Scott Olson

Just over five months ago, I wrote on Shake Shack (NYSE:SHAK), noting that chasing the stock above $50.00 per share made little sense. This was because the stock was up 40% after a sharp multi-week rally but running into overhead resistance. Additionally, from a fundamental standpoint, the company had a tough H2 ahead with development delays, commodity inflation that was worse than expected sector-wide, and minimal improvement from a staffing standpoint across the industry. Following this August update, SHAK suffered a 20% drawdown to finish the year but has since rallied sharply after reporting its preliminary Q4 results.

I see little justification for this advance and continue to see SHAK as fully valued and continue to see far more attractive opportunities elsewhere in the market.

Q4 Preliminary Results & FY2023 Outlook

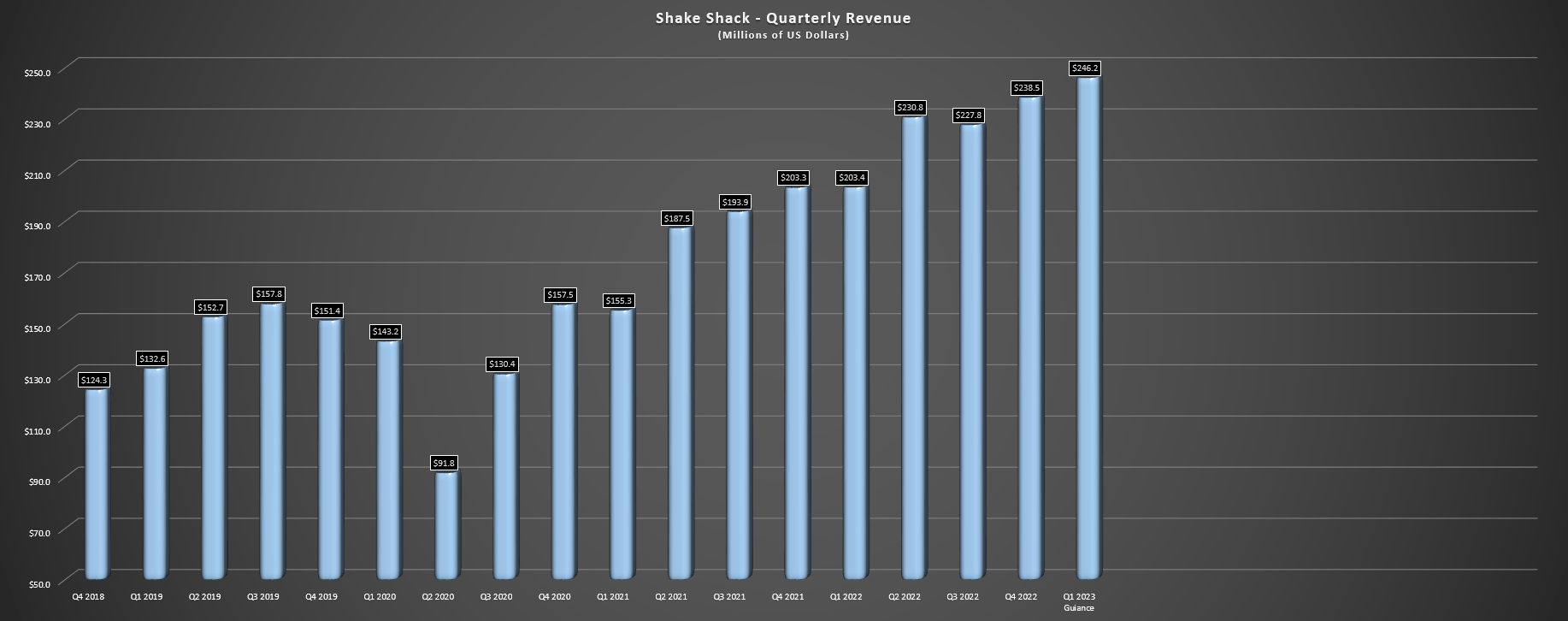

Shake Shack released its Q3 results in November, reporting quarterly revenue of $227.8 million, a 17% increase year-over-year. Unfortunately, this was overshadowed by another quarter of relatively weak shack-level operating margins (16.3%), which were up 50 basis points year-over-year but only due to being up against very easy year-over-year comps (15.8%). The continued softness in margins can be attributed to continued inflationary pressures and investments in team members, partially offset by pricing, guests trading up to premium offers and limited-time offerings, and continued improvement in urban traffic, which has weighed on results post-pandemic.

Shake Shack – Quarterly Revenue (Company Filings, Author’s Chart)

Although these issues were not company-specific, and we’ve seen margin pressure for most operators industry-wide, all eyes were on the Q4 results. Shake Shack had guided for revenue of $236.0 million at the mid-point, 21 new company-operated shack openings to deliver into guidance, and shack-level operating profit of 16-18%. Fortunately, the company easily beat these figures, reporting preliminary revenue of $238.5 million (1.1% beat) and shack-level operating margin of 19% (12% beat), but came in at the low end from a development standpoint, opening just 36 company-operated shacks vs. its initial guidance of 35-40 shacks in FY2022. The miss was related to permitting/landlord construction delays and equipment availability.

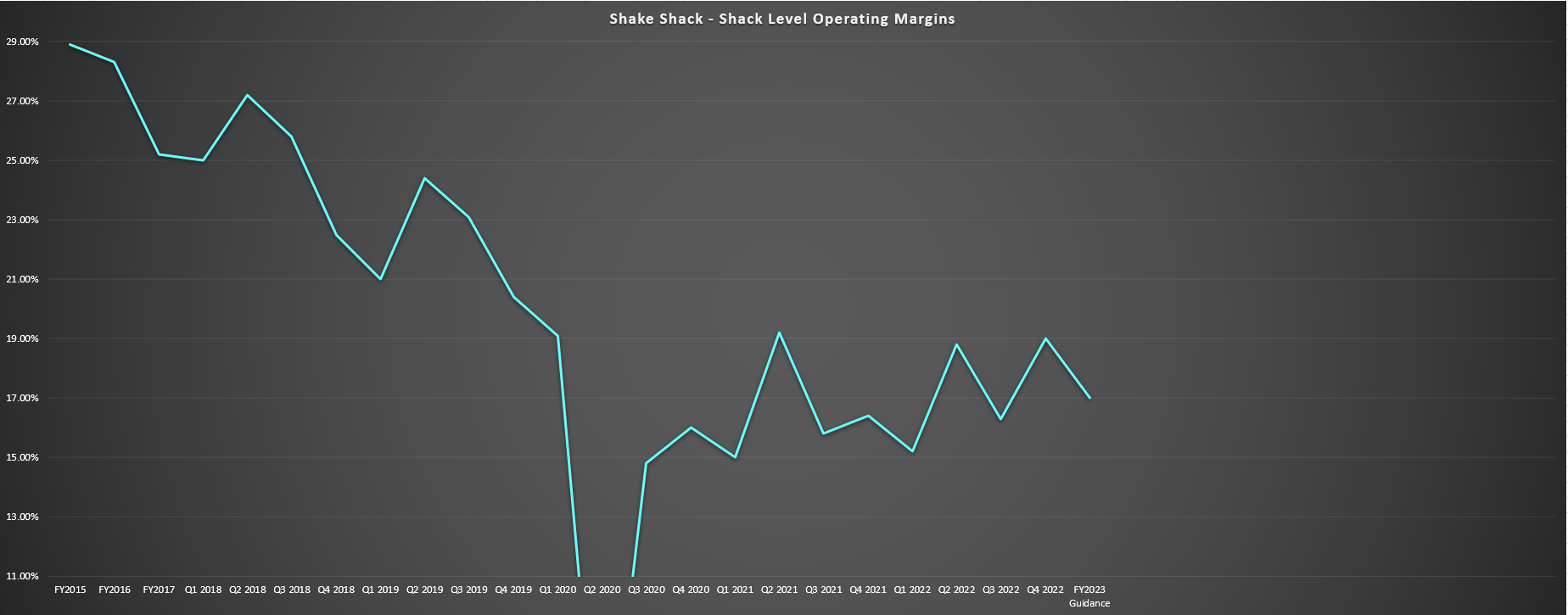

Shake Shack – Shack Level Operating Margins (Company Filings, Author’s Chart)

Some investors might be elated with the margin performance that trounced the guidance provided, but it’s important to note while margins may have ticked up short-term, the multi-year trend is down, and we’ve seen little traction to the upside. This is evidenced by margins sliding from 28.9% in FY2015 to 17% in FY2022, with this figure being well below its target of 18-22% shack-level operating margins long-term, which is miles below its previous baseline, with the sharp decline in margins beginning in FY2017 when the company guided for 27.0% margins and came in at 25.2%. It doesn’t help that build costs per shack are up significantly to ~$2.4 million vs. $2.0 to $2.1 million previously, reducing payback per store.

The good news is that Shake Shack has identified areas for margin improvement, doubling down on kiosks (rolling out across the full system by the end of this year) which are its highest-margin channel, and provide operators during heavy traffic periods and amid staffing challenges. In addition, the company continues to see successful limited-time offerings, with its recent Hot collaboration being a hit. However, with upward pressure on wage rates and what could be higher inflation for longer, it’s difficult to see how Shake Shack will return to sustainable 19% plus shack-level margins without more aggressive pricing or significant productivity gains.

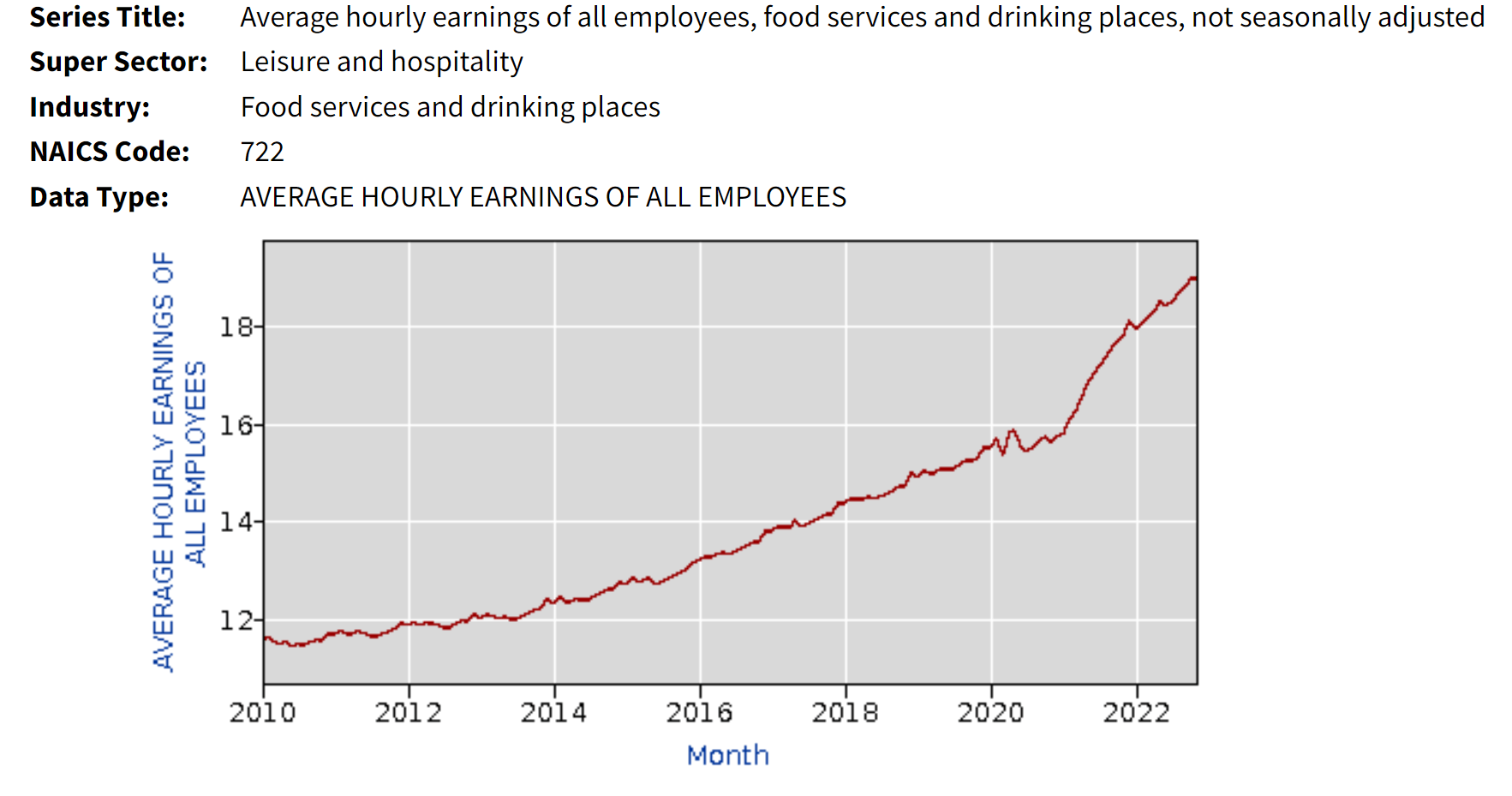

As shown below, the rate of change in average hourly earnings for all food services/drinking places employees is entirely different from the past, and even if wage rates return to a slow crawl from these levels, this paints an entirely different picture than what restaurant operators were used to in the previous decade. Shake Shack noted in its most recent earnings call that it continued to face staffing pressures in certain markets, and it continues to increase wage rates in markets that need high levels. While this is positive for retention and attracting talent, it’s not ideal from a margin standpoint that further regular raises are required after two years of significant investments in wages already.

Average Hourly Earnings – Food/Drink Employees (Bureau of Labor Statistics)

Recent Developments & Industry Trends

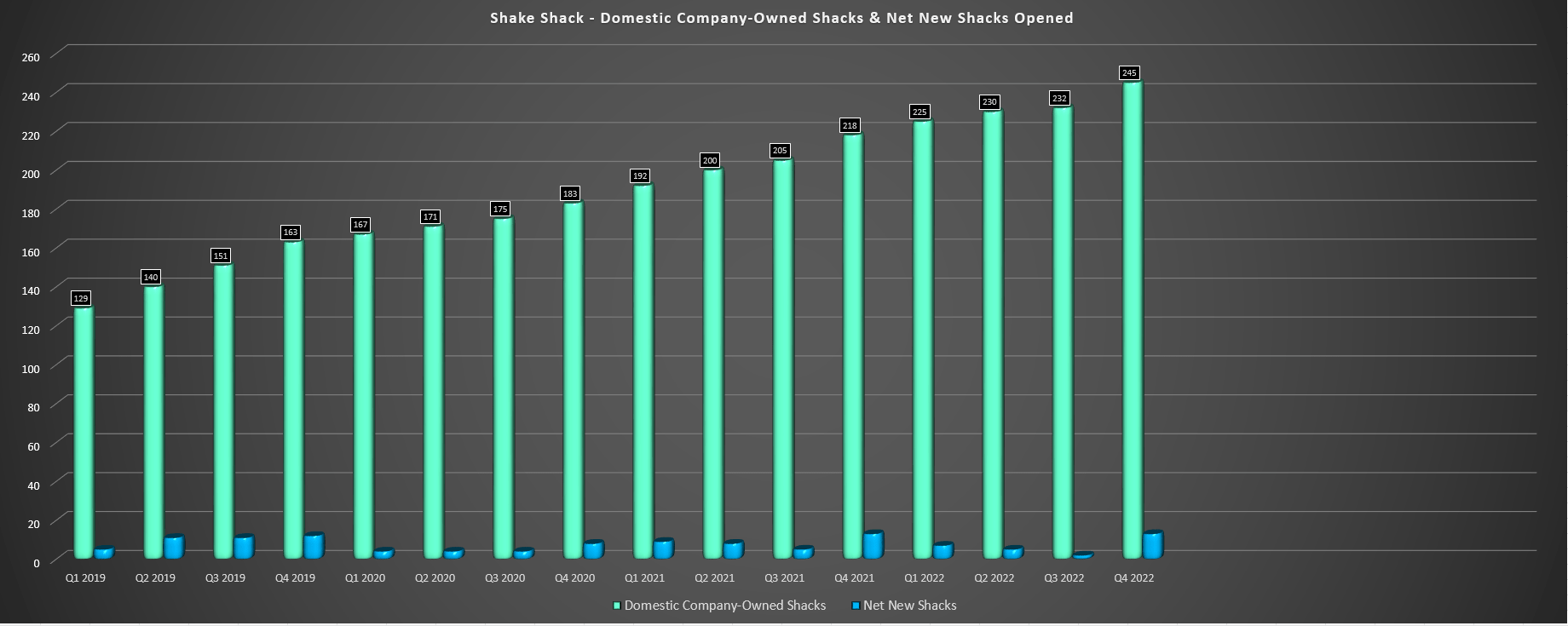

Moving over to recent developments, Shake Shack guided for ~40 new company-owned shack openings in FY2023 which would translate to an industry-leading ~16% unit growth rate this year. This is one clear differentiator between this story vs. its peer group. However, the major difference is that while Chipotle (CMG) and Kura Sushi (KRUS) are growing rapidly, they’re doing while enjoying margin expansion which justifies a very aggressive pace of unit growth. In Shake Shack’s case, margins are in long-term decline, and there’s no clear path to clawing back these lost margins unless one takes a very optimistic view on inflation levels rolling over materially and limited pressure regarding wage growth in the food service industry.

Shake Shack – Domestic Company-Owned Shacks & Net New Openings (Company Filings, Author’s Chart)

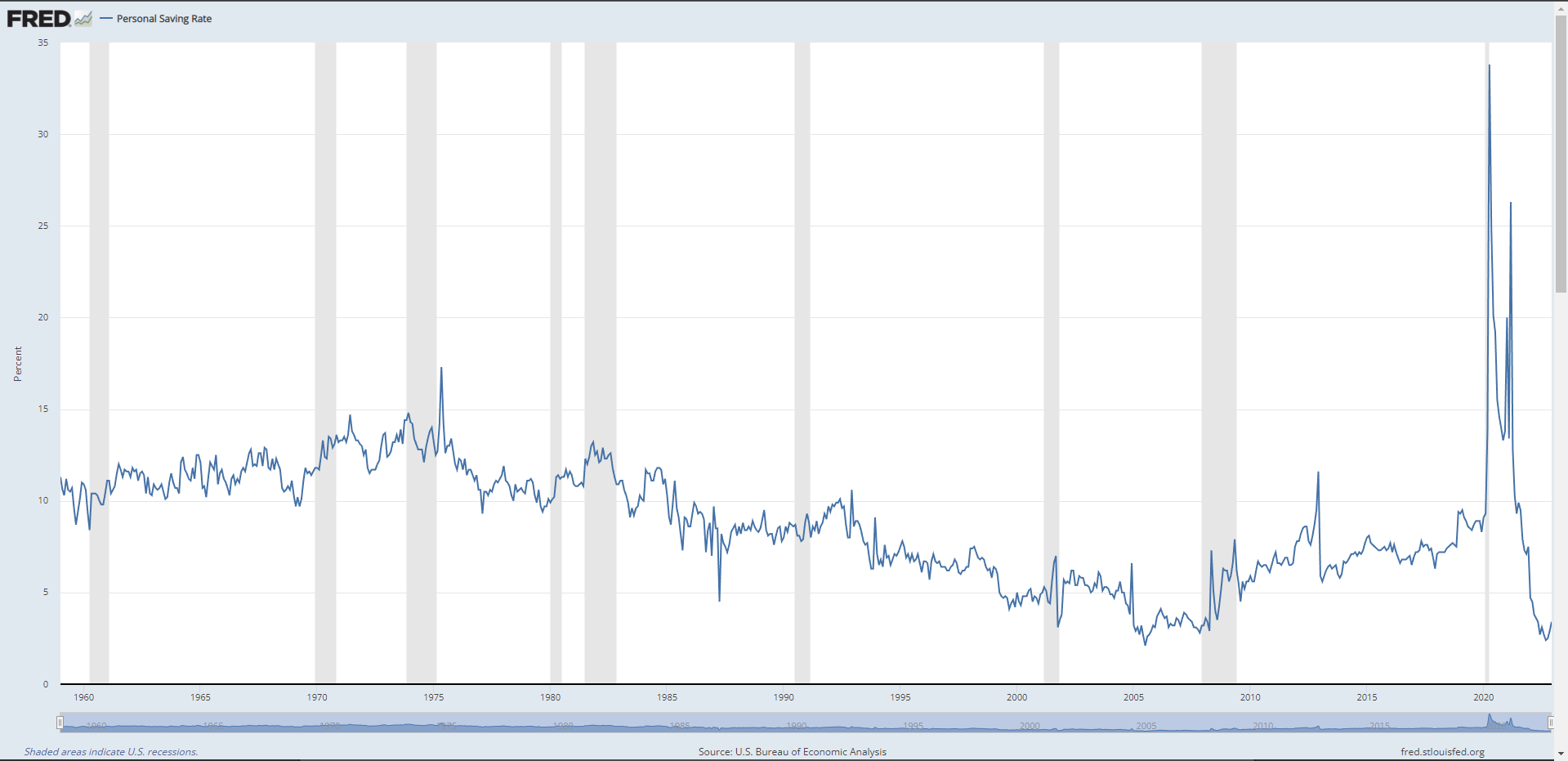

The other negative is that the industry backdrop remains challenging, with personal savings rates at multi-year lows and discretionary budgets continuing to remain under pressure. This can be attributed to rising rent/mortgage costs, higher grocery/energy costs, and general inflation, which have placed financial stress on the average consumer. Worse, we’ve seen a sharp reversal in the wealth effect with bear markets in equities and cryptocurrencies, plus a more negative outlook for the housing market, which certainly doesn’t increase consumers’ appetite to spend when they’re feeling less affluent. Hence, it’s little surprise that restaurant sales softened in November, with same-store traffic down 4.3%, according to Black Box Intelligence.

Personal Savings Rates (Fred.St.LouisFed.Org)

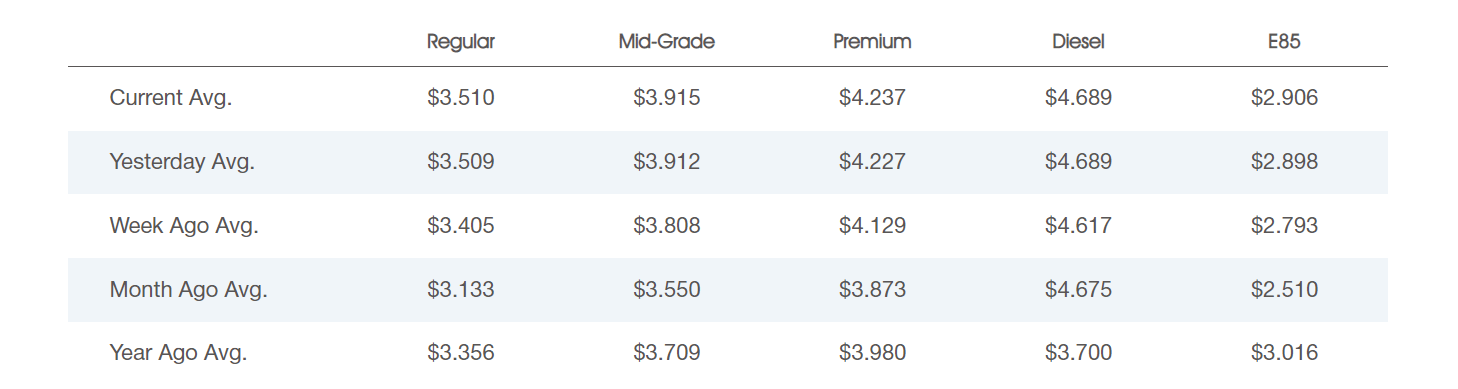

National Average Gas Prices (AAA Gas Prices)

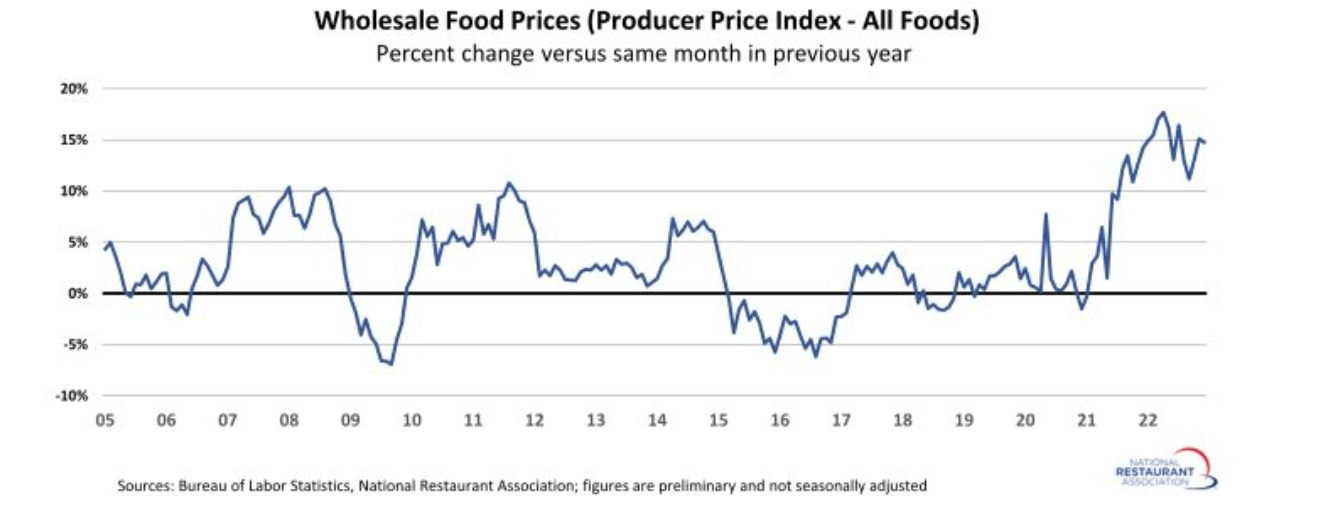

Finally, while negative traffic growth due to inflation and the reverse wealth effect are headwinds from a revenue standpoint for Shake Shack and other operators, the industry has continued to see commodity/wage inflation which has maimed margins. We’ve seen clear evidence of this in Shake Shack’s margins, with food and paper costs up 190 basis points, labor costs up 210 basis points, and other expenses up 310 basis points vs. pre-COVID-19 levels (Q3 2019). This has resulted in a 680 basis point decline in shack-level operating margins despite high double-digit pricing in the period. Within commodities, Shake Shack called out dairy, fryer oil, fries, and packaging as being drivers of higher costs, while wage inflation and higher energy and repair/maintenance impacted the latter two categories.

Wholesale Food Prices (National Restaurant Association, Bureau of Labor Statistics)

The good news is that we appear to be seeing some moderation in commodity inflation, and some quick-service brands expect only mild commodity inflation in 2023. This would certainly benefit Shake Shack, whose food and paper costs came in at ~31% in Q3 2022. However, as noted at a recent conference, Shake Shack management stated the following:

“But then the one thing that does not look like it’s going to be coming down is wage inflation. And we know we have to step up there and support our team members to be fully staffed and open.”

– Eat, Sleep, Play Conference – November 2022

To summarize, while there are green shoots when it comes to commodity inflation in 2023, and many operators could benefit from a much lower inflation rate for some items, wage inflation remains a significant headwind, and I would be shocked to see material traffic growth industry-wide. This setup is not ideal when it comes to the ability to beat estimates, and in a period of rising rates (and higher for longer rates), industry-wide labor tightness, and arguably a recessionary environment, investors should demand a significant margin of safety to justify investing in restaurant stocks, and especially those where margins remain in downtrends like Red Robin (RRGB) and Shake Shack. Let’s take a look at SHAK’s valuation to see whether this less ebullient outlook is priced into the stock.

Valuation & Technical Picture

Based on ~42.2 million shares and a share price of $56.50, Shake Shack trades at a market cap of $2.38 billion, which leaves the stock trading at ~23.3x FY2023 EBITDA estimates (~$102 million). If we compare this to its historical multiple of ~27.7x EBITDA, this might appear to be a cheap valuation for Shake Shack. However, it’s worth noting that margins remain in a long-term downtrend, and the industry continues to face challenges (negative traffic growth and commodity/wage inflation, even if it is moderating). Hence, I do not believe it makes sense to expect SHAK to trade at its historical multiple of ~27.7x EBITDA in the current environment. Instead, I think a more conservative multiple is 15.0 when factoring in margin erosion, multiple compression in growth stocks, and industry headwinds.

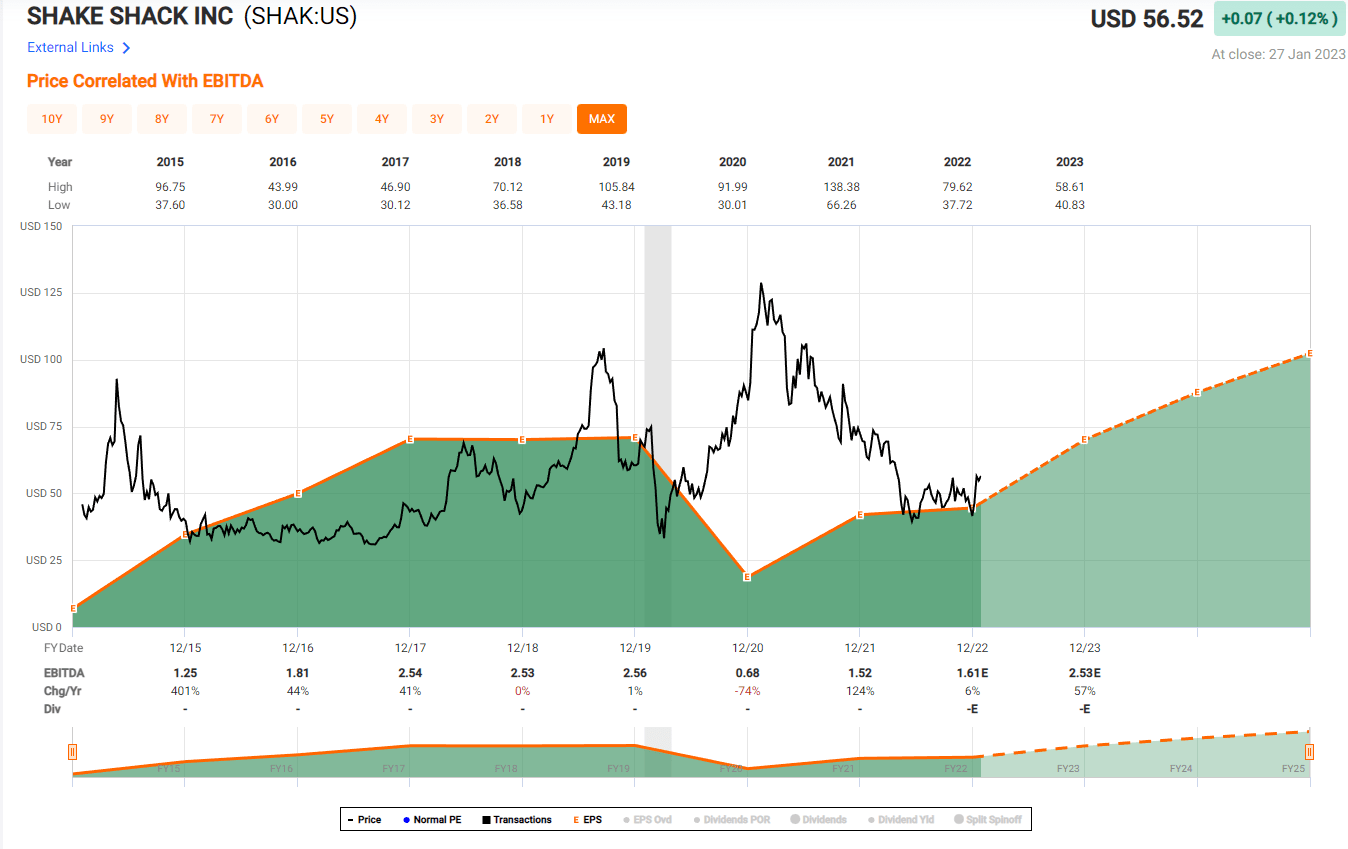

SHAK Historical EBITDA Multiple & Forward Estimates (FASTGraphs.com)

Using a more conservative EBITDA multiple of 16.0 and medium-term FY2024 EBITDA estimates of $129 million, I see a fair value for Shake Shack of ~$2.06 billion, translating to a fair value of $48.90. This suggests that the stock is fully valued at current levels and is trading 15% above what I believe to be a more conservative assessment of fair value vs. the premium multiple it enjoyed while it had a rare combination of industry-leading unit growth and strong margins (26% shack level operating profit). As discussed earlier, this is not the case currently, and even if Shake Shack meets the mid-point of FY2023 margin estimates, margins would still be down more than 1100 basis points from its 2015/2016 two-year average shack level operating profit of 28.6%. Hence, I don’t see any way to justify paying up for the stock here.

