greenbutterfly

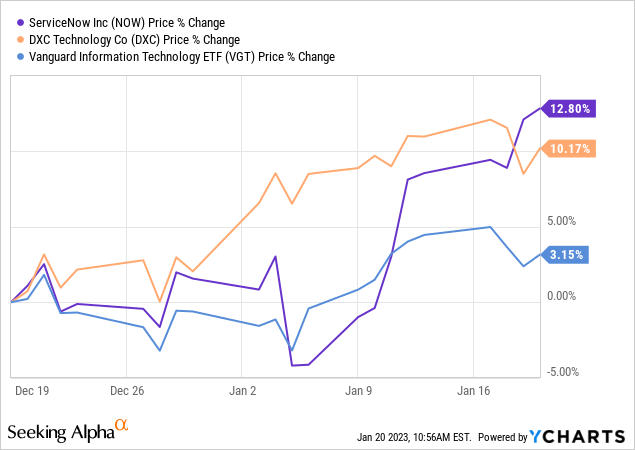

Both ServiceNow (NYSE:NOW) and DXC Technology (NYSE:DXC) stocks have been outperforming the Vanguard Information Technology ETF (VGT) since the last month during a period that has been marked by a lot of uncertainty pertaining to how aggressive the Fed is likely to be in its battle against inflation and also some warning by Gartner about IT spend going down as I will elaborate on later.

Now, an analyst at UBS Group (UBS) is bullish for ServiceNow’s outlook because of its partnership ecosystem despite the uncertainty, while others are optimistic about the company’s profitability. As for DXC, it has been upgraded too due to prospects for margin expansion together with a more defensive revenue mix by analysts at JPMorgan (JPM).

Now, DXC is the leading ServiceNow ecosystem partner for Platform X as I will detail later, and my objective with this thesis is to show how their partnership in current uncertain economic conditions can prove beneficial for customers, as well as assess the benefits for the two companies, both in terms of revenue growth and margin expansion.

First, for those who are new to the concept, I explain how partnership involving platforms means a lot for customers as they have at their disposal a tool that they can use right from Day 1.

The Platform-Partnership Approach

Today when you go through the earnings transcripts or corporate presentations of IT software companies, most of them talk about platforms or cloud-based platforms. Well, it was not always like this just seven years ago. Before the platform age, in order to cater to a new client, service providers had to painstakingly go through a procedure including many steps like server provisioning, installation of the operating system, the configuration of software, and testing before a customer could use applications.

Things were even more complicated when a company’s footprint was spread over a wide area. It could take months for projects to materialize if the customer required specific customizations. Talking figures, according to Tech Republic, costs (both setup and implementation) drop by around 50% by adopting cloud apps and infrastructure, or, in other words, a platform. In this case, you just have to log in to the platform portal and with a few clicks, you are ready to go as exemplified by ServiceNow’s cloud-based workflow automation platform.

It plays a key role in organizations to streamline their routine operations and improve operational efficiencies, namely through self-service tools whereby users can go to a large extent in solving technical issues themselves while sparring costly support man-hours to the IT department. This all makes sense when wage inflation is high.

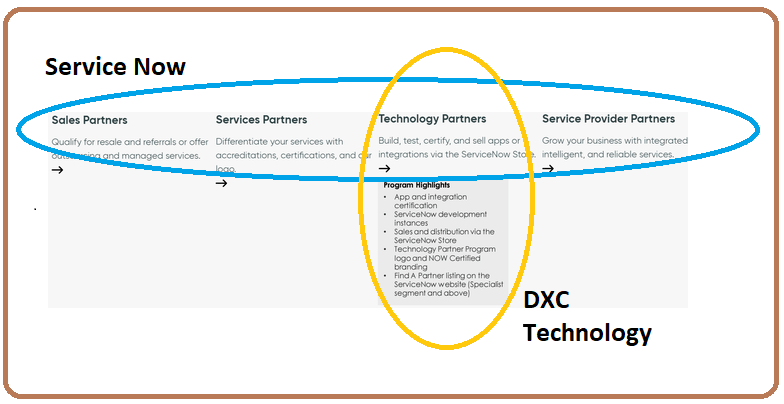

Of course, there are still tasks like integration with other platforms, which are done by technology partners like DXC as pictured below.

Technology partnership diagram Built using data from (www.servicenow.com)

Noteworthily, whereas cloud-based workflow automation platform provider ServiceNow focuses on more general purpose ITSM, systems integrator DXC focuses on enabling IT teams to quickly detect and fix problems that may occur on their infrastructures.

It is now time to go into the specifics of how the companies’ platforms are appealing to customers.

Appeal to Customers and Organic Growth

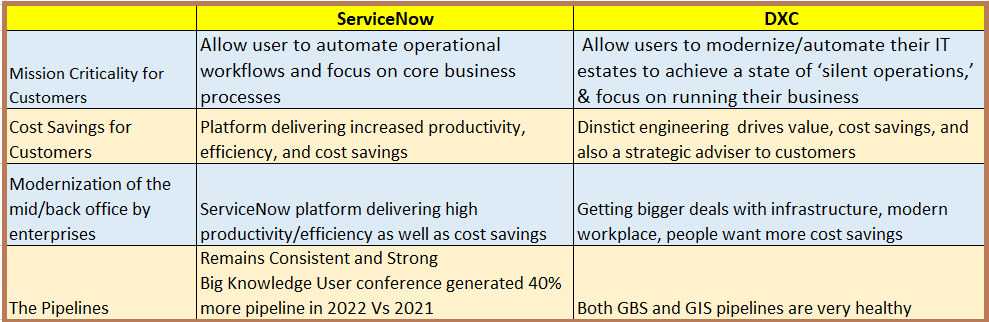

Looking at the mission criticality aspect of their platforms for customers as pictured below, these basically automate operations and allow customers to focus on core business processes. According to DXC’s President and CEO, “it’s about modernizing and automating their IT estates to achieve a state of ‘silent operations,’ saving time, money and letting customers focus on what’s most important — running their business.”

Appeal to Customers in terms of mission criticality, cost savings (www.seekingalpha.com)

Therefore, there are also the cost savings aspects together with productivity gains, and with DXC and ServiceNow working together, it’s like customers having a ready-to-operate platform from Day 1 and where the integration is done in advance for them.

This is the reason ServiceNow’s growth prospects remain strong, with 40% more pipeline, or the possibility to convert leads into sales in 2022 versus 2021 while DXC is seeing bigger deals for IT infrastructure. This company operates with two main segments, GBS (Global Business Services) which accelerates digital transformation for customers, and GIS (Global Infrastructure Services), which focuses on infrastructure.

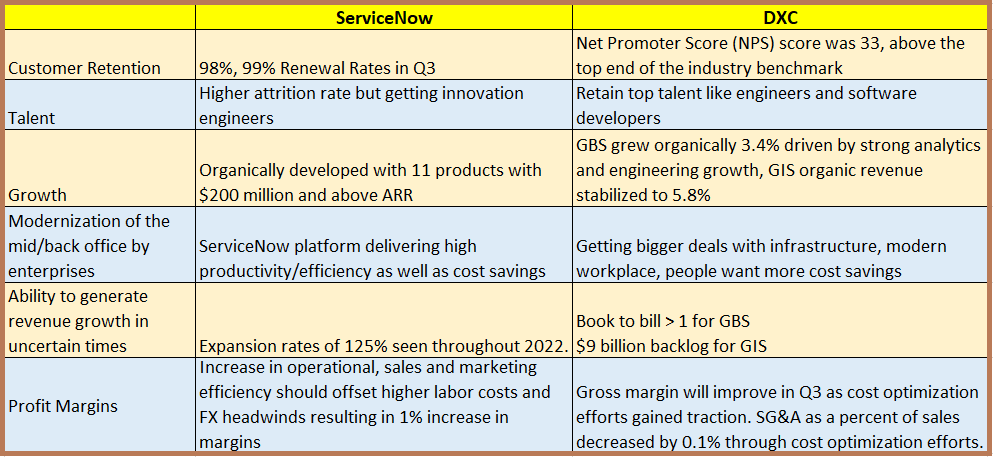

Looking at the advantages of each of the companies, they both have good customer retention metrics as shown in the table below. Now, when a company’s product is appealing and in demand, it has to deliver and for this purpose, it needs talented employees. Now, both platform players have suffered from higher attrition rates in 2022 compared to 2021, as is the case for most software companies, but have still been able to recruit key innovation engineers. This ability is key to generating organic growth, which is a more cash-friendly way to grow revenues in uncertain times compared to acquisitions. In this way, ServiceNow has developed 11 products with an ARR of $200 million some of them even exceeding $500 million.

