Oat_Phawat

Investment Thesis

SilverCrest Metals Inc. (NYSE:SILV) yesterday after the close released the summary information of an updated technical report on Las Chispas, and earlier today hosted a conference call to discuss the report. The new report was released because the mining method has partly changed and inflation has made the 2021 feasibility study (“FS”) less relevant.

Figure 1 – Source: SilverCrest August 2023 Presentation

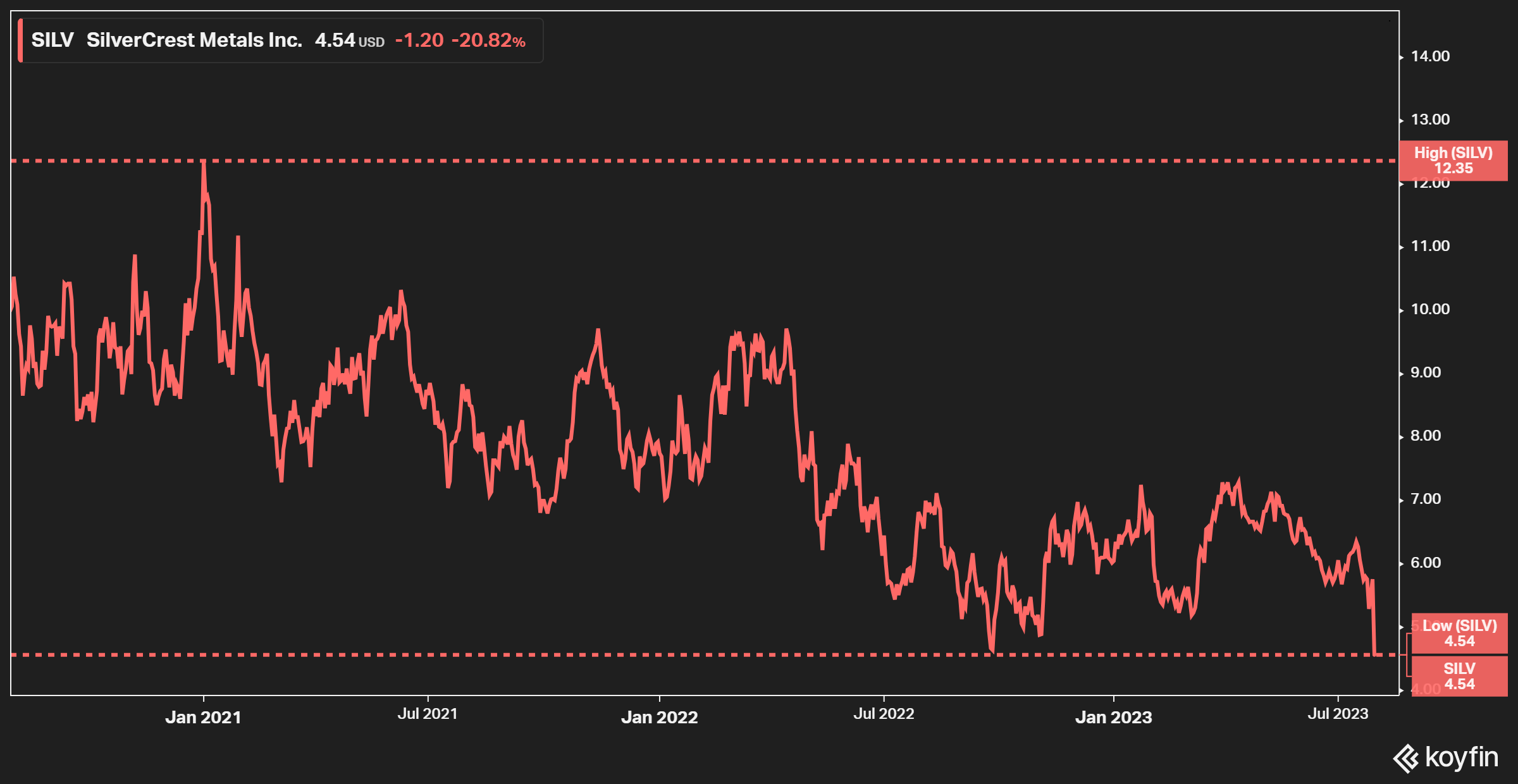

The 2023 report showed increasing costs and decreasing reserves, which caused the stock to sell off hard today. However, I would argue the selloff looks excessive, as at least the cost increases were well advertised in advance.

Figure 2 – Source: Koyfin

An investment in SilverCrest has always been dependent on the company bringing Las Chispas to production, which the company did on time and on budget, and then gradually growing the reserves over time. While decreasing reserves is not something I was expecting at this point, I am not overly concerned about the reserve life and feel confident the company will be able to extend the mine life going forward. A 20% stock price decline today looks like an opportunity, which has caused the stock to now trade at a 3-year low.

