Somrerk Kosolwitthayanant

Investment Thesis

SeaBank is Sea Limited’s (NYSE:SE) finance arm that is growing its credit business very quickly and has already booked net profitability since Jan 2022. During the last 3Q22 earnings call, management hinted to secure third-party financing, which not only allows management to reduce the capital needed in the business but to also scale its lending. Additionally, I also talked about how Sea Limited is in an enviable position to attain profitability while its peer, GoTo is still struggling. If you have not dived into my most recent analysis of its 3Q22 result, do head over here.

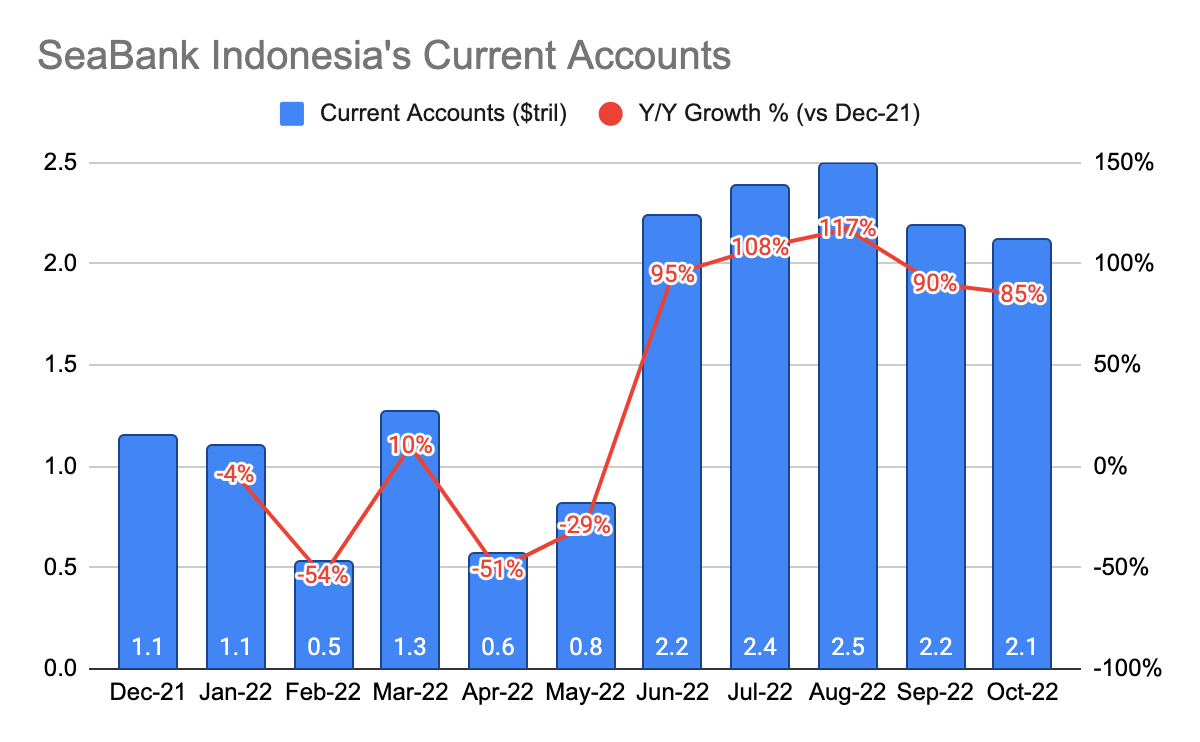

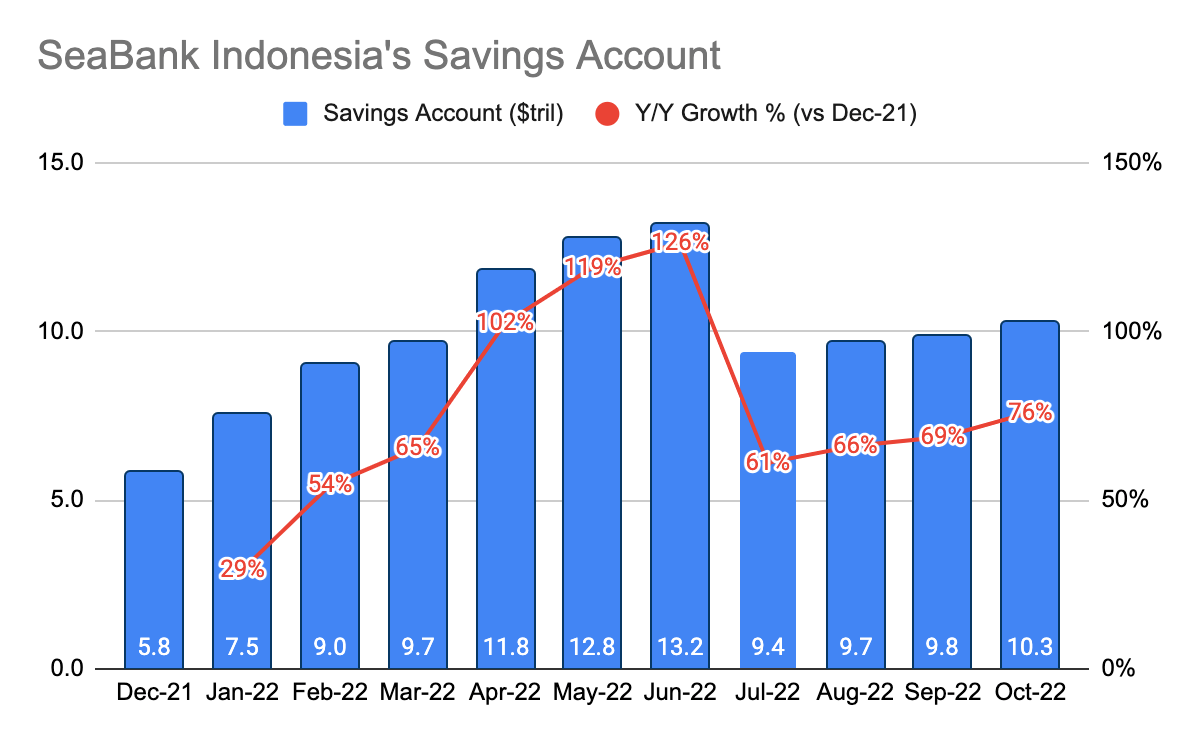

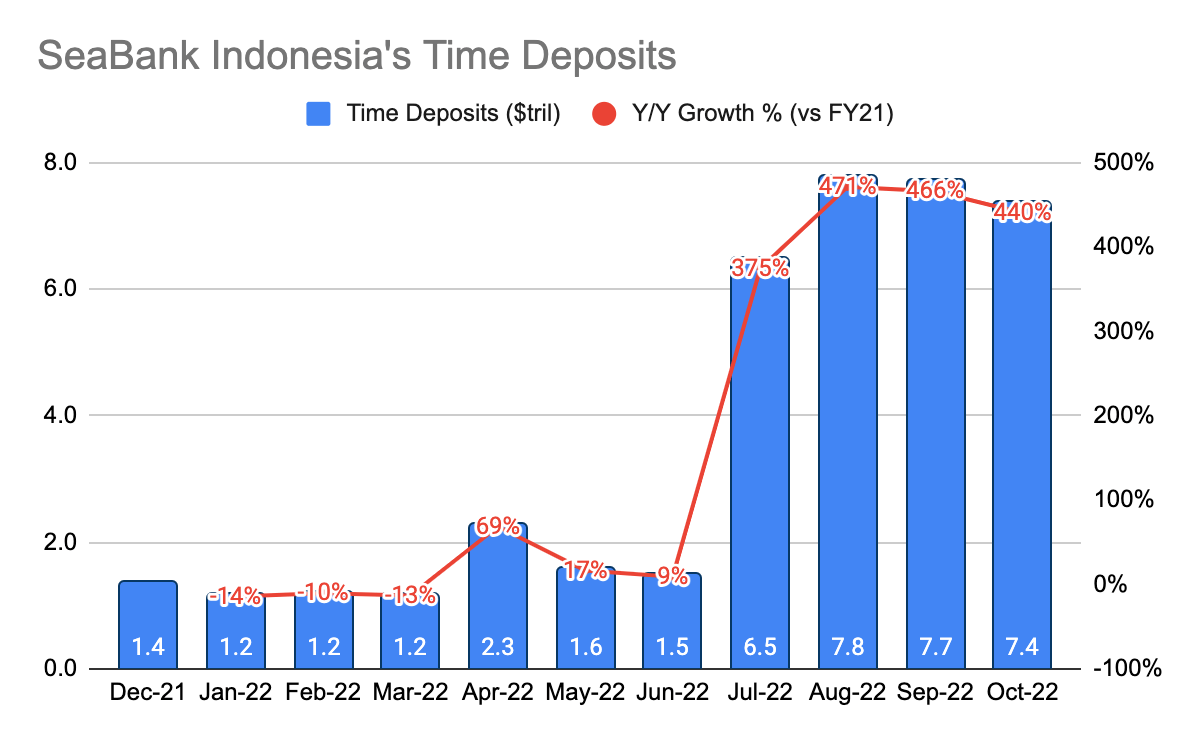

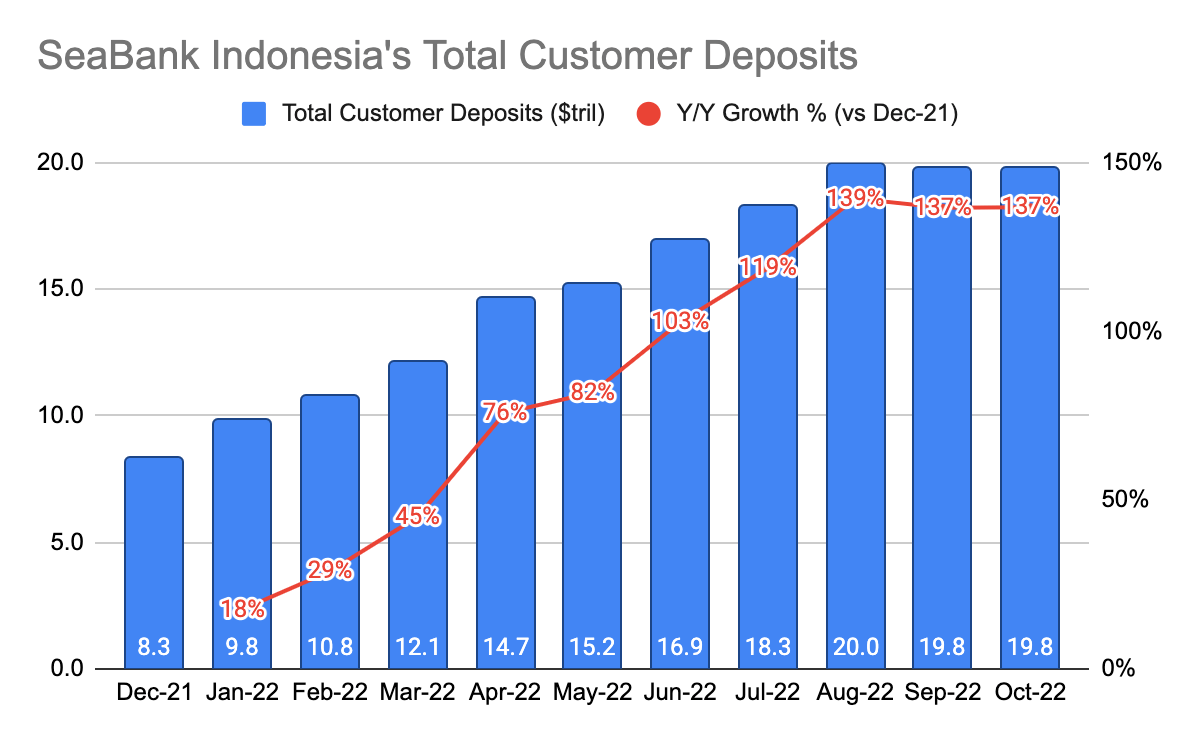

Customer Deposits

SeaBank ID Monthly Financial Statements SeaBank ID Monthly Financial Statements SeaBank ID Monthly Financial Statements SeaBank ID Monthly Financial Statements

On Oct 22, its current accounts, savings account, and time deposits grew 85%, 76%, and 440%, respectively, on a Y/Y basis. Its total customer deposits grew 137% Y/Y, which is flat from the previous quarter.

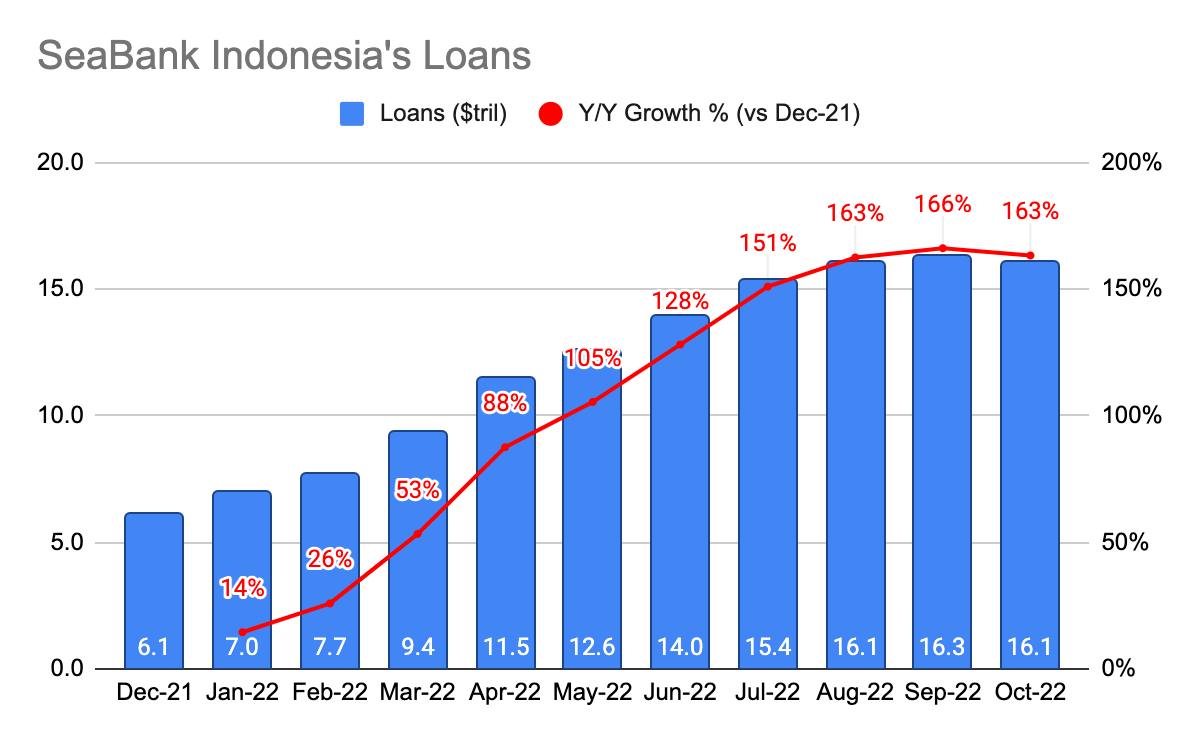

Growing Loans

SeaBank ID Monthly Financial Statements

On the other hand, its total loans have been accelerating from 14% Y/Y on Jan 22 to over 163% Y/Y on Oct 22. We’ve seen how quickly its loans have been growing, and I believe securing third-party financing will be able to scale its loans and deposits over time. Most recently, SeaMoney struck a partnership with CIMB Bank PH to onboard 2.5 million BNPL users in 2023, which is double that of the current SeaMoney user base of 1.3 million.

