Sean Gallup

Investment Thesis

Shopify Inc. (NYSE:SHOP) is a leading ecommerce infrastructure provider, giving its customers the tools to help start, grow, market, and manage a retail business of any size. It is a founder-led company with a strong net cash position and has seen phenomenal growth since it came public in 2015.

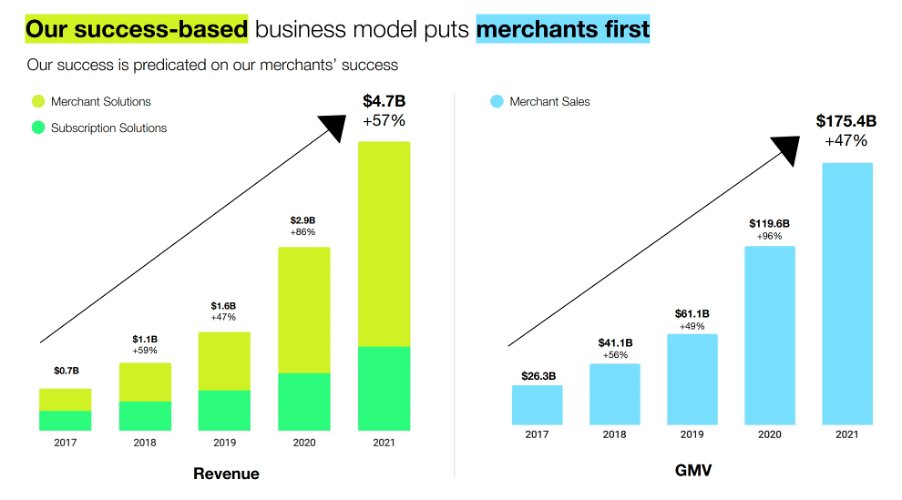

One of the most appealing aspects of Shopify, for me, is the split of its business model between the recurring, subscription-based revenues from its Subscription Solutions and the customer-aligned performance-based revenues from its Merchant Solutions. This enables the company to have a solid base of recurring revenues alongside Merchant Solutions that have the potential to grow quicker, as Shopify continues to roll out more and more solutions to its customers.

Shopify Q3’22 Investor Presentation

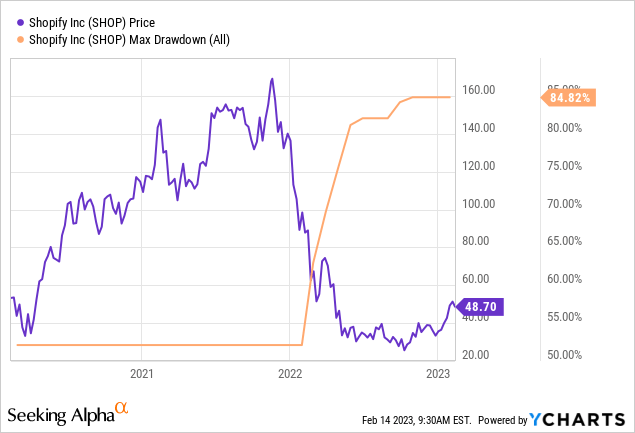

The past 18 months have been a rollercoaster for shareholders, with Shopify shares seeing drawdowns as large as 85% from their recent highs. There have also been bright spots for more recent shareholders, as Shopify stock has more than doubled since its recent October lows – which was around the time I decided to dismantle the bear thesis for Shopify in an article, sticking a ‘Strong Buy’ rating on the company.

But investing is a forward-looking game, and with Shopify set to report its Q4 earnings this week, investors will be looking to see whether Shopify can continue its recovery, or if it will be battered by the weak macroeconomic conditions.

Shopify’s Q4 Results Expectations

Shopify is set to report its Q4’22 results on Wednesday, February 15, after the market closes, and there are several key items that investors should keep their eyes on.

