iambuff/iStock via Getty Images

Recommendation

My recommendation is to go long Schrodinger (NASDAQ:SDGR). At first glance, it might seem like SDGR is a biotech company that is hard to value due to the binary nature of the industry. However, the main value of the business comes from its computational platform that has extremely high value proposition that addresses the critical needs of biopharma companies. I believe SDGR’s deep experience and years of computing data are key differentiating factors for its software, which should allow it to continue capturing share.

Business

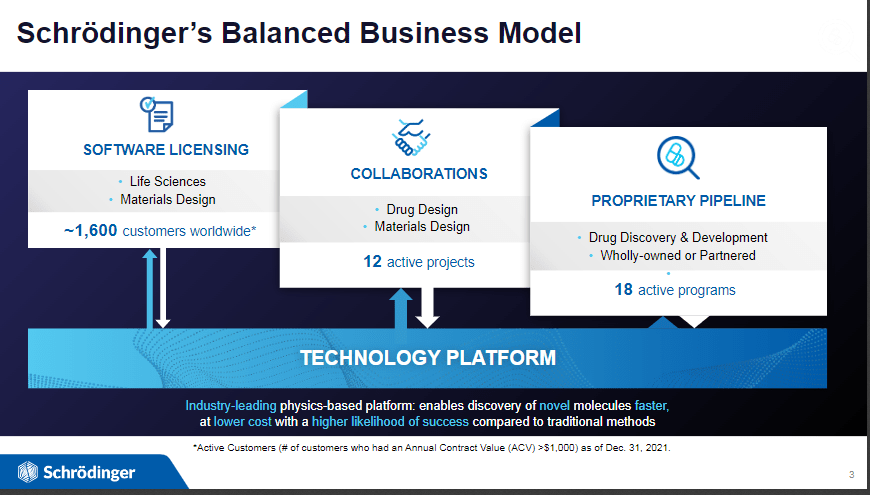

SDGR’s primary focus is on the pharmaceutical industry, specifically drug discovery and materials design software development and the management of both stand-alone and collaborative drug discovery initiatives. Given that I am not a biomed expert, my focus will be on SDGR’s software business.

Nov’22 ppt

SDGR software business has strong value proposition

The majority of revenue comes from licensing software that the company develops and sells to the worldwide biopharmaceutical industry for use in drug discovery. Initially lacking in technical prowess, SDGR has expanded its offerings to include a comprehensive suite of software and services for the entire drug design process. A wide variety of clients use the service, from small biotechs to multinational pharmas.

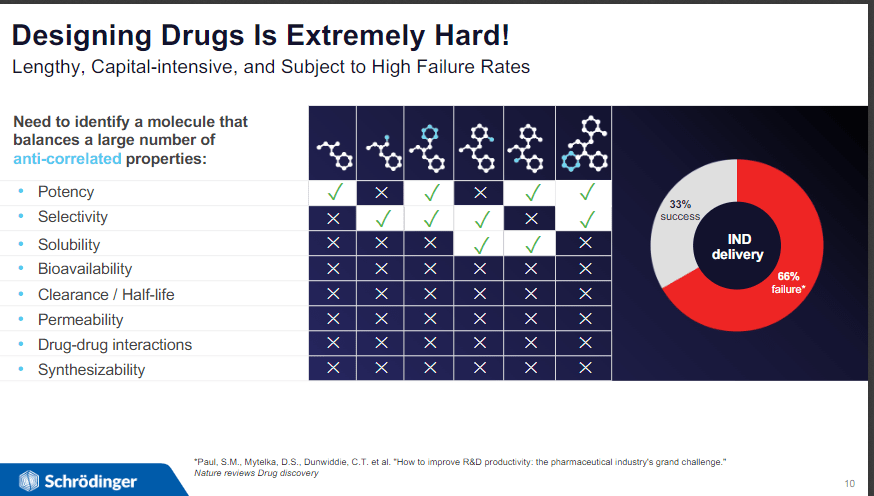

The company’s software products are in high demand because they are useful tools for biotech and pharmaceutical firms engaged in drug discovery and development. Customers are not limited to those in the medical industry; rather, they also include those in the advanced materials sector who are working to overcome fundamental challenges like lengthy, capital-intensive processes with high failure risks. Regarding pharmaceuticals, the chemistry-related difficulties are complex. It is very challenging to make an accurate forecast of the future given the complexity of all these factors in drug design. Multi-decade efforts have paid off in SDGR’s well-established brand name and competitive advantage in the market for its software suite. Scientists and software engineers at SDGR were instrumental in creating a computation platform with the ability to accurately predict drug properties.

Oct’22 presentation

SDGR’s software business is driven primarily by these factors:

- To attract new clientele

- Expand the company’s use of its pipeline products among its current base of clientele

- To expand the company’s customer base into new markets.

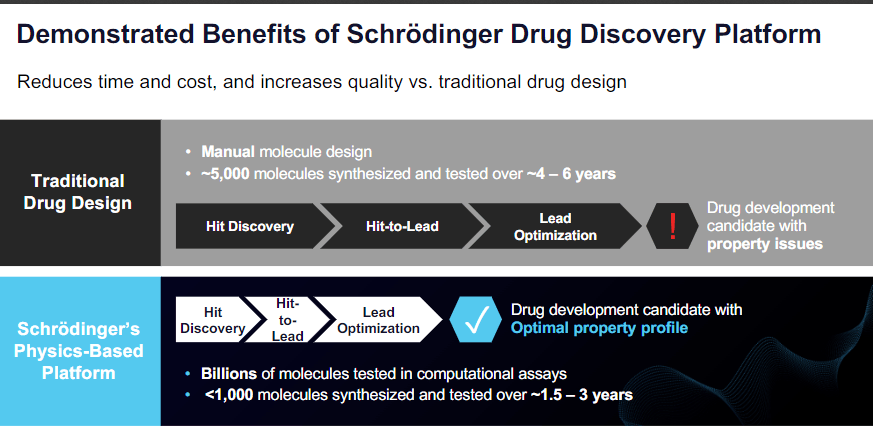

SDGR’s recurring fee is calculated by the number of molecules a user is exploring at once and the length of time that user is exploring them. The demand for more effective R&D in biopharmaceutical companies in order to identify high-quality drug candidates is a key driver for SDGR’s software. As the number of possible molecules is so large, this is significant as factors such as computational power often limit the extent to which they can be explored efficiently. The software developed by SDGR allows users to quickly and accurately assess the properties of a large number of molecules, potentially in the billions. Comparatively, conventional methods may call for the synthesis of many fewer molecules over a much longer time frame.

Oct’22 presentation

Differentiated product stemmed from years of data processing

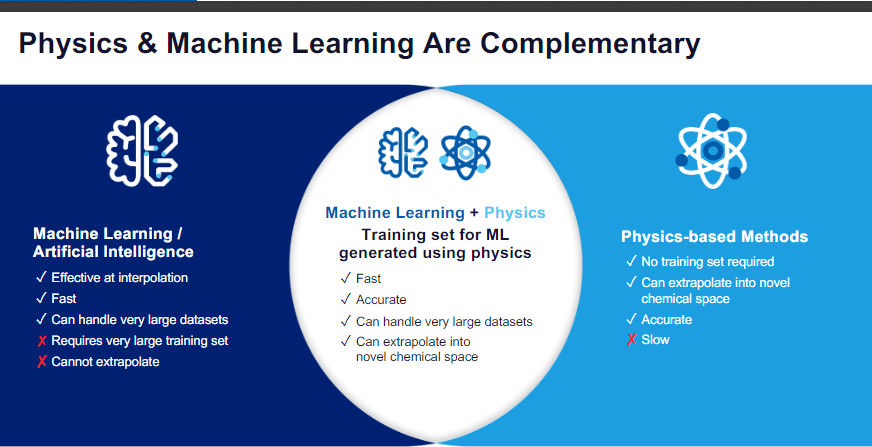

The SDGR platform is established on a bedrock of physics-based methods, makes use of data processing muscle, and takes advantage of the scaling benefits of machine learning. Computing power improvements, improved model understanding, and developments in high-resolution protein structure analysis have all contributed to this development over time. These allowed SDGR to create their unique, physics-based simulation-based software platform.

Oct’22 presentation

Other use cases in material sciences

Businesses from the materials sciences industry who are looking to create novel molecules for use in industry are among SDGR’s software license purchasers. Aerospace, semiconductors, and the energy sector are just some of the industries served by SDGR. I believe there is room for growth in the use of computational methods for molecular discovery among these customers, as they make use of a lot of the same technology as life science customers. However, the proportion of the company’s revenue and customers attributable to this focus is relatively small.

Growth expectation for the software business

The amount of money spent on research and development in the life sciences is a significant factor influencing demand dynamics. My concern is that financing opportunities for startups in the biotechnology industry have become more difficult in recent years due to the overall economic climate. However, I think the SDGR value proposition wins out here, and that customers will remain invested in the SDGR platform due to the savings they realize compared to real-world experiments.

In a nutshell, customers from the biopharmaceutical industry are the primary force behind the software division’s expansion. And I think there’s growing interest in applying AI and ML to the biopharmaceutical industry, mainly driven by the need develop new medicines. To this end, I think SDGR is in a great position to take advantage of their existing partnerships in order to further expand their technological capabilities, given their status as an established player and front-runner in adopting physics-based methods in machine learning.

Short-term growth

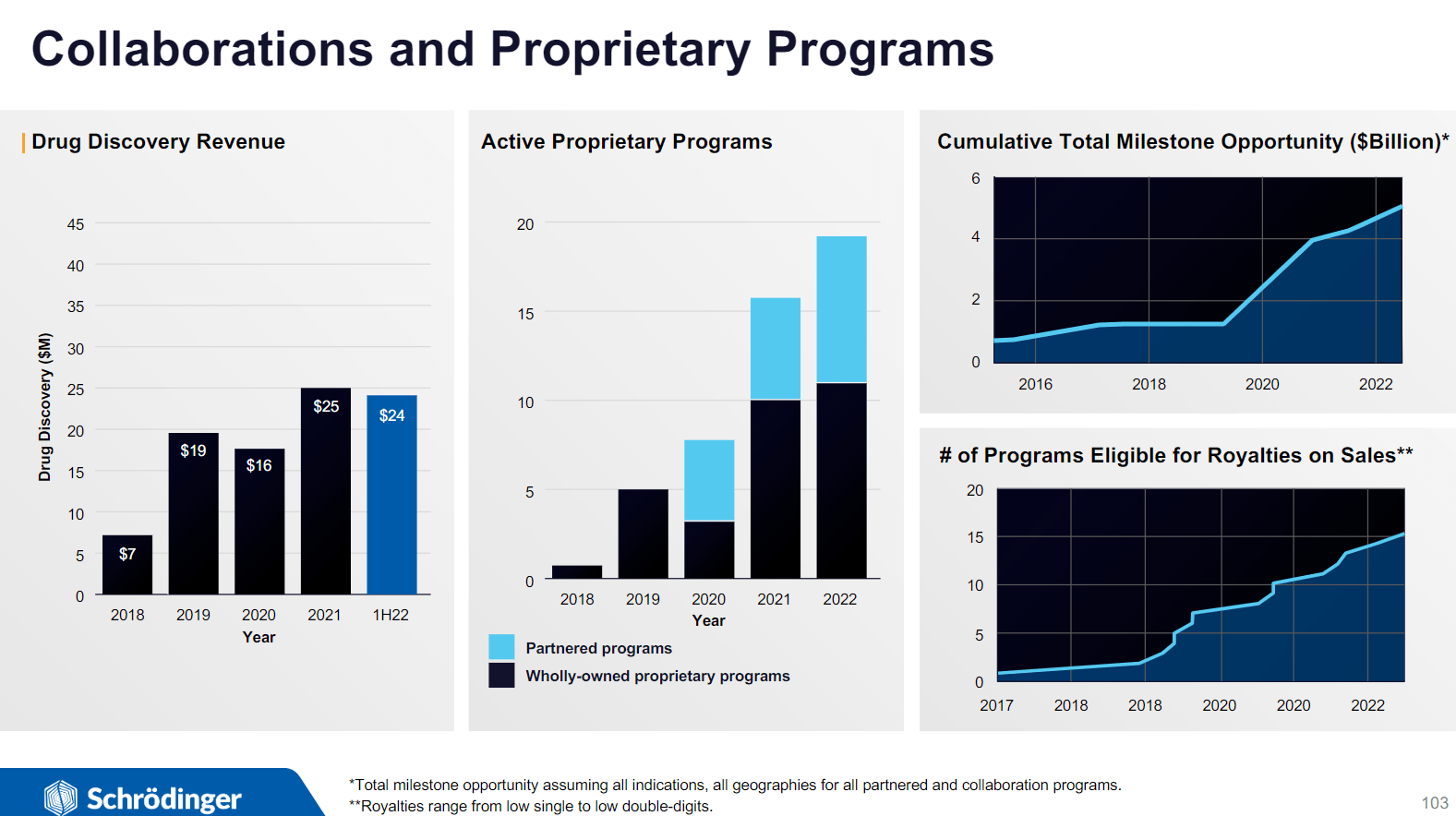

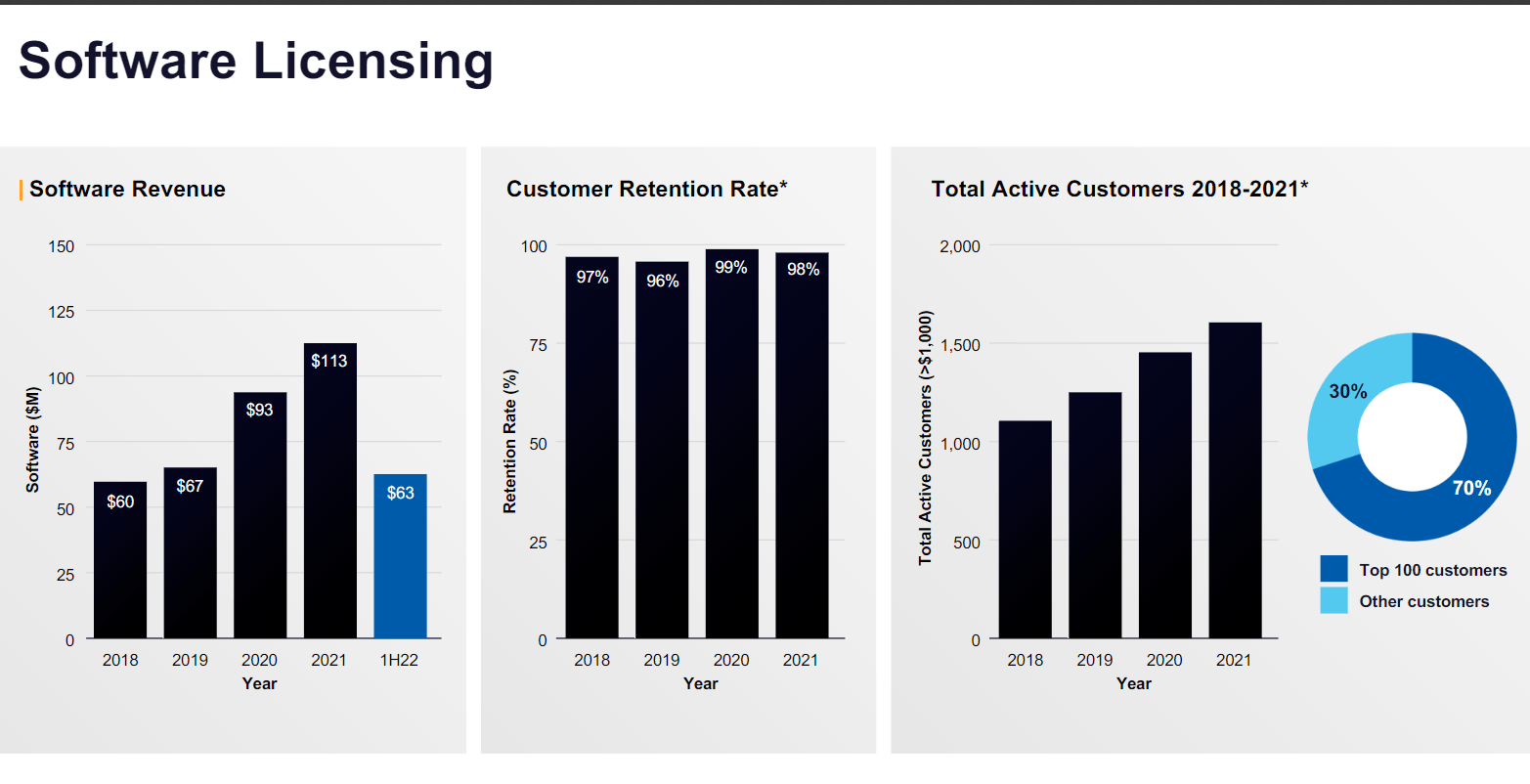

In the near future, I anticipate that SDGR will reap the rewards of their well-established competitive advantage in the pharmaceutical industry. The foundation of this perspective is the long-standing computational platform, loyal customer base, and proven track record of success SDGR has enjoyed through its partnerships. In addition to qualitative evidence, such as the increased number of programs that progress to the next stage, SDGR has provided quantitative metrics to demonstrate its success in streamlining drug discovery. Additionally, SDGR also has a very high retention rate (>97%). I believe all of these are clear evidence of success.

Oct’22 presentation Oct’22 presentation

Valuation & model

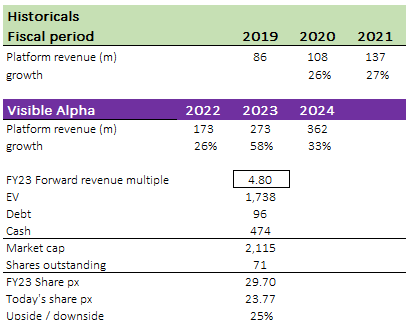

Using consensus estimates, I believe SDGR is worth $29.7 in FY23. My model only focused on valuing the platform business – which I think has the most value proposition and can be modelled with good amount of certainty (unlike the drug development business that has binary outcomes).

Now, the question is what valuation multiple should a company with strong value proposition, high retention rates, high gross margin, and growth outlook trade at? I would think it is a lot higher than 4.8x but to be conservative, I assumed it would trade at this level.

Author’s own calculations

Risks

Future competition

There is technological competition from other companies providing computational platforms that are increasingly using physics-based methods. While the underlying technology for all machine learning applications is the same, the careful selection of training inputs and ultimate application is what sets each business apart. Though SDGR has been ahead of the curve in this space, competitors like Exscientia (EXAI) are beginning to see the potential and introduce the feature on their own proprietary platforms.

Summary

At first glance, SDGR may appear to be a biotech company with a difficult to value due to the binary nature of the industry. However, the company’s primary worth originates from its cutting-edge computational platform, which offers a compelling value proposition and meets the pressing requirements of the biopharma industry. I think SDGR’s extensive background and years of computing data are major selling points for its software and will allow it to maintain its market dominance.

Be the first to comment