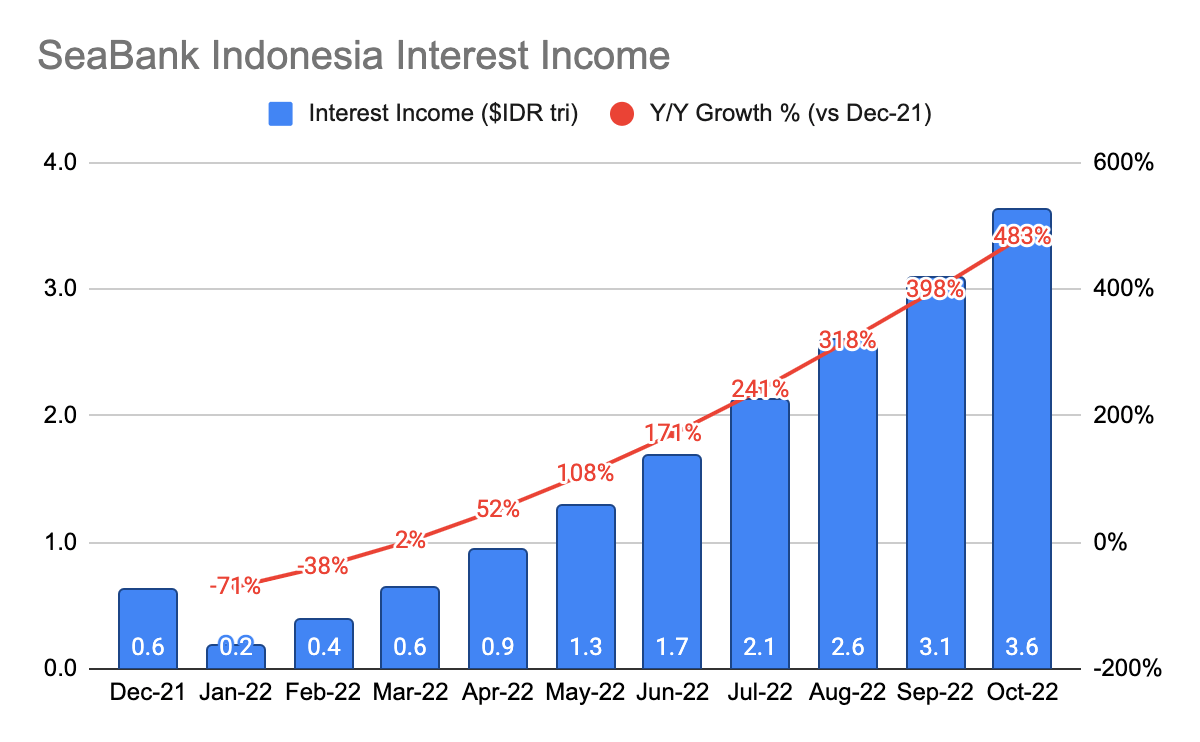

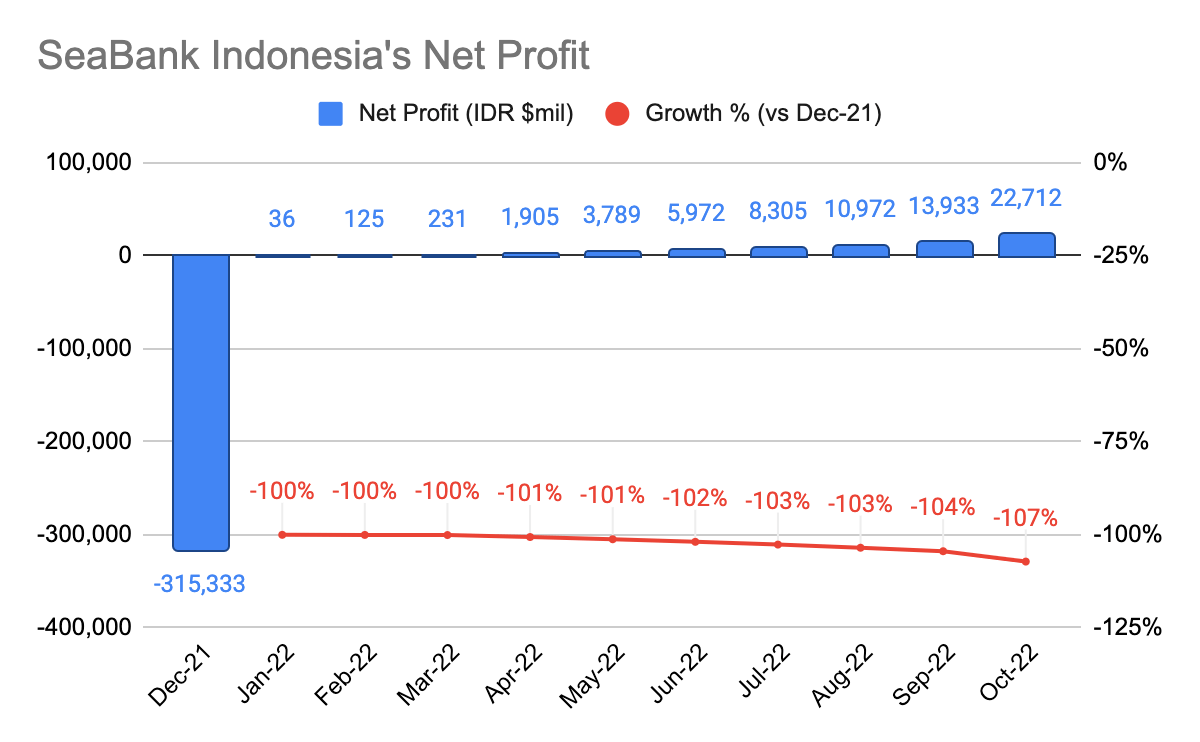

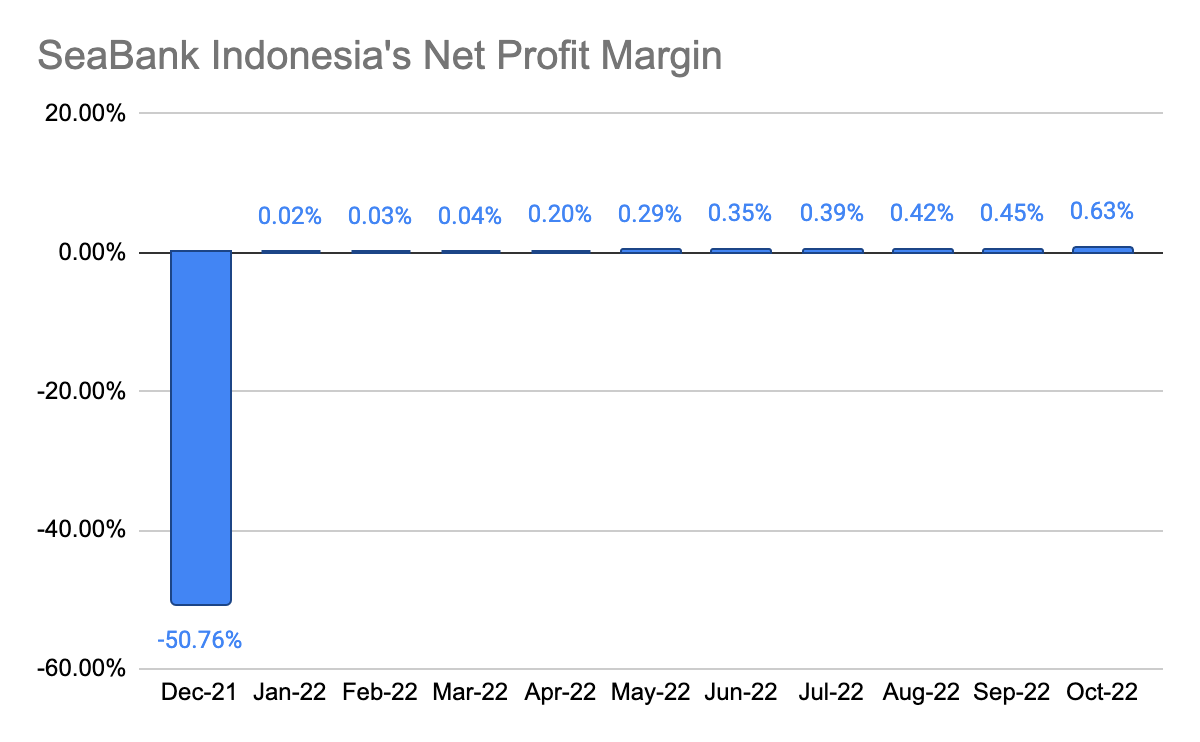

Accelerating Interest Income With Expanding Margins

SeaBank ID Monthly Financial Statements SeaBank ID Monthly Financial Statements SeaBank ID Monthly Financial Statements

Driven by increasing loans and customer deposits, its interest income (aka revenue) grew 483% Y/Y to $IDR 3.6 trillion while its net profit grew 107% Y/Y to $IDR $22 billion. Net profit margin expanded to 0.63% from 0.45% in Sep 2022.

GoTo 3Q22 Press Release

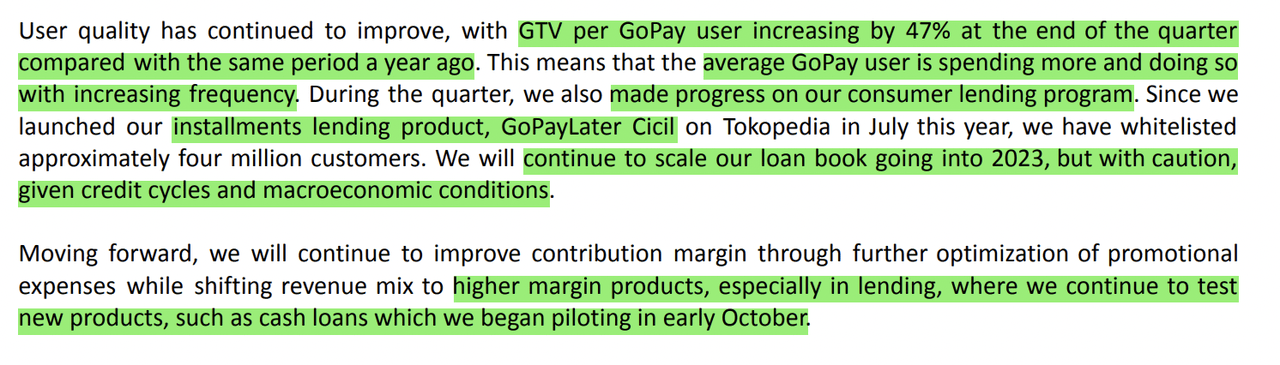

This shows how accretive the high-margin, lending business is, and the focus on self-sufficiency moving forward is going to place further emphasis on scaling its credit business. During GoTo’s (IDX: GOTO) 3Q22 earnings, management is also placing emphasis on scaling its lending business, with the launch of its installment program in July 2022 and cash loans in early October.

Sea Limited Profitability Versus Peers

GoTo 3Q22 Press Release Alibaba 3Q22 Investor Presentation

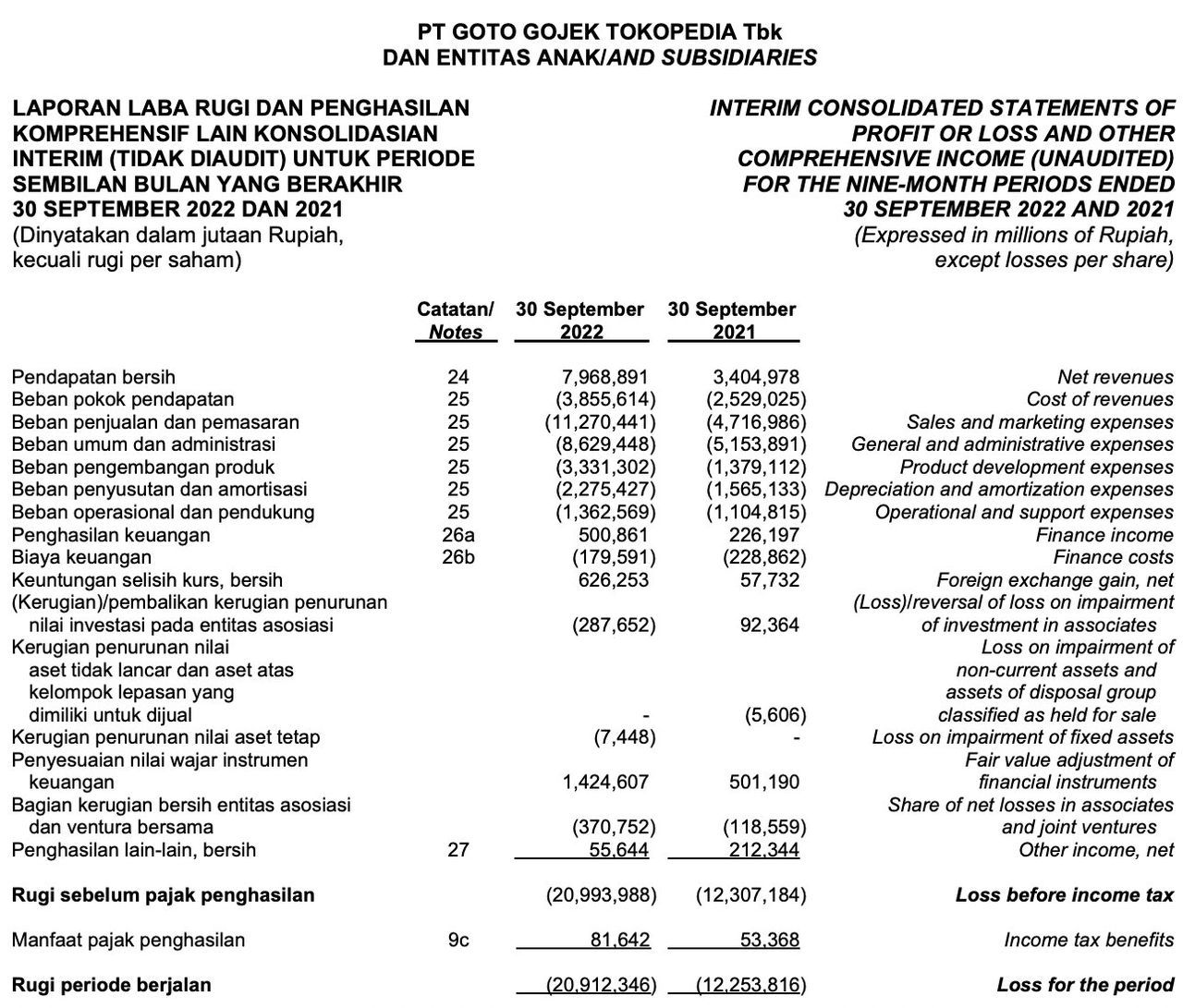

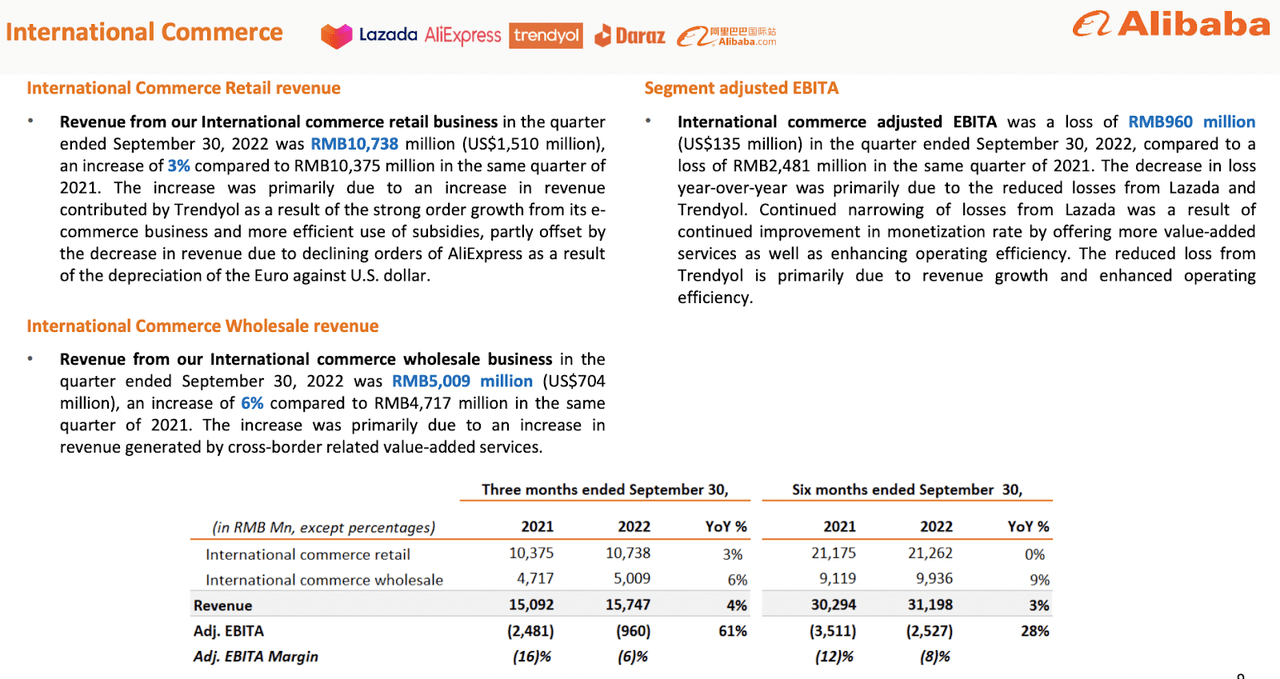

As of 3Q22, Sea Limited’s net margin is -18% as compared to GoTo’s net margin of -262%. We see that GoTo is still struggling to attain profitability given its huge operating losses, while Sea Limited is in an enviable position to hit profitability. Whereas, Alibaba’s international commerce’s adjusted EBITDA margin is 6% for 2Q22 as compared to Shopee’s net margin of -30% in 3Q22. While Lazada does not break down its adjusted EBITDA, I believe its losses are much higher given that the 6% margin is a consolidated figure and Shopee’s losses are also driven by Shopee Brazil.

While SeaBank has continued to grow strongly as it is still relatively early in its lifecycle, I still believe that the bigger thesis still lies on Shopee and the focus should be on seeing improved profitability moving forward. A question that I have in mind, though, is that given Shopee’s increasingly saturated market share in Southeast Asia, exit from multiple markets, and macro, how does Shopee intend to grow?

Conclusion

The continued strong growth in Oct 2022 is not surprising, and there weren’t many surprises during the month. Net profit margin has continued to expand, showing that operating leverage is starting to kick in. By securing third-party financing and launching its credit business in Brazil, I believe its loans and customer deposits can further scale. Additionally, I also did a comparison of Sea Limited’s profitability against its peers.

What are your thoughts on SeaBank Indonesia and the company in general so far? Let me know in the comment section below.

Be the first to comment