DNY59/E+ via Getty Images

Investment Thesis

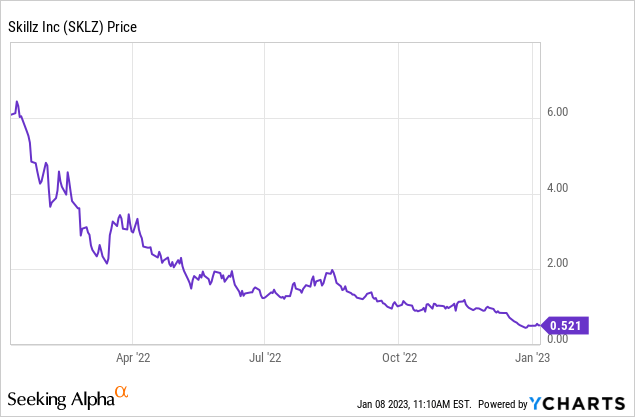

After its IPO in 2020, the mobile gaming company Skillz Inc. (NYSE:SKLZ) rapidly increased its share price, going from $10 to over $40. It was a major milestone when Skillz stock hit $40 in early 2021. As of 2022, it has plummeted by about 91% from its 2021 high.

I believe that the absurd SG&A costs are to blame for the company’s dire financial performance and, specifically, its inferior earnings, because of which its stock price has plunged.

The current momentum of -91.79% is lower than the industry average of -17.06%, and there have been five >100% downward earnings revisions for the company. These numbers demonstrate, both absolutely and relatively, how poorly the company is doing.

The administration is well aware of this dismal performance and has launched a profitability mission that includes, but is not limited to, a drastic decrease in the workforce. Even while these might assist in reducing overhead costs, I’m more encouraged by the company’s decision to put resources toward cloud gaming amidst rising demand in this sector as the gaming market is expected to grow. Despite these positive fundamentals, I remain pessimistic about the company’s near- and intermediate-term prospects due to its dire financial situation. The company is experiencing declining revenue growth, awful profitability, and negative cash flows. It has a plan to turn things around, but it will be a while before its vision comes true, thus I expect the company’s dismal financial records to endure for the foreseeable future.

Financials

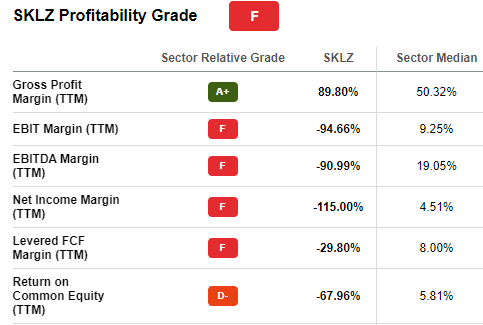

SKLZ’s financial situation is quite precarious from the top to the bottom line. To begin with, its revenues have a YoY growth rate of -2.07%. Although this revenue growth might result from the challenging financial environment, the resulting profit margins are unimaginable. The company has a gross profit margin of 89.80%, an EBIT margin of -94.66%, a net income margin of -115%, and a return on equity of -67.96%.

Seeking Alpha

Other than the gross profit margin, all of the company’s margins are abysmally low and far below the industry median, suggesting that this company is an underdog to its peers in terms of profitability.

The company’s negative cashflows are increasing, further worsening the company’s already precarious financial status. Based on its trailing twelve-month Levered free cash flow [FCF] of $-100.11M and cash flow from operations [CFO] of $-243.61M, cashflow seems to be a big problem.

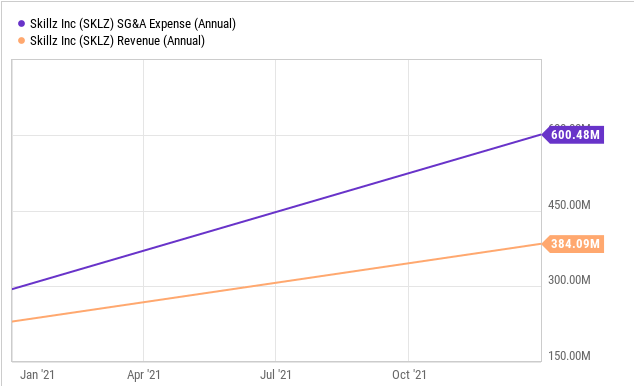

SKLZ’s extremely high SG&A expenses, which exceed its revenues by a substantial margin, are to blame for its dire financial state and, notably, its poor profitability.

YCharts

Eyeing Profitability

After experiencing poor profitability, management has made it a priority to turn things around. It has embraced fundamental pillars it hopes will help it recover.

“We are focused on four key pillars to enable us to return to durable growth and long-term profitability.”

-CEO Andrew Paradise (source)

The pillars include;

Pillar 1: Improving its platform to retain customers and developers

They’re reverting to thorough split testing and controlled product rollouts after 18 months of fruitless product modifications. Cloud gaming hits the mark. Their concept demonstrates they can give customers game-streaming technology that simulates native iOS and Android games. As they prepare for a full launch, they’re AB testing its onboarding experiences for new cloud gamers, among other initiatives geared towards improving its platform.

Pillar 2: Elevating the company to new heights

They laid off workers during the third quarter of 2022. They have reduced its workforce by about over half from where it was a year ago as a result of careful and intentional structural changes, which I assume were made to rein in SG&A expenses.

They returned to the office the same quarter. The carefully selected new hires know they must act quickly and effectively to address management’s concerns. To revive Skillz’s innovative culture, they’ve hired Vassily and other significant employees in Q3 2022. They are revamping the RT team and intend to make some crucial and compelling appointments in the next quarter. SL Advisers Portfolio Manager Henry Hoffman and gaming executive Seth Schorr joined the board. These seasoned operators and experts will help them make challenging company-building decisions.

Pillar 3: Go-to-market

They anticipate returning the six-month user acquisition payback period by decreasing end-user discounts that were not generating profitable growth, increasing organic traffic through owned communication channels, and being more granular with their UA spending.

Pillar 4: Showing a clear road to profit

This pillar summarizes the previous three; all expenditures are being scrutinized for their potential return, and this practice will be maintained to increase efficiency and productivity.

My Take On These Pillars

I think it’s vital that management has made a commitment to restoring profitability to the business and has developed a comprehensive strategy to do so. It’s about time management made a change, otherwise, the company could end up insolvent. With this in mind, my take on their plan to achieve is as follows;

- It’s encouraging that they’ve put so much effort into the platform to keep users and programmers. There are two ways in which I interpret this action. While platform enhancements will undoubtedly boost the user experience, the increased marketing expenditures required to spread the word about these cutting-edge platforms will stymie their efforts to become financially sustainable in the near and medium term. Second, I think the upgraded platform will boost MAU and income in the long run with the help of some positive press. In particular, I believe that the implementation of the cloud gaming endeavor will be a huge tailwind because of the increasing demand for the game around the world.

- While I do agree that cutting staff numbers could assist reduce SG&A costs, I have not yet come to terms with the rationale of reducing more than half of a company’s employees. Does that imply a far larger number of employees were hired than was necessary in the beginning? In that case, how will the remaining staff handle the pending tasks? Despite my satisfaction with the cautious hiring that appears to have followed the layoffs (and which is based on expertise and competence), I still don’t comprehend the motives behind the massive layoff. To add to that, the entrants who have been tasked with fixing the current crisis won’t be able to do so overnight. It will take time, in my opinion, regardless of how competent they are.

- The third and fourth pillars are both about making the best use of resources and being as efficient as possible. I’m very hopeful that they will help the company make the best use of its resources and get back to profitability. However, that won’t be achieved in the short run because they are dependent on the other pillars.

To sum up, the four pillars will drive the organization back to profitability, but not in the near future. Since I do not anticipate any positive changes in the immediate term, my present pessimistic outlook on the state of the finances remains unchanged, even though I do believe the plan will eventually bear fruit.

Growing Demand for Global Cloud Gaming

Revenue-wise, the global Cloud Gaming Market was worth USD 1,592.40 M in 2021, and it is projected to reach around USD 13,333.41M by 2028, expanding at a CAGR (compound annual growth rate) of approximately 42.50% between 2022 and 2028.

Cloud-based games are becoming more popular due to internet accessibility. 5G offers higher bandwidths and lower latency, making X.R. game streaming easy. Smartphone adoption may also enhance the worldwide cloud gaming business. Mobile gaming and digitalization are driving industry growth. Cloud gaming offers regular backups. It cuts gaming costs by eliminating the requirement for physical program copies.

By hosting games in the cloud, developers can cut down on storage needs, and players can get to their games faster. The widespread acceptance of cloud-based video games results from all of these factors. The growth of the Internet and the availability of instant-play games and those that don’t call for download or installation on almost any platform or OS, including Android, Linux, Mac, iOS, and Chrome O.S., are other contributing factors.

In my opinion, the firm’s dropping revenues, mostly due to declining MAUs, will improve if the company enhances its platform to better customer experience, which in turn, I believe, will help expand the number of MAUs, given the rising demand for cloud gaming.

Conclusion

Shares of SKLZ soared following the company’s initial public offering [IPO], peaking at about $40 per share in 2021. Since then, the company’s stock price has steadily declined, dropping by more than 91% in the past year. High SG&A costs are mostly blamed for the company’s lackluster financial performance. The corporation has devised a four-pillar plan to recover profitability, with the cloud gaming initiative, significant layoffs, and careful recruiting among the most noticeable courses of action.

The company’s financial situation won’t improve in the short or medium term, although these measures have a good initial look. While all of these actions will likely pay off in the end, it may be some time before the corporation can finally clean up the mess. In light of the company’s current situation, I recommend holding off until the company’s aspirations for profitability are realized.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment