CloudVisual

Note:

I have previously covered Seanergy Maritime Holdings (NASDAQ:SHIP), so investors should view this as an update to my earlier articles on the company.

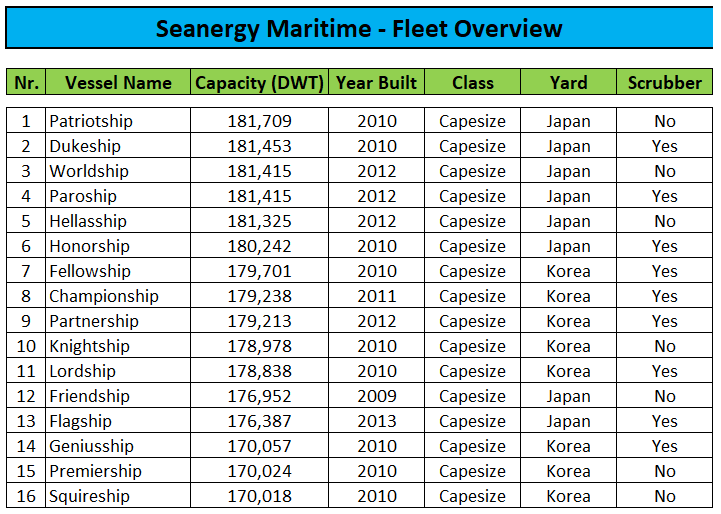

Earlier this week, Greece-based Capesize pure play Seanergy Maritime Holdings or “Seanergy” continued its recent fleet renewal efforts by acquiring the former Navios Obeliks, a 2012 Japanese-built, scrubber-fitted Capesize carrier at a gross purchase price of $31 million while dropping down its two oldest vessels Goodship and Tradership to recent spin-off United Maritime (USEA) or “United” at an aggregate sales price of $36.25 million thus effectively skimming most of the proceeds from United’s recent sale of a LR2 product tanker.

Management expects the disposals to result in a profit of more than $8 million which will be recognized in Q1.

The new vessel has been renamed Paroship and fixed on an up to twelve month index-linked time charter with a leading European operator.

The acquisition was funded through a combination of cash on hand and a new $16.5 million senior credit facility which bears interest of SOFR +2.90%.

Looking at individual vessel valuations provided my MarineTraffic.com (“MarineTraffic”), United Maritime appears to be overpaying by approximately 10% despite the purchase price having been agreed upon “the basis of the average of three independent broker valuations“. That said, at least from my experience, MarineTraffic valuations tend to be on the low side.

In the current environment, the trade-off makes perfect sense for Seanergy as the scrubber-fitted new vessel is likely to generate positive cash flow while the old Capesizes do not. In addition, operating expenses will be reduced.

Lastly, liquidity will be improved by an estimated $8 million after adjusting for the repayment of legacy debt related to Goodship and Tradership and the cash portion of the Paroship purchase price.

In total, nine out of sixteen vessels in the company’s fleet are now scrubber-fitted.

Company Press Releases

On the flip side, United Maritime shareholders appear to be on the receiving end of this deal with close to 95% of the proceeds from the recent sale of the LR2 product tanker Minoansea being skimmed by former parent Seanergy Maritime in exchange for two old and currently unprofitable bulk carriers.

That said, management has already shown its ability to time the market with United Maritime’s purchase of four Aframax / LR2 tankers in July for an aggregate consideration of $79.5 million. Over the past three months, the company has flipped three of the vessels for total sales proceeds of $101.5 million with the remaining LR2 product tanker Epanastasea carrying an estimated value of between $35 million and $40 million.

Given the requirement to drydock the Epanastasea for its upcoming special-survey and ballast-water treatment system installation later this year, I would expect United Maritime to sell its last remaining tanker sooner rather than later which would provide funds for additional vessel purchases from Seanergy or unaffiliated parties.

In addition, United Maritime likely received up to $26 million in cash proceeds from warrant exercises in the fourth quarter as holders scrambled to exercise their warrants ahead of the December 12 record date for the recently announced $1 special dividend.

At this point, I do not expect United Maritime to declare another surprise special dividend anytime soon or continue its aggressive share buyback program as the company will likely look to preserve funds for opportunistic dry bulk carrier acquisitions after the recent drop in second hand vessel values.

Bottom Line

Seanergy Maritime’s decision to replace two older vessels with a newer, scrubber-fitted Capesize carrier appears to be smart strategic move in the current market environment.

While the transaction should provide incremental liquidity and improved near-term cash flows, Q1 won’t be a great quarter for the company.

Based on current forward freight agreement (“FFA”) rates, Seanergy is likely to experience cash outflows in Q1 with only mild improvement in Q2.

Braemar Atlantic Securities

Highly speculative investors with some faith in management’s expectations for Capesize charter rates to recover sooner rather than later should consider scaling into Seanergy Maritime’s common shares at the current 60% discount to net asset value.

That said, the beaten-down share price very much reflects the poor charter rate environment and associated risks of a dividend cut and potential near-term reverse stock split.

At least spin-off United Maritime is apparently betting on a near-term market recovery and I firmly expect the company to sell its remaining product tanker and acquire additional dry bulk vessels in the not-too-distant future. After the recent setback, shares are trading at an estimated 55% discount to NAV.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment