trait2lumiere

Thesis Summary

The market has rallied very strongly as we approach what could be the last rate hike in this cycle. With the S&P (SPX) hovering around the 4000 point mark, investor confidence has been renewed, but I remain of the opinion that this is still a bear market rally.

Numerous indicators show that the market could still have lower to go, and my macro analysis supports this thesis.

The Fed is doing what it shouldn’t, tightening into a recession, and the market will be feeling this in the next 6 months.

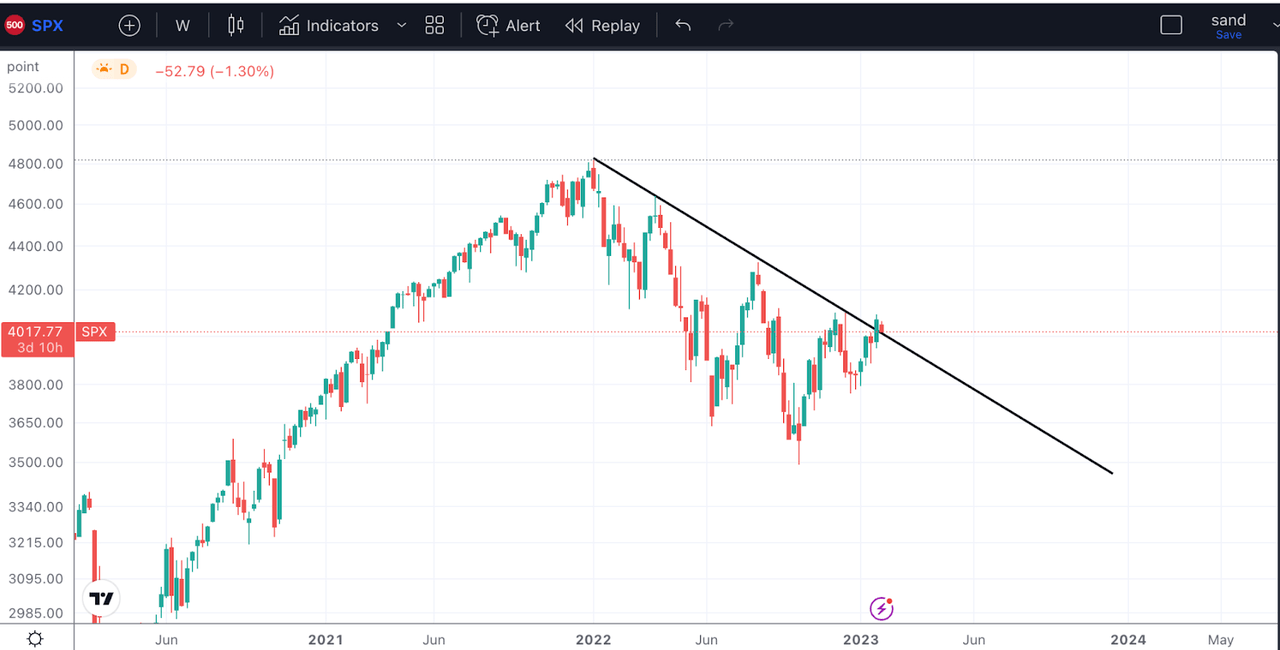

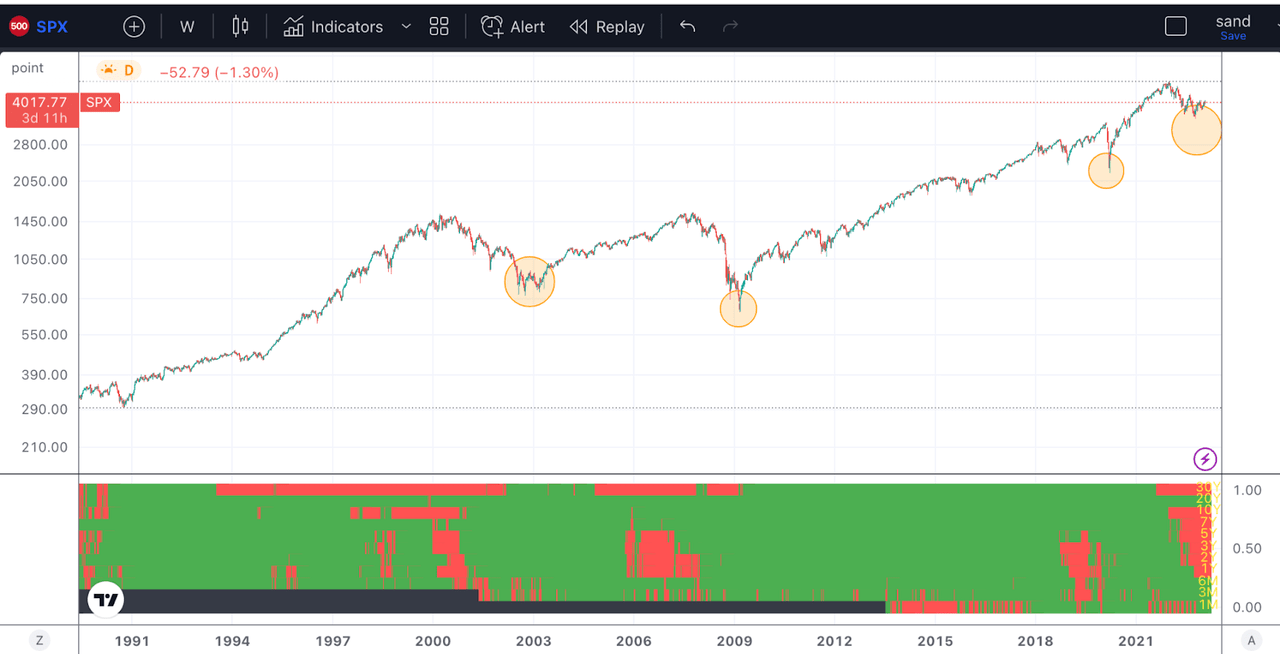

The Bulls Are Back

The bulls are back, and it only took a break above the trendline to reignite their conviction.

SPX (TadingView)

Yes, we closed a weekly candle above 4050 in the SPX, and while this signals a change in momentum, it is far from a guarantee that the bottom is in, something which history will show us.

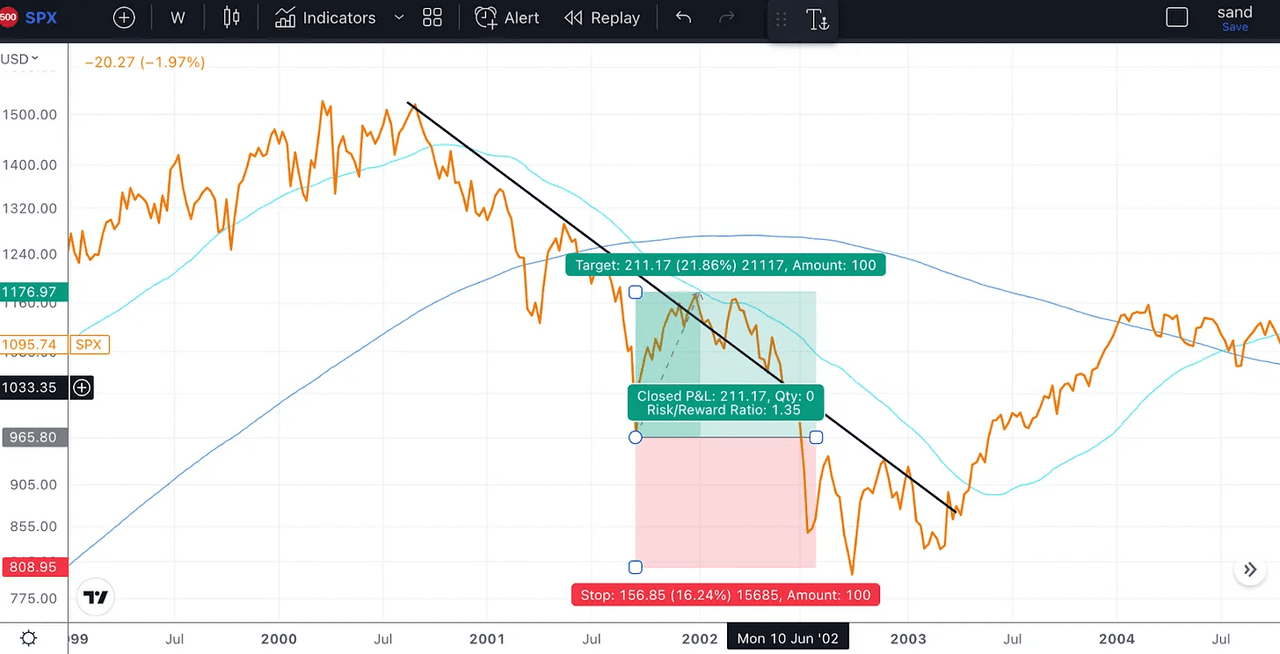

SPX in 2001 (TradingView)

Back in 2001, as the market was coming down from the dot-com bubble, we also got a bullish break off the trendline. The market rallied over 20%, provided us with a fake-out and then went on to lose another 30% before a bottom was found. All this, may I add, as the Fed was cutting rates.

Let’s go ahead and look at another couple of indicators that would suggest that the bottom is likely not in.

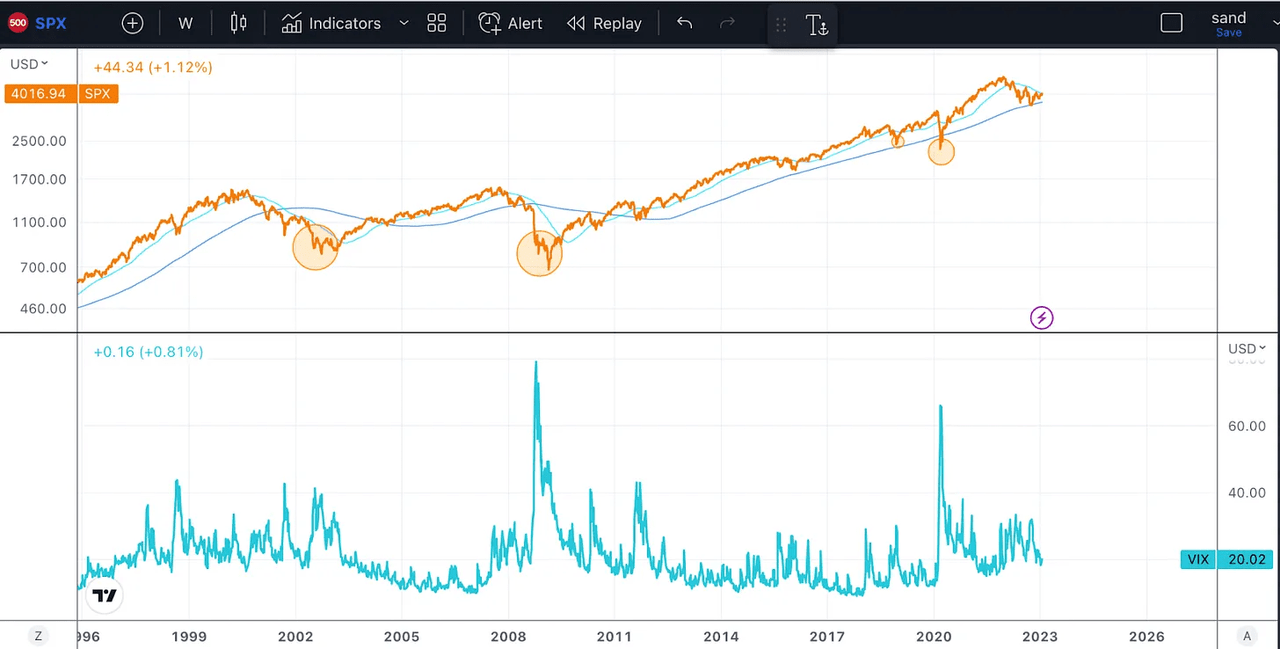

SPX and VIX (TradingView)

First up, here’s a long-term view of the SPX and the VIX index. We can clearly see that, in the past ,market bottoms have coincided with periods of high volatility, shown by VIX readings at least above 40 points.

This did not happen when the SPX fell towards 3500 points.

On another more fundamental note, since 1993, we haven’t seen a market bottom take place with such an inverted yield curve.

SPX and Yield Inversion (TradingView)

The indicator below the chart shows the different inversions in the yield curve. In the past few market bottoms, it has taken at least a few rate hikes and a normalization of the curve before a solid bottom was found.

If investing was as easy as looking at one line on the chart, analysts would not be needed. Technical indicators are useful tools but must support a more comprehensive macroeconomic framework.

My own macro research suggests we are in for a rough 2023.

Macro Outlook

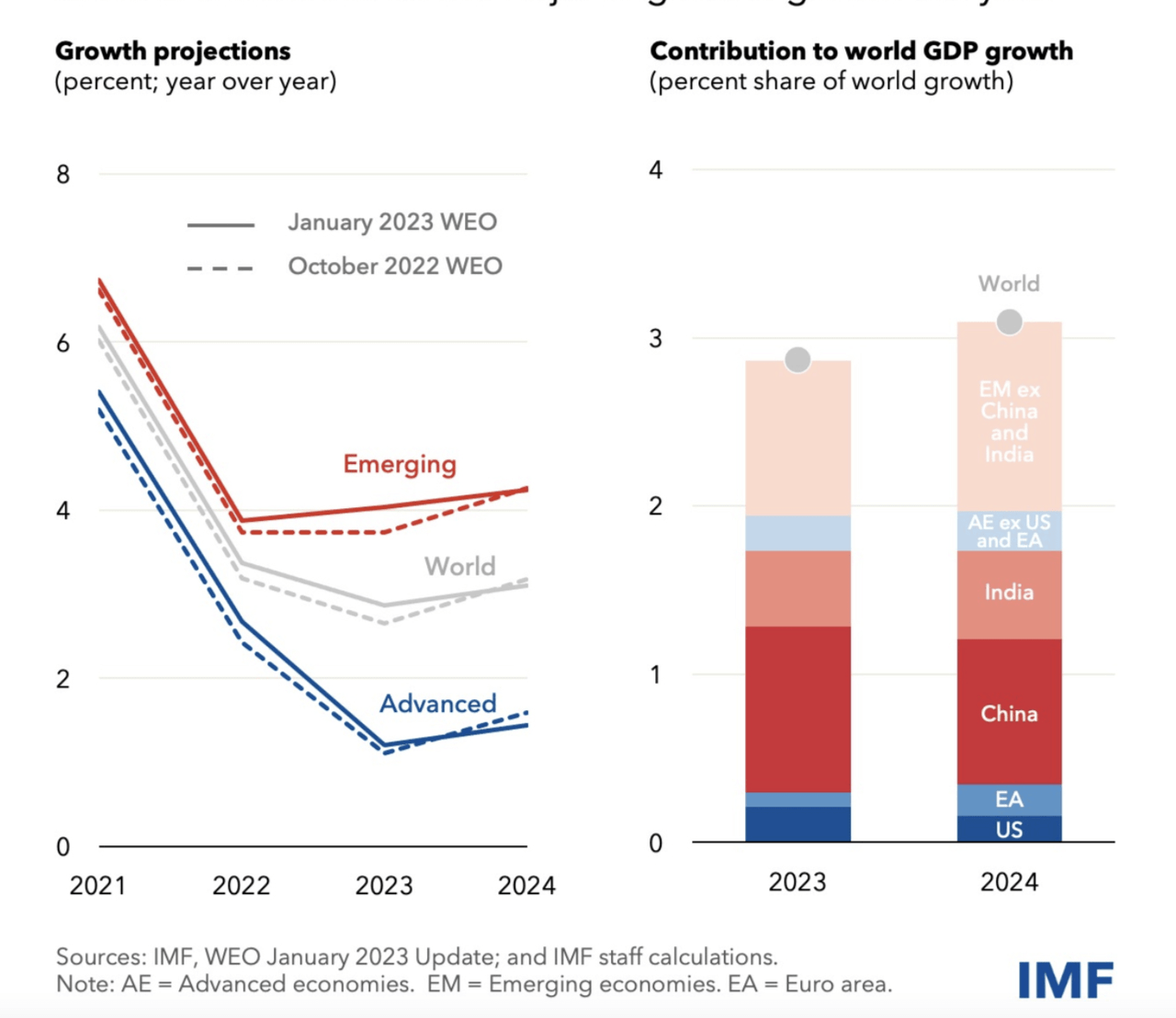

This week is going to be chock full of economic data both domestically and abroad. Just yesterday, the IMF revised its growth outlook for the world economy.

Growth Outlook (IMF)

Advanced economies will be laggards, while China and India will be the motors of growth in 2024.

Inflation outlook (IMF)

