PM Images

The recent sell-off in equities has crushed many small-cap companies due to their apparent risks and need for fundraising. Semler Scientific (NASDAQ:SMLR) has seen its stock’s value fall from about $150 per share in November of 2021 to around $30 per share. However, Semler is not exactly a highly speculative ticker that is deserving of this punishment considering it is profitable with a unique product that is in a niche market. I believe the market has taken the selling too far and is overlooking the company’s performance and the company’s intrinsic valuations. As a result, I am looking to find a spot for SMLR in my Compounding Healthcare “Bio Boom” Portfolio.

I intend to provide a brief background on Semler Scientific and its performance track record. In addition, I will point out my leading downside risk that investors should consider when managing their position. Finally, I present how I plan on accumulating SMLR and managing the position in the second half of 2022.

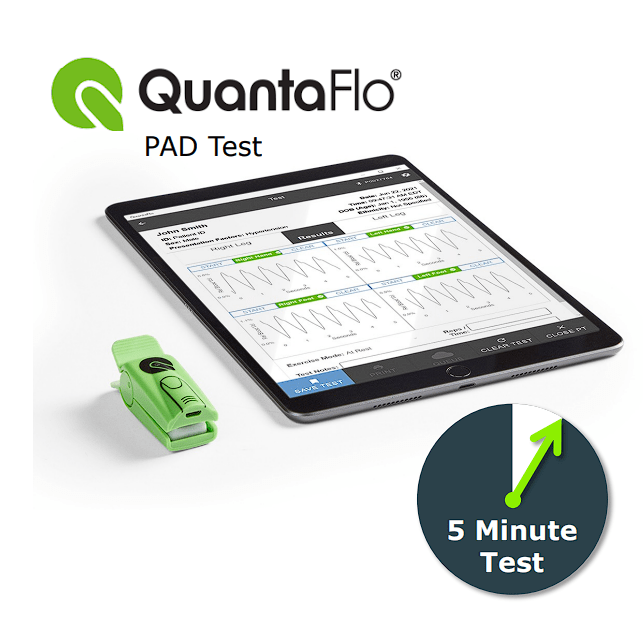

QuantaFlo Device (Semler Scientific)

Background on Semler Scientific

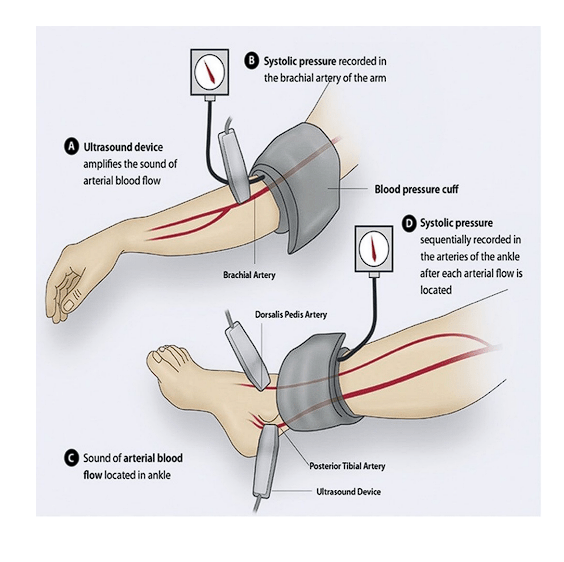

Semler Scientific offers medical devices and software that aid providers in diagnosing and evaluating chronic diseases. The company’s flagship product, QuantaFlo, is designed to measure arterial blood flow in the body’s extremities to help detect peripheral arterial disease (“PAD”), which is associated with heart failure, diabetes, and renal failure. QuantaFlo is suggested to be a significant upgrade from the old-fashioned test for PAD using the ankle-brachial index (“ABI”) method.

ABI Method (Semler Scientific)

This is because QuantaFlo is considered faster, cheaper, and does not require to be performed in a specialized setting. Instead, QuantaFlo allows the PAD test to be completed in a provider’s office.

Semler’s top commercial targets are insurance companies who are looking to reduce the risk of paying future acute care costs from heart attacks and strokes. So, insurers are happy to pay the healthcare providers to use QuantaFlo to test for PAD to potentially avoid bigger bills from more acute events. What is more, Semler employs a SaaS model where its customers have a subscription fee rather than having to buy the entire QuantaFlo product up front.

In terms of the size of the PAD market, the company stated that there are roughly 20M people in the U.S. who may have PAD. However, only 1M to 2M of these patients with PAD are being diagnosed in the conventional fashion, so roughly 75% of PAD patients are walking around asymptomatic, making PAD an immensely underdiagnosed condition. A simple 5-minute QuantaFlo test could change those statistics.

According to the company’s CEO, Doug Murphy-Chutorian, M.D., Semler’s aim is to get QuantaFlo up to the level of “the standard of care for testing multiple cardiovascular diseases, including peripheral arterial disease.” Furthermore, Semler is looking to expand QuantaFlo’s uses to help identify patients who could have “another underlying cardiovascular disease.” Obviously, expanding QuantaFlo’s uses to help diagnose other cardiovascular diseases will increase the device’s value and marketability.

Beyond QuantaFlo, the company is on the lookout for new products and services that can be beneficial to its expanding customer base. The company already has an agreement with Mellitus Health to market and distribute Insulin Insights in the U.S. and Puerto Rico. Insulin Insights is an FDA-cleared software that proposes optimum insulin dosing for diabetic patients. The company also made investments in Synaps Dx, which has Discern, a test for early Alzheimer’s disease. These products should complement QuantaFlo and diversify Semler’s portfolio.

Growth and Profitability

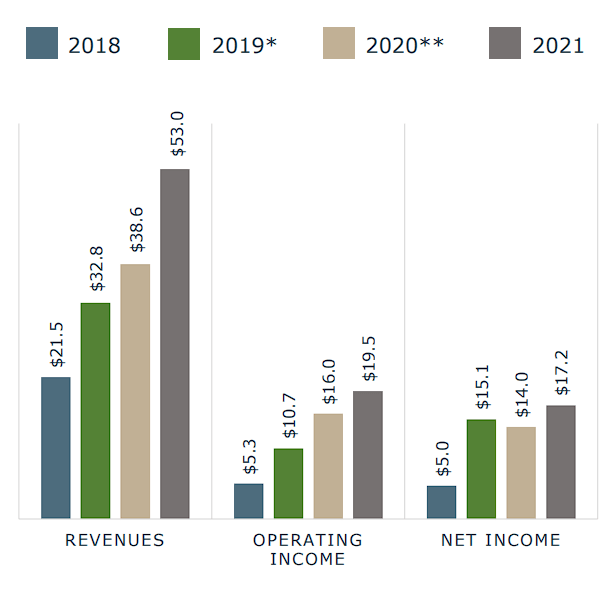

Semler is developing a nice track record of growth profitability, despite the COVID-19 pandemic. Furthermore, the company has reported a net income since Q4 of 2017.

Semler Financial Performance (Semler Scientific)

In Q1, Semler pulled in $14M in revenue up 6% from Q1 of 2021, marking another consecutive quarter of profitability since Q4 of 2017. Indeed, the company’s Q1 earnings revealed a miss on EPS and revenue thanks to “slower growth.” However, the company still reported growth and added to the bank account. As a result, the company’s cash position increased to $38.4M, and the company started a stock buyback program for “up to $20M.”

Looking ahead, the company expects to maintain profitability and generate cash for the remainder of 2022. In Q2, the company is projecting to report $14.2M-$15.2M in revenues. For the full year, Semler is projecting revenue to come in the range of $58M-$60M with OpEx coming in between $44M and $46M.

