Micha Pawlitzki/Corbis Documentary via Getty Images

Investment Thesis

Microsoft Corporation (NASDAQ:MSFT) is undoubtedly one of the best companies in the world, led by a super management team.

In light of this notion, I’d like to focus on two contradictory ideas, quality and price.

Firstly, we’ll talk about Microsoft as one of the highest-quality businesses around. Even though Microsoft is no longer a monopoly, it nevertheless retains huge dominance at the IT enterprise level. Moreover, few large enterprises operate without going through Microsoft’s toll bridge in some way.

What’s more, Microsoft is in a fantastic position to take part in the digital economy. Microsoft can be viewed as a tool in the digital economy.

Every facet of data passes through Microsoft in some way, from routine office productivity to home gaming, from developers needing tools to produce and analyze data to companies wanting safe access to cloud storage.

And the next wave? The new era of AI. This will be the new concept to get investors excited about Microsoft.

Secondly, we’ll talk about that pesky detail, price.

The Only Question That Matters is Not Will AI be Enough to Move the Need

Let’s face it; I think we can now all agree that the previous two years were marked by a bull market. Most businesses benefited from this to some extent. But it was especially advantageous for businesses that gave us the freedom to embrace the digital economy.

We were all led to believe — and we did believe — as investors that the good days would continue. The management team wanted to believe in the cherished tales they told us and one another.

As a result, not only did Microsoft over-earn, but it also over-invested in its infrastructure and staffing.

Now that things are returning to a more normalized environment, there’s really only one question that investors have to form some sort of view upon. And that is not whether or not AI will be the next wave of the future.

What kind of multiple makes sense for a company with low teen revenue growth rates, to put it more pragmatically?

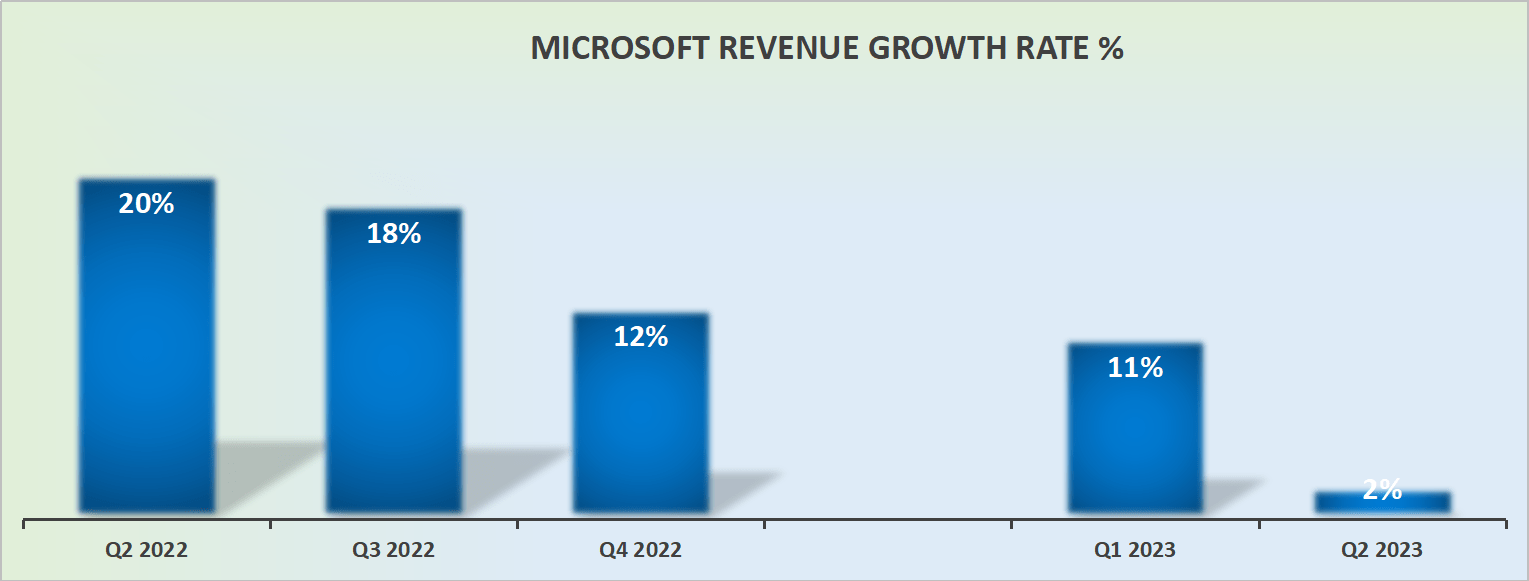

Fact: MSFT Revenue Growth Rates Fizzling Out

MSFT revenue growth rates

The graphic above uses GAAP revenue figures. This means that FX headwinds are included in the above figures.

For fiscal Q2 2023, excluding FX, Microsoft’s revenue growth rates were up 7% y/y.

As you’d expect given all the recent news about ChatGPT, Microsoft wants to shift its narrative beyond Cloud, and focus investors on the next wave of growth, namely AI.

Yes, Azure sizzled in Q2 2022 and was up 38% y/y (adjusted for FX). But this strong unit wasn’t strong enough to move Microsoft’s Intelligent Cloud beyond up 24%.

Meanwhile, Microsoft’s More Personal Computing was down 16% y/y (adjusted for FX).

Thus, we once again face the unavoidable and unpleasant question, what multiple makes sense?

MSFT Stock Valuation — 25x Forward EPS

One part of me knows Microsoft’s investment thesis very well. This is a very high-quality compounder. Or better said, this compounder is of the highest caliber. And the definition of a compounder is a stock that you never sell. Where the best holding period is forever.

Another part of me, the pesky investor within, wonders, does it make sense to pay 25 times forward EPS for a company like Microsoft that isn’t going to experience mid-teens CAGR EPS anytime soon. With interest rates at 4%, that’s the same as Microsoft at 25x forward earnings. The only difference is that interest rates are guaranteed.

The Bottom Line

At the time of writing, Microsoft Corporation’s Q2 results have been welcomed by investors, with the stock jumping more than 4% after hours.

After the dust has settled, I have to wonder how much emphasis investors will place on Microsoft’s vision for AI and the new era of future growth versus how much they will take into account that most of its upside potential is already priced into the stock.

Be the first to comment