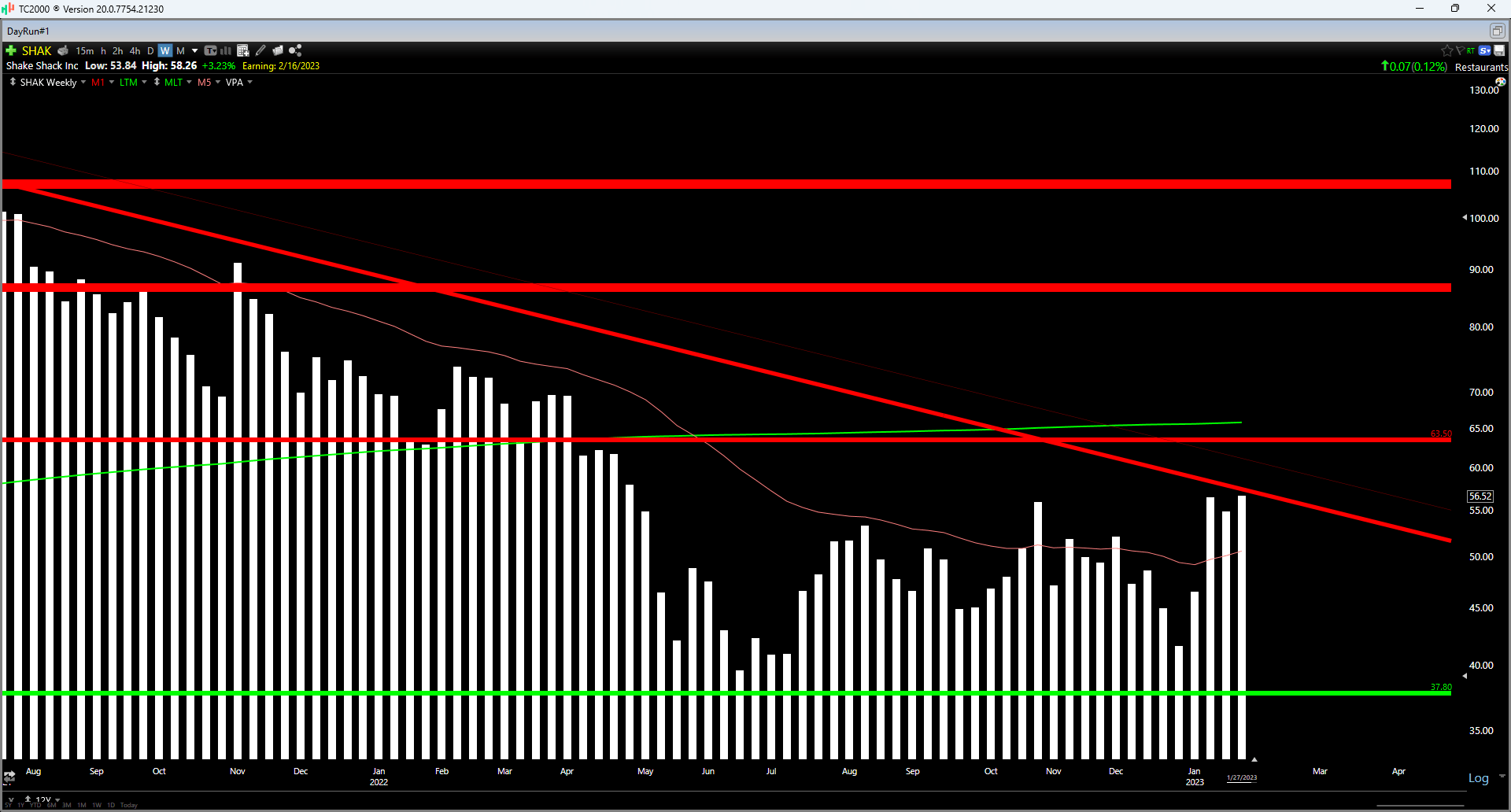

While Shake Shack’s valuation leaves much to be desired with no margin of safety at current levels, its technical picture isn’t great either. As shown in the chart below, the stock is now extended above major support at $37.80, has short-term resistance at $57.20 (long-term downtrend line), and strong resistance at $63.50. If we compare this to a current share price of $56.50 and even if we ignore short-term resistance (which could provide some trouble for the stock), this translates to just $7.00 in potential upside to resistance and $18.70 in potential downside to support. The result is a 0.37 to 1.0 reward/risk, a very unfavorable reward/risk ratio for starting new positions.

I prefer a minimum 6 to 1 reward/risk ratio for mid-cap names, which would require a pullback below $41.40 per share.

SHAK Weekly Chart (TC2000.com)

Summary

Shake Shack’s store count continues to grow like a weed, and the company is working hard to optimize its restaurants and claw back lost margins, including a vast array of store formats and rolling out kiosks and drive-thrus across the chain to provide added convenience for guests and double down on its highest-margin channel (kiosks). That said, the path to 18.0% to 20.0% margins looks elusive, especially with the potential for long-term pressure on wages and what could be higher for longer inflation than many expect (even if we are seeing more moderation). Given this outlook, I don’t see any way to justify historical multiples, and I see SHAK as fully valued using more conservative multiples. To summarize, I see no reason to chase the stock here and would view any rallies to $60.00 before June as an opportunity to book some profits.

Be the first to comment