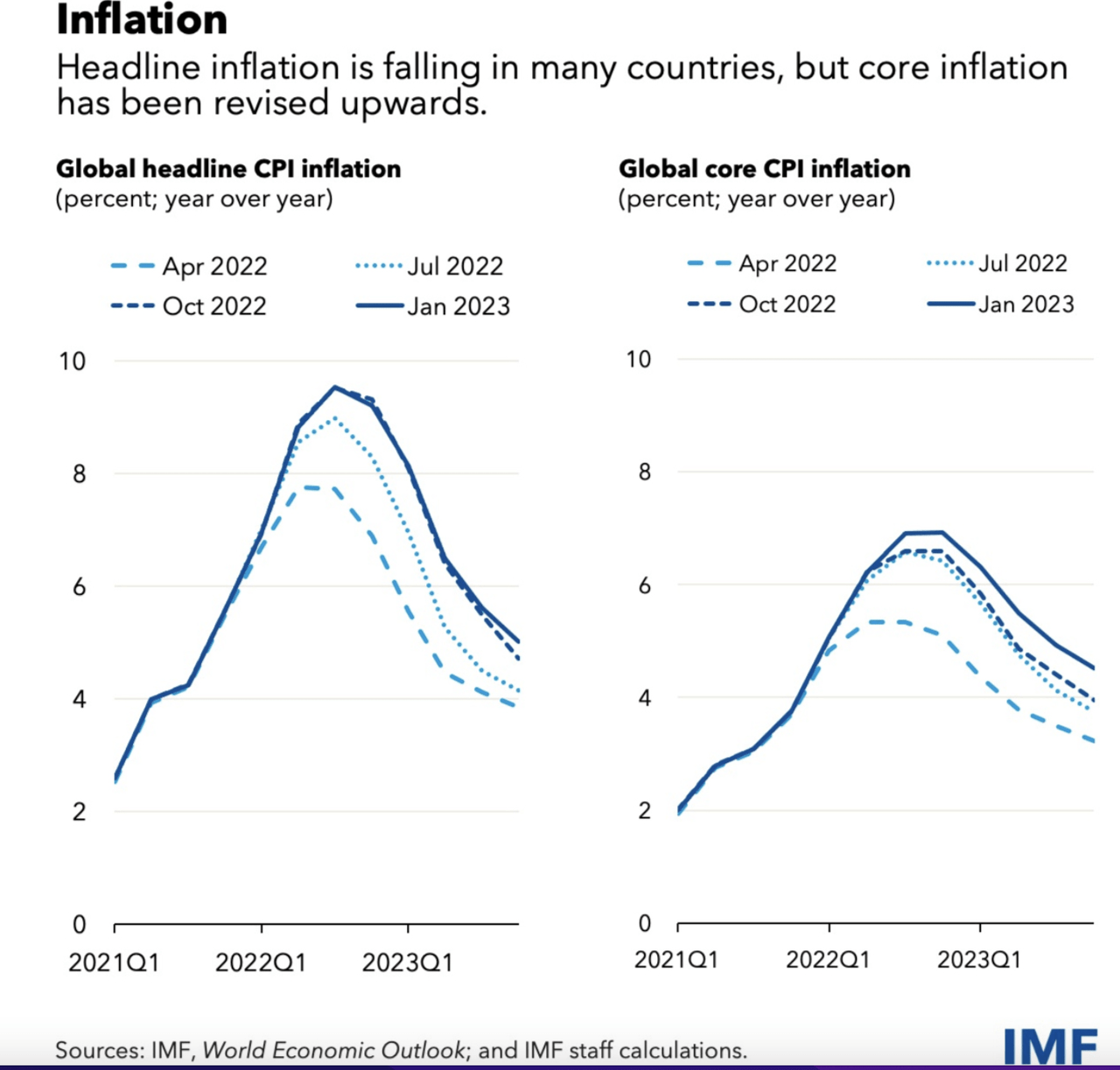

Headline inflation was revised downward, while the core inflation outlook was increased. While we have clearly disinflationary data coming out of the US, China’s reopening could cause upwards pressure on inflation. This pressure could be particularly felt in commodities.

Given the above data, it’s understandable that the Fed is still wary about pivoting too soon, even in the face of a slowing down US economy.

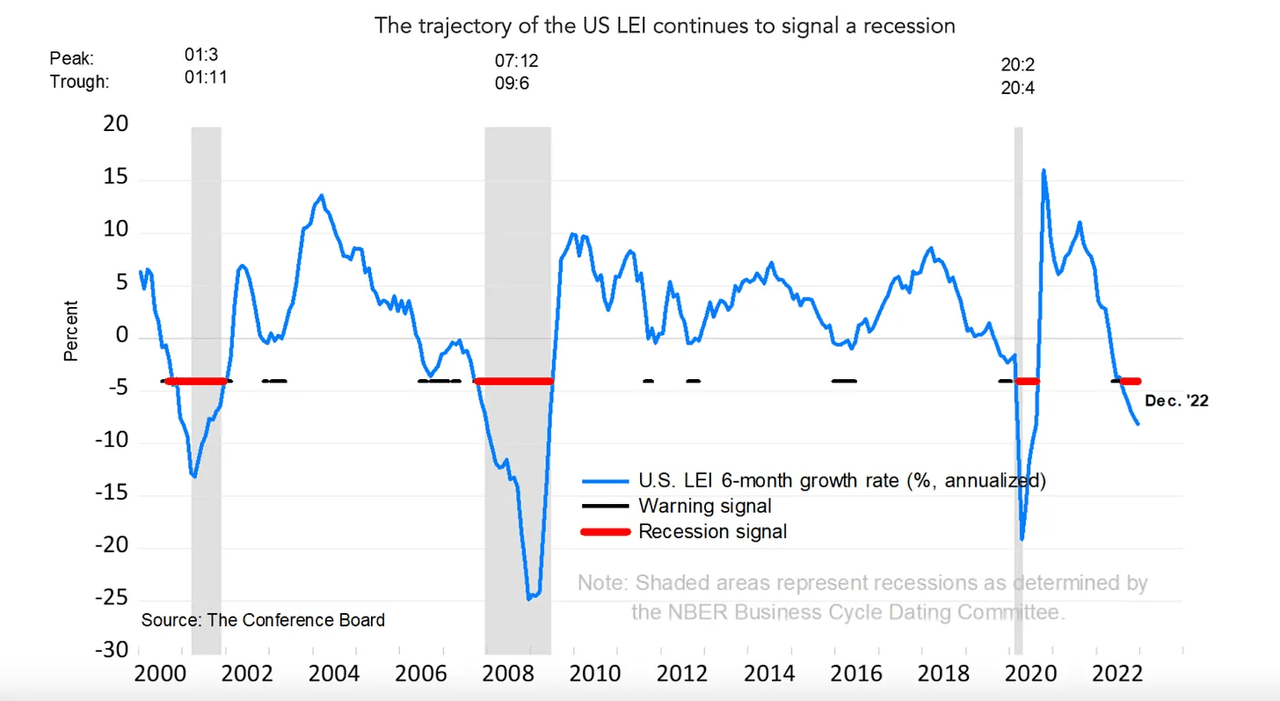

US LEI (The conference board)

The Leading Economic Indicator has flashed us a clear recession signal. A signal which has accurately predicted the past 3 recessions.

While employment is strong, it’s hard to see how the US could fall into a severe recession. But this may change as data comes out in the next few months.

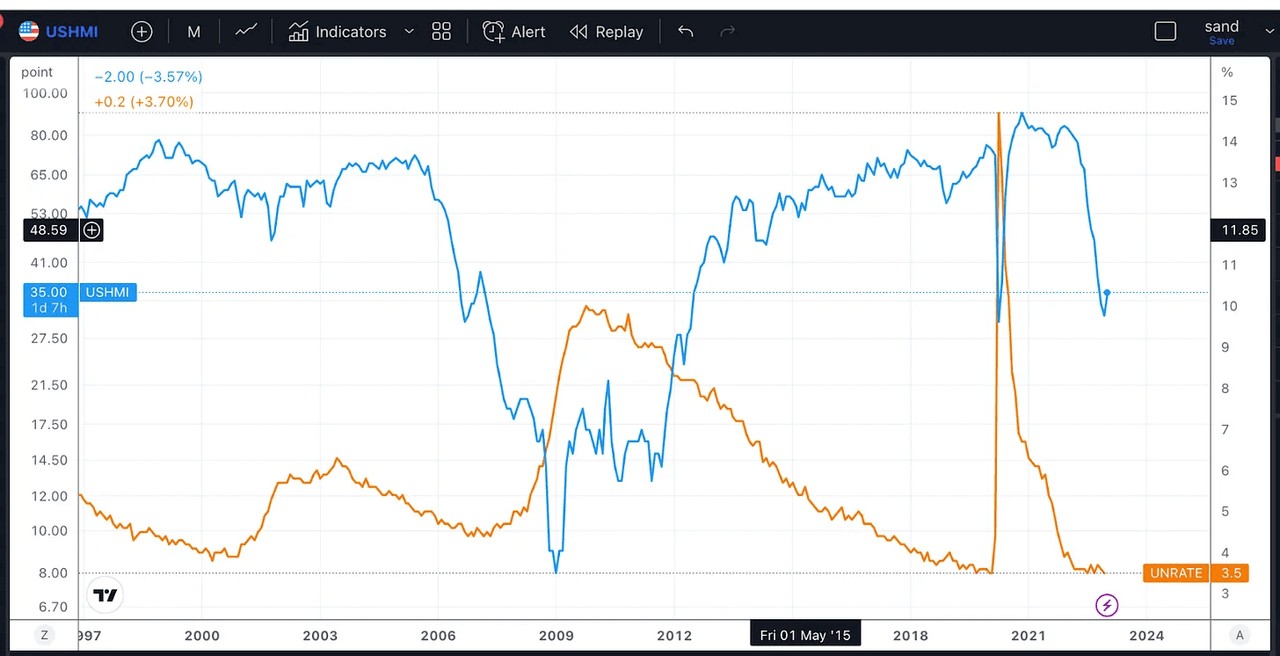

USHMI and Unemployment (TradingView)

The chart above shows the US Housing Manufacturing Index and the unemployment rate. In the past, the USHMI has served as a strong leading indicator for employment. We have started to see weakness in housing in the last 3 months, which means we could likely see weakness in employment in the next 3.

Closing Remarks

With a US recession clearly on the way, and a Federal Reserve hell-bent on not giving the market what it wants, I’d be surprised if we didn’t see some weakness in equities in the next 6 months.

The way I see it, the market can’t win at this point, since it already seems to be pricing in both a soft-landing and rate cuts this year.

If economic data does stay strong, then we will soon realize no rate cuts are coming this year. In other words, even if the Fed doesn’t tighten, it will remain tighter than people expect.

If instead, we get a recession, as it seems likely, this might justify rate cuts, but it might still not save equities from a significant drawdown. Furthermore, this could very likely lead to another bout of inflation and perhaps even the dreaded stagflation.

Be the first to comment