take place in 2023.

And that its valuation is still very compelling, even though it’s already been widely reported that there’s a strong upswing in the demand for oil services.

Be the first to comment