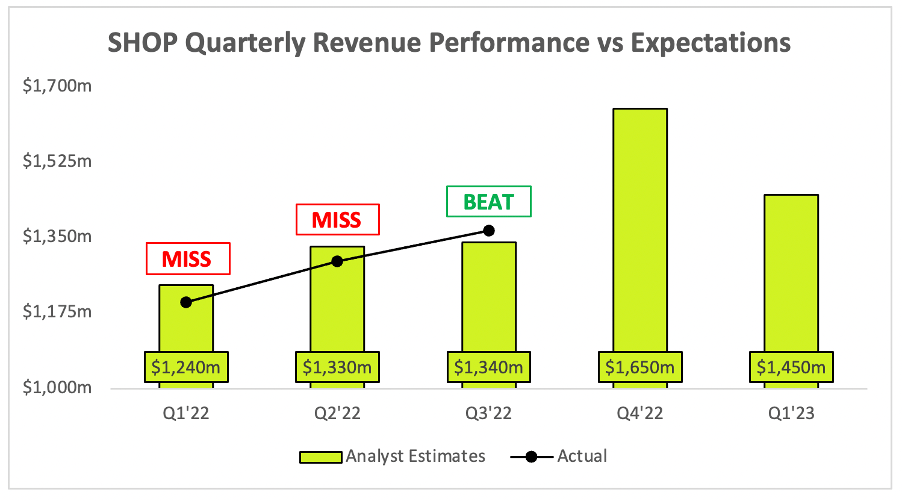

Starting with the headline numbers, where analysts are expecting Q4’22 revenue of $1,650m, representing YoY growth of 19.6%. It’s worth pointing out that Shopify’s management team doesn’t give precise forward guidance when it comes to quarterly results.

Author’s Work

Looking ahead to Q1’23, analysts are expecting Shopify to deliver revenue of $1,450m, which would represent 20.5% YoY growth. This is a pretty optimistic projection when you consider all the headwinds facing Shopify, such as the slowdown in ecommerce, the slowdown in the economy as a whole, the more severe impact of recessions on smaller businesses, and the strengthening dollar.

As mentioned, I don’t expect management to put an exact figure on their Q1 revenue expectations, but they may well outline some high-level details about revenue for 2023 – so it will be interesting to see if Co-founder/CEO Tobi Lütke and his team are feeling better about the next 12 months than the previous 12 months.

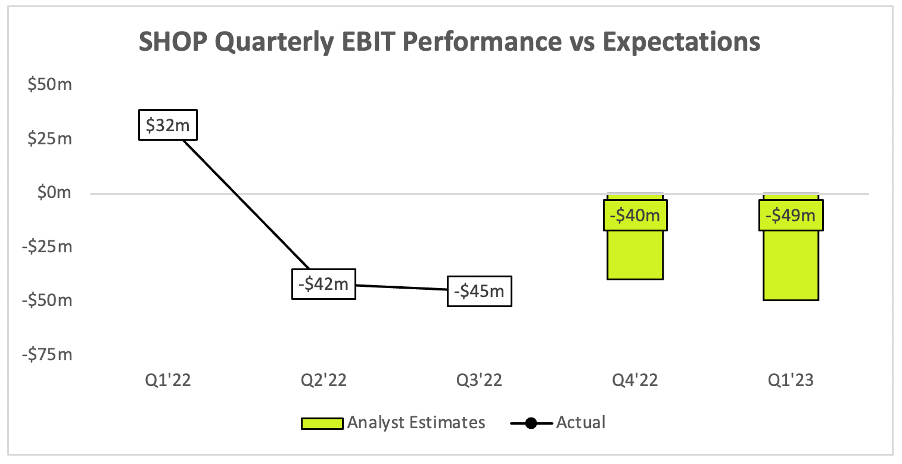

I’ve also decided to start tracking Shopify’s EBIT (Operating Profit) against analysts’ estimates, although I can’t access historical data… so this is what I’ve got so far – analysts are expecting Shopify to deliver Q4’22 EBIT of (-$40m). This represents an improvement from the last two quarters, but Shopify does tend to benefit from more operating leverage in the final quarter of the year thanks to holiday sales giving a boost to revenue.

Author’s Work

I’m tracking EBIT now because 1) I’ve found a useful tool to help (TIKR.com), and 2) the current market and the current economy are a lot more focused on profitability, and quite frankly Shopify should be focusing on profitability a bit more too. The time of growth-at-any-cost is over for now, and so it’s important that businesses like Shopify show that they can turn a profit and that they do benefit from operating leverage.

There are plenty of headline numbers for investors to watch, and I’m sure these will dictate any short-term share price movements after Shopify reports. But, aside from the obvious headline figures, what else should investors be looking out for?

The Biggest News Yet

In January, Shopify made what I believe to be one of the most substantial and business-changing announcements in a long time – and I think it will boost the company’s financials in a big way over the coming years.

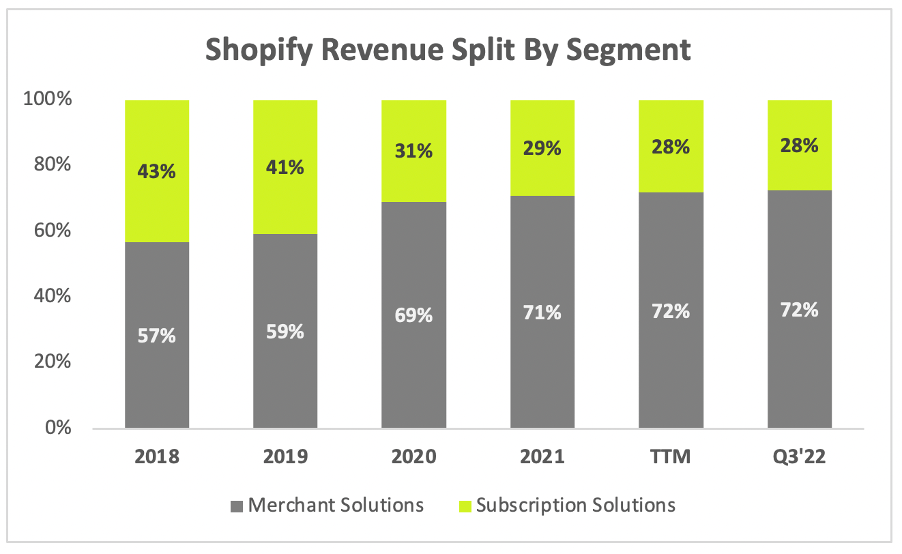

But a bit of background before we get into the announcement. Shopify has its two core segments: Merchant Solutions and Subscription Solutions. Over the past few years, more and more of Shopify’s revenue has been coming from the Merchant Solutions. This makes a lot of sense, and is great for shareholders, because it shows that Shopify’s land-and-expand business model is working.

Author’s Work

The Subscription Solutions are paid as a monthly or annual fee to give customers access to Shopify’s ecommerce platform, but the Merchant Solutions such as Shopify Payments, Shopify Capital, and Shopify Fulfilment are all add-ons that make the merchant’s life easier whilst boosting Shopify’s revenue.

Shopify Q3’22 Investor Presentation

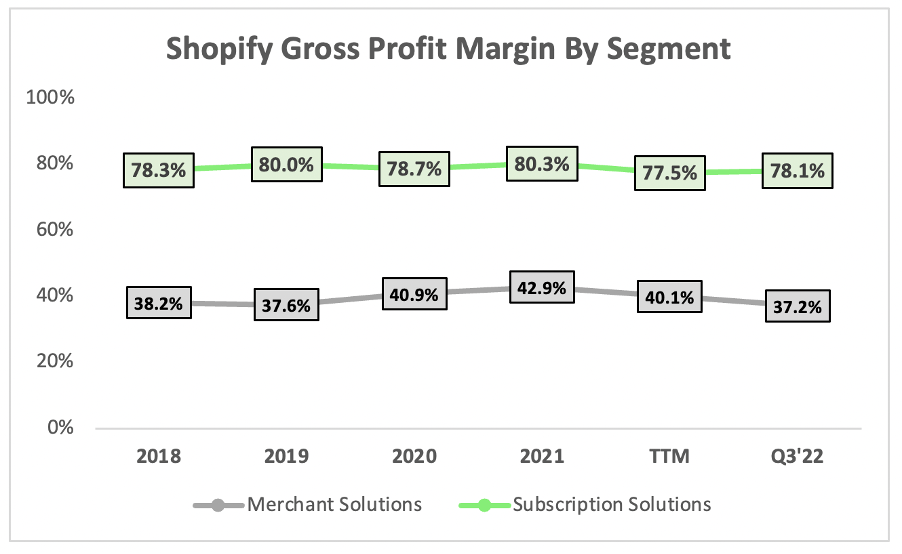

This is a part of the investment thesis, but there is a downside; the Merchant Solutions have a substantially lower gross profit margin than the Subscription Solutions. This makes sense, as there are many more costs that go into providing payment and fulfilment solutions compared to the costs of running a cloud platform (just look at any SaaS, PaaS, or IaaS margins).

Author’s Work

Now, the announcement, per Seeking Alpha:

Shopify stock drove to a double-digit gain on Wednesday after announcing major changes to pricing for sellers.

The Canadian e-commerce company slated 33% increases to plans across the board. The platform will now charge $39 for the basic plan, up from $29, $105 for its Shopify plan, up from $79, and $399 for the top-end plan, up from $299.

Shopify is bumping up the price for its Subscription Solutions considerably, increasing them by 33% across the board. I outlined in my detailed Shopify analysis article that I believe switching costs to be the ultimate moat for this business, and these price increases will be the first test of my assertion.

Considering Shopify is so well integrated into the businesses of its customers (see the ever-increasing Merchant Solution revenue), these customers will really not want to switch away.

Analysts are also not expecting too much churn, as Baird analyst Colin Sebastian commented:

We don’t think these prices warrant a change for the vast majority of merchants, given the time and effort required to shift platforms, and our view that Shopify’s platform, in many respects, offers superior e-commerce functionality at a reasonable price.

All things considered, I think this is a fantastic move from Shopify. The subscription costs are still fairly low, even after these increases, so I think virtually all businesses using Shopify will be able to absorb them – but they could provide a huge boost to Shopify’s top and bottom line.

It’s worth noting that these price changes won’t come into effect until Q2’23, so don’t go looking for a revenue or margin boost this quarter or next. Crucially, listen in to the call and see what management has to say about their full year revenue and margin outlook, as this decision could provide a massive boost.

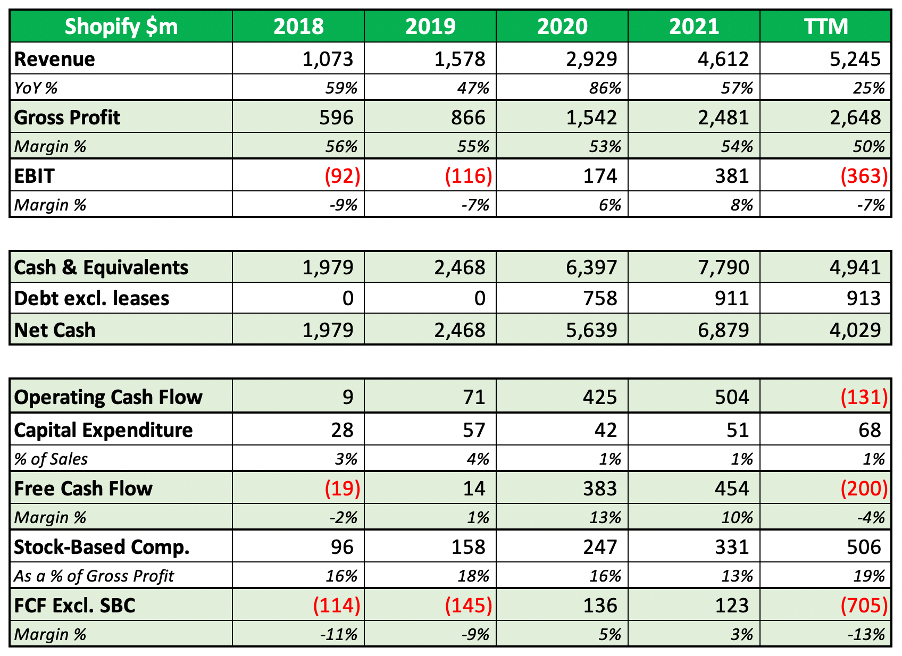

Quick Take: Shopify’s Financial Trends

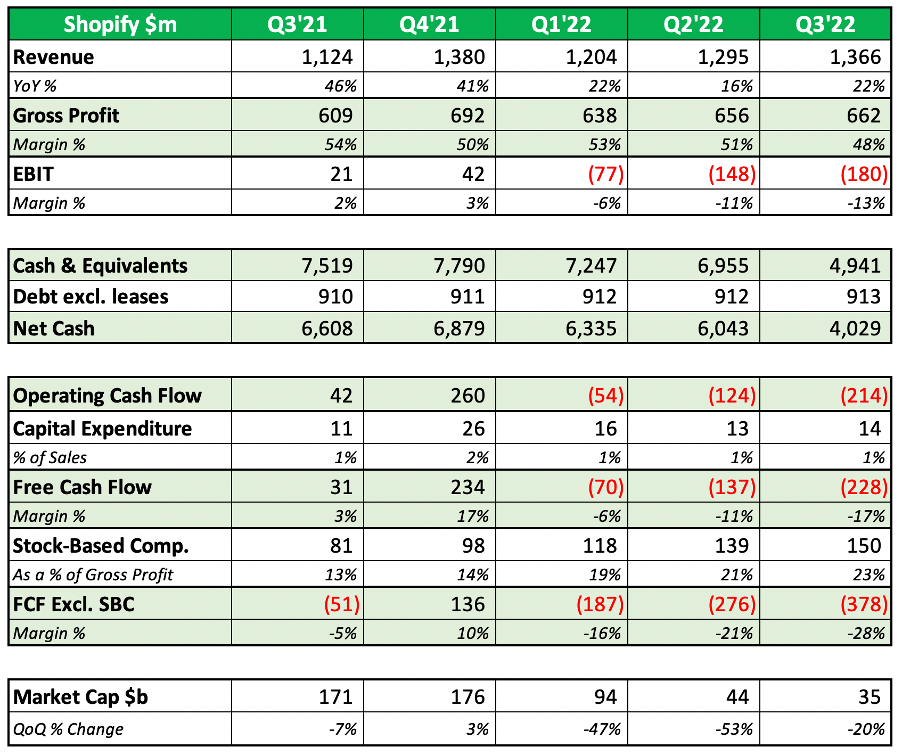

I also want to quickly touch on Shopify’s financial trends, although it really doesn’t paint a pretty picture.

I normally highlight various trends in green, orange, and red on the below charts to indicate items that are trending in the right or wrong direction, but I didn’t have to bother on the below – literally, everything would’ve been in the red.

Revenue growth down, gross margin down, EBIT margin down, cash position down, cash flows down, stock-based compensation up… it’s pretty darn awful.

Author’s Work

Obviously, there are plenty of reasons for these dreadful trends, and I think Shopify is going to start recovering, but it’s no surprise that shares have been whacked. I decided to also include the trend in Shopify’s market capitalisation alongside these financial results, which has unsurprisingly also been heading in the wrong direction.

The annual financials down below should paint more of a picture of Shopify’s last few years; a crazily impressive 2020 and 2021 thanks to multiple tailwinds, and a terrible twelve months thanks to multiple headwinds.

Author’s Work

Whilst I won’t talk in detail too much about these figures (the tables are included more for your reference), I do believe that 2023 will be a much better year for Shopify in terms of its financials. The company looks set to focus on balancing profitability with growth, and it also won’t be coming off the back of incredibly difficult YoY comps.

Let’s also not forget that >20% growth for an ecommerce company over the past twelve months is, in isolation, incredible. It’s just been such a slowdown that Shopify shares have been rightfully whacked.

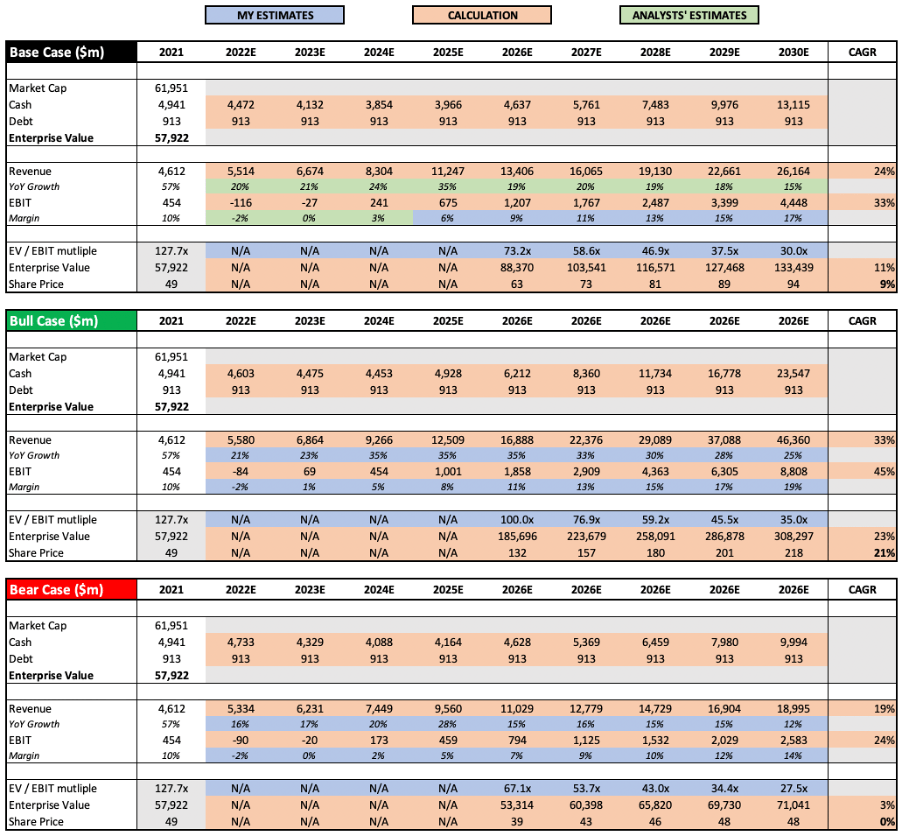

SHOP Stock Valuation

As with all high-growth, disruptive companies, valuation is tough. I believe that my approach will give me an idea about whether Shopify is insanely overvalued or undervalued, but valuation is the final thing I look at – the quality of the business itself is far more important in the long run.

Author’s Work

New year, new me, new valuation model; or at least slightly altered from my previous valuation model. I’ve decided to now use analysts’ revenue estimates from Seeking Alpha and EBIT margin forecasts from TIKR in my base case scenario, rather than my own estimates. I think it makes sense to use their estimates in my base case scenario and put my own views into the bull and bear case.

I’ve also expanded my model out into 2030 so that I can use EV/EBIT multiples that appear reasonable (rather than a 73x EV/EBIT multiple in 2026 that looks unrealistic in isolation).

My assumptions in both the bull and bear case scenarios, and the rationales behind them, remain pretty similar to my previous model. Essentially the bull case scenario assumes that Shopify executes successfully going forward, and operating leverage starts to kick in with certain solutions (such as fulfilment); the bear case scenario effectively assumes the opposite.

Put all this together, and I can see Shopify shares achieving a CAGR through to 2030 of 0%, 9%, and 21% in my respective bear, base, and bull case scenarios.

Bottom Line

The past two years should be a lesson to investors on the importance of valuation. No matter how brilliant a business is, and Shopify has undeniably been a brilliant business since its IPO, there has to be a point where the valuation takes precedence over the quality of the company – such as when Shopify was valued at $200 billion…

But since October, Shopify shares have been on a remarkable run, which has left the valuation looking quite stretched given the difficult macroeconomic environment. I am expecting great things from this company over the next decade, and I hope to see its Q4 results confirm the optimism I had after Q3 – that the trend for Shopify will start to be to the upside, following a tough year.

Given the risks that this business faces, combined with a share price that appears reasonable rather than enticing, I will be lowering my previous ‘Strong Buy’ rating to a ‘Buy’.

Be the first to comment