Internet strength, growth, talent retention, and margins. Table built using data from (www.seekingalpha.com)

As for DXC, GBS is seeing progression, driven by analytics tools while for GIS, the worst is over with the decline of revenues having been stabilized as the company obtains larger deals. There is demand despite deteriorating macros with a trailing 12-month book-to-bill of over one implying that they’re more orders have been received compared to what has been delivered.

The next step is to assess the revenue mix and profit margins.

Revenue Mix, Margins, and Valuations

DXC’s margins were impacted by its Russian exit, lower income from pension, and the strong dollar. Forex exchange headwinds are expected to create a shortfall of $1.2 billion for the full fiscal year 2023 which ends in March, but this figure which was provided by the management on November 3 when the dollar was at its peak could decrease as the greenback since receded by 9%.

Another key factor that can improve profitability is revenue mix as GBS’s role in the business becomes more prominent and it contributes to a higher share of overall revenues. GBS has seen sustained growth for the last six quarters and it is also more profitable than GIS and requires relatively fewer capital expenses, implying better free cash flow prospects.

Also, as seen in the table below, while its gross margins are only 21.63% as it is also a consultancy business with a higher cost of revenues as a result of employing many consultants, DXC’s net income, at 4.93% surpasses ServiceNow, showing efficiency at the operational level. For this matter, gross margins are expected to ameliorate in the third quarter as cost optimization efforts pay back with SG&A as a percent of sales has already decreased by 0.1% in the second quarter which ended in September 2022. Also, the company expects to generate about $250 million of cash from the disposal of underutilized offices and data centers.

Comparison of key metrics (www.seekingalpha.com)

As for valuations, with a trailing price-to-earnings multiple (GAAP) of 9.07x, the company is undervalued relative to the IT sector by a whopping 61.5%. Adjusting for a 20% gain, I obtain a share price of $33.8 (28.17×1.2) based on the current share price of $28.17.

As for ServiceNow, an increase in operational, sales, and marketing efficiencies should offset higher labor costs and currency headwinds resulting in a 1% increase in margins. Also, Fx headwinds are expected to reduce operating margins by 1% and decrease subscription revenues by $290 million. Again these predictions were made when the dollar index was at its peak and could benefit from some relief with a lower greenback.

The company can also count on its high free cash flow margins of over 31% as pictured above, which is above the IT sector by a whopping 327%. Now, with such a high cash-generating capacity, it is no surprise that investors have rewarded it with a price-to-cash flow of 35x which is above the median for the IT sector by 85%. However, after a fall of 20% in one year, it is probable that the stock could again flirt with the $445-$450 support level in case it beats earnings estimates, as has been the case for the last 12 quarters.

Conclusion

Therefore, both these companies have the capability to increment revenue and expand their margins, which is the reason I have a buy rating on both, which is aligned with Wall Street’s analysts’ positions. This buy rating is also based on platform and partnership strengths.

In this respect, platform economics are advantageous in terms of deployment time and effort. The reason is that these two companies can continue to add new functionalities to their platforms and it is automatically replicated across every product and available to all customers, depending on their subscriptions. One example is ServiceNow evolving from ITSM, ITOM, ERP, and creator workflows without having to overhaul its infrastructure completely.

Going one step further, its partnership with DXC goes beyond the simple partner paradigm as it is its preferred workflow partner for its DXC Platform X offering. This enables ultra-fast deployment of industry-specific workflows, thereby reducing costs drastically for customers.

Finally, a partnership based on platforms is also a cost-effective way to offer services to clients who are ready to pay for it given the perceived value.

Be the first to comment