macbaszii/iStock via Getty Images

With the developed economies slamming the brakes on growth with sharp interest rate increases, 2023 may be a year to look further afield for strong returns. Likewise, big gains in the U.S. dollar may also be coming to an end and foreign investment may start to cash out on their American-based stocks. With a possible end to Covid policies in China and strong growth projected for the country, I am looking at Sea Limited (NYSE:SE) to get back to growth with a stronger balance sheet.

Sea releases third-quarter earnings results

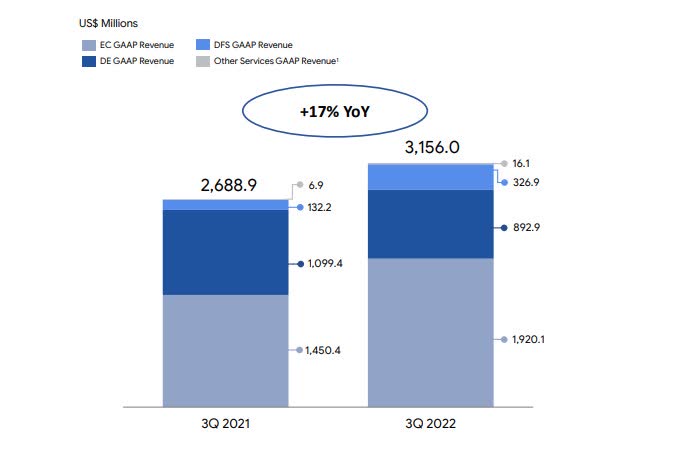

Sea Ltd. Released its third-quarter earnings results in November 2022 and the Singapore-based entertainment firm saw its total GAAP revenue increase by 17% year-over-year. That was a good performance in a tough macroeconomic environment and sets the stage for better days ahead.

GAAP Revenues (Sea Limited)

Sea was a darling technology stock that shrugged off the pandemic market turmoil with a move from around $40 at the start of 2020, to highs of $372 before the tech bubble burst in 2021. The recent collapse in the share price to $52.40 is an opportunity for investors and probably a blessing in disguise for the company. Having ridden the wave of lofty tech valuations in the low-interest rate environment, investors now have to look for real growth. This is something that Sea’s management understands and they will have different ideas on how the business moves forward.

Founder and Chief Executive, Forrest Li, said on the November earnings call:

Given the uncertainties in the macro environment, we have shifted our mindset and focus from growth to achieving self-sufficiency and profitability as soon as possible, without relying on external funding. We are adapting quickly to the changing climate because we believe that companies that fail to do so may not survive.

All our efforts are directed to ensure that Sea not only survives the macro storms but emerges stronger, more efficient, and more resilient – and as a long-term winner in our markets. This positions us to continue capturing the long-term potential of our businesses and markets, and to deliver strong and sustained shareholder returns over time.

The executive team also made a bold statement by refusing to take compensation until the company is self-sufficient.

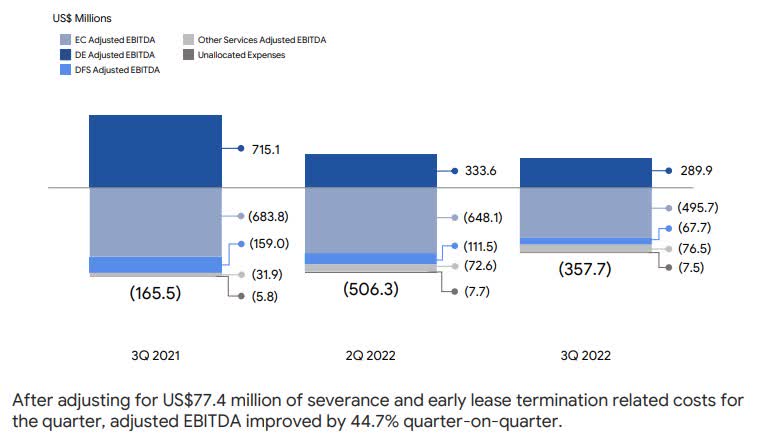

In the earnings report, it was also noted that adjusted EBITDA for the group improved by 29% quarter-on-quarter.

EBITDA (Sea Limited)

This was attributed to better profitability from the e-commerce and digital financial services businesses and included $77.4M of severance costs. The company is committed to maintaining a strong cash position and although it has declined from $11.8 billion since the market peak, the current $7.3 billion in cash gives a lot of room to maneuver.

Finally, the CEO said that the company, “took decisive actions to improve margins, and set clear goals and priorities for the quarters to come.”

Net Profit Margin (Sea Limited)

Margins have already been improving since 2018 but the market slowdown has seen net margins plateau around the -22% level. With the current cost-cutting actions, a return to economic growth in Asia could see those margins rocket higher from this base.

A look at the current business segment performance

Shopee is the company’s e-commerce platform and in 2021 it was the largest in South-East Asia with 343 million monthly visitors. The platform has had to face job cuts in 2022 due to the macroeconomic environment. The company is not yet profitable but saw a year-on-year boost to gross profit margins in 2022, due to growth in transaction fees and advertising income.

However, rising inflation and interest rates coupled with setbacks on its path to global expansion saw staff cuts in June 2022, including employees from Indonesia, Thailand, and Vietnam. Another round of job cuts was announced by the CEO in September 2022 with the leader citing the cost-cutting measures and the road to “self-sufficiency”.

