FatCamera/E+ via Getty Images

Seagen Inc. (NASDAQ:SGEN) is a leader in the segment of biotech focusing on antibody-drug conjugates (ADCs) which bind on targeted proteins and receptors to destroy cancer cells while avoiding damage to healthy tissue. This is a field that has gained momentum through improving technology driving a growing number of FDA approvals in recent years, including several from Seagen.

We like the stock as a pure play on ADCs with the company benefiting from an expanding portfolio of first-in-class drugs covering advanced-stage lymphoma, urothelial, breast, and other cancers as a significant market opportunity. With accelerating sales this year following the launch of “TIVDAK” for the treatment of cervical cancer along with expected trial readouts over the next year, 2023 is shaping up to be a breakout year for the company. An outlook for sales to more than triple over the next five years and a shift towards profitability on the horizon highlights the attraction of SGEN.

Company IR

SGEN Key Metrics

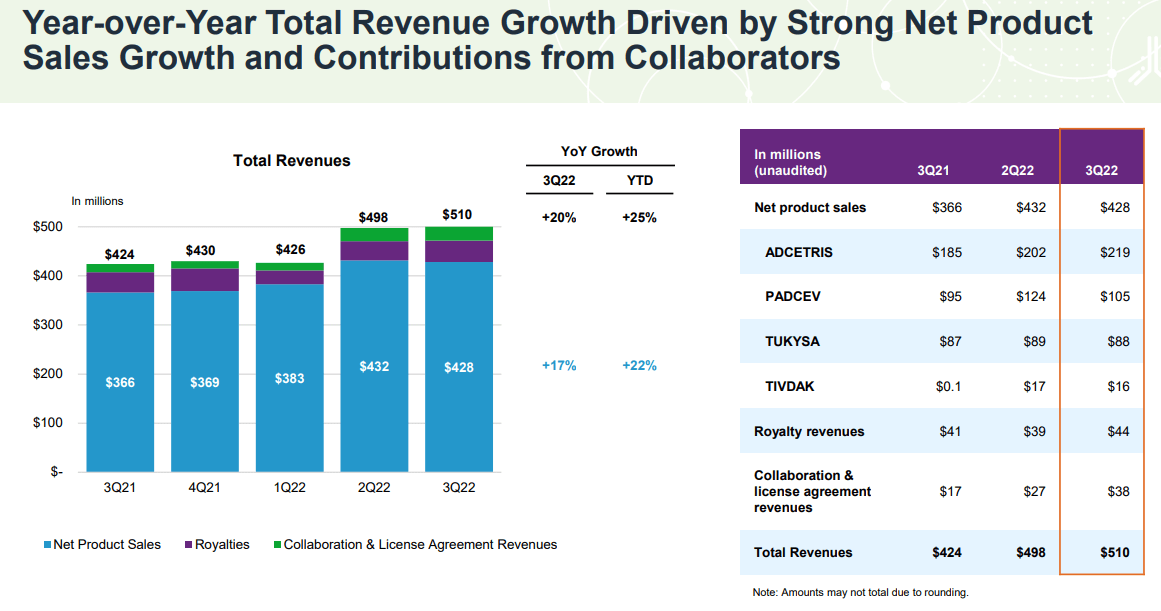

The company last reported its Q3 earnings back in October with a headline EPS loss of -$1.03, which was $0.07 below estimates. More favorably, revenue at $510.3 million, up 20.3% year-over-year came in $49 million above the consensus. Management explained the success in the quarter was driven by continued commercial execution as product sales climbed 17%, with strength in its “ADCETRIS” Hodgkin lymphoma therapy capturing increased diagnosis rates and higher average pricing.

TIVDAK, developed in collaboration with Genmab A/S (GMAB), was FDA-approved in Q3 2021 and generated $16 million in sales this last quarter adding to the top-line momentum. The urothelial cancer drug “PADCEV” saw strong growth with sales climbing by 20% on an adjusted basis, excluding a large clinical trial supply order in the comparison period.

This quarter, Seagen also saw higher royalty revenues and licensing fees as part of its global distribution strategy. Notably, a new collaboration agreement with Zai Lab Limited (ZLAB) is set to commercialize TIVDAK in China and related territories.

