shaunl

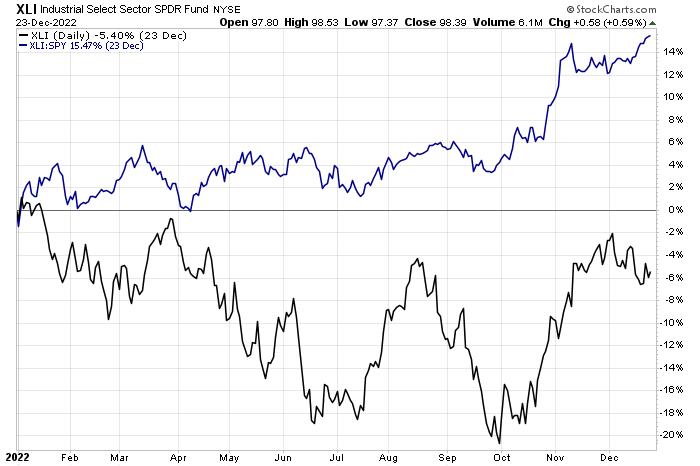

Amid so many global macroeconomic warning signs, there are green shoots seen in Industrials-sector equities. The Industrial Select Sector SPDR ETF (XLI) has been notching fresh relative highs compared to the S&P 500 lately as its absolute chart exhibits a bull flag pattern. Still, volatility has been seen in the niche dry bulk shipping space.

One small Marine player had an earnings beat last month, but shares feature technical weakness. Let’s navigate the risks and potential upside of Safe Bulkers.

Industrials: Fresh 52-week Relative Highs

Stockcharts.com

According to CFRA Research, Safe Bulkers (NYSE:SB), together with its subsidiaries, provides marine dry bulk transportation services. It owns and operates dry bulk vessels for transporting bulk cargoes primarily coal, grain, and iron ore. As of March 18, 2022, the company had a fleet of 40 dry bulk vessels having an average age of 10.4 years; and an aggregate carrying capacity of 3,925,500 deadweight tons. Its fleet consisted of 12 Panamax class vessels, 7 Kamsarmax class vessels, 15 post-Panamax class vessels, and 6 Capesize class vessels. The company trades at low historic price-to-sales and price-to-earnings ratios.

The Monaco-based $356 million market cap Marine industry company within the Industrials sector trades at a low 1.9 trailing 12-month GAAP price-to-earnings ratio and pays a high 6.8% dividend yield, according to The Wall Street Journal.

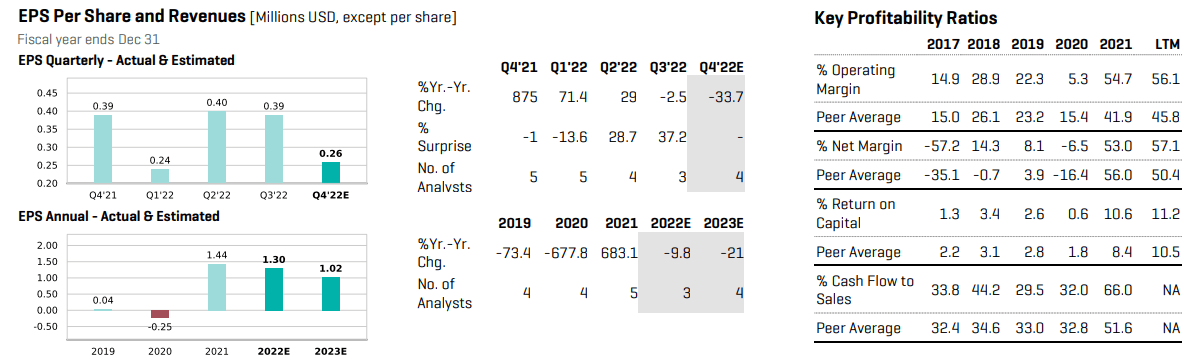

Back in November, Safe Bulkers reported Q3 non-GAAP earnings per share of $0.39 with a small 1.3% rise in yoy sales. The stock traded up slightly post-reporting. The firm also declared a $0.05/share dividend, which brought the forward yield to 7.4% at the time.

On valuation, CFRA notes that Q4 earnings are expected to feature a significant sequential decline from $0.39 earned in the same period a year ago. In terms of full-year profits, a second consecutive annual EPS decline is expected.

What’s positive about the fundamentals, though, is that SB’s profitability ratios are better than its peers. Seeking Alpha rates the stock with a stellar A+ valuation as it features very low trailing and forward earnings multiples. While its EV/sales ratio is not too cheap, shares trade at a low price to cash flow figure. I continue to like the valuation despite the tepid earnings outlook.

Safe Bulkers: Earnings Outlook & Key Profitability Ratios

CFRA Research

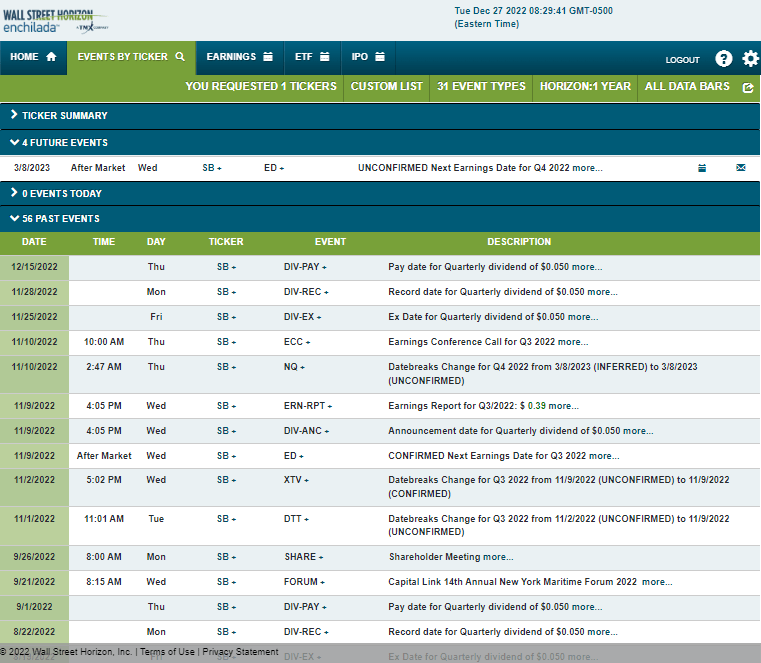

Looking ahead, the corporate event calendar is light in terms of volatility catalysts. Safe Bulkers reports Q4 2022 earnings on Wednesday, March 8 AMC (unconfirmed).

Corporate Event Calendar

Wall Street Horizon

The Technical Take

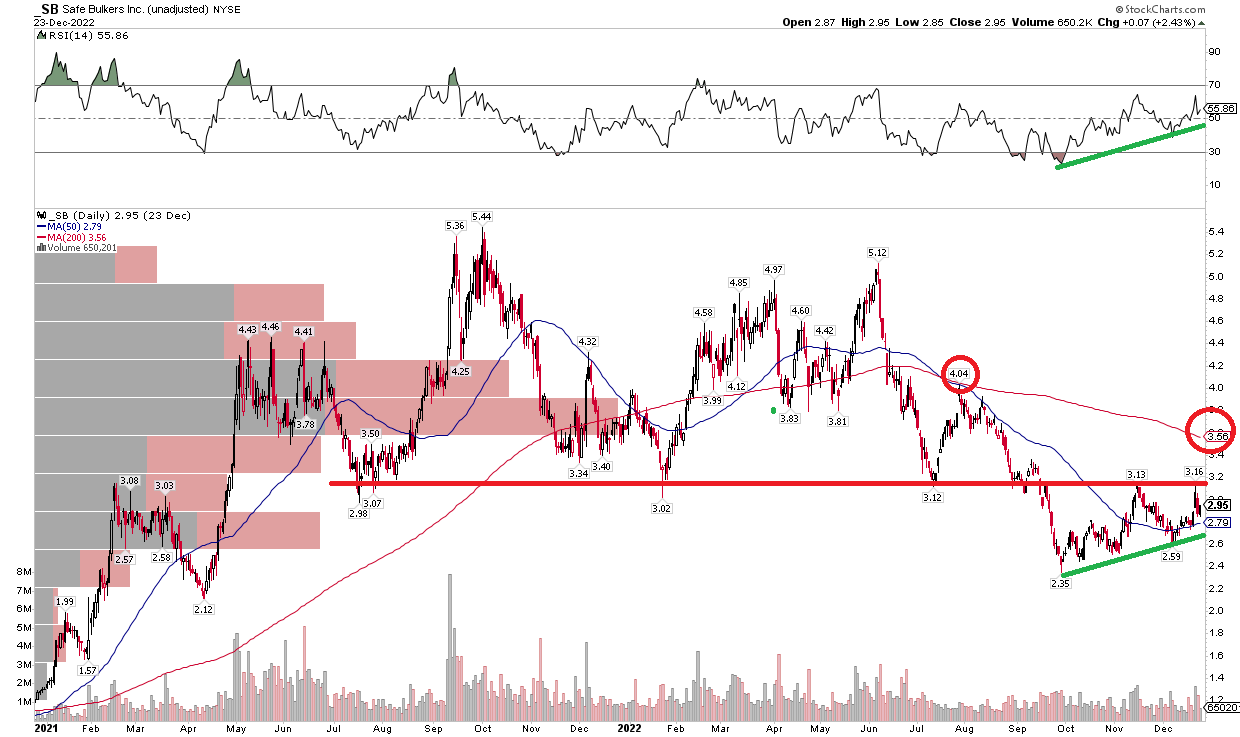

SB has key resistance in the $3 to $3.16 area – I noted this back in August. The stock was above this critical range from the second half of 2021 through the middle portion of this year. A key bearish break came in late September, though, and the stock then failed to rally back above resistance on two attempts – once in November and another in December.

Also notice in the chart below that shares feature an uptrend support line on both price and momentum. That makes the horizontal red line all the more important. But there could also be some selling pressure near the falling 200-day moving average – that was a tough spot for the bulls in July on a rally to just above $4. Overall, I now see more bearish than bullish risks on the chart. Waiting for a breakout above about $3.20 on a closing basis is a prudent strategy.

SB: Shares Fall Below Important Support

Stockcharts.com

The Bottom Line

I am downgrading SB based on some bearish technical developments. I like the valuation, but the stock is in a tough spot so long as it’s below $3 to $3.20. Keep this one on your radar to see how shares react in the low $3s.

Be the first to comment