olejx/iStock via Getty Images

I’m out of Sachem’s (NYSE:SACH) common shares on the back of a number of worsening credit market conditions, the looming prospect of a recession, and the recent dividend cut. The odd 7% dividend cut has raised a question of whether management is out of its depth and does not inspire confidence against what is shaping up to be one of the most difficult macroeconomic conditions for real estate since the 2008 global financial crisis.

Firstly, whilst management stated the cut would happen during their prior earnings call, it fundamentally made no sense for the quarterly cash payout to be increased and then immediately cut afterwards. The company’s common shareholders are mainly income investors seeking stability. Unnecessary moves to the downside in terms of payout would rightly shake confidence in the management. A supplemental dividend payout should have been used if management wanted to return excess cash to shareholders. When combined with no set declaration dates and their small-cap status, bulls have been left asking whether the company will be able to fully meander through the current economic malaise.

Don’t Throw The Baby Out With The Bathwater

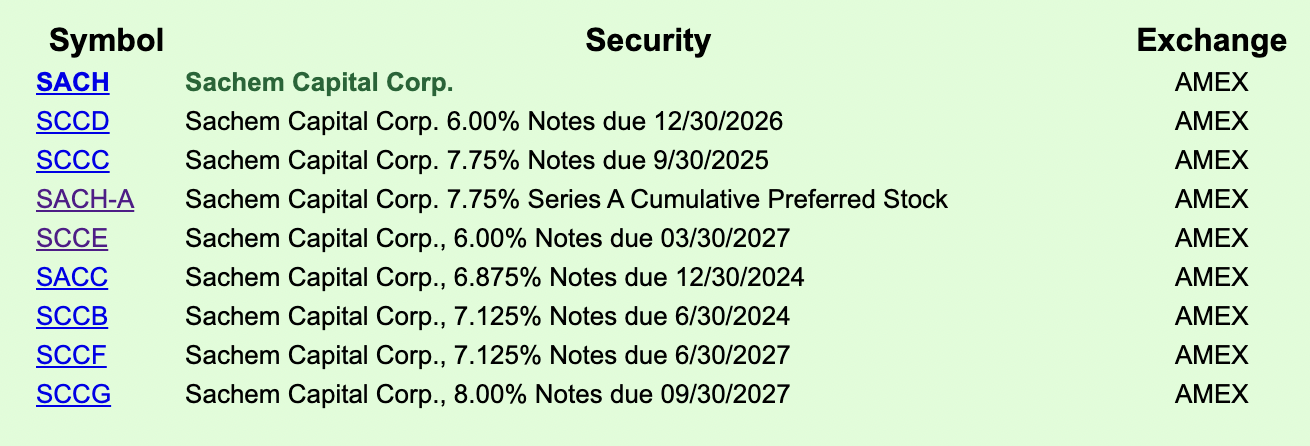

The 6.00% notes due 03/30/2027 (NYSE:SCCE) provide more stability with fixed coupon payments. The baby bond was issued earlier this year in a $50 million debt offering and comes with a $1.50 annual coupon paid quarterly and currently trading for $20 per share. This is a 20% discount to their $25 redemption value and for a current yield of 7.5%. The bonds form part of the company’s financing structure that includes seven other baby bonds and preferred stock.

QuantumOnline

Whilst they provide no voting rights, the bonds rank higher in the capital structure than shares. The interest payments of the bonds are a legal obligation and are payable before taxes. Failure to pay the coupon would mean a default against dividends that can be scrapped anytime the company faces financial difficulty.

Sachem recently reported earnings for its fiscal 2022 third quarter which saw revenue come in at $13.5 million, a 58.8% increase over the year-ago quarter and in line with consensus expectations. This came on the back of an increase in originations driving loan interest income to $11.5 million, up from $6.1 million in the year-ago quarter.

The company recorded $4.1 Million of net income attributable to common shareholders which meant an EPS of $0.11. Further, non-GAAP adjusted EPS of $0.13 came in at a $0.01 beat on consensus estimates. This was on the back of $5.2 million in adjusted earnings and helped support a $7.5 million share buyback program as the company takes defensive measures to protect its financials versus the worsening macro outlook. This will see a reduction of its typical loan terms. The New Haven acquisition is also meant to be a defensive measure to being expertise around all phases of construction in-house. Management thinks this will reduce the risk associated with distressed properties and will enable Sachem to take on larger and more profitable construction loans.

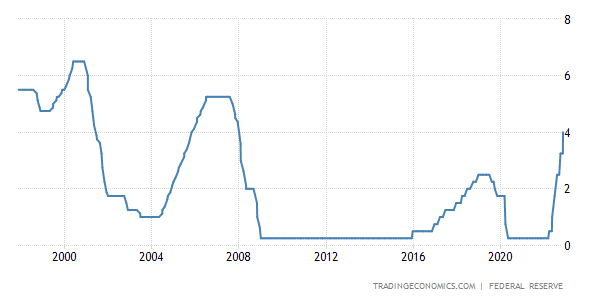

The Macro Environment Has Ramped Up Risks

Real estate continues to get disrupted by consecutive interest rate hikes as high inflation has forced the Fed to take aggressive action. The Fed funds rate now stands at 3.75% to 4%. This is set to be hiked by at least another 50 basis points at the December Federal Open Market Committee meeting.

Trading Economics

What is the impact? A further increase in financing costs for developers and speculators alike. Sachem offers fix and flip, bridge, new construction, and refinancing loans. Hence, the Fed fund rates rising to new highs will apply more pressure on a housing market already pulling back.

Sachem’s loans remain short-term as they are typically provided for between 12 to 36 months. The short-duration loans mitigate the company’s exposure to interest rate movements and allow for a more agile approach to lending in their core markets as the environment changes over the next year.

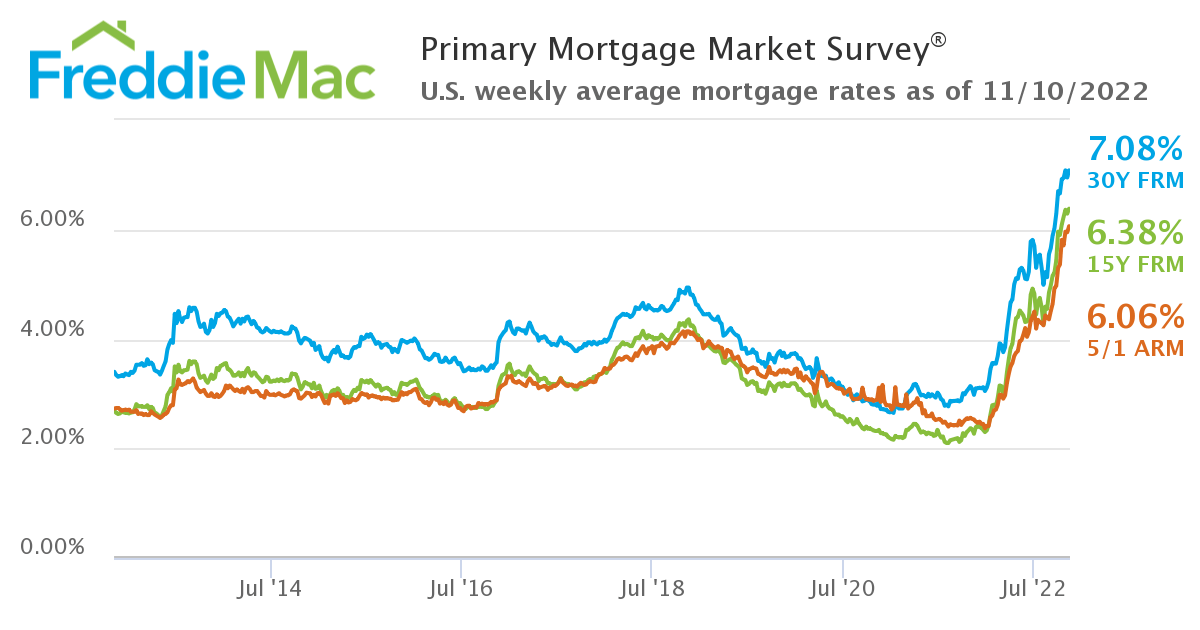

Freddie Mac

Freddie Mac’s primary mortgage market survey has placed the 30-year fixed mortgage rate at 7.08%, significantly up from a year ago when rates hovered just above 3%. This is against Fannie Mae’s Home Purchase Sentiment Index dropping to its lowest level since 2011 when it reached 56.7 in October, its eighth consecutive month-on-month decline. As mortgages become more unaffordable for millions, real estate transactions will slow down materially and push the market into a state of shock.

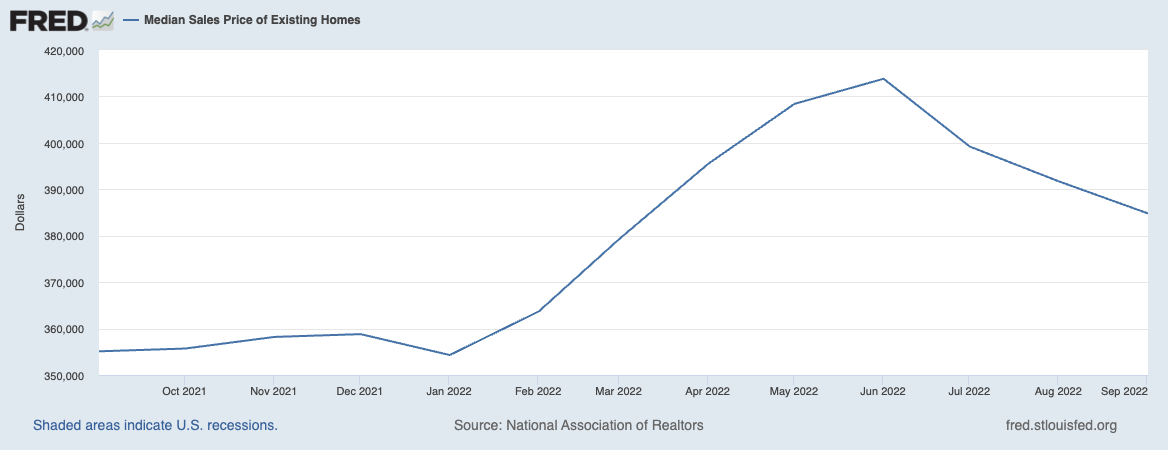

St Louis Fed

The median sales price of existing homes is dropping, down 7% from a recent peak of $413,800 to $384,800. The near-term outlook for the US economy is also poor with a recession expected in 2023. However, with interest rates expected to peak in early 2023 and inflation to fall closer to the Fed target in the second half of the year.

This rare combination of negative economic growth, high inflation, and rising interest rates will further accelerate the trend of collapsing housing sentiment and give further legs to the pullback in house prices. Hence, Sachem could face a high rate of loans in default which could affect its ability to pay a covered dividend on its commons. This drove the move to the baby bond with the commons likely to continue to face near-term headwinds from a capital gains perspective.

Be the first to comment