MarsBars

It’s near official that there won’t be a Santa Claus rally, with it being replaced by tax loss harvesting and portfolio window dressing by hedge funds. I have no problems with that, as this simply creates bargain opportunities on solid dividend payers, like Bank of Nova Scotia (NYSE:BNS).

As shown below, BNS has again fallen below the $50 level, giving investors an above 6% dividend yield. In this article, I highlight why BNS is now a great value opportunity for dividend investors, so let’s get started.

BNS Stock (Seeking Alpha)

Why BNS?

BNS, otherwise known as Scotiabank, is one of the oldest banks in the world, with a history dating back to the 19th century. It’s also the third largest Canadian bank by assets, and is the country’s most international bank, with around 40% of its revenue coming from international regions, primarily in Central and South America.

Scotiabank offers a range of financial products and services, including retail and commercial banking, and wealth management. Scotiabank’s diversified revenue stream is a key strength, as it allows the bank to weather economic downturns and mitigate the impact of any specific business unit underperforming.

In addition, the bank’s global presence allows it to tap into growth opportunities in emerging markets and diversify its revenue stream even further, and management has been significantly expanding its domestic wealth operations domestically in Canada, with the acquisitions of MD Financial and Jarislowsky Fraser, transforming BNS into Canada’s third largest asset manager.

Meanwhile, BNS is seeing encouraging growth, particularly in the current economic environment, with adjusted earnings growing by 8% for the full fiscal year 2022. Moreover, it achieved a strong adjusted return on equity of 15.6%, sitting 60 basis points higher than the 15.0% realized last year. This was driven by robust loan growth, fueled by total deposits growing by an impressive 15% for the full fiscal year.

Importantly, BNS maintains a strong A+ credit rating and carries a Tier 1 capital ratio of 13.2%, sitting well above the 6% minimum requirement for Tier 1 capital. Importantly, BNS’s dividend is well covered by a 51% payout ratio, based on diluted earnings per share of C$8.02 for recently completed full fiscal year. Notably, BNS has a storied history of paying an uninterrupted dividend and the current quarterly dividend rate of C$1.03 is 13 cents higher than where it was last year.

Near term risks to BNS include global economic uncertainty, which may hit some of its markets harder than others. However, I do see some silver linings on the horizon, particularly for the second half of next year, as there are early signs of slowing tightening by central banks in Canada and the U.S. Management is also seeing encouraging signs coming out of Central America, as noted during the recent conference call:

In Canada, the economic growth is moderating, but economic levels of activity remained robust. The strength of our labor market and strong balance sheet, along with robust commodity prices, are providing a counterbalance to the impact of a less blunt European and Asian economic environment.

Central banks in our key Latin American economies have responded early and aggressively to inflation with orthodox monetary policy. And despite this, we have not seen any meaningful reduction in capital sources in the region. We are confident that this decisive action will allow most central banks to hit terminal rates soon and allow others to ease during fiscal 2023.

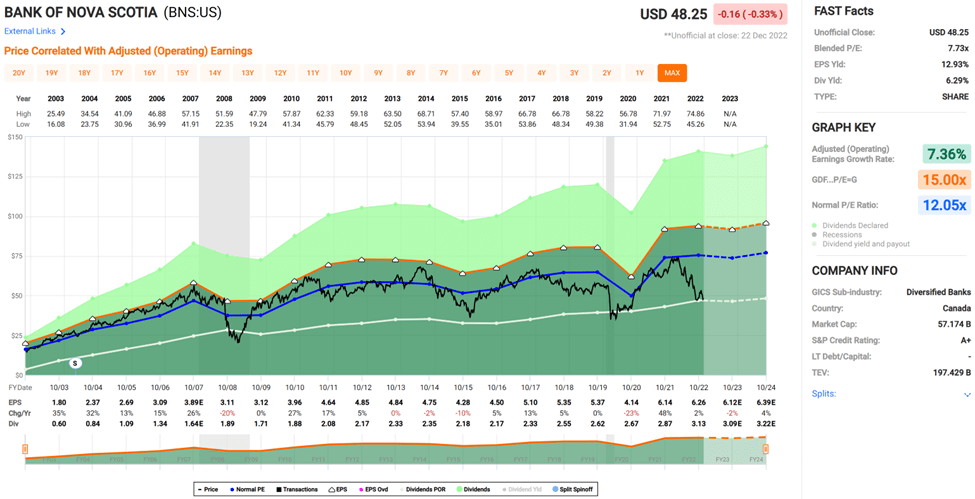

Turning to valuation, there’s no mistaking that BNS is rather cheap at the current price of $48.25 with a forward PE of just 7.9, sitting well below its normal PE of 12.1. I believe the discount is unwarranted considering the strength of the operating fundamentals and strong balance sheet.

BNS Valuation (FAST Graphs)

As such, it appears the market is baking in more than a fair share of risks into the stock price. Analysts seem to agree, as they have a conservative average price target of $55.72, which still translates to a robust 22% total return potential from the current price.

Investor Takeaway

Overall, Scotiabank is an attractive pick for those seeking exposure to a large Canadian bank with a solid balance sheet and strong operating fundamentals. It has solid growth prospects through its expansion in domestic wealth management services and through strategic exposure to emerging markets. Lastly, BNS pays a well-covered and attractive dividend yield and is currently trading at a compelling valuation, which could result in potentially very strong total returns for patient investors.

Be the first to comment