filo/iStock Unreleased via Getty Images

SkyWest Airlines (NASDAQ:SKYW) has been on my watchlist for a while. When the stock was at $40, I thought it was not cheap enough and bought its largest public competitor Mesa Airlines (MESA) instead, despite SKYW’s significant competitive advantages over MESA. Today, SKYW is finally as cheap as MESA a year ago. Is it finally time to buy?

Thesis

As the largest regional airline, SKYW enjoys multiple competitive advantages such as long remaining contract terms, a diversified customer base, better cost control, and a more flexible business model, etc. However, the headwinds are significant too: The airline industry as a whole is experiencing a serious pilot shortage which inflates operation expenses and compresses margins. Considering all the factors above, I believe SKYW is a hold that should be able to generate good long-term returns but has many short-term uncertainties.

Business

According to the latest 10-K, SKYW is a regional airline that offers scheduled passenger service to multiple destinations. All of SKYW’s flights are operated as United Express, Delta Connection, American Eagle or Alaska Airlines flights under code-share arrangements (“commercial agreements between airlines that, among other things, allow one airline to use another airline’s flight designator codes”). SKYW generally provides regional flying to the major airline partners under long-term, fixed-fee, code-share agreements. Under these fixed-fee agreements, SKYW are paid fixed rates for operating the aircraft primarily based on the number of completed flights, flight time and the number of aircraft under contract. The major airlines reimburse SKYW for specified operating expenses such as fuel expenses.

Compared to its competitors such as MESA, SKYW has the following advantages:

- Scale: a larger scale allows SKYW to generate better margins, have more bargaining power, and maintain a more stable customer relationship. For example, according to MESA’s last 10-Q, American Airlines (AAL) terminated its Capacity Purchase Agreement (CPA) with MESA in 3Q22 since American didn’t want to take on MESA’s inflated cost to maintain its crew. In comparison, SKYW managed to add more fleets to American’s CPA. SKYW also gets better engine and aircraft maintenance deals due to its large scale.

- Diversified customer base and longer contract duration: One of the reasons I lost money in MESA is that I didn’t notice that MESA’s CPA with American will expire soon. The renewal didn’t go well: MESA had to cut many planes from the CPA and the revenues dropped significantly since the idled planes can’t generate revenue but MESA still need to pay them off.

- Dual Class: According to the 3Q22 earnings call, 80% of SKYW’s block hours are flown utilizing its dual class fleet.

- Flexible business models: SKYW has both the CPA model and the Prorate model (in which SKYW receives all of the passenger fare but also bears all the related costs). SKYW also has a leasing business which allows it to better utilize its spared fleets. The leasing business has been generating most of the profits since the pandemic hit.

- Stock scarcity: SKYW is one of the few public regional airlines so it would become the only option for regional airline play if the industry was to recover. MESA will not become a good option since it virtually only has one customer.

Headwinds

Despite having significant competitive advantages over its peers, SKYW is facing significant headwinds along with the industry. The most significant one is the shortage of pilots and crew members. MESA’s completion rate dropped from 99.99% to 80s% due to this issue, per its last 10-Q. This situation is more unfavorable to regional airlines since the major airlines compete with them to recruit new pilots. The crew shortage forces airlines to cut block hours therefore directly impacting their profitability.

Despite these headwinds, SKYW has maintained an outstanding performance record. For example, SKYW has accomplished a 99.99% completion rate and has been a Top 3 On-time Performer on DOJ’s list for several months of the year, per 3Q22 earnings call.

Why did the stock plunge?

SKYW’s stock dropped primarily because of the management’s pessimistic guidance. In 3Q22 earnings call, the management said “We expect total 2023 earnings to be down significantly from 2022, but remain modestly profitable as we continue to put the pieces together for a successful 2024 and beyond.”

They also predicted that 2023 block hours will drop by 20%. However, when an analyst asked if this block hour level will continue for years, the management said that there are many opportunities to increase the block hour level in 2024. The earnings depression is primarily caused by the pilot shortage, and SKYW has a large number of pilots in training right now, so I tend to believe the earnings level will come back in 2024.

Per 3Q22 earnings call:

when you don’t hire pilots until 2021 and it roughly takes two years to get a lot of your FOs into an upgradable captain scenario, that’s when it starts to – given various levels of attrition, that’s when it starts to turn around in 2023 organically.

Financials

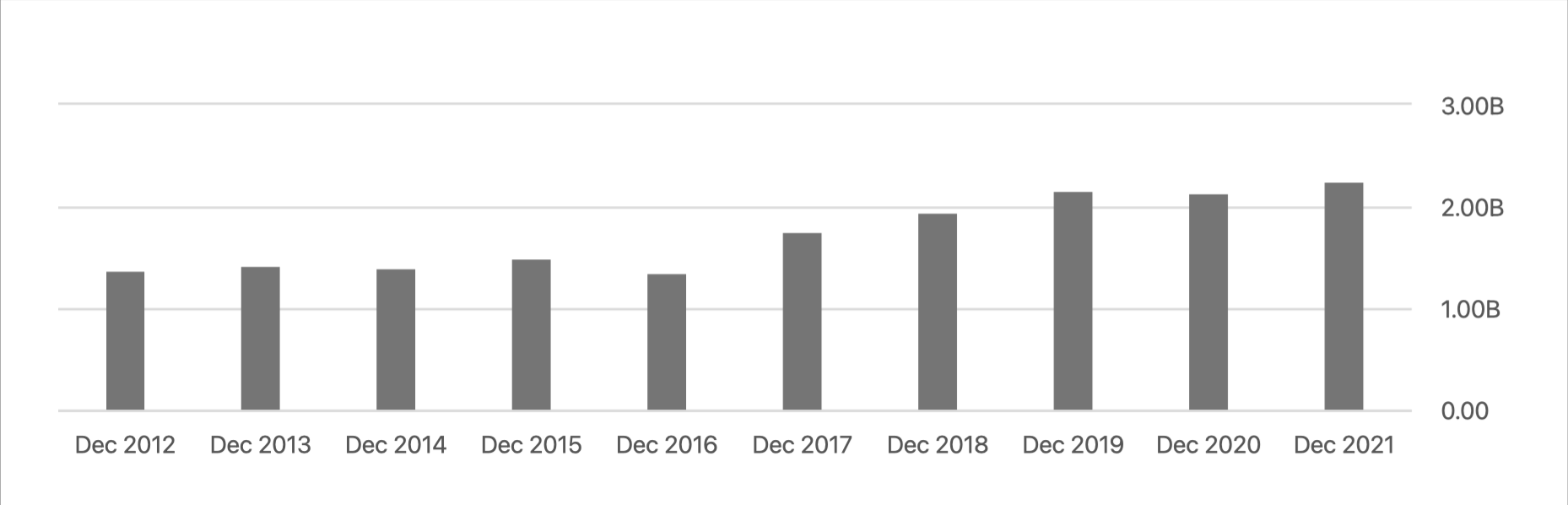

SKYW shareholders’ equity chart (Seeking Alpha)

As we can see from the chart above, SKYW’s equity has reached a historical high while its stock price has hit a multi-year low. The majority of SKYW’s equity is in its aircraft, which is relatively stable. As of the last 10-Q SKYW has ~$5.5 billion worth of PPE against ~$2.5 billion of debts.

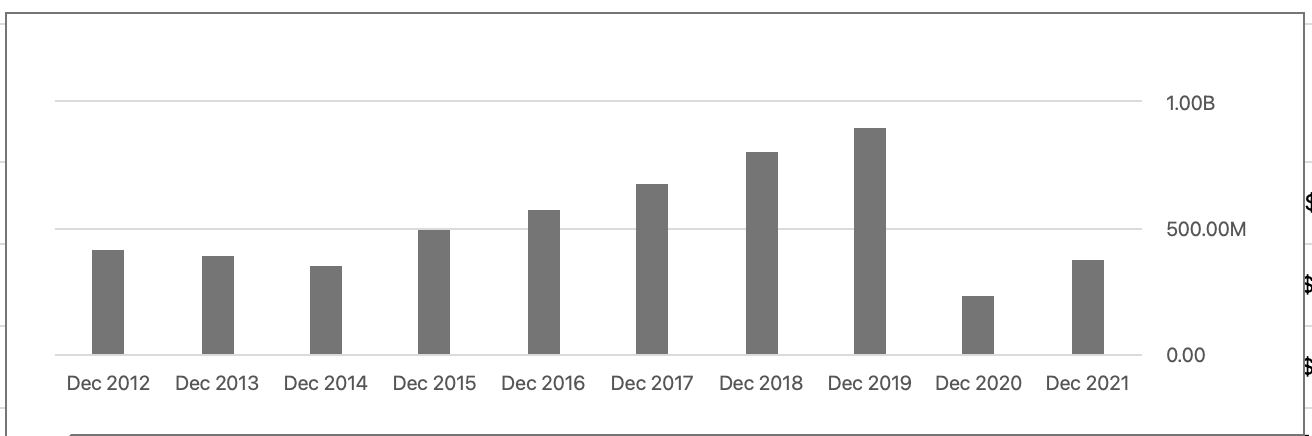

SKYW EBITDA chart (Seeking Alpha)

As we can see from the chart above, SKYW is trading at less than 3x EV/2019 EBITDA. While it’s impossible for SKYW to reach the 2019 profitability level in 2023 given the headwinds mentioned above, the stock can definitely generate rich returns if SKYW was to turn around.

A factor that potentially obscured the true economics of the past few quarters would be the $110 million worth of deferred revenue from last year, due to significantly lower block hours flown. On average, ~$13 million of deferred revenues from 2021 were recognized in each of the past 3 quarters of this year, which artificially inflated the gross margins by about 2%.

Conclusion

As the largest player in the market, SKYW has significant competitive advantages against its peers, which can be proven by the large bottom-line growth during the past decade. However, the challenges that SKYW is facing today will certainly create earnings volatility. Although the stock is cheap on an EV/Book value and EV/2019 EBITDA basis, I recommend investors hold the stock for now and accumulate when signs of earnings recovery appear.

Be the first to comment