Klaus Vedfelt/DigitalVision via Getty Images

Sienna Senior Living (OTCPK:LWSCF) (TSX:SIA:CA) has a decently long history of operation. It has operated for about half a century.

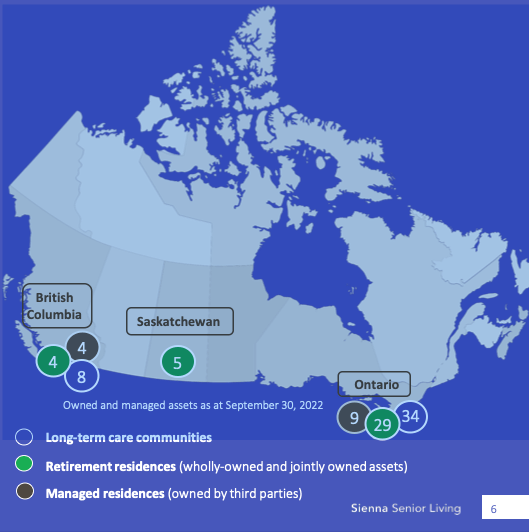

It owns and operates seniors’ living residences in the Canadian provinces of British Columbia, Saskatchewan, and Ontario. Its portfolio consists of 42 long-term care (“LTC”) communities (with 6,632 beds), 38 retirement residences (including 4,389 suites), and 13 managed residences (with 1,461 beds or suites).

Investor Presentation Nov 2022

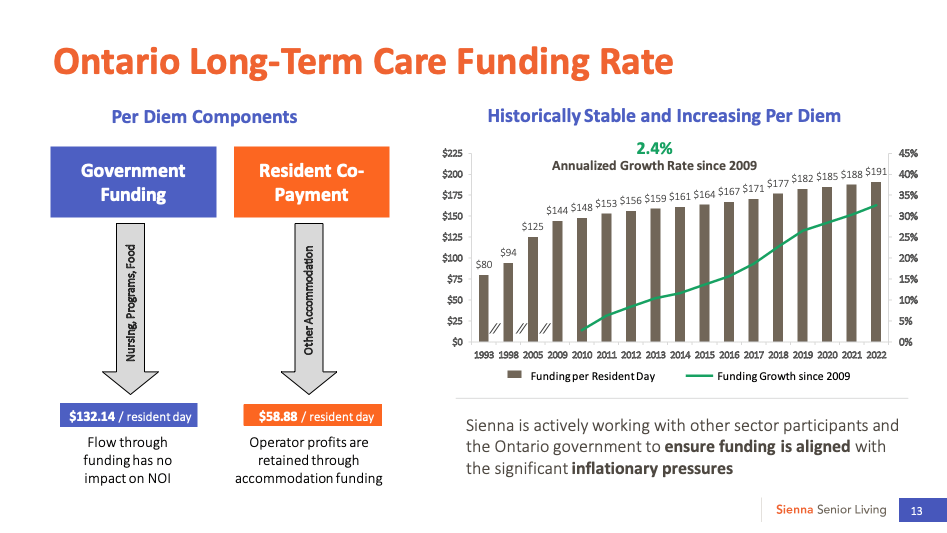

Sienna Senior Living’s revenue stream is relatively stable because of support from government funding for its LTC communities in British Columbia and Ontario.

For example, since 2009, its Ontario LTC government funding has historically increased at 2.4%, which is roughly the long-term inflation rate (unlike the high inflation rate that was experienced in 2022).

Investor Presentation Nov 2022

Its latest report indicated that in the first nine months of 2022, its average LTC occupancy (including private occupancy) was 88.4% (an improvement of 5.7%) and its same-property occupancy at its retirement portfolio was 86.5% (an improvement of 7.8% year over year (“YOY”)).

(The company reports in Canadian dollars, so the figures in this article are in CAD$ unless otherwise noted.)

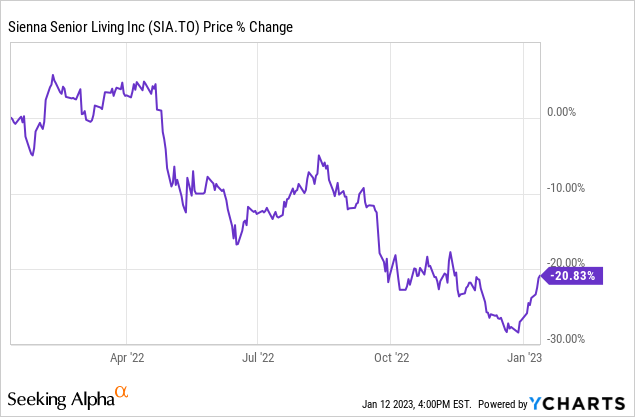

The stock seems to have been forgotten by the investing community as the last Seeking Alpha coverage on it was in late May 2019.

