Thomas Lohnes

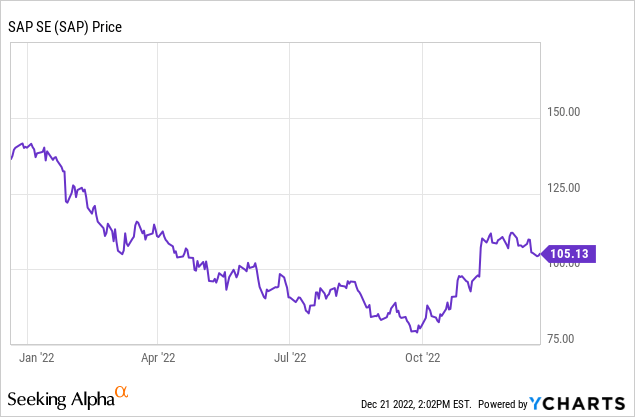

SAP (NYSE:SAP), the German software giant, has long been a “boring” tech stock but a dependable one. In 2022 as well, as the majority of the tech sector cratered (names large and small suffered – even Amazon.com (AMZN) has seen more than half of its market cap sliced off this year), SAP’s relatively modest ~25% loss looks like a port in a storm.

SAP has also benefited from a recent rally. Since September, SAP has seen its stock lift by more than 30% – which is even more substantial when we consider that most tech stocks saw corresponding drops of that magnitude over the same time frame. Investors are cheering the company’s strong growth rates (boosted in no small part by FX tailwinds) as well as its upcoming plans to raise prices for support contracts.

I have long been bullish and championed SAP as a buy-and-hold stock, but after seeing the tectonic shifts in the tech sector this year, I am shifting my opinion on SAP to neutral. In a nutshell, I think there are far better opportunities to play a 2023 rebound within beaten-down, smaller-cap tech names: and now is an excellent time to emphasize stock-picking and take on more risk.

To me, SAP is now a mixed bag of both positive elements and potential downside catalysts. On the positive end for the company:

- Category leadership in many areas of enterprise software- Though the average consumer likely won’t interact with SAP, its dominance in enterprise software is unmistakable. It is the dominant player in ERP systems – which help companies manage their data and run their operations. Via a surprisingly sharp-eyed M&A strategy, SAP has also inherited other major category leaders, including Ariba, Concur, SuccessFactors, Qualtrics, and other notable brands. SAP, in fact, may have one of the most successful track records for M&A among enterprise software stocks, without any noticeable flame-outs and write-downs.

- Ambitious transition to the cloud- The company has heavily been pushing its customers away from license deals and into its SaaS products, which will stunt near-term revenue growth. Over the long term, however, cloud customers will deliver greater lifetime value.

- Aggressive long-term targets- By 2025, SAP intends to triple its cloud business, hitting €22 billion in revenue. Relative to 2021, the company also intends to boost its operating profit by 40% by 2025.

At the same time, we should be wary of the following:

- Growth rates right now are propped up by FX tailwinds- Unlike U.S.-based companies, the strengthening of the dollar has boosted SAP. In its most recent quarter, FX tailwinds provided ten points of revenue growth lift. Once these impacts moderate, investors may be disappointed when optical growth rates slow down again.

- Valuation- At current share prices near $105, SAP already trades at an ~18x forward P/E based on Wall Street’s consensus FY23 EPS of $5.83 (data from Yahoo Finance). That represents a premium valuation multiple versus the rest of the market – in my view, there are far better value-driven opportunities to invest in at the moment.

The bottom line here: while I think SAP remains a good hold for a 3-5 year period, I’m focused on redirecting my capital into rebound plays for 2023. I’d recommend replacing or at least trimming your SAP position to make room for more risk-oriented growth stocks.

Q3 download

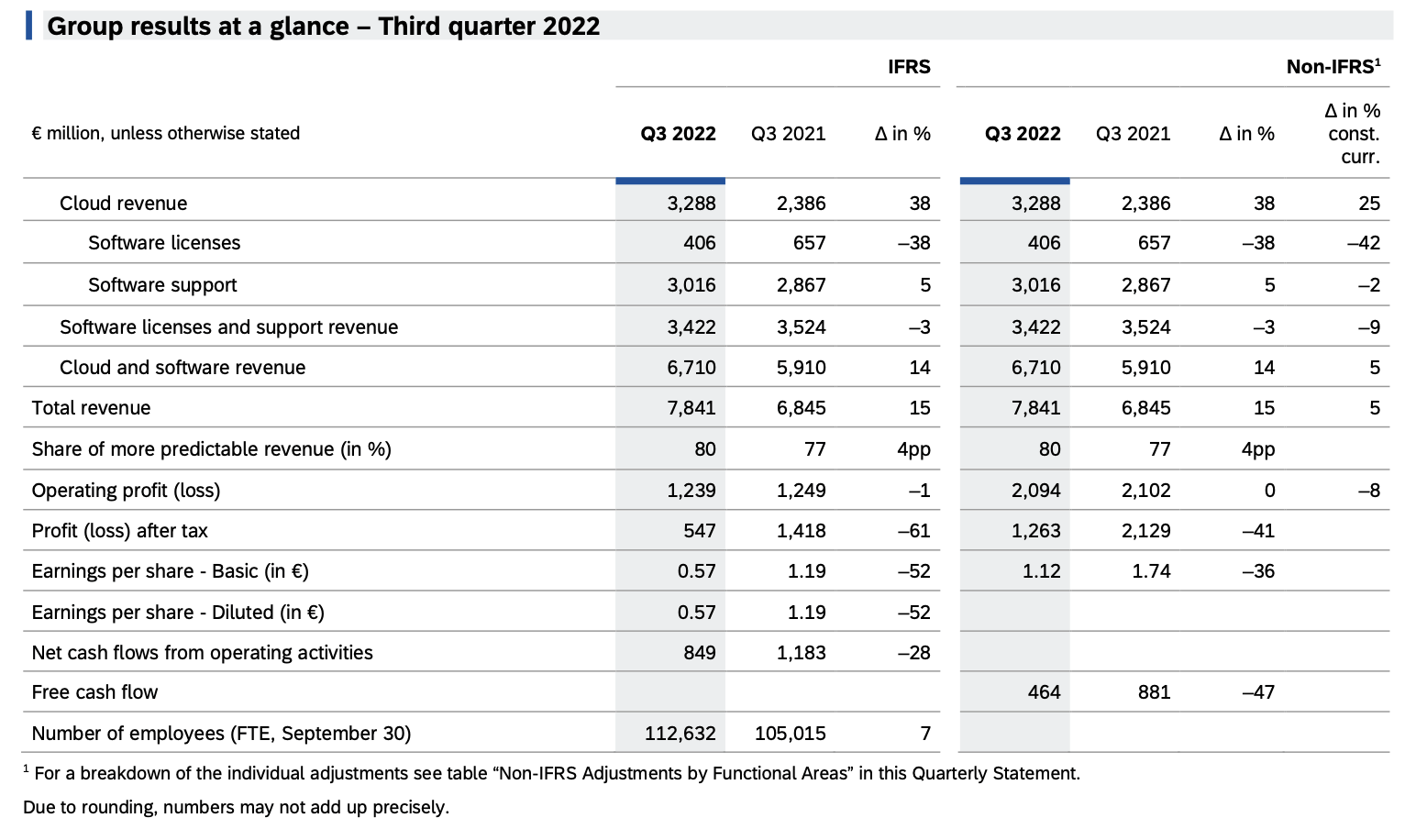

This being said, we will still acknowledge that SAP has printed excellent results that boosted investor enthusiasm of late. Take a look at the Q3 earnings summary below:

SAP Q3 highlights (SAP Q3 earnings release)

SAP’s revenue in Q3 grew 15% y/y to €7.84 billion, accelerating over 11% y/y growth in Q2 and beating Wall Street’s expectations of €7.60 billion (+11% y/y) by a four-point margin.

The big callout here: FX tailwinds provided ten points of growth lift in the quarter. The company’s largest sales region, the U.S., generated 37% of the quarter’s revenue – and due to the euro and the dollar reaching parity for a good chunk of Q3, this provided a huge optical benefit to Q3 results. On a constant-currency basis, the company’s revenue grew only 5% y/y.

That’s not to say, however, that underlying demand – particularly for cloud products – wasn’t strong in the absence of FX lifts. The chart below shows the disaggregation of SAP’s cloud revenue by geo. On a global basis, revenue grew 38% y/y (25% y/y on constant currency); revenue in the Americas indexed above this at 26% y/y growth in constant currency.

SAP cloud revenue by geo (SAP Q3 earnings release)

Management noted robust end-customer demand despite macro headwinds, and reiterated its near-term goal of delivering double-digit operating profit growth in 2023. Per CEO Christian Klein’s remarks on the Q3 earnings call:

Despite the macro challenges, we see strong demand as our SaaS portfolio is especially relevant during these times. And we anticipate that the flywheel effect of our Business Technology Platform together with our partner ecosystem will power strong cloud consumption. We are also excited about our innovation pipeline, and we look forward to announcing new innovations at our Annual TechEd event in November. As we mentioned last quarter, we are continuing to simplify and consolidate our portfolio to focus on high growth solution, which may also be complemented by potential future acquisition to strengthen our core. As such, we remain committed to deliver our 2023 commitments including double-digit operating profit growth in 2023. We are also very confident in delivering our 2025 mid-term ambitions.”

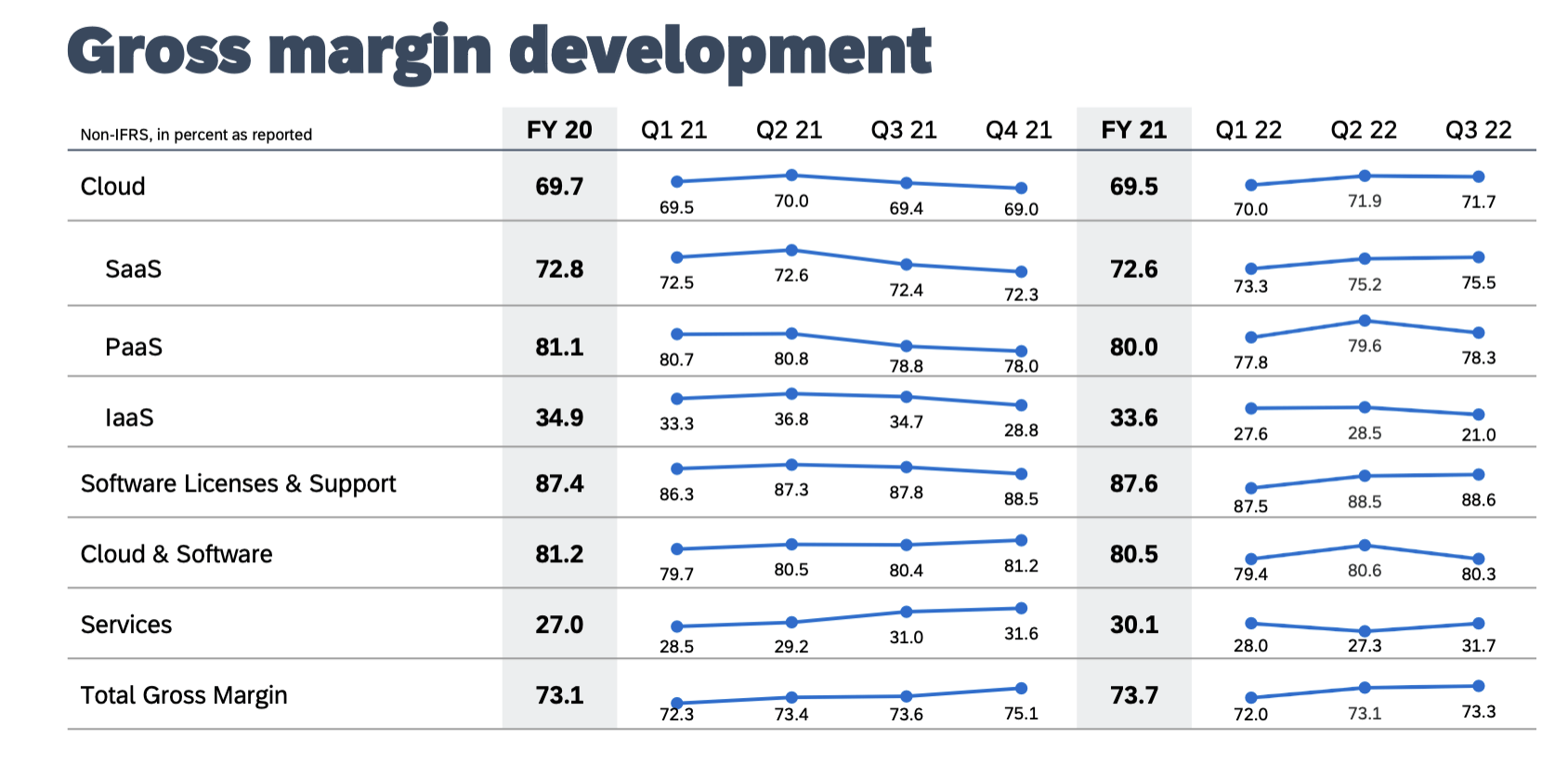

SAP also delivered a 230bps boost in cloud gross margins to 71.7%, driven by economies of scale on the company’s cloud infrastructure platform:

SAP gross margin trends (SAP Q3 earnings release)

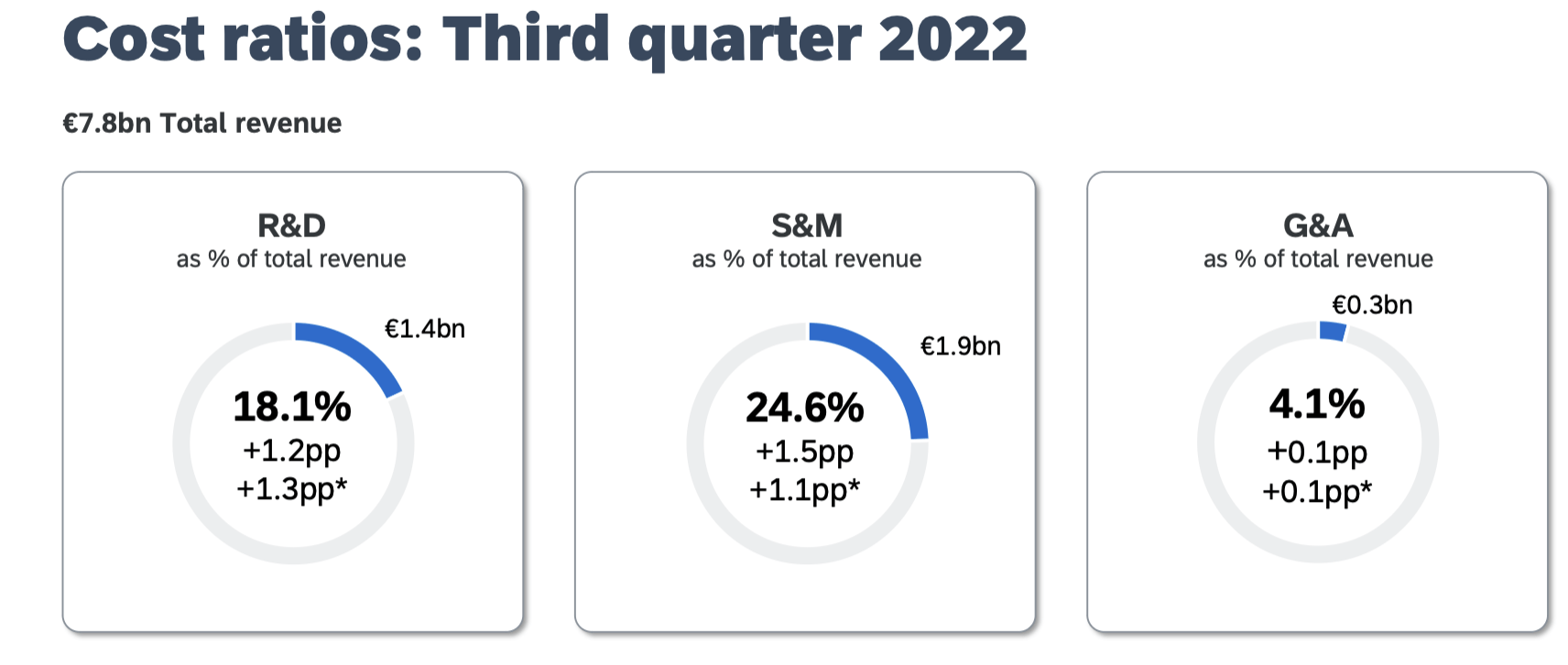

We do note, however, that SAP has absorbed slightly higher opex costs owing to wage inflation (as well as FX impacts having an inverse headwind on expense). Both R&D and sales and marketing costs saw a one-point rise as a percentage of revenue:

SAP opex ratios (SAP Q3 earnings release)

As a result, pro forma operating profit of €2.09 billion was flat year over year, representing a 26.7% margin (a 400bps decline versus 30.7% in the year-ago Q3).

Key takeaways

All in all, I don’t see SAP materially outperforming or underperforming the major indices in 2023. If your risk tolerance and willingness to look past near-term volatility is high, I’d recommend shifting more of your portfolio out of safer assets like SAP and allocating more toward beaten-down growth stocks.

Be the first to comment