pepifoto/E+ via Getty Images

This year, Silgan Holdings (NYSE:SLGN) is set to reach 20 consecutive years of dividend growth. Not only has the company grown the dividend, but it has grown rapidly, growing the payment by over 10% annually in the past ten years. Better yet, the growth rate is accelerating with a 5-year growth rate of 12%, and the last two increases have been over 14%. Many investors have never heard of Silgan Holdings for two reasons: Firstly, it is a small cap at less than $6B, and secondly, it is incredibly dull.

Silgan Holdings is one of those companies that operates in the background. Their products are everywhere, but we take them for granted and never buy them directly. They provide the packaging that everyday products come in, from canned food to beauty products. While we rarely think about packaging, it is a profitable business.

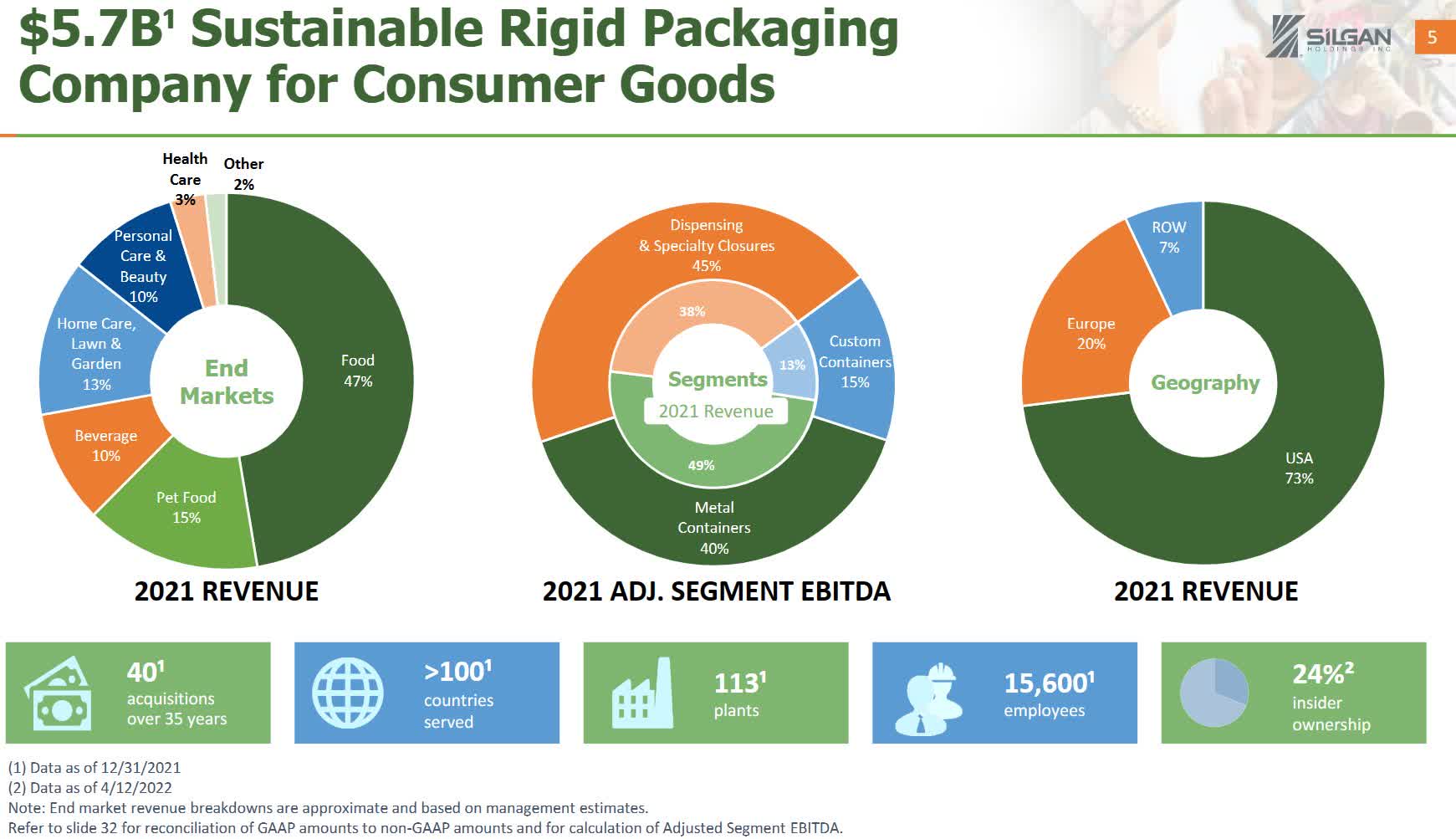

Silgan operates in three segments, Dispensing and Specialty Closures, Metal Containers, and Custom Containers. The diversity of products allows them to serve a wide swath of clients. The company slide below displays some information on the segments and customers.

Investor Slide Show – silganholdings.com

Growth Through Acquisitions

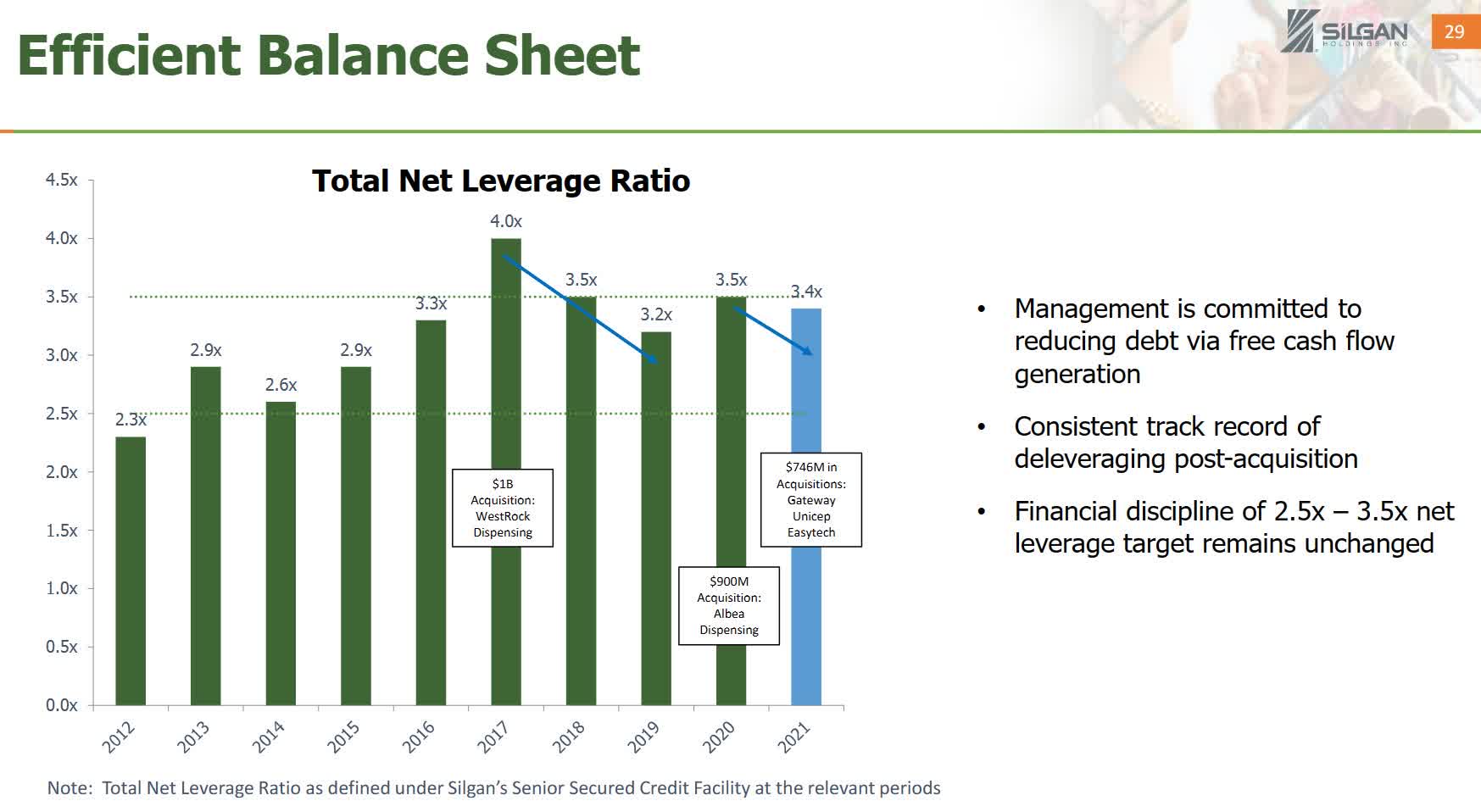

The packaging business is relatively unconsolidated. This means that potential smaller acquisitions are readily available without making a large bet on an outsized purchase.

Many companies make promises of significant shareholder returns on acquisitions, but few do it well. Silgan is one of the few companies that makes regular acquisitions, manages to integrate them, and takes a disciplined approach to paying down debt. This is illustrated in the slide below from the investor deck.

Investor Slide Show – silganholdings.com

Sustainability

There is no doubt that both companies and consumers today are more aware of the packaging surrounding their products. Of course, metal containers are infinitely recyclable, but their smaller custom container segment is growing due to this trend. In fact, they tout that 99% of the custom containers are recyclable and can produce products from 100% recycled plastic.

As consumers and companies emphasize sustainable packaging, the custom container segment will continue to grow. Of course, plastics are a concern to everyone. Given Silgan’s penchant for acquisitions, it is likely that should a viable alternative arrive, they would acquire the technology through a direct purchase or licensing.

Is the dividend sustainable?

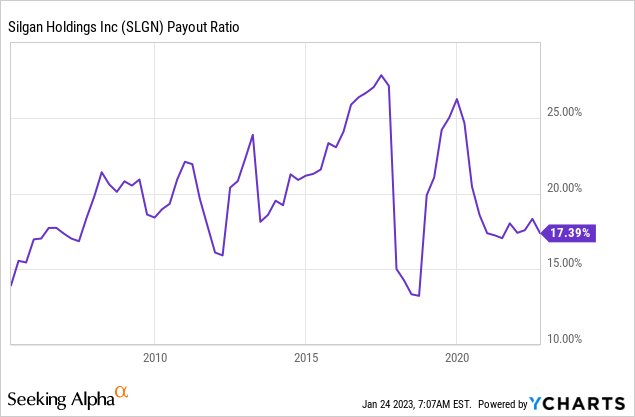

With any company that has rapidly grown the dividend, it’s essential to determine if the growth was due to the business growth or payout ratio growth.

The chart below shows the payout ratio over the past twenty years. It has consistently been around 20% but even lower in the past three years. Not only has the payout ratio been flat to shrinking, but the absolute payout ratio is very low. This indicates that the dividend is likely safe in any economic downturn.

In order to grow the dividend in the future, earnings also need to increase. The current estimates indicate only 6-7% annual growth in EPS over the next five years. There is currently a share buyback authorized which equates to about 5% of the company that will add to the EPS. Additionally, it is impossible to account for any acquisitions that the company may have in its sights. However, at this moment, the dividend growth might need to slow unless the payout ratio is expanded.

Valuation on Dividends

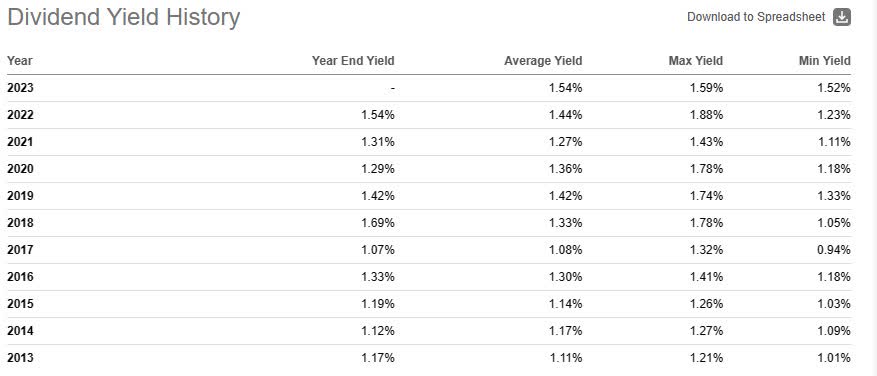

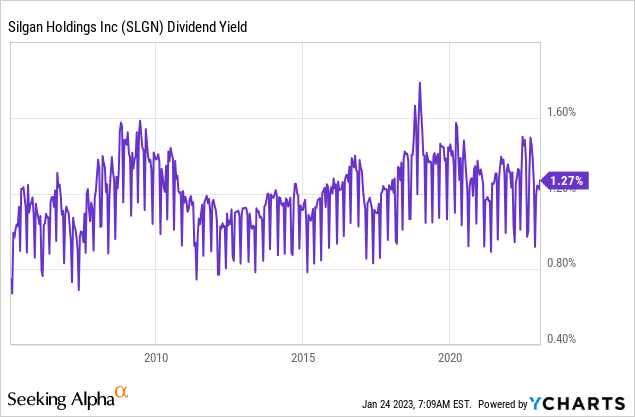

The current dividend yield is only around 1.25%. This is the average yield over the last ten years. The highest yield over the previous ten years was just last year when it reached nearly 1.9%. The table below shows the dividend data over this period.

Seeking Alpha

When the data is expanded to look at the entire 20 years of dividend growth, it can be seen that the company rarely exceeds a yield of 1.6%, and the 1.25% remains an average historical yield. This is shown in the chart below.

Today, based on dividend yield, the company is not a buy. It could be considered a buy at a yield of 1.6% or a price of $40.

Valuation on P/E

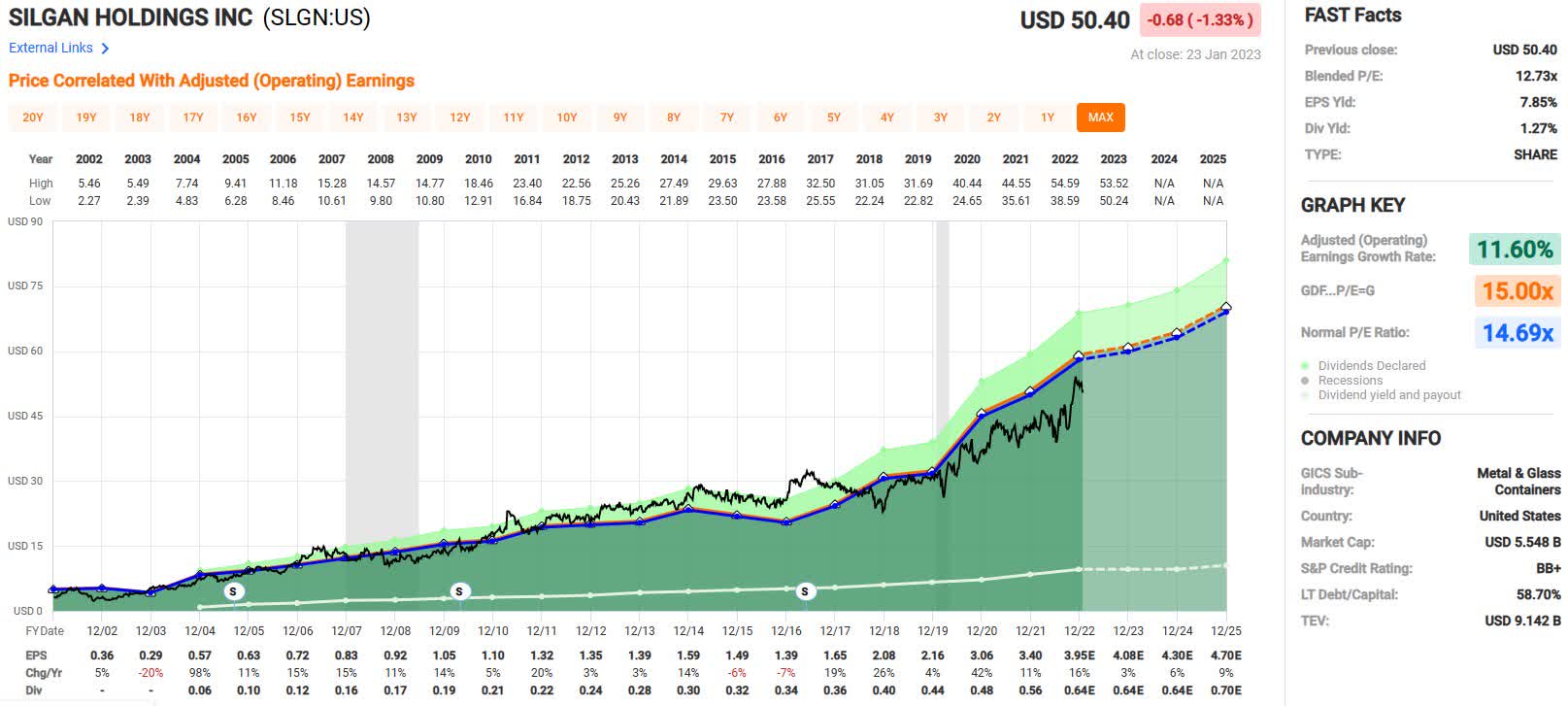

Using the Fastgraph below, we can see that today’s P/E of just under 13 is below the 20-year normal P/E for SLGN of just under 15. This indicates that the company may be a slight bargain. The company would need to rise in price to $58 to reach the average P/E.

fastgraphs.com

However, a consideration is that since 2018, the company has had an average P/E ratio of about 13, right where it is trading today. Additionally, over the past five years, the company has regularly hit P/Es of under 12. This doesn’t necessarily mean that this is a new normal; companies come in and out of favor, but they usually revert to a historical norm eventually. Based on the totality, SLGN appears to be fairly valued at this time.

Conclusion

As a product container company, Silgan Holdings is well-positioned for the future. The continued trend of “shrinkflation” only requires more packaging, as well as our ever-growing demand for more products. The company’s commitment to sustainability and successful integration of acquisitions are also positive forward trends.

While there may be a short-term risk from a recession, the company didn’t see a downturn during the 2008-2009 recession. In fact, EPS has been strong over the past 20 years, with only a slight downturn in 2015-2016 and a down year in 2003. With the very low payout ratio, Silgan should easily continue growing the dividend through a recession in my view.

The company is fully valued today. I will consider opening a position below $40, which is close to the 10 P/E. With the likely upcoming dividend increase in February, I also expect that this price will put the yield close to 1.8%.

Be the first to comment