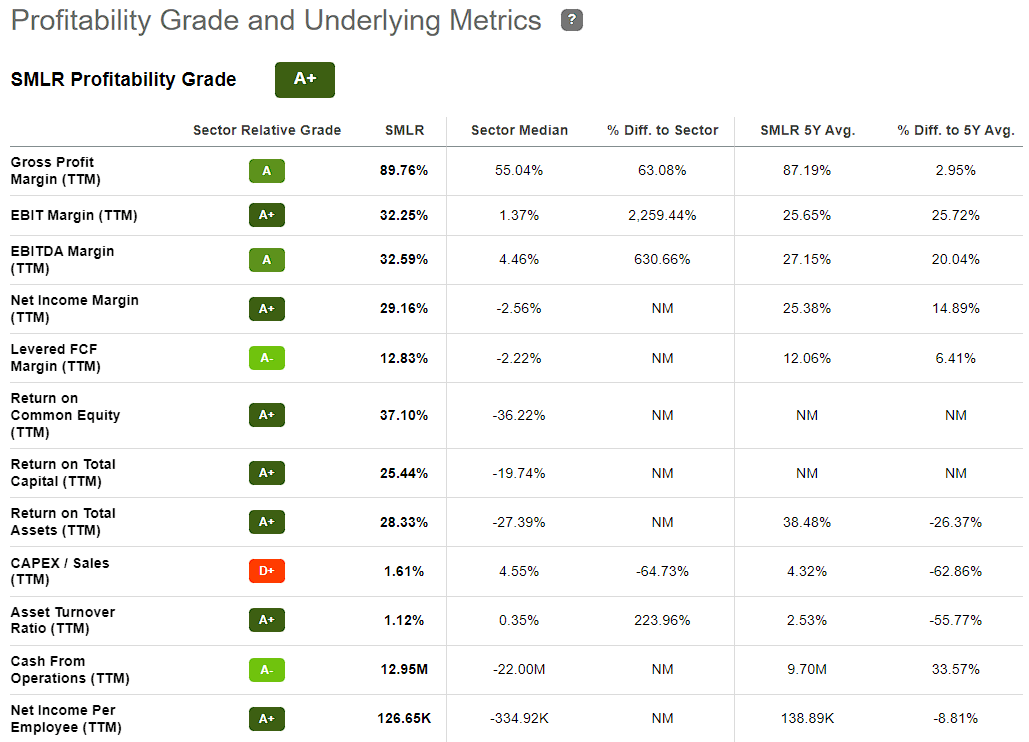

In terms of profitability, Semler has astounding profitability grades compared to the sector’s median. I would like to point out the company’s ~90% gross profit margin and the ~29% net income margin, which are attributable to the company’s decision to have a SaaS model.

SMLR Profitability Grades and Metrics (Seeking Alpha)

A Risk to Consider

Semler’s QuantaFlo is the modern PAD test on the market and could be seen as the standard of care. At this point in time, I don’t see any major contenders coming up behind QuantaFlo; however, some of QuantaFlo’s patents are valid until 2027, so it is possible we see some competition enter the arena in the coming years. Obviously, any competition could impede QuantaFlo’s growth and could have a negative impact on the share price as the market attempts to assess the threat. As a result, I give SMLR a conviction rating of 2 out of 5 at this point in time.

Calculating Intrinsic Valuation

After performing some basic valuation calculations, I have Semler’s DCF five-year growth exit at $89 and the ten-year is at $163.

DCF 5Y Growth Exit (Author Using Value Investing) DCF 10Y Growth Exit (Author Using Value Investing)

My DCF EBITDA five-year is $104 and the ten-year is at $183.

DCF EV/EBITDA 5Y (Author Value Investing) DCF EV/EBITDA 10Y (Author Using Value Investing)

For P/E Multiples, I used a trailing P/E of 17.5x and a forward P/E of 11.4x, which gave me a fair price of ~$40 for SMLR.

P/E Multiple (Author Using Value Investing)

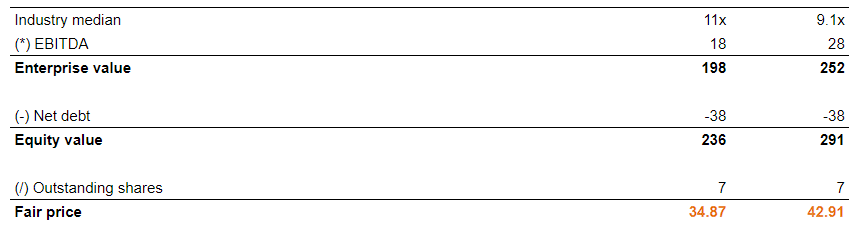

For EV/EBITDA, I used a trailing multiple of 11x and a forward multiple of 9.1x, which put SMLR’s fair price at ~$39.

EV/EBITDA (Author Using Value Investing)

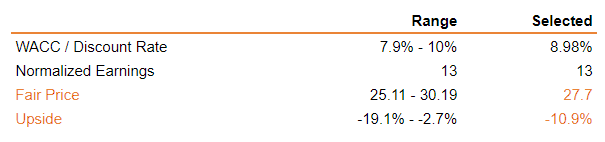

The only valuation that showed a downside was the earnings power value, which was ~$27.50 (-11%).

Earnings Power Value (Author Using Value Investing)

So, it appears SMLR is significantly undervalued based on multiple valuation models.

My Plan

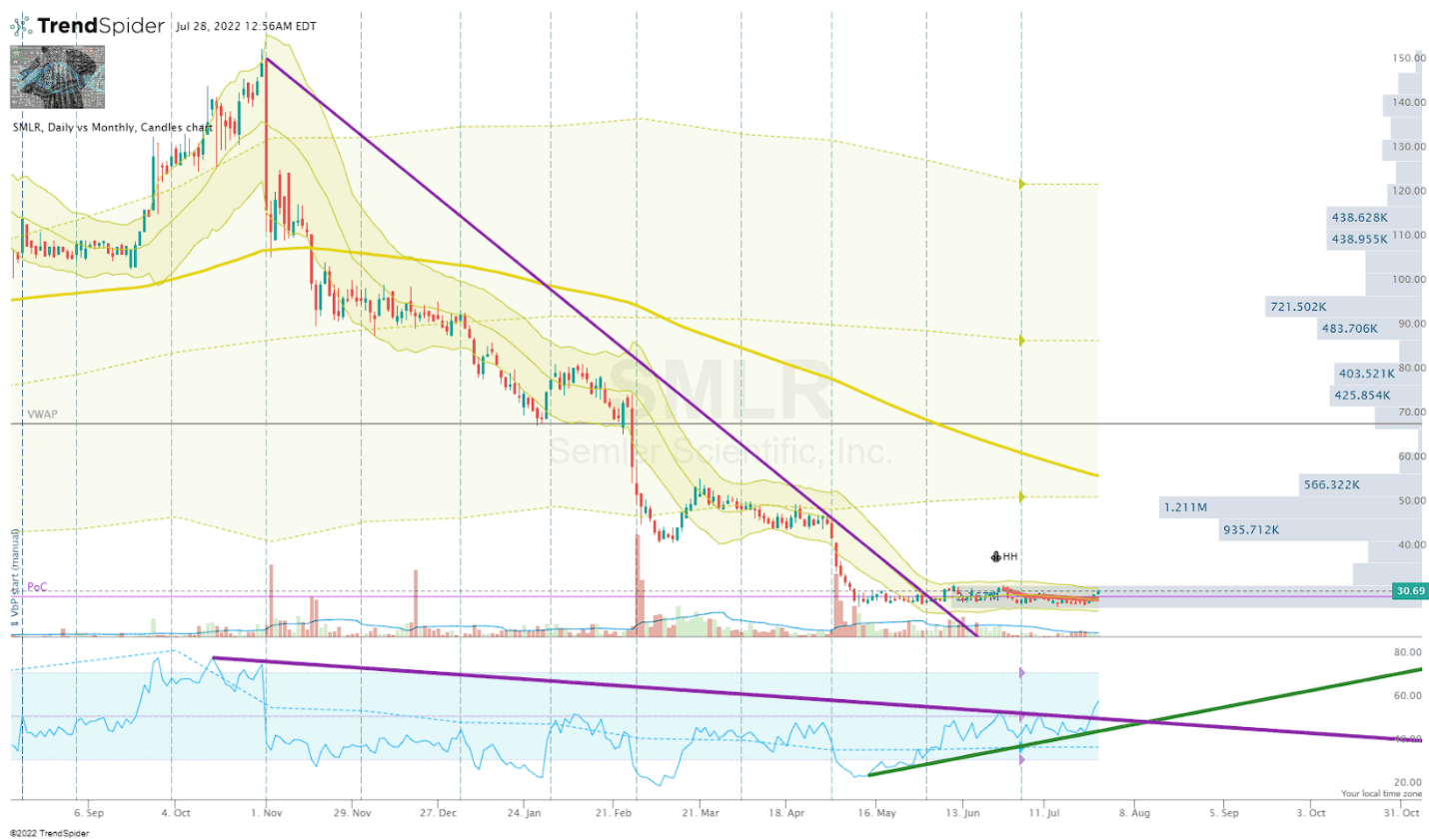

Semler’s QuantaFlo and the company’s distinctive distribution model have fueled growth and allowed the company to quickly move profitably. Even though there is a threat of new entrants impacting future revenues, QuantaFlo is becoming entrenched and could become the standard of care. Considering these items and the company’s intrinsic valuations, I am looking to initiate a starter position in SMLR in the near term to take advantage of this long base that started back in May.

SMLR Daily Chart (TrendSpider)

I have set some small buy orders around SMLR’s buy threshold of ~$31. After initiating a position, I will set additional buy orders to accumulate a position under $31 per share.

Once I have accumulated a respectable position, I will set sell orders in order to book some profits and get SMLR to a “house money” position. Long-term, I am expecting to maintain an SMLR position for at least five years in anticipation that the company will be able to find growth opportunities beyond QuantaFlo and/or the company will be acquired for a respectable valuation.

Be the first to comment