Company IR

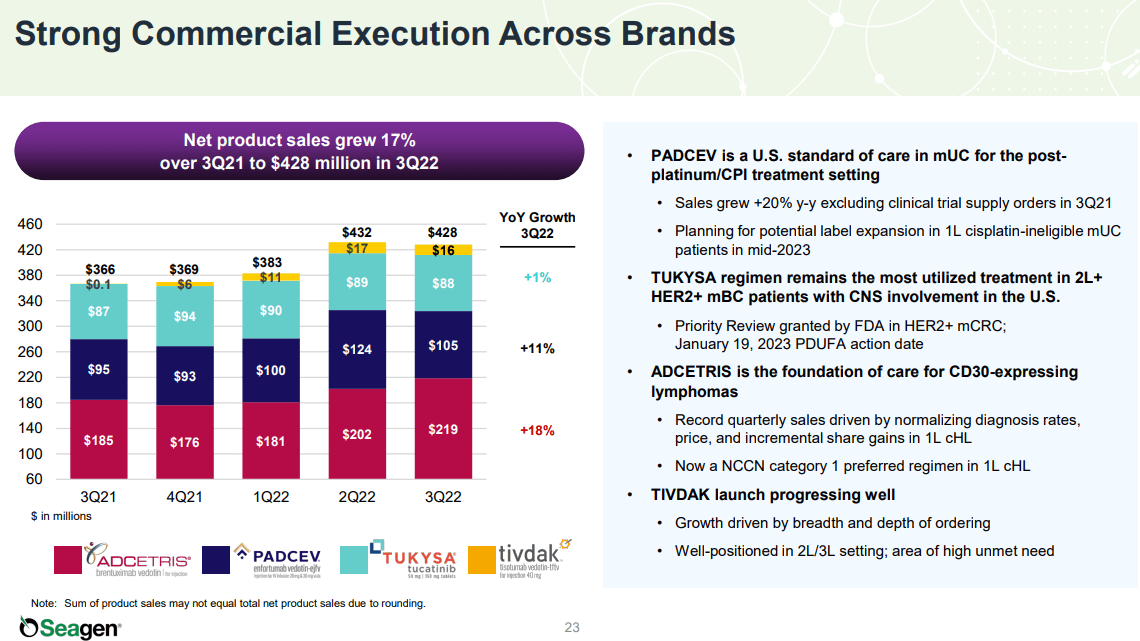

If there was a weak point this quarter, sales of “TUKYSA” as a tyrosine kinase inhibitor (TKI) for breast cancer have been flat, up just 1% y/y, which the company connects to “competitive dynamics” in its current indication. Even as the product remains the most utilized treatment for 2L+ HER2+ metastatic breast cancer with central nervous system involvement in the U.S., the recent approval of rival therapies has represented a headwind that management believes is only temporary.

An expectation for expanding TUKYSA sales in countries like Canada and Germany into Europe may add a resurgence of growth going forward. TUKYSA is also in stage 3 clinical trials for separate indications with an upcoming priority review action date in January as another growth opportunity.

Company IR

In terms of the financials, the growth along with moderating costs as a percentage of revenue has helped the operating loss narrow to -$193 million in Q3 from -$298 million in the period last year. This trend is expected to continue. The company ended the quarter with $1.8 billion in cash and equivalents against just $71 million in long-term debt. The understanding is that the liquidity profile is stable and adequate to fund growth for the foreseeable future

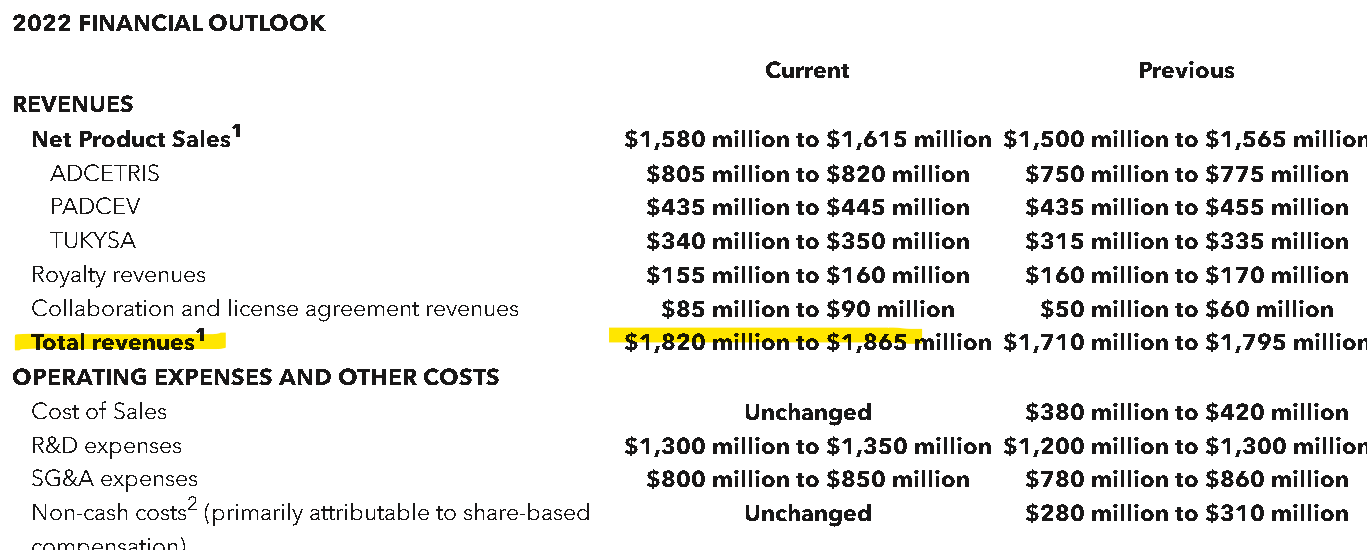

Favorably, management revised higher the full-year revenue target to a range between $1.82 billion and $1.87 billion compared to a prior midpoint estimate of $1.53 billion. The setup considers both the stronger Q3 product results with better than expected demand for its “ADCETRIS” and “TUKYSA” programs expected to maintain momentum in the yet-to-be-reported Q4 results and into 2023. The forecast for license agreement revenues was also bumped higher.

On the other hand, the outlook for royalty revenues narrowed, largely related to FX volatility through a partnership with Takeda Pharmaceutical Co. Ltd. (TAK) in Japan. An R&D deal with LAVA Therapeutics (LVTX) which included an upfront payment announced in September is reflected in higher expenses.

Overall, the tone during the earnings conference call projected optimism toward the several ongoing developments including ongoing trials, label expansion opportunities, and two pending FDA regulatory submissions. The expectation is that 2023 guidance is released with the Q4 results, likely coming in early February, although a date has not been set.

Company IR

What’s Next for SGEN?

We touched on what is an exciting group of ADCs as independent programs that are already on the market. The strong point here is that these therapies have all been recognized as effective and safe for their core indications, which bodes well for the label expansion.

With ADCETRIS, for example, beyond the current foundation care for CD30 expressing lymphomas, ongoing trials including pediatric Hodgkin lymphoma, non-Hodgkin lymphoma, post-Parkinsons disease, and even HIV are being studied. Indeed, the latest update has been data from a phase 2 trial in combination with Bristol-Myers Squibb’s (BMY) “Opdivo” reaching the desired endpoint with an overall response rate of 93% in patients with advanced-stage disease.

PADCEV is particularly promising as monotherapy for different cancers. There is also a broader portfolio of separate ADC technologies and sugar-engineered antibody platforms in development. Several readouts are expected into 2023 as potential catalysts for the stocks.

Company IR

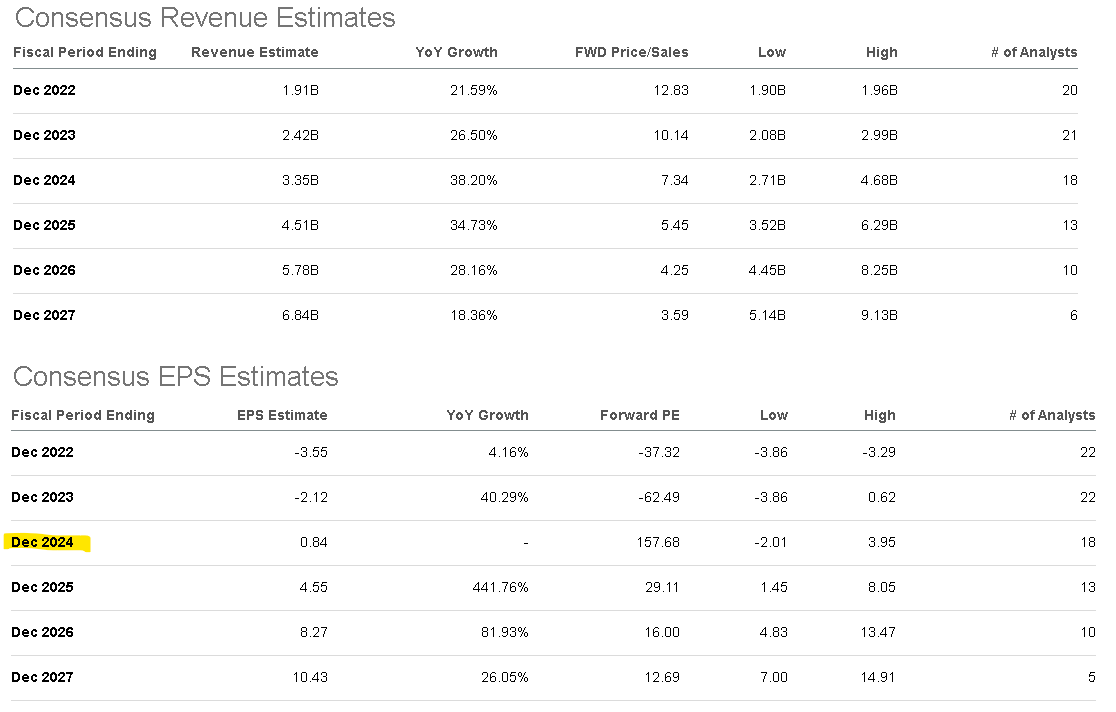

The result here is a very impressive outlook, where the current market consensus is for growth to average nearly 30% per year through fiscal 2027 as the company continues to execute the clinical development and commercialization strategy. From the market forecast of Seagen reaching $1.9b million in sales this year, that top-line is expected to more than triple towards $6.8 billion over the next five years.

What also stands out to us is that compared to a forecasted negative EPS of -$3.55 for the full-year 2022, the market sees the loss narrowing to -$2.12 in 2023 and ultimately turning positive towards $0.84 by 2024. This is particularly significant as it is based on the average earnings forecast by 18 Wall Street analysts, which further accelerates to an EPS of $4.55 by 2025.

Seeking Alpha

SGEN is effectively trading at a 3-year forward P/E of 29x on the consensus 2024 EPS, which is particularly compelling considering its underlying growth momentum. Investors would be hard-pressed to find a comparable established large-cap corporation in any sector with this type of runway over the next decade.

That being said, the big caveat is that the above forecasts face several uncertainties, between both the drug approvals timeline and reception at commercialization. There is a thought that the estimates could be too optimistic regarding the addressable market for some of the key drugs down the line.

SGEN competitors between Daiichi Sankyo (OTCPK:DSKYF) (OTCPK:DSNKY), which partners with AstraZeneca (AZN), ADC Therapeutics SA (ADCT), Mersana Therapeutics, Inc. (MRSN), along with larger players like AbbVie Inc. (ABBV), Roche Holding AG (OTCQX:RHHBF), and even Gilead Sciences, Inc. (GILD) all have ADC programs with potentially rival alternatives.

The point here is to say that SGEN is very promising, but the next step where it can potentially transform into a business that generates consistent positive cash flows will be critical to secure its long-term outlook.

SGEN Stock Price Forecast

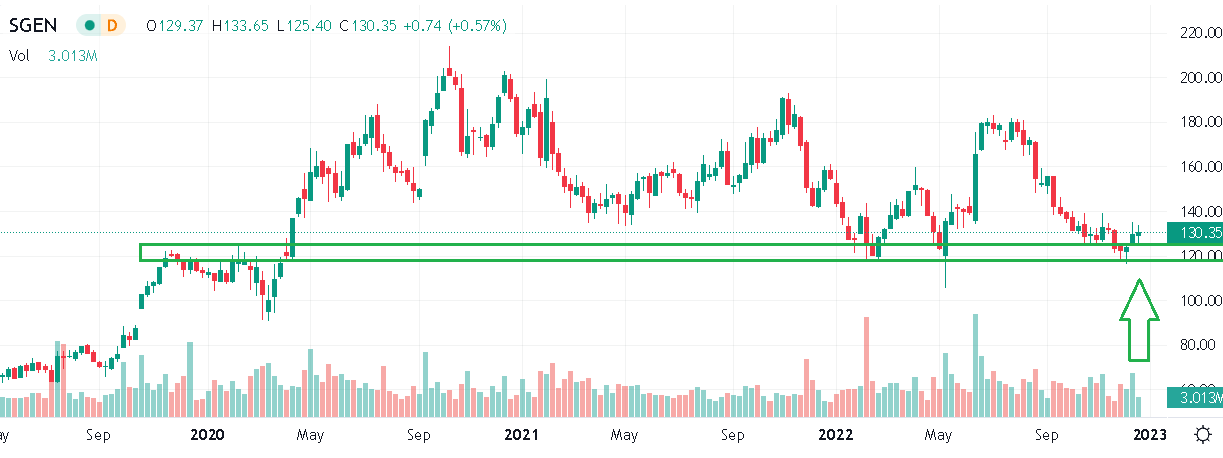

In our view, SGEN is a high-quality biotech that is likely still in the early stages of reaching its potential in terms of developing novel therapeutics. Shares have been under pressure all year amid the broader market volatility. There was talk back in Q2 of a potential buyout from Merck & Co., Inc. (MRK) that sent shares towards $180 as a takeover price. With the deal not going through likely based on a disagreement over price, SGEN is now trading back to near lows of the year and levels from pre-pandemic early 2020.

All things consider beyond the macro headwinds, the argument we make is that the company’s outlook is stronger than ever while shares have been excessively discounted against the weakness in the biotech industry performance. Considering a current market value sitting around $25 billion trading at a forward sales multiple approaching 10x has not been this “cheap” at any time over the past decade.

Ultimately, we expect the stock to trade higher going forward, with further progress in the clinical development program over the coming months helping to turn sentiment more positive. We mentioned risks, and it’s clear that companies involved with cancer drugs are inherently speculative. Any setback from ongoing clinical trials, or trends suggesting the path to profitability will get pushed back, are the biggest risks to watch that will likely keep shares volatile.

Seeking Alpha

Be the first to comment