Cineberg

Introduction

I have been following the KBC Group (OTCPK:KBCSY) (OTCPK:KBCSF) for quite a while now as I like the bank’s model of acting as a bank and an insurance company. Headquartered in Belgium, KBC also has activities in Central and Eastern Europe which provide an interesting diversification. But the main reason why I like KBC is its very solid capital ratio. The European regulator recently released the updated required capital ratios and KBC is – as expected – in a very safe position and has been hinting on returning excess capital to its shareholders.

Yahoo Finance

KBC Group has its primary listing in Belgium where the company is trading with KBC as its ticker symbol. The Brussels listing has an average daily volume of 720,000 shares, making it the most liquid listing. I would strongly recommend to use KBC’s primary listing to trade in the company’s shares as the average daily Euro volume exceeds 40M EUR. As KBC reports in EUR and has its primary listing in the same currency, I will use the Euro as base currency throughout this article.

The new capital requirements are in

Across the Atlantic Ocean, in Canada, we saw how the Bank of Montreal (BMO) had to raise in excess of C$3B in cash to shore up its reserves as the required capital ratios were updated by the regulator. A smart move by the Bank of Montreal to nip all potential issues in the bud, but it does show that the required capital ratios will play an important role now the counter-cyclical buffers may be increased.

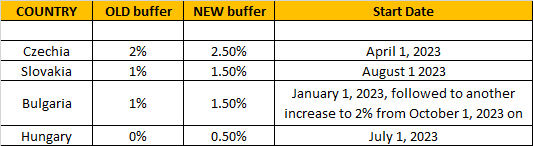

December traditionally also is the month where European banks are being notified of the changes in the required capital buffers. KBC disclosed its new required capital ratios last week and virtually all of the non-ECB regulators (KBC is active in Czechia, Slovakia, Bulgaria and Hungary and as none of those four countries use the Euro, it’s the national regulator that sets the countercyclical capital buffers).

The table below shows the old countercyclical buffer, the newly required countercyclical buffers and the date the new requirements will become active.

KBC Investor Relations

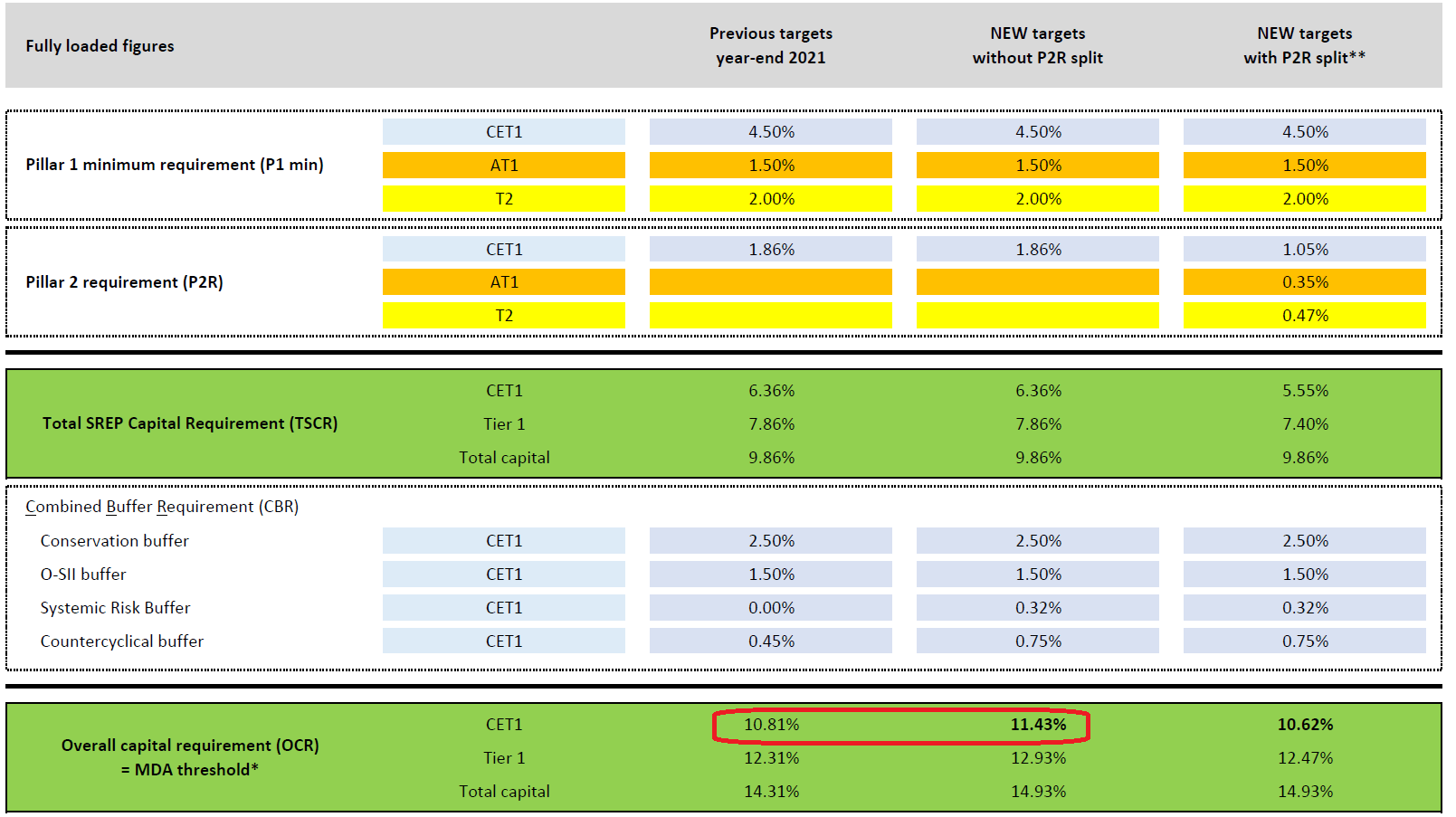

Additionally, the National Bank of Belgium has introduced a sectorial systemic risk buffer for exposure related to residential real estate in Belgium. These new rules will require KBC to further increase its minimum regulatory CET1 capital ratio by 32 basis points.

Taking all updates and new requirements into consideration, KBC’s fully loaded CET1 ratio requirement increases to 11.43%.

KBC Investor Relations

What does this mean for shareholders?

The updated capital requirements are pretty easy to understand but the main question is what this really means for KBC shareholders.

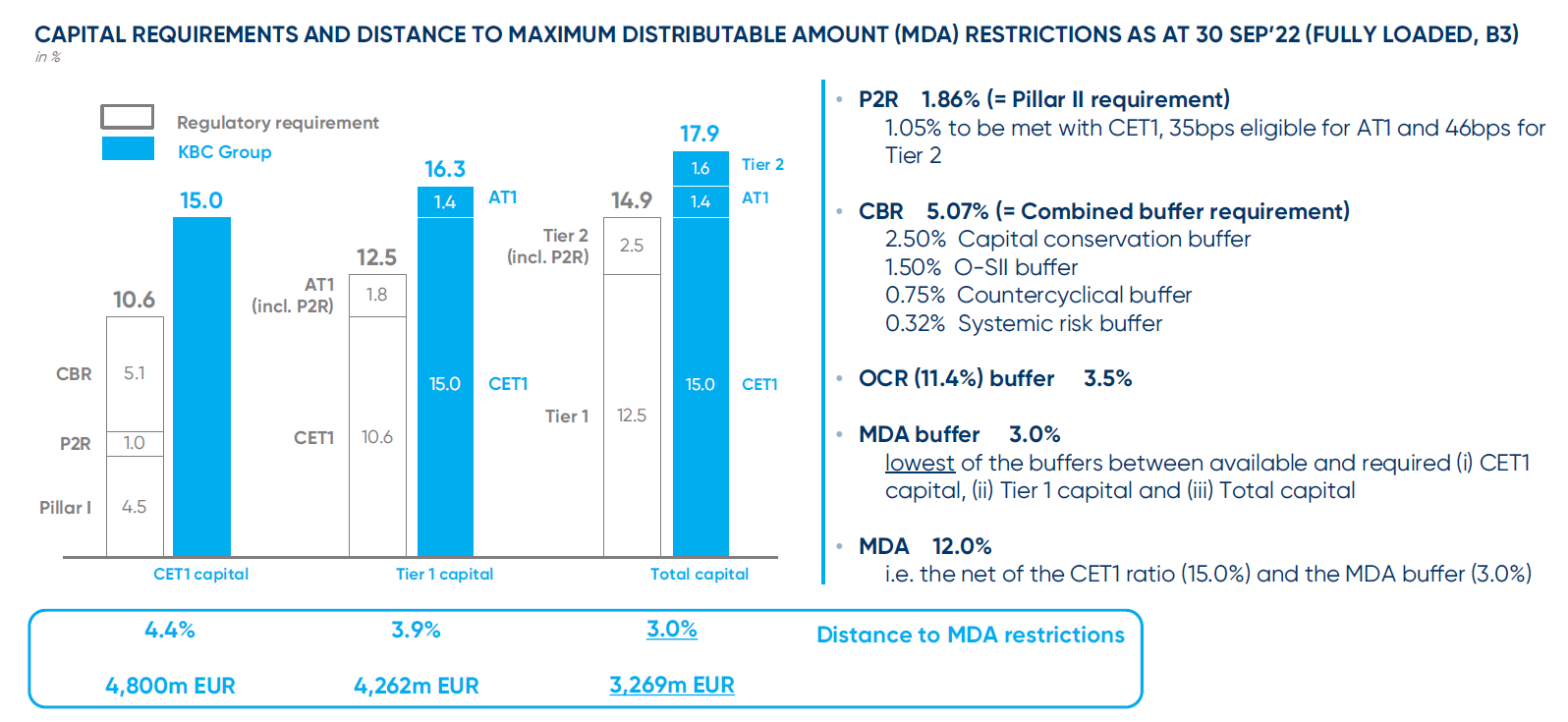

As of the end of the third quarter, the bank’s CET1 capital ratio came in at 15%.

KBC Investor Relations

So despite the increase of the required CET1 ratio to 11.43%, KBC is fine as its CET1 ratio already comes in at 15% (and will likely exceed that level by the end of this year).

That 15% level now also appears to be the bank’s official capital ratio policy. Upon the announcement of the new required CET1 ratio, KBC disclosed it will decide on an annual basis if it will just return the capital above the 15% threshold to its shareholders in the form of a special dividend and/or share buybacks. Keep in mind KBC’s normal dividend policy calls for a 50% payout ratio of the reported net income but the willingness to distribute everything above a 15% CET1 ratio indicates shareholders may soon see 75%-100% of the net income come their way.

Of course, there are still a lot of variables: The total amount of Risk-Weighted Assets can fluctuate, KBC can decide to acquire smaller regional banks to bolster its presence which could have an impact on the CET1 ratio, etc. So while moving to a 100% payout ratio is not a guarantee, I have the impression that the total shareholder distributions will exceed the standard 50% payout ratio in the coming years.

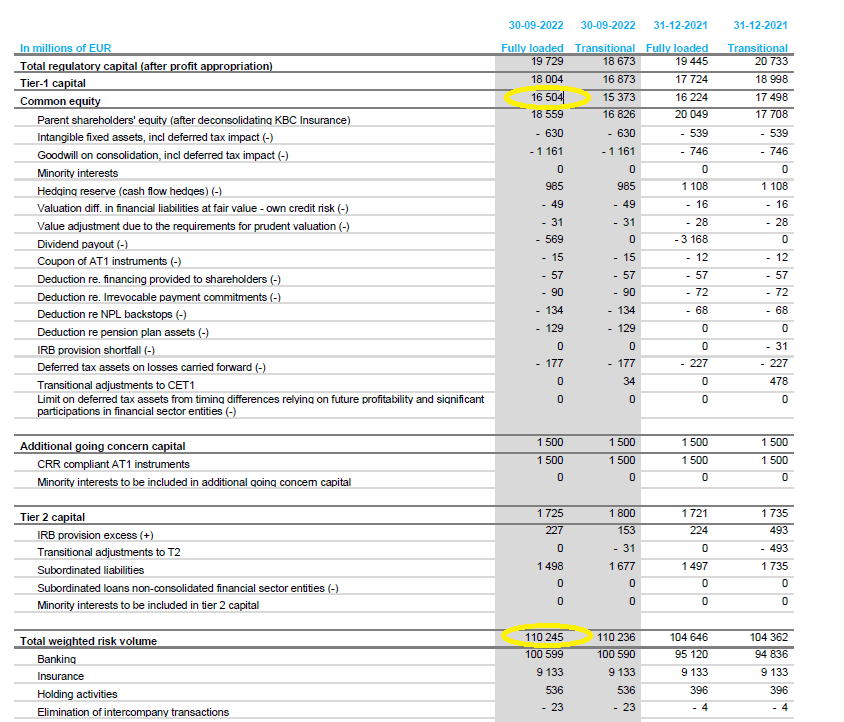

Looking at the Q3 financial report published by KBC, the total CET1 capital as of the end of September was 16.5B EUR. The total amount of risk-weighted assets was 110.2B EUR, resulting in the aforementioned CET1 capital ratio of 14.97% (15% on a rounded basis).

KBC Investor Relations

The bank reported a total EPS of 4.82 EUR in the first nine months of the year and will likely post an EPS north of 6 EUR per share in 2022. The EPS should increase in 2023 thanks to the expanding net interest margin (likely partially offset by a slightly higher loan loss provision). This means that – barren unforeseen circumstances – KBC will generate north of 2.5B EUR per year in profits which may be entirely distributed to its shareholders.

Investment thesis

While the higher required CET1 capital ratio doesn’t come as a surprise, KBC’s existing capital ratio is sufficiently strong to remain one of the Eurozone banks with the highest capital ratios. Based on 110.2B EUR in Risk-Weighted Assets, the bank has approximately 3.5B EUR in excess capital vs. the required regulatory minimum. And as the bank will generate roughly 2.5-2.8B EUR per year in net income in the next few years, there’s little doubt the bank’s dividend will increase as the 50% payout ratio will be complemented with special dividends and/or share buybacks.

I have written put options on KBC (which are now all out of the money) and although I have no long position in the bank, I have an indirect long position through KBC Ancora, a holding company with KBC shares as its sole asset.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment