JHVEPhoto

UBS (UBS) analysts attempted to stun Shopify Inc. (NYSE:SHOP) (TSX:SHOP:CA) investors yesterday (January 10), as it highlighted critical metrics showing that Amazon’s (AMZN) Buy with Prime could make further inroads.

As a reminder, we discussed previously how Amazon intends to use its Buy with Prime initiative launched in 2022 to chart its direct-to-consumer (D2C) forays more aggressively.

Notably, Amazon has been exploring significant cost-cutting measures in recent months, including its 18K layoffs. It also impacted headcounts in its unprofitable bets, as CEO Andy Jassy & team refocused efforts to recover AMZN from its collapse.

But, with AWS’ profitability impacted by the slowdown in enterprise spending, we assessed that Amazon would likely increase its intensity in newer growth segments such as advertising, healthcare, and of course, fulfillment.

Why fulfillment? Because Amazon overexpanded! A recent study by supply chain consulting firm MWPVL highlighted that “in 2022, Amazon grew its warehouse footprint by 52 million square feet, less than half the capacity it added in each of the two previous years.” But, it has expanded so rapidly over the past three years that its total US warehouse space is now worth “roughly a third of what Walmart has added throughout its entire history.”

As such, Amazon’s capacity utilization has dropped significantly down to 65% (from 85% pre-pandemic), suggesting that Amazon has much more space to do fulfillment, likely from Shopify’s D2C merchants.

Notwithstanding, Shopify had a “record-setting Black Friday Cyber Monday weekend” in late November 2022. Hence, the company’s platform remains sticky with its merchants, even though Amazon’s Buy with Prime could gain share. We believe Amazon will likely intensify its competition with Shopify, with its profitability at stake after misjudging its expansion footprint.

Hence, Shopify must demonstrate increased momentum and operating leverage with Deliverr moving ahead while furthering its value proposition with its customers.

Notably, Shopify launched a new integration service, “Commerce Components,” aimed at helping more prominent D2C merchants to scale further, leveraging Shopify’s tech stack.

eMarketer highlighted that Shopify, with the slowdown in its smaller D2C merchants, “has sought to attract enterprise retailers to help it drive growth.” As such, enterprise merchants are projected to comprise 23.4% of its merchant base by 2024, up from just 16.5% in 2021. Hence, we believe that Shopify has several growth levers to pull, as it remains well-poised to build its D2C value proposition, helping its merchants to scale more effectively.

Also, Shopify is still founder-led, with CEO Tobi Lütke at the helm, constantly thinking of how to reinvigorate the company’s growth momentum. Amazon had reportedly sunk into the “Day Two” mindset that Chairman and founder Jeff Bezos warned about.

As such, investors should be pleased to know that founder-led Lütke is having none of it. Accordingly, management conducted a major revamp of its Slack (CRM) usage and adjusted the company’s meeting schedules in its bid to reshape its working culture and refocus on its growth initiatives.

Notably, the company “removed each employee from every existing public channel on the company’s Slack workspace, automatically canceling all meetings with more than two people as well as all meetings taking place on Wednesdays.”

Codenamed “Chaos Monkey 2023,” it has indeed created chaos among its ranks, leading to employees questioning the intent and effectiveness.

But Lütke was clear in his message to his company, highlighting why Shopify needs to move faster, with more focus, as 2023 could prove to be a highly challenging year for retail, worsened by intensifying macro headwinds. He articulated:

So what I’m trying to create is an environment where almost everyone around me feels uncomfortable all the time, because I’m dragging them into the next box. – Insider

With the Fed likely at peak hawkishness as inflation rates could fall further, we believe the steep decline in SHOP is likely near/at its end.

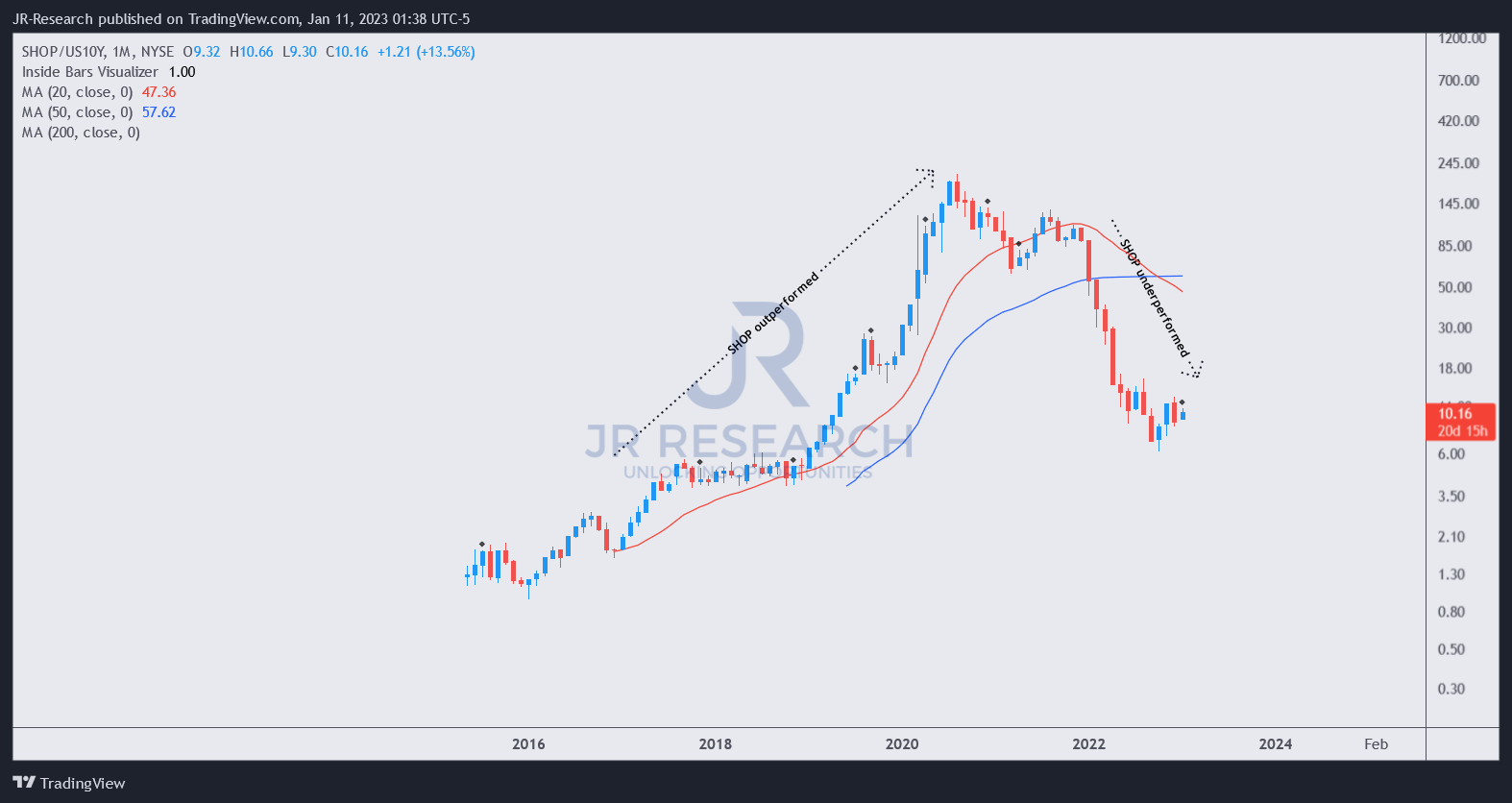

SHOP price chart (monthly) (TradingView)

As seen above, SHOP has underperformed significantly against the 10Y Treasury yields over the past year, falling below its 50-month moving average support (blue line).

But, SHOP’s growth premium suggests that investors need to be patient with it and not expect a rapid recovery anytime soon, as interest rates could remain high for some time.

However, we believe the recent pullback from its November highs is a constructive opportunity for investors to layer in.

Rating: Speculative Buy (Revise from Hold).

Note: As with our cautious/speculative ratings, investors must consider appropriate risk management strategies, including pre-defined stop-loss/profit-taking targets, within an appropriate risk exposure.

Be the first to comment