It’s understandable. The stock is down about 38% since then. And in the last 12 months, the stock is down 21%.

What’s Weighing on the Stock?

In the first nine months of 2022, Sienna reported adjusted revenue growth of 10.0% to $543.6 million. However, net adjusted operating expenses rose 14.7% to $442.2 million.

It’s not at all surprising that operating expenses rose faster than revenue because of higher inflation such as from labor costs, utilities, insurance, and higher unfunded pandemic expenses. Rising interest rates are another factor weighing on the stock.

Its same-property net operating income (“NOI”) fell 7.2% to $97.6 million, while total NOI fell 6.7% to $101.4 million.

Its retirement portfolio is holding up better than its LTC portfolio in terms of same-property NOI. Its Q3 retirement occupancy of 88.6% recovered from the lowest rate of 78.4% during the pandemic in May 2021 and was higher than the pre-pandemic levels of about 85%.

In the first nine months of 2022, its retirement portfolio’s same-property NOI increased by 14.1%, but its LTC portfolio’s declined 19.4%.

The EBITDA, a cash flow proxy, rose 16.5% to $99.0 million. The operating funds from operations (“OFFO) dropped 12.5% to $51.4 million. On a per-share basis, OFFO dropped by 17.6% to $0.722, resulting in a payout ratio of 97.2%. The more stringent adjusted FFO payout ratio was 99.6%.

Higher Interest Rates

Generally, higher interest rates make Sienna stock a riskier investment. In the first nine months of 2022, its debt to gross book value improved by 2.3% to 43.3%. Its interest coverage ratio worsened from 3.8 to 3.3, which is still acceptable. As well, its debt service coverage ratio worsened from 2.2 to 1.8.

Its weighted average cost of debt increased from 3.4% at the end of Q3 2021 to 3.6% at the end of Q3 2022. Similarly, its debt to adjusted EBITDA ratio worsened from 7.8 to 9.0.

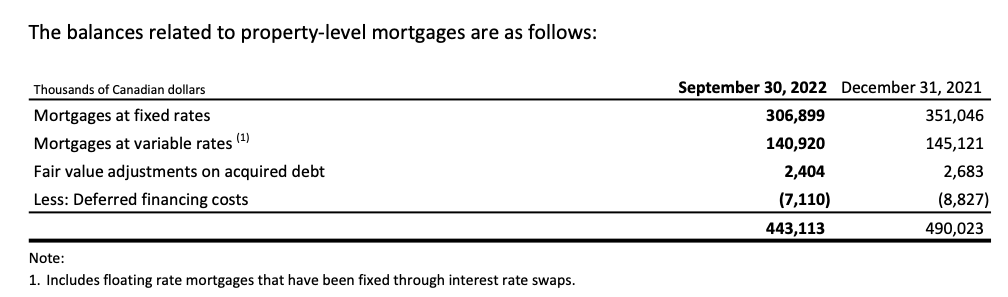

As the table below shows, Sienna’s mortgage debt portfolio has about 31% exposure to variable interest rates. It also enjoys low-cost mortgage financing from CMHC. As of the end of Q3, 54% of its property-level mortgages were insured by CMHC, which aligns with the same period in 2021.

Q3 2022 MD&A Q3 2022 MD&A

Sienna has debt maturities of $168.1 million in 2023 – about 46% in mortgages and 54% in an unsecured term loan.

The Dividend Appears Sustainable

Sienna yields just under 8.0%. Its high payout ratio gives it little room for error. So, there’s a slim chance it would reduce its dividend. That said, it has been managing its retirement portfolio well, and its LTC portfolio should have growing demand (see “The Turnaround Potential” section).

The company also has ample liquidity to cover its 2023 debt maturities and interest expense, with leftover for its dividend. As of the end of Q3, the company had liquidity of $259.4 million, including $50.9 million in cash and cash equivalents, and $208.5 million of available funds from credit facilities. It further boosted its liquidity to $350.9 million at Nov 9, 2022, while its annualized dividend payments total about $68.2 million.

Returns Potential

Longer term, Sienna should benefit from a growing aging population. Sienna highlighted in its November 2022 presentation that according to the 2021 census, the Canadian seniors’ population in the 85+ age group is projected to triple over the next 25 years. And one in four people who are 85+ years old is already living in a seniors’ living setting.

Yahoo Finance

The stock also gives a margin of safety from its valuation. After a correction in Sienna stock, it now trades with a discount of about 19% and a high yield of just below 8.0%. According to the analyst consensus 12-month price target of $14.50 the stock can appreciate almost 24% over the next 12 months. This implies near-term total returns potential of approximately 31.5%.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment