Just_Super

SentinelOne (NYSE:S) is a leading next-gen endpoint and cloud security company that has been punished by investors since its IPO in 2021 due to valuation concerns and large losses. SentinelOne’s valuation is now far more reasonable and profitability will come as the business matures due to strong unit economics.

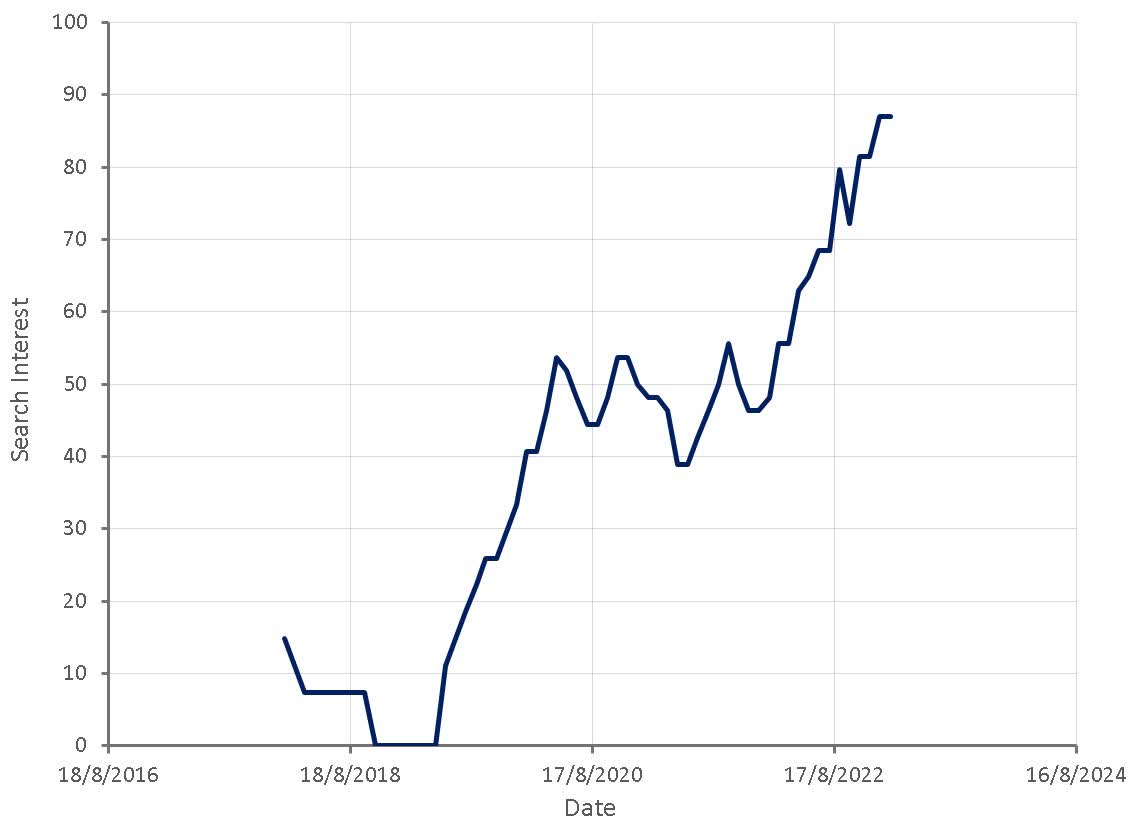

Search interest for SentinelOne pricing continues to increase, indicating growing demand for SentinelOne’s platform. Other upstream indicators of demand like website traffic and job openings also still appear to be fairly robust. It is reasonable to expect 2023 to be more difficult for cybersecurity vendors though, given strong increases in spending over the past few years, ongoing job losses amongst white collar workers and pressure on remote workers to return to the office.

Figure 1: “SentinelOne Pricing” Search Interest (source: Created by author using data from Google Trends)

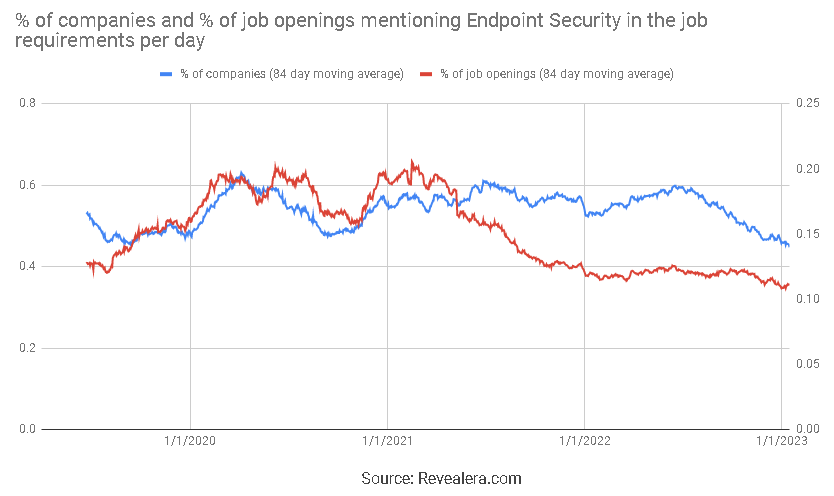

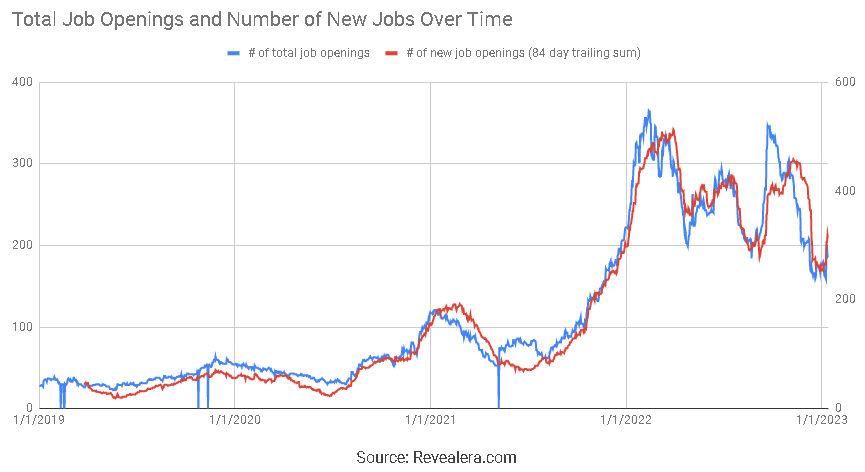

The number of job openings mentioning endpoint security in the job requirements has eased over the past 12 months, although may now be beginning to stabilize. It should be noted that changes in demand are bifurcated between legacy and next-gen vendors, with the former rapidly giving up share to the latter.

Figure 2: Job Openings Mentioning Endpoint Security in the Job Requirements (source: Revealera.com)

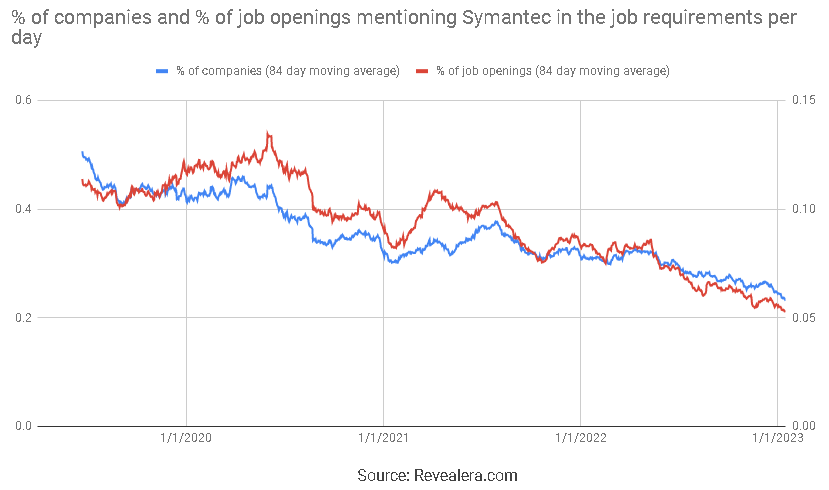

This is illustrated by the number of job openings mentioning Symantec in the job requirements, which has declined steadily over the past 3 years.

Figure 3: Job Openings Mentioning Symantec in the Job Requirements (source: Revealera.com)

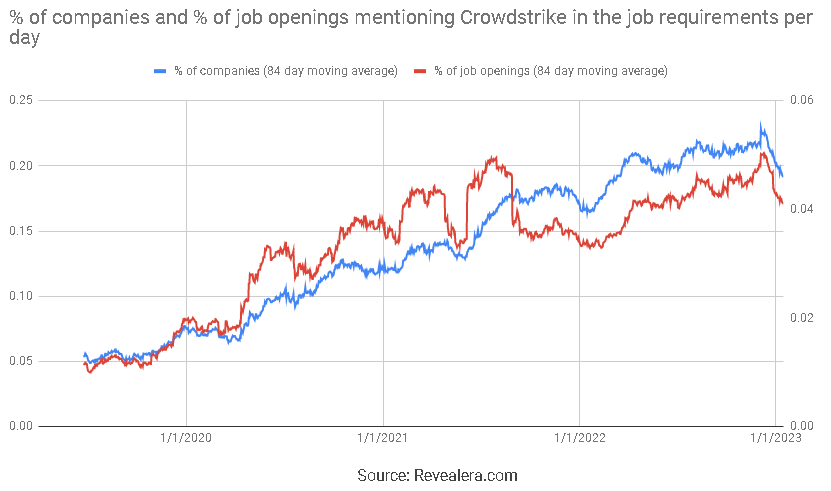

In comparison, the number of job openings mentioning CrowdStrike (CRWD) in the job requirements increased steadily over the same period. These job openings have dipped in the last few weeks, but there may be a seasonal component to this.

Figure 4: Job Openings Mentioning CrowdStrike in the Job Requirements (source: Revealera.com)

SentinelOne continues to face macro headwinds, with uncertainty affecting customer procurement decisions, leading to longer sales cycles and purchase delays (particularly amongst larger deals). Singularity Cloud remains SentinelOne’s fastest-growing solution, followed by strong contributions from other emerging solutions. This stands in contrast with CrowdStrike, where emerging solutions are driving revenue growth. SentinelOne’s partner ecosystem (MSSPs and Incident Response providers) is another area of strength.

SentinelOne also secured three new federal agencies during the third quarter. This builds on SentinelOne’s partnership with CISA, which recently expanded to include membership in the Joint Cyber Defense Collaborative. JCDC is designed to unite the global cyber community in the collective defense of cyberspace.

SentinelOne also recently launched S Ventures to support innovation in security and data technologies through minority investments. S Ventures will be used to expand the reach of SentinelOne’s platform into adjacent verticals. Recent investments include:

- Armorblox – an API-based email security platform that leverages machine learning to detect and prevent threats

- Noetic Cyber – a cyber asset management & controls platform that provides teams with unified visibility into the security posture of all assets

Given the current lack of liquidity in markets, this could be a good use of SentinelOne’s large cash balance, provided they are able to leverage their expertise to identify attractive investment opportunities.

The fourth quarter should be reasonably strong for SentinelOne as there were a number of deals that pushed beyond Q3, and these represented several million dollars. Management has stated that pricing remains healthy and that win rates continue to be extremely strong. Net new ARR is expected to increase by at least 20% sequentially in the fourth quarter, despite macro weakness.

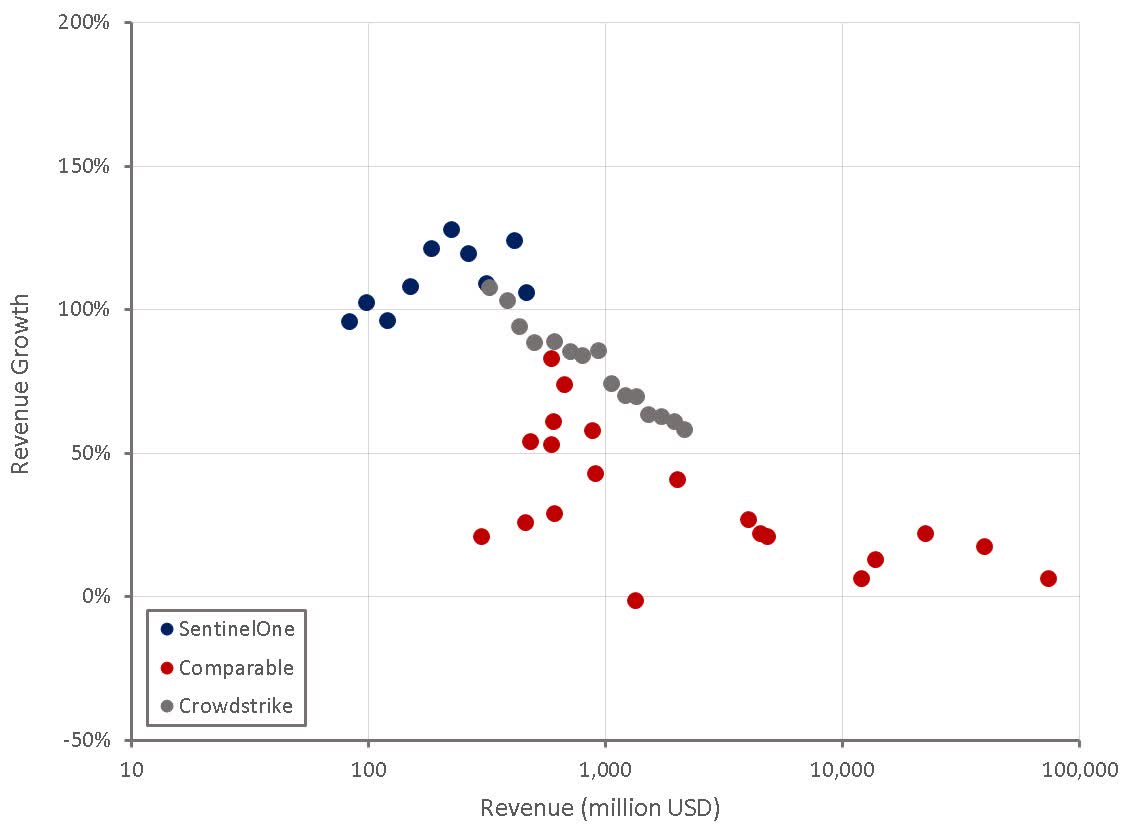

Figure 5: SentinelOne Revenue Growth (source: Created by author using data from SentinelOne)

SentinelOne expects to deliver at least 50% total ARR growth in FY2024, which management has stated is a conservative estimate and should be viewed more as a floor. Analysts are also expecting a steep growth decline in 2023, although growth will still be strong by any reasonable measure.

Table 1: Analyst Estimates of SentinelOne Revenue Growth (source: Created by author using data from Seeking Alpha)

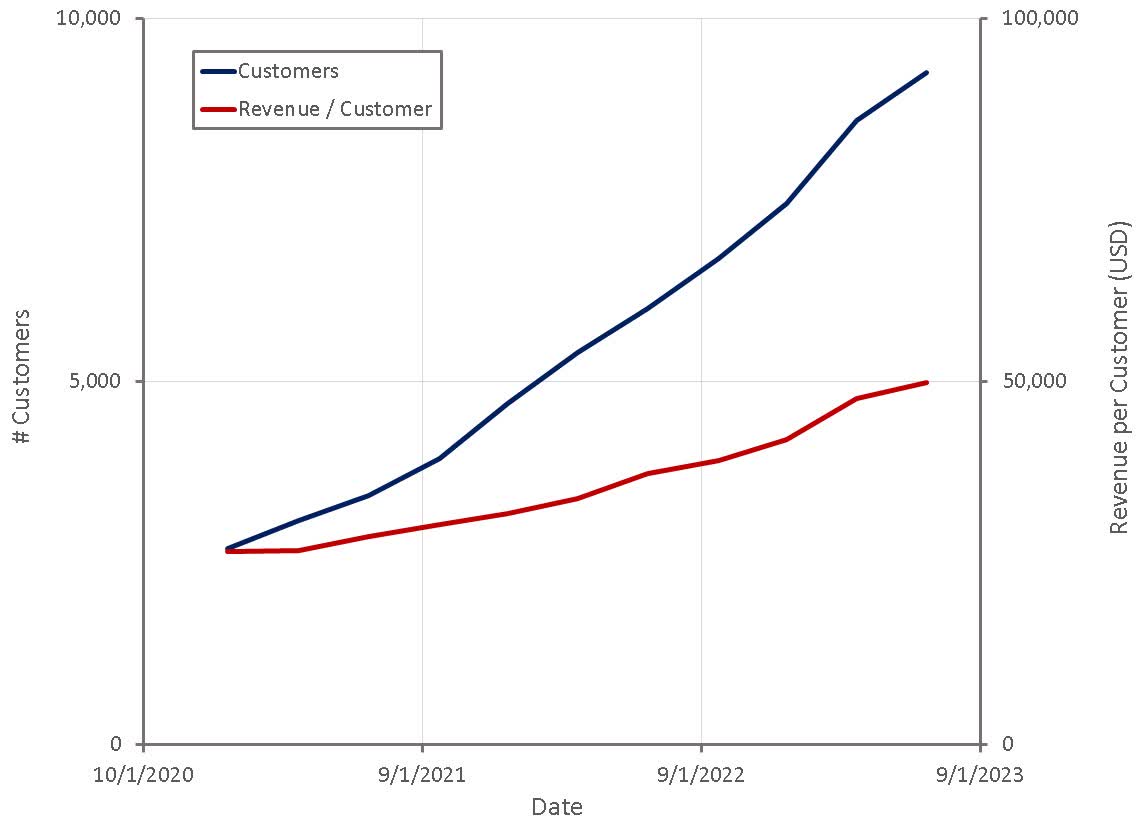

SentinelOne’s growth continues to come from a healthy mix of new customers and expansion within existing customers. Over two-thirds of ARR now comes from large enterprises, and customers with ARR over 1 million USD grew by more than 100% YoY in Q3. SentinelOne’s historical strength has been with smaller organizations, making increased penetration of larger organizations an important driver of future growth.

Strong adoption by larger customers along with expansion amongst existing customers is driving SentinelOne’s average revenue per customer higher, although this figure is still less than half of CrowdStrike’s. The addition of new customers weakened in the third quarter, likely pointing towards a growth slowdown next year.

Figure 6: SentinelOne Customers (source: Created by author using data from SentinelOne)

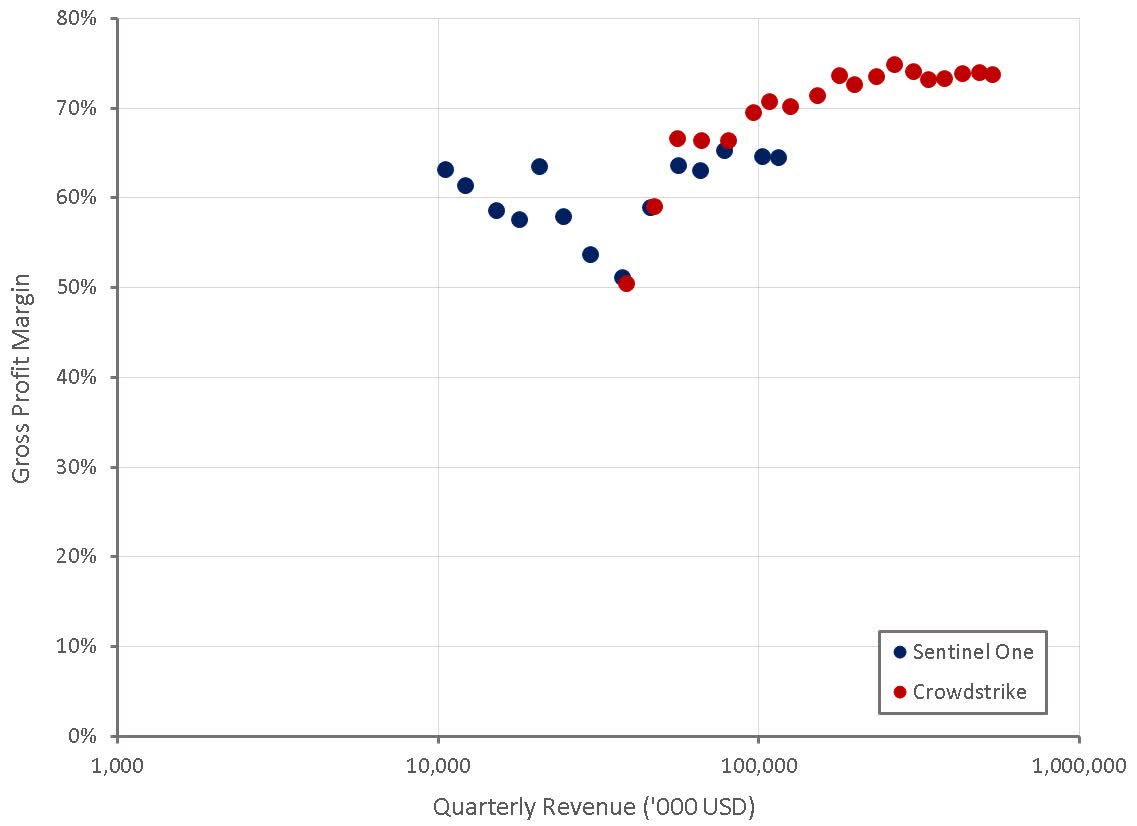

Gross profit margins disappointed in the third quarter and this is an area that SentinelOne needs to begin demonstrating progress. SentinelOne are targeting gross margins of 75-80+ percent in the long-term but have been facing headwinds from the migration of customers to the DataSet backend. While management has suggested that win rates are healthy and there has been no change in the pricing environment, an ongoing inability to scale gross margins could call into question the company’s competitive position.

Figure 7: SentinelOne Gross Profit Margins (source: Created by author using data from company reports)

SentinelOne’s operating losses remain large, despite substantial progress being made over the past few quarters. Management has begun taking a more prudent approach to investments, including moderating headcount growth, and they are also trying to streamline processes and improve productivity. SaaS companies in general should also be aided by the fact that the market for talent has cooled significantly. For companies that are managed in the interest of shareholders, this should lead to lower compensation expenses.

SentinelOne continue to target operating breakeven in FY2025 and positive free cash flow by the end of this year, which based on their current trajectory and the past experience of similar companies is an achievable, although aggressive target.

Figure 8: SentinelOne Operating Profit Margins (source: Created by author using data from company reports)

Much of SentinelOne’s operating expenses are due to sales and marketing, but this does not imply they have a problem with their salesforce. SentinelOne’s magic number was over 1.2x in the third quarter, in line with CrowdStrike’s magic number of 1.2x.

Nearly half of SentinelOne’s sales reps are still ramping and as they mature, meaningful productivity gains should be realized. SentinelOne’s employee retention also remains better than industry average, something that some companies have struggled with over the past few years.

Figure 9: SentinelOne Job Openings (source: Revealera.com)

SentinelOne believes that their ability to offer automated solutions and best-in-class protection help them to win customers. Multi-tenancy support, fully customizable role-based access control and a full set of open and documented APIs are also highlighted strengths.

Management continues to point to wins across a significant majority of competitive situations, which is somewhat difficult to parse given that CrowdStrike make similar claims. This would suggest that CrowdStrike and SentinelOne are often not competing directly against each other or that win rates are not as strong as implied.

SentinelOne has also suggested that they are seeing more Microsoft (MSFT) displacements, with some customers citing cost as a primary reason. This, despite the fact that Microsoft’s solutions may be bundled and hence perceived as free. In this case, integration and management costs and affiliated services are likely to dominate the TCO.

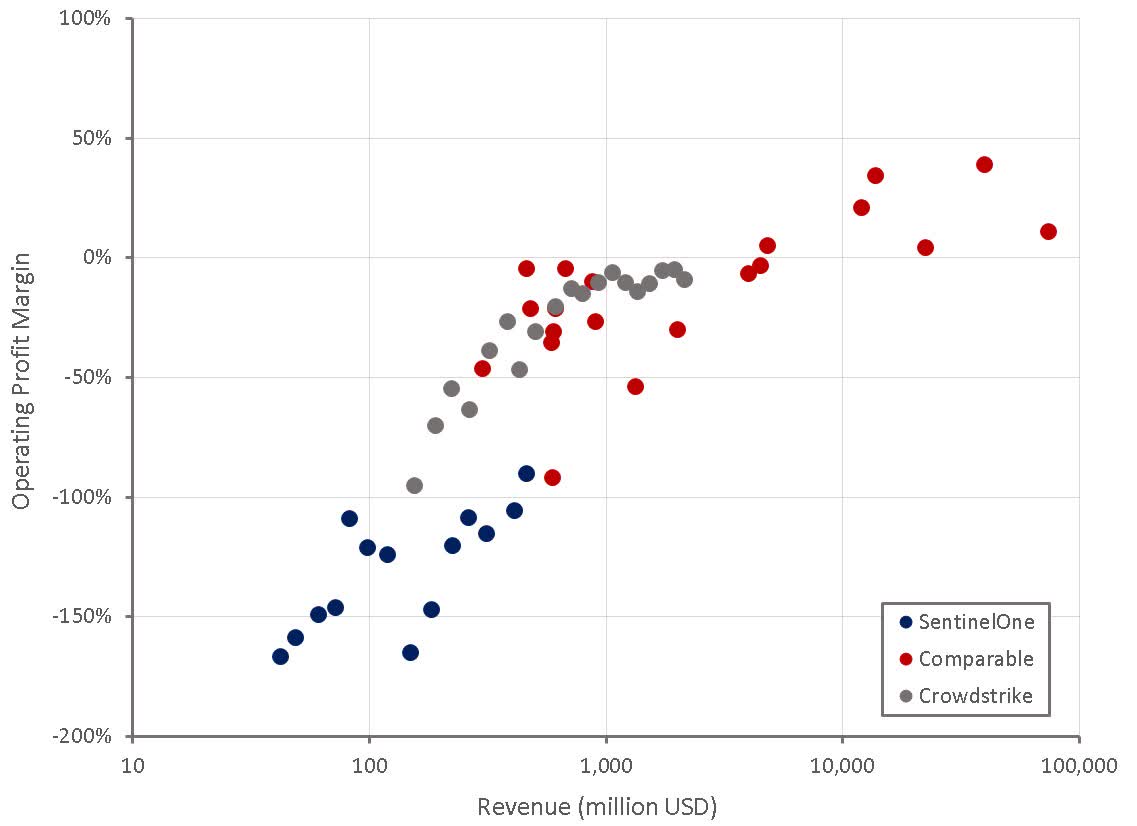

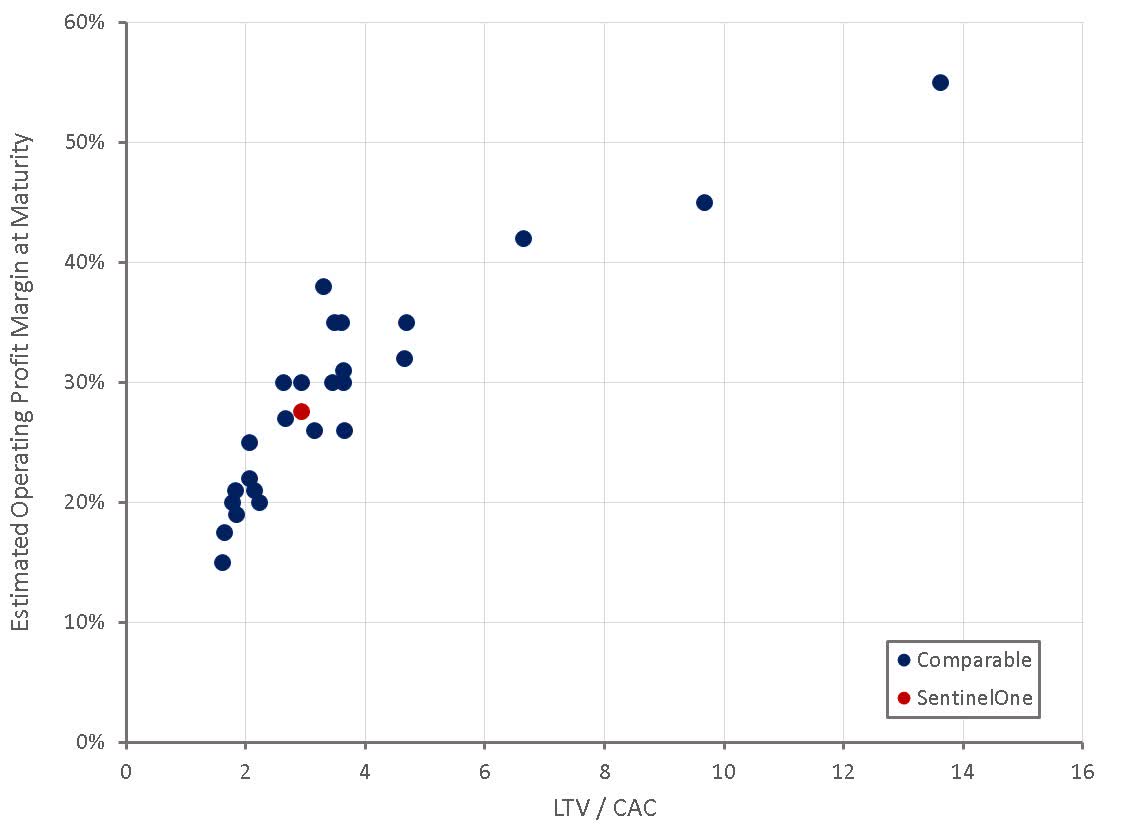

High win rates, along with low churn, will eventually translate to more reasonable sales and marketing expenses. This can be seen by looking at the LTV/CAC ratio and profitability of a range of software companies. While SentinelOne cannot currently be considered a top tier firm based on this metric, it should be able to achieve a solid level of profitability. There is also scope for this metric to improve as SentinelOne’s salesforce matures and SentinelOne continues to expand within its existing customer base.

Figure 10: SentinelOne LTV/CAC (source: Created by author using data from SentinelOne)

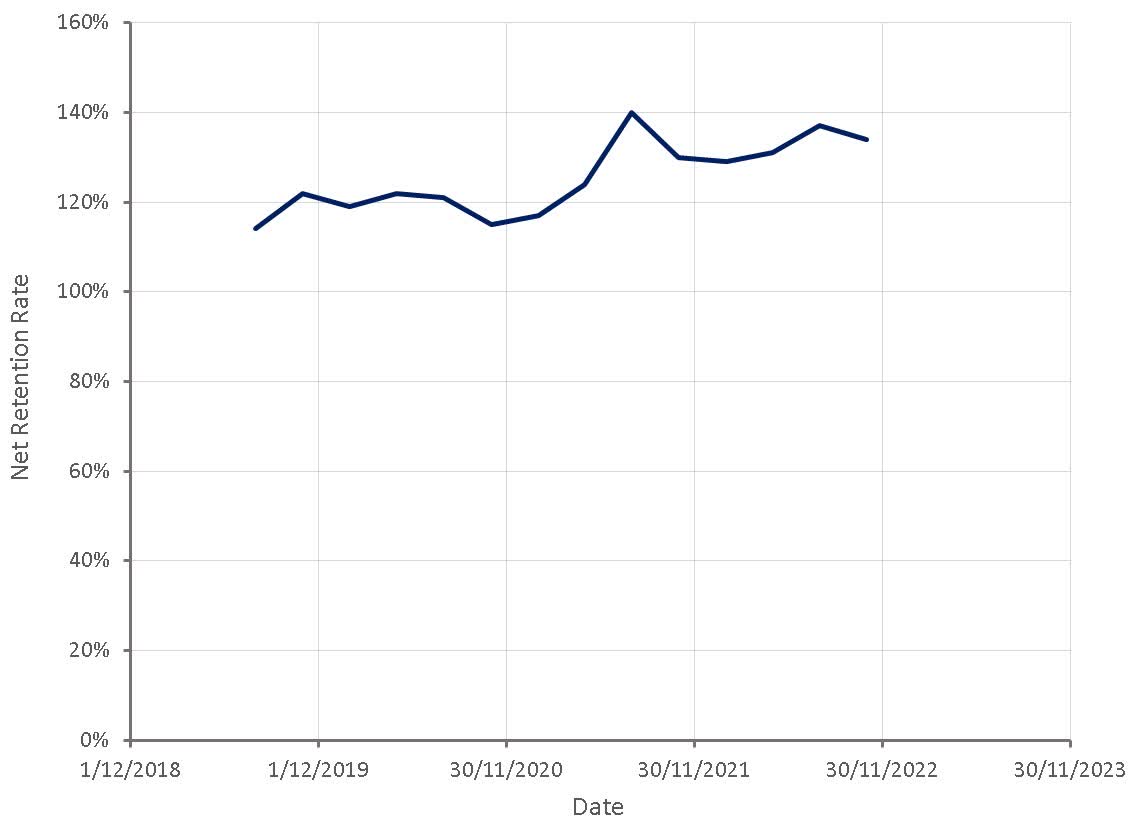

Figure 11: SentinelOne Net Retention Rate (source: Created by author using data from SentinelOne)

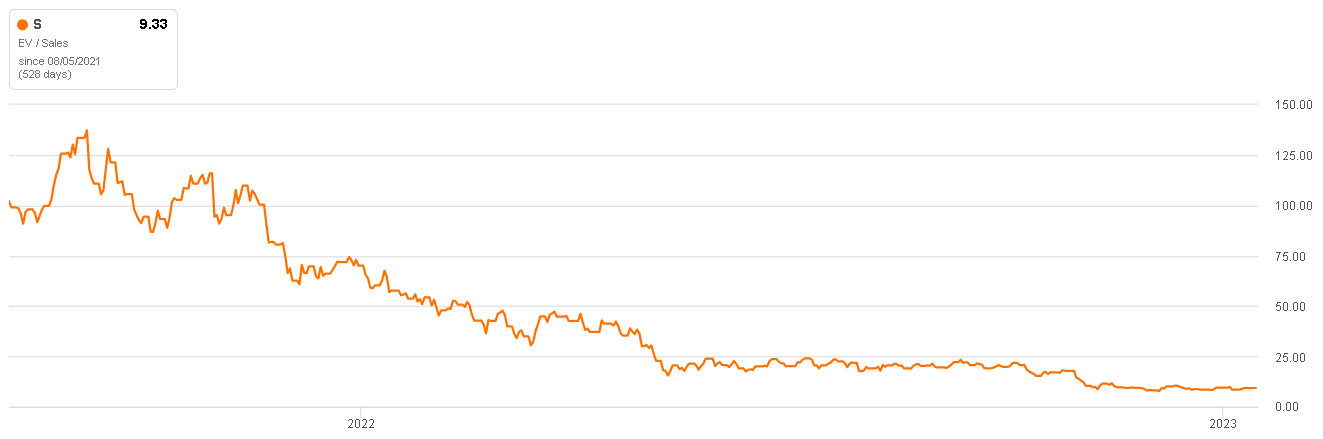

SentinelOne trades on a low revenue multiple given the company’s gross profit margins and growth rate. This stems from current investor demand for profitability, something that SentinelOne is still quite a long way from achieving. Despite this, the underlying unit economics of SentinelOne’s business are attractive and this will become more apparent as the business scales and growth moderates. While the short-term may remain volatile, it is likely that over a 5+ year time horizon SentinelOne’s share price moves significantly higher.

Figure 12: SentinelOne EV/S Multiple (source: Seeking Alpha)

Be the first to comment