alvarez

Schrodinger

Making new drugs is hard because it involves finding just the right molecule that can help treat a specific problem. This molecule needs to be powerful, target certain cells or proteins, dissolve well in the body, easily reach the right part of the body, not stay too long in the body, be able to pass through cell walls, not have bad reactions with other drugs, and be able to be made in big quantities. And even with all that, making new drugs takes a long time, costs a lot of money, and often doesn’t work out.

Using smart computer methods like machine learning and physics-based modeling can make it much easier to design new drugs. These methods can help predict how new molecules will behave and increase the chances of finding just the right molecule for a certain problem. A company called Schrodinger has made a platform that can help with this process. They make money by selling the use of their platform’s software to other companies and working on projects with them.

Schrodinger (NASDAQ:SDGR) has built a computer program that can predict important aspects of molecules with a high level of accuracy by using advanced physics and machine learning methods. They believe that this is better than the usual ways of discovering drugs. This program can help find new drugs faster and cheaper, and increase the chance that a drug will be successful in further testing. The program can also test a lot of molecules at once, quickly and well, which helps speed up the process and reduce costs. It has several special features like finding leads faster, predicting properties better, exploring lots of molecules, and evaluating them.

As a result, the company has a portfolio of 18 proprietary drug discovery programs with potential to be first or best in class, with 9 programs in the clinical phase and 12 projects in discovery phase in their collaborative pipeline. They have reported recent progress on their pipeline and drug discovery portfolio including their MALT1 inhibitor which is open for patient enrolment and announced a partnership with Lilly for the discovery of small molecule compounds for an undisclosed target. They also highlighted that they and their collaborators are achieving cumulative technical success rates that signal improvements relative to published industry averages, which they believe is a promising trend that highlights the effectiveness of their computational platform.

Financial analysis

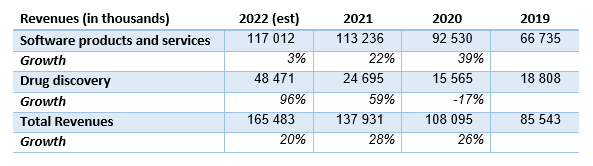

The company made $37 million in sales in Q3, which is more than they made last year. They made most of the money selling their drugs and software. They also said that they’re doing okay for next year, even though the economy is tough right now.

The company used up $34 million of its money this quarter, which is more than the $16 million it used up last quarter. They’ve been using about $30 million every quarter this year. But the company thinks that their software business will keep growing and they will spend less money soon, so they don’t think they’ll use up as much money in the near future.

The company’s software sales are not growing as much as they used to, most of their growth is coming from the drug discovery side. This means that the company’s software is not doing as well as it seemed it would be. It appears that the narrative around both software and drug discovery is not keeping traction. They are essentially dependent on drug discovery to keep growth going.

Author’s computations based on company financials

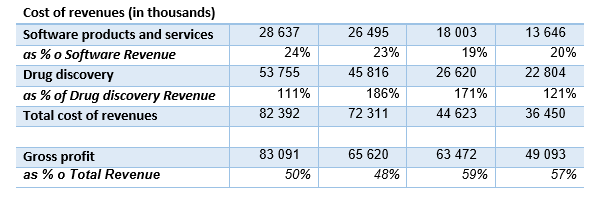

The COGS analysis also supports this conclusion. The relative costs of the software business have increased, contradicting the narrative about scaling sales and diluting costs, while the costs of the drug discovery business have reached a peak in 2021 and are now going down (relative to revenues). This suggests that the company’s growth is being driven by the drug discovery side of the business, but the costs of running this business are higher than the revenue it brings in.

Author’s computations based on company financials

The company’s expenses and costs are not balanced and they are still trying to grow to be financially stable. This is normal for many great companies, but it’s not the best time to do this right now because of the current macro landscape. The company may need to pivot its strategy to save money. The company is expected to spend around $130 million in 2022 and will have about $440 million in cash and other assets by the end of the year. This should be enough for 3.4 years at their current rate of spending.

Risks

The company is exposed to a multitude of risks, I’ll just expose the most relevant in the context of this article. As we’ve seen the platform has high potential but also has risks. These risks include:

- Whether people will want to use the software

- Whether there are other similar software that may be better

- Whether the company can keep working with partners or get more money to fund the business

Additionally, there may be some uncertainty about how long it will take to develop new products and get them approved by the government to be sold.

The company’s internal drug discovery programs and computational platform have some risks. These risks include:

- Whether the company can start and finish the programs on time

- Whether the programs will be successful and lead to new drugs

- Whether the company can make money from the drugs they develop

- Whether the company will have enough money to keep running the business

There may also be uncertainty about whether the company will receive money from its partnerships, such as the one with Bristol-Myers Squibb, and whether they will have enough money to pay for everything they need to do.

There are additional risks related to the company’s cash burn and its ability to access funding if needed. The company may run out of cash before it can generate enough revenue to sustain its operations.

Valuation

Schrodinger is currently trading at 10 times sales. In the short term, it’s possible that the market may shift its focus from growth to cash conservation, which could put pressure on Schrodinger to prioritize cash preservation over growth. This could be a difficult and painful process, as we’ve seen with other companies like Invitae who have gone through similar situations.

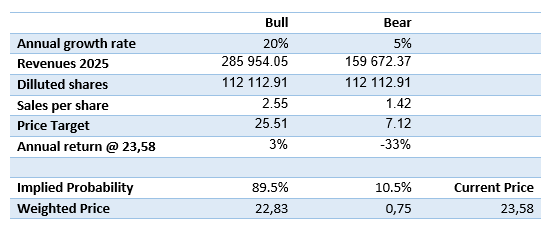

To assess the situation, imagine a world where this company continues to soar, growing at a steady 20% clip and the market rewards it with a generous 10 times sales valuation by 2025. On the flip side, let’s also consider a less favorable scenario where growth slows to just 5% as a result of cost-cutting measures and the market only assigns a 5 times sales valuation. But in both scenarios, let’s assume the number of outstanding shares increases by 17% each year. By 2025, our model estimates the following:

Author’s computations

The bull scenario paints a rosy picture, but the current market price already discounts a significant part of it, which means the potential upside is limited. But the downside, on the other hand, is quite severe. Based on my recent experience with similar tech companies at this stage of development, I believe the downside risk is very real. All in all, I find Schrodinger’s technology and business model intriguing, but for now, I’m going to sit on the sidelines and wait for more information.

Be the first to comment