I have covered SilverCrest a few times before, and those articles can be found here. This article will primarily be about the updated technical report.

Updated Technical Report

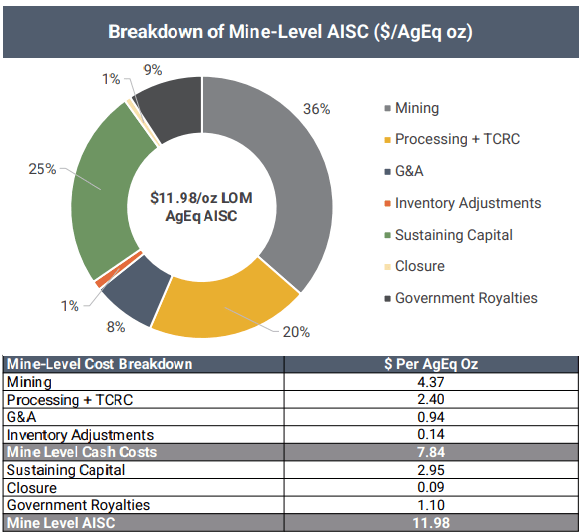

The updated technical data indicates a substantial increase in operating costs compared to the 2021 FS, which was expected given the inflation we have seen in the mining industry lately. The strong Mexican Peso was no doubt had an impact as well, as we look at cash costs and all-in sustaining costs (“AISC”) in U.S. Dollars per ounce.

Figure 3 – Source: Koyfin

Mine level cash cost is now estimated at $7.84/oz, and AISC is estimated at $11.98/oz for the life of the mine. AISC will, however, be slightly higher in the $13-14/oz range the next few years, due to more sustaining capital investments during this period.

Management has in the prior conference calls guided for costs in this range, so I don’t think these figures should be much of a surprise. It is important to remember that Las Chispas does still, after the updated estimates, have costs in the lowest quartile of the industry. Also, the margin for error in these estimated costs is likely very small as we have already seen the company deliver extremely cost-competitive production in the most recent quarters.

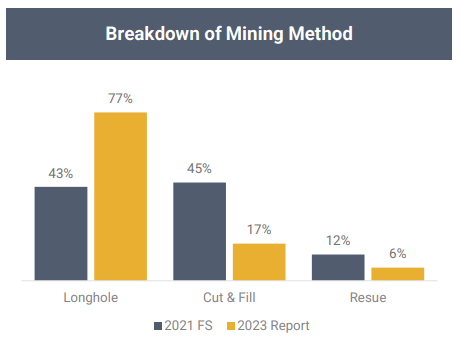

Figure 4 – Source: SilverCrest August 2023 Presentation

The new technical report did also indicate an annual production of 10M silver equivalent ounces per year, for a mine life of 8 years. Where about half of production comes from silver and the other half from gold.

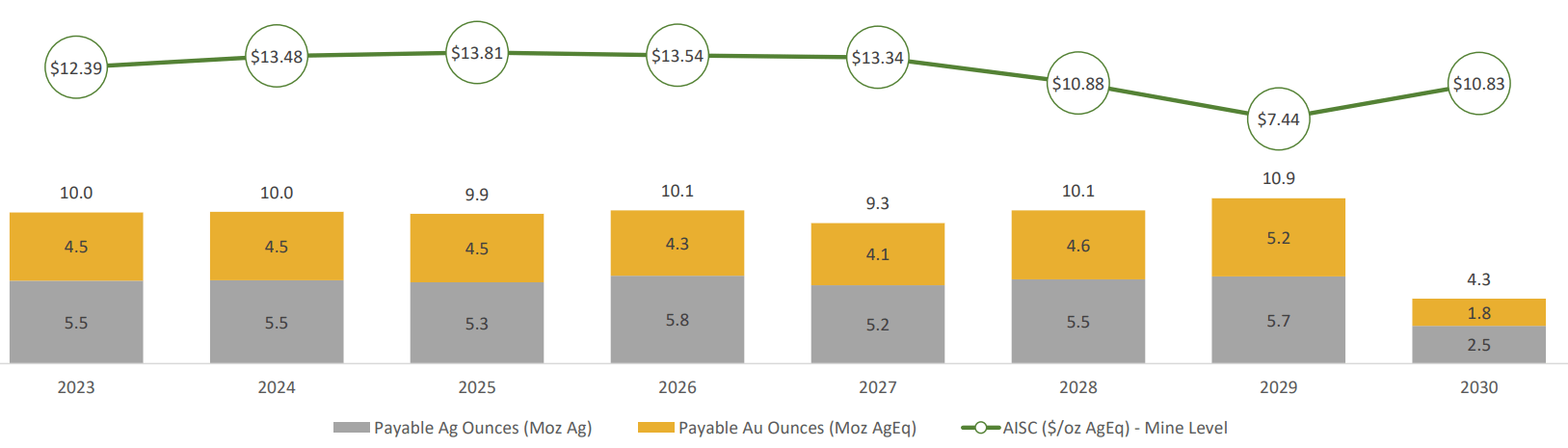

Reserves decreased by 13% compared to the 2021 FS, which is likely what the market disliked the most about this report. This was due to a combination of factors, where “narrower and more widely dispersed veins than originally modelled” does not instill confidence. However, it was also due to an increased cut-off because of higher costs, a change in the mining method, and a lower gold to silver ratio also had some impact. So, it is hard to be too critical about this change in reserves, as some of it is beyond management’s control.

Figure 5 – Source: SilverCrest August 2023 Presentation

One positive development was that the recoveries have increased to 98.0% and 97.0% for gold and silver from 97.6% and 94.3% gold and silver in the 2021 FS.

Valuation

SilverCrest Metals Inc. has a share price of $4.54 at the time of this writing, 153.3M fully diluted number of shares as of the Q1-23 MDA, $53M in cash as of Q2 that was indicated in the August presentation, and no debt. The company is currently trading with a market cap of $668M and an enterprise value of $615M.

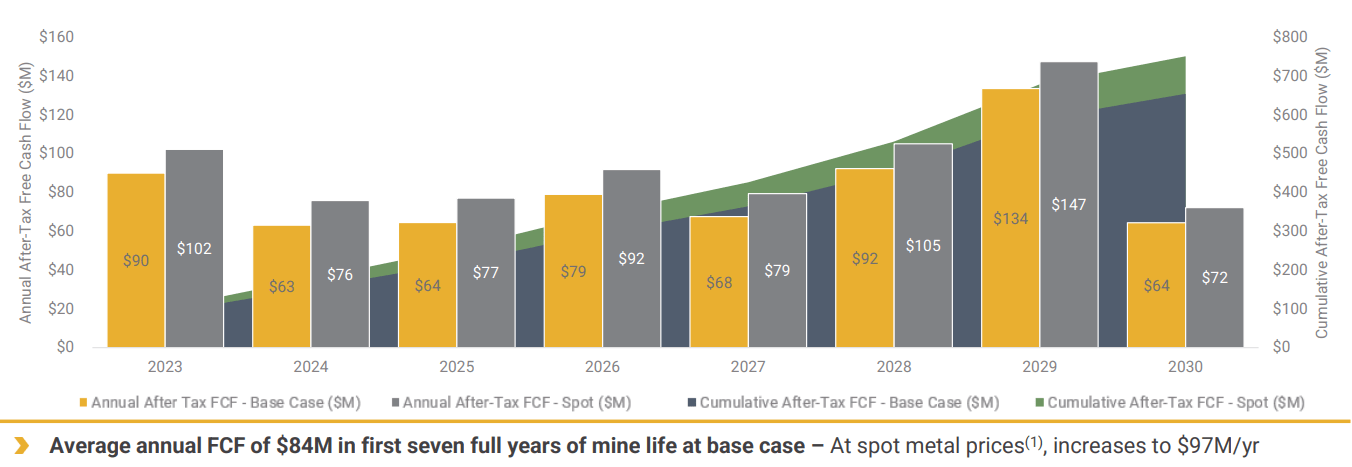

That is about equivalent to net asset value using spot prices according to the company. However, the cash flow yield is a very attractive around 12%, using the company’s spot price estimate below, where I have assumed another $20M per year in non-mine site G&A and other expenses.

Figure 6 – Source: SilverCrest August 2023 Presentation

Conclusion

Overall, I continue to think SilverCrest Metals Inc. stock is a good investment, despite a somewhat disappointing decrease in reserves. Part of it was due to modelling errors, but other market factors also played a part. So, I continue to have trust is the management team.

Just as the management team brought Las Chispas into production on time and on budget, have repaid all the debt in 9 months of commercial production. I feel confident the company will see reserves grow over time. I consequently choose to focus more on the attractive free cash flow yield, than the current net asset value and assume no reserve growth.

There is little doubt the political risk in Mexican has increased lately, but I would argue that applies much more to exploration and development companies than established producers like SilverCrest. The company is already paying royalties, and will from 2024 be paying rather substantial income taxes in Mexico due to the highly profitable operation, which is at least an incentive for a less heavy-handed government.

Be the first to comment