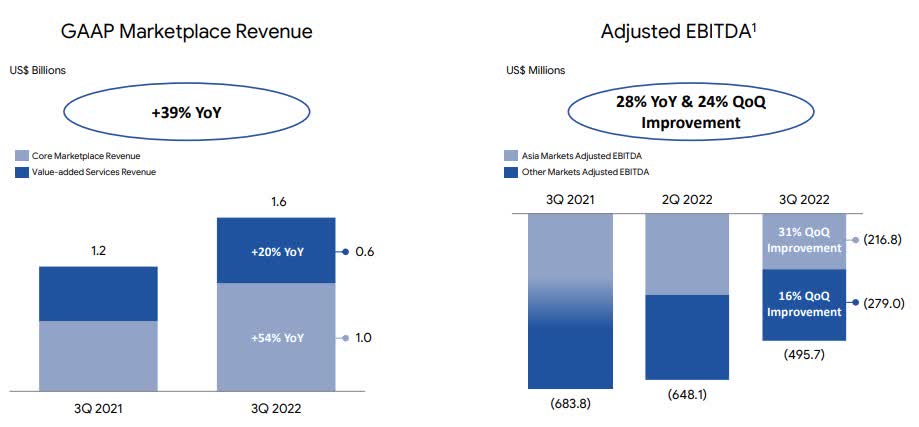

Revenue and EBITDA (Shopee)

Despite the tough environment, Shopee recorded a 39% y-o-y increase in marketplace revenue and also cut its EBITDA loss from $683M in Q3 2021 to $495M a year later. The company noted that Shopee’s GAAP sales and marketing expenses in the third quarter decreased by 15% quarter-on-quarter, due to free shipping adjustments so there is further improvement ahead.

Garena is the digital entertainment arm of Sea Limited and is involved in video game development and e-sports. This segment has seen a decline in users since Q3 2021 of around 160M. The Garena numbers had actually been bloated by the pandemic lockdowns as gamers were unable to attend work or school and had more time to spend on the platform.

Once again, the Chief Executive and management have learned from the new normal and said:

“Looking ahead, we will focus on stabilizing our large, existing franchises while selectively launching new games, and investing in our pipeline with greater discipline and a stronger focus on efficiency and returns.”

Finally, the Sea Money segment is the digital financial services arm and it has seen 147% growth in revenues year-over-year. GAAP revenue grew from $132M to $326M. The adjusted EBITDA loss decreased by 57% year-on-year to only 68 million dollars. The improvement was driven, “by more targeted sales and marketing spending for the mobile wallet business, and our credit business maintaining its healthy profitability while generating cash for the group.”

It should also be noted that R&D expenses rose for the year from $231M to $421M, while Cost of Revenue and G&A expenses were also higher. Therefore, the company is closer to its self-sufficiency goals than the top-line numbers suggest.

Valuations, macro outlook, and risks in Sea Limited

The current market valuation of Sea Limited is $26.4bn, which is down from the high of over $190bn in January 2022. That provides investors with an 86% discount on the year in a stock that is still growing revenues and is adjusting the business model towards profitability. The current price/sales ratio is 2.16x sales and investors were happy to pay over 20x sales throughout 2021.The key for investors is that Asia is set to outperform the U.S. and Europe this year and organic growth can be the fuel for a rally in Sea. Christian Mueller-Glissmann and Cecilia Mariotti at Goldman Sachs said last month that they see a 39% probability of a US growth slowdown in the next 12 months, however, risk assets were only pricing in an 11% chance.

Morgan Stanley analysts are overweight on Asian emerging-market stocks versus developed markets as they’re “more confident that a new bull cycle is beginning.” Nomura Holdings analysts said that the expected recessions in the West will allow Asia to outperform as stocks there provide cheaper valuations and a better fundamental outlook.

For China, Goldman Sachs sees potential growth of 4.5% in 2023, compared to 3.3% in 2022. Meanwhile, Morgan Stanley estimates the GDP growth to be 5.4% in 2023. China’s economy is a growth engine for the rest of Asia and that could be a big driver of growth for Sea Ltd. In 2023.

The risks to the bullish thesis in Sea revolve around that same macroeconomic environment and the continuing Covid policies. A recent surge in cases is not helpful but the Chinses stock market is showing resiliency, hinting that traders see an end to the aggressive lockdowns.

On the business side, Sea is over-reliant on a small number of business segments, and they need to make adjustments to the gaming and entertainment division to drive more profitability. The financial services arm is showing strong growth potential and could soon match the revenues of Garena if it continues on its current growth trajectory.

Finally, the Shopee e-commerce arm has made some tough staff cuts, but the company is still edging closer to profitability and the decisions being taken by management should see profit margins improve if China can get back to strong growth in 2023. Sea investors would then benefit from the very low valuations currently being offered.

Another threat to the region is a potential escalation of tensions between China and Taiwan. Although this could hurt the region, Sea’s revenues are not focused on the U.S. and Europe and would not be hurt by any sanctions. The company does make some of its revenues in Taiwan but it would fare better than more globalized stocks.

Conclusion

Sea Limited was a huge gainer throughout 2020-21 as the company was able to avoid the lockdown market turmoil and was seeing strong growth in its gaming and digital finance divisions. The Shopee e-commerce platform also benefited from the stay-at-home dynamic during that time. As the head into 2023, the company has been cutting costs and management has taken a tough lesson from the bear market but the company is emerging stronger. As developed economies move towards a recession, China can power the Asian region if it can emerge from the Zero-Covid lockdown policies. That would be a boost for Sea’s revenues and with the cost-cutting in place, it could see net margins and profitability going positive towards the end of 2023